- Healthcare Services

- India Malaria Diagnostics Market

India Malaria Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

India Malaria Diagnostics Market by Product Type (Instruments, Kits and Reagents, Rapid Diagnostic Test (RDT) Kits, PCR Reagents and Assay Kits, Others), Technology (Microscopy, Rapid Diagnostic Tests (RDTs), Polymerase Chain Reaction (PCR), Serology-Based Tests, Others), End-user (Hospitals, Specialty Clinics, Diagnostic Laboratories, Research Institutes and Academic Laboratories, Others), 2026-2033

India Malaria Diagnostics Market Size and Trend Analysis

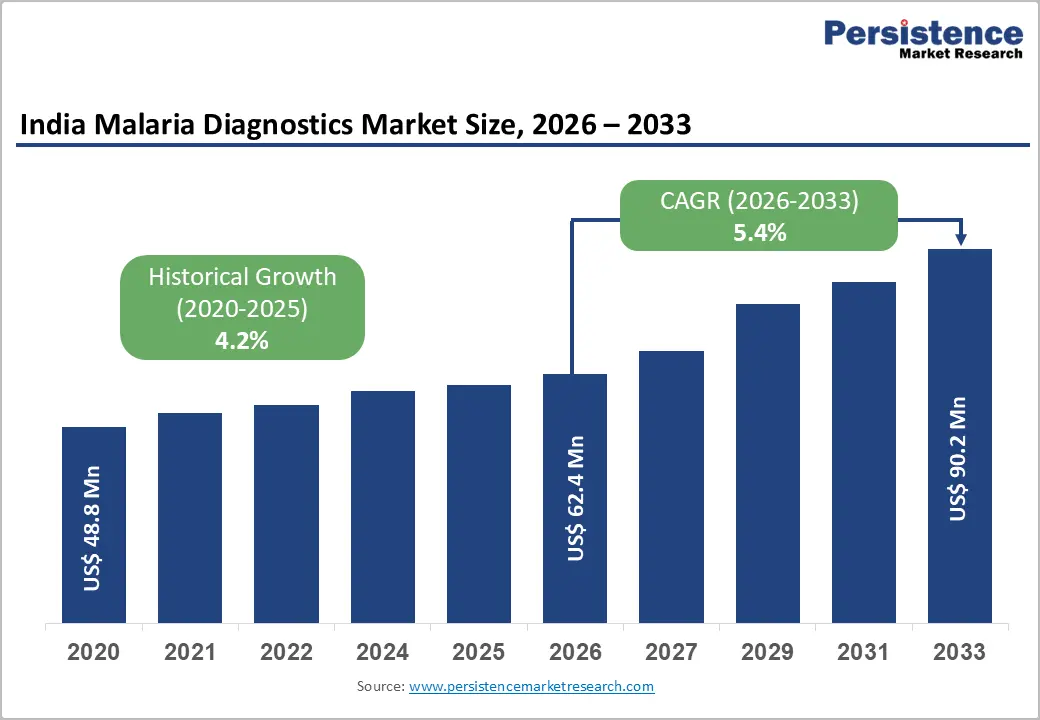

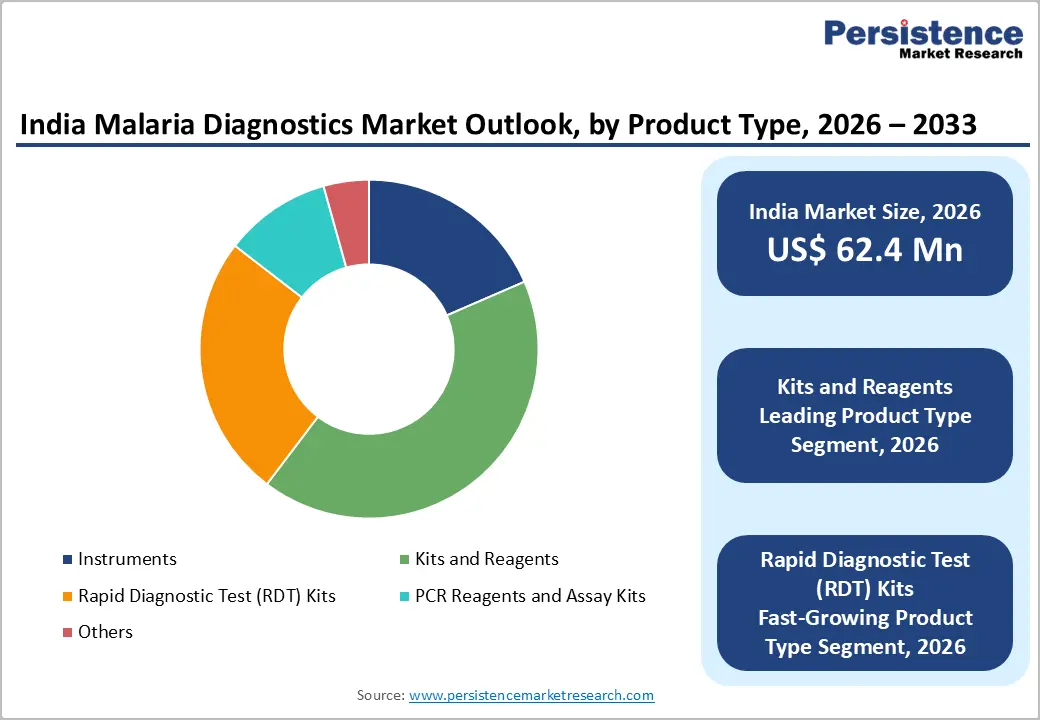

India malaria diagnostics market size is expected to be valued at US$ 62.4 million in 2026 and projected to reach US$ 90.2 million by 2033, growing at a CAGR of 5.4% between 2026 and 2033. It is experiencing sustained growth driven by the government's ambitious National Framework for Malaria Elimination (NFME) 2016-2030, targeting malaria elimination by 2030, which mandates universal case detection through quality-assured diagnostic testing as the cornerstone of the elimination strategy.

According to the World Health Organization (WHO) World Malaria Report 2023, India accounted for approximately 66% of all malaria cases in the South-East Asia Region in 2022, representing 5.5 million confirmed cases. This epidemiological reality, combined with scaling government procurement of Rapid Diagnostic Tests (RDTs) under Ayushman Bharat health coverage programs and the expanding private diagnostic laboratory sector, is sustaining above-average value growth through 2033.

Key Industry Highlights:

- Leading Diagnostic Technology - RDTs (52% Share): Rapid Diagnostic Tests command 52% of India's malaria diagnostics technology share in 2025, driven by NVBDCP's 75 million+ annual RDT procurement, ASHA worker community-level deployment, and WHO prequalification standards ensuring diagnostic accuracy in field conditions.

- Fast-Growing Technology - PCR-Based Diagnostics: PCR-based malaria diagnostics are the fastest-growing technology segment, driven by India's malaria elimination phase requiring zero-miss surveillance, ICMR's NIMR laboratory network expansion, and sub-microscopic parasitemia detection needs in low-transmission settings.

