- Chipsets & Processors

- True Wireless Stereo Earbuds Market

True Wireless Stereo Earbuds Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

True Wireless Stereo Earbuds Market by Product Type (Standard TWS Earbuds, Noise Cancelling (ANC) TWS Earbuds, Sports/Fitness TWS Earbuds, Gaming/Low-Latency TWS Earbuds, Smart/AI-Enabled TWS Earbuds), Price Band (Below US$ 100, US$ 101 to 200, Over US$ 200), Distribution Channel (Online Retail/E-commerce, Offline Retail (electronics stores, supermarkets, specialty stores), Direct-to-Consumer (DTC)/Brand Stores), and Regional Analysis for 2026 to 2033

True Wireless Stereo Earbuds Market Trends & Analysis