- Dominant Segment - Kits and Reagents (~65% Share): Kits and Reagents lead with 65% share in 2025, anchored by 75M+ annual government RDT procurement under NVBDCP and growing private laboratory demand for malaria fever panel testing kits from chains like Dr. Lal PathLabs and SRL Diagnostics.

- Fastest Growing Segment - RDT Kits: RDT Kits are the fastest-growing product type, driven by next-generation WHO-prequalified P. vivax/P. falciparum dual-species kits improving sensitivity, ASHA worker scale-up in tribal districts, and Ayushman Bharat PMJAY reimbursement expanding private sector malaria testing access.

- Key Opportunity - Malaria Elimination Surveillance PCR Scale-up: India's 2030 elimination target mandates increasingly sensitive PCR-based surveillance as case counts decline, creating a structurally growing, high-value diagnostic market opportunity for molecular malaria testing platforms from Mylab Discovery Solutions and Bio-Rad.

Market Dynamics

Drivers - National Malaria Elimination Policy Mandating Universal Quality Diagnostic Testing

India's National Framework for Malaria Elimination (NFME) 2016-2030 and the National Vector Borne Disease Control Programme (NVBDCP) jointly mandate that every suspected malaria case must receive a parasitological confirmation through either microscopy or a WHO-prequalified Rapid Diagnostic Test (RDT) before treatment a policy that has structurally transformed India's malaria diagnostics market from presumptive to test-confirmed case management.

The Ministry of Health and Family Welfare (MoHFW) distributes free RDTs through the public health system, procuring over 75 million RDTs annually under national disease control programs, according to program reports. This government procurement volume creates a stable, high-volume, non-discretionary demand base for RDT kit manufacturers including J. Mitra & Co. Pvt. Ltd., Premier Medical Corporation, and SD Biosensor Healthcare Pvt. Ltd., sustaining consistent market growth independent of private sector fluctuations.

Expanding Private Diagnostic Laboratory Sector and Health Insurance Coverage

The rapid expansion of India's private diagnostic laboratory sector is creating a growing incremental revenue stream for malaria diagnostics manufacturers operating outside government procurement channels. According to FICCI and CII healthcare sector reports, India's diagnostics industry has grown at approximately 15% annually post-pandemic, with national laboratory chains including Dr. Lal PathLabs, SRL Diagnostics, and Thyrocare expanding fever diagnostic panel offerings that routinely include malaria testing.

The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PMJAY) scheme covering over 500 million beneficiaries, has expanded reimbursement for diagnostic testing including malaria diagnosis across empanelled hospitals, driving increased utilization of PCR-based and RDT malaria testing in the semi-urban and rural private healthcare segments that were previously cash-limited in diagnostic uptake.

Restraints - Heavy Dependence on Subsidized Government Procurement, Suppressing Commercial Pricing

India's malaria diagnostics market is heavily dominated by government procurement at subsidized or tendered prices, which creates significant downward pricing pressure on commercial market segments. The NVBDCP procures RDTs at tendered rates often 60-70% below international commercial prices, creating a distorted baseline that depresses overall average selling prices across the market. For private sector diagnostic manufacturers seeking to expand commercial revenues beyond government contracts, competing against heavily subsidized public sector supply chains is a persistent commercial barrier that limits revenue growth and margin realization, particularly for domestic manufacturers, including Tulip Diagnostics and MicroGene Diagnostic Systems.

Inadequate Diagnostic Infrastructure and Skilled Personnel in High-Burden Remote Areas

Despite policy mandates for universal parasitological diagnosis, significant implementation gaps persist in high-malaria-burden remote tribal and forested areas across Odisha, Chhattisgarh, Jharkhand, and Northeast India, where laboratory infrastructure and trained microscopy technicians remain scarce. The WHO World Malaria Report 2023 notes that while RDT deployment has expanded access to diagnosis, quality assurance challenges,s including cold chain maintenance for antigen-based RDTs in tropical field conditions can compromise test performance, leading to diagnostic gaps. These infrastructure limitations suppress test volumes in geographies with the highest disease burden, constraining the market's full potential.

Opportunities - Rapid Diagnostic Test (RDT) Kits: Fastest-Growing Segment Driven by LMIC Deployment Scale-up

Rapid Diagnostic Test (RDT) Kits represent the India Malaria Diagnostics market's fastest-growing product segment, projected to deliver the highest CAGR through 2033, driven by continued government scale-up under the NFME and expanding WHO-prequalified product adoption. RDTs offer critical operational advantages in resource-limited settings no need for electricity, laboratory equipment, or skilled technicians, making them uniquely suited for deployment by ASHA (Accredited Social Health Activist) workers and front-line health workers conducting malaria case detection in remote communities under India's NVBDCP framework.

The WHO's Malaria Rapid Diagnostic Test Product Testing program reports that next-generation RDTs with improved sensitivity for Plasmodium vivax and P. falciparum mixed-species detection are advancing through prequalification, creating product upgrade cycles that generate replacement procurement demand. Manufacturers, including Access Bio, Inc., J. Mitra & Co., and SD Biosensor, are well-positioned to capture this high-volume, recurring demand.

PCR-Based Malaria Diagnostics Expansion in Tertiary Hospitals and Reference Laboratories

The expansion of molecular PCR-based malaria diagnostics represents a high-value growth opportunity for India malaria diagnostics market, particularly within the tertiary hospital and reference laboratory end-user segments. PCR-based malaria detection offers superior sensitivity for low-density parasitemia, species differentiation (critical for distinguishing P. vivax from P. falciparum for appropriate treatment), and detection of mixed infections missed by both microscopy and RDTs. The Indian Council of Medical Research (ICMR) has actively promoted molecular diagnostic capacity building across its network of National Institute of Malaria Research (NIMR) laboratories.

As the Indian government's malaria elimination phase requires confirmation of all cases and active surveillance in low-transmission settings where parasitemia may be sub-microscopic, PCR demand will structurally grow. Companies, including Mylab Discovery Solutions Pvt. Ltd. and Bio-Rad Laboratories, Inc. are expanding PCR-based malaria diagnostic product offerings tailored for Indian reference laboratory settings.

Category-wise Analysis

Product Type Insights

The kits and reagents segment leads India malaria diagnostics market by product type, commanding approximately 65% of the total share in 2026. This dominance reflects the fundamental consumption model of malaria diagnostics in India, where every diagnostic test requires fresh RDT kits, microscopy staining reagents, or PCR assay consumables, generating high-frequency, recurring procurement across both government and private sector channels. The NVBDCP's annual procurement of over 75 million RDTs alone constitutes a massive kit and reagents revenue base sustaining market leadership. Additionally, the expanding private diagnostic laboratory sector's malaria fever panel deployments consume significant volumes of malaria RDT kits and blood film staining reagents. Rapid Diagnostic Test (RDT) Kits are the fastest-growing product subtype, driven by government scale-up and ASHA worker deployment programs across India's high-burden tribal districts under the High Burden to High Impact (HBHI) initiative.

Technology Insights

The rapid diagnostic tests (RDTs) technology segment is leading, accounting for approximately 52% of the total share in 2026. RDTs have achieved technology leadership through their operational practicality in India's challenging diagnostic delivery context, enabling test-and-treat malaria management at the community level without requiring electricity, microscopes, or laboratory infrastructure.

The WHO's prequalification program ensures that RDTs deployed in India meet the minimum sensitivity of 95% for P. falciparum at 200 parasites/microlitre of blood, a validated performance standard endorsed by the MoHFW for national program procurement. Microscopy remains the second-largest technology segment, valued for its cost-effectiveness and species quantification capability in reference laboratories. PCR is the fastest-growing technology, driven by malaria elimination phase surveillance requirements and ICMR laboratory network capacity building.

End-user Insights

Diagnostic laboratories represent the leading end-user segment, commanding approximately 38% revenue share in 2026. Both government public health laboratories under the NVBDCP network and rapidly expanding private diagnostic laboratory chains drive this segment's leadership. Government district and sub-district malaria testing laboratories process the highest test volumes nationally, while private laboratory chains, including Dr. Lal PathLabs and SRL Diagnostics, expand malaria testing as part of comprehensive fever diagnostic panels.

Hospitals are the second-largest end-user segment, integrating malaria diagnostics into fever workup protocols in both government tertiary hospitals and private hospital networks. Research Institutes and Academic Laboratories, particularly ICMR's National Institute of Malaria Research (NIMR) and medical college-affiliated laboratories, are the fastest-growing end-user segment, driven by malaria elimination research programs and PCR surveillance laboratory expansion.

Regional-wise Insights

East India Malaria Diagnostics Market Trends

East India is likely to account for approximately 38.6% in 2026 and remains the largest regional market due to the high malaria burden across Odisha, Assam, Jharkhand, West Bengal, and the northeastern states. Favorable climatic conditions, dense forest cover, and large tribal populations contribute to sustained transmission and extensive screening requirements.

Government initiatives such as active case detection and the DAMaN program have significantly increased the use of rapid diagnostic tests and microscopy in remote districts. In addition, public health authorities are gradually adopting PCR and other molecular diagnostic tools to detect asymptomatic and low-parasite infections, supporting India’s malaria elimination objective and strengthening surveillance capabilities across endemic zones.

North India Malaria Diagnostics Market Trends

North India is likely to represent nearly 16.9% share in 2026. Compared with eastern and central regions, malaria incidence is lower; however, states such as Punjab, Haryana, Uttar Pradesh, and Uttarakhand continue to invest in surveillance to prevent disease resurgence. The region is increasingly adopting molecular diagnostics, including nested PCR and real-time PCR, to identify submicroscopic infections that are frequently missed by microscopy and rapid tests. Expansion of integrated disease surveillance systems, digitization of reporting, and improved inclusion of private laboratory data are enhancing outbreak monitoring and creating demand for high-sensitivity diagnostic technologies in low-transmission settings.

West India Malaria Diagnostics Market Trends

West India held an estimated 22.8% share in 2026, driven by Maharashtra, Gujarat, Rajasthan, and Goa. The region benefits from a well-developed healthcare infrastructure, strong public health programs, and a dense network of private diagnostic laboratories. Government-funded microscopy services and large-scale deployment of rapid diagnostic tests continue to support malaria screening in both urban and tribal districts. At the same time, reference laboratories are expanding the use of PCR-based diagnostics for accurate species identification and epidemiological surveillance. Continued investments in vector control and early diagnosis are expected to sustain steady market growth across the region.

Competitive Landscape

India malaria diagnostics market is moderately fragmented, with a mix of domestic manufacturers including J. Mitra & Co. Pvt. Ltd., Premier Medical Corporation, Tulip Diagnostics, MicroGene Diagnostic Systems, and Mylab Discovery Solutions competing alongside global IVD companies operating through Indian subsidiaries or distributors including Abbott, Bio-Rad Laboratories, bioMérieux, and Meridian Bioscience.

Key competitive differentiators include WHO prequalification status (critical for government tender eligibility), ICMR and CDSCO regulatory approvals, government supply chain relationships, product sensitivity/specificity performance, and cold chain management capabilities. Domestic manufacturers benefit from lower production costs and established government procurement relationships, while global players compete on premium product performance in the private and institutional segments.

Key Developments:

- In April 2026, the Global Health Innovative Technology Fund allocated approximately USD 2 million (JPY 330 million) to support multi-country clinical trials in Kenya, Senegal, and India for fosravuconazole, highlighting India’s growing role in neglected tropical disease research and strengthening laboratory and molecular diagnostic capabilities that also support broader infectious disease testing, including malaria diagnostics.

- In September 2025, the Indian Council of Medical Research introduced AdFalciVax, India’s first indigenous multi-stage malaria vaccine, marking a significant advancement in domestic malaria control efforts and expected to strengthen demand for diagnostic testing to support screening, surveillance, and monitoring as immunization programs expand.

- In June 2023, GenWorks Health launched iScreen rapid in-vitro diagnostic test kits for malaria and dengue, expanding access to affordable point-of-care testing and strengthening the availability of rapid diagnostic solutions across India’s hospitals, clinics, and rural healthcare settings.

Global India Malaria Diagnostics Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 48.8 Mn |

|

Current Market Value (2026) |

US$ 62.4 Mn |

|

Projected Market Value (2033) |

US$ 90.2 Mn |

|

CAGR (2026-2033) |

5.4% |

|

Dominant Technology |

Microscopy, 53.8% share |

|

Top-ranking Product Type |

Kits and Reagents, 64.7% |

|

Incremental Opportunity |

US$ 27.8 Mn |

Companies Covered in India Malaria Diagnostics Market

- Abbott

- Bio-Rad Laboratories, Inc.

- Access Bio, Inc.

- J. Mitra & Co. Pvt. Ltd.

- Premier Medical Corporation Private Limited

- Tulip Diagnostics (P) Ltd.

- SD Biosensor Healthcare Pvt. Ltd.

- MicroGene Diagnostic Systems (P) Ltd.

- Meridian Bioscience, Inc.

- Trivitron Healthcare

- Olympus Medical Systems India Pvt. Ltd.

- Sysmex India Pvt. Ltd.

- bioMérieux India Pvt. Ltd.

- Mylab Discovery Solutions Pvt. Ltd.

- HLL Lifecare Limited

- Others

Frequently Asked Questions

India malaria diagnostics market is projected to reach US$ 62.4 million in 2026, having grown at a historical CAGR of 4.2% during 2020-2025. The market is forecast to expand to US$ 90.2 million by 2033, driven by government NVBDCP RDT procurement scale-up, Ayushman Bharat-facilitated private diagnostic growth, and expanding PCR-based surveillance testing under India's 2030 Malaria Elimination Framework.

Rising government-led malaria elimination programs, increasing deployment of rapid diagnostic tests in endemic rural and tribal areas, and growing awareness of early and accurate diagnosis are the primary demand drivers in India malaria diagnostics market.

India malaria diagnostics market is poised to witness a CAGR of 5.4%% from 2026 to 2033.

The key growth opportunity lies in expanding molecular and AI-enabled diagnostic solutions for surveillance and detection in hard-to-reach and high-burden regions under India’s malaria elimination initiatives.

Leading companies include J. Mitra & Co. Pvt. Ltd., SD Biosensor Healthcare Pvt. Ltd., Premier Medical Corporation Pvt. Ltd., Tulip Diagnostics (P) Ltd., HLL Lifecare Limited, Mylab Discovery Solutions Pvt. Ltd., Trivitron Healthcare, bioMérieux India Pvt. Ltd., Abbott India, Bio-Rad Laboratories Inc., Meridian Bioscience Inc., MicroGene Diagnostic Systems (P) Ltd., Transasia Bio-Medicals Ltd., and Reckon Diagnostics Pvt. Ltd., among others. These players compete through WHO prequalification status, CDSCO regulatory approvals, government tender relationships, diagnostic sensitivity/specificity performance, and India-specific cold chain supply chain management capabilities.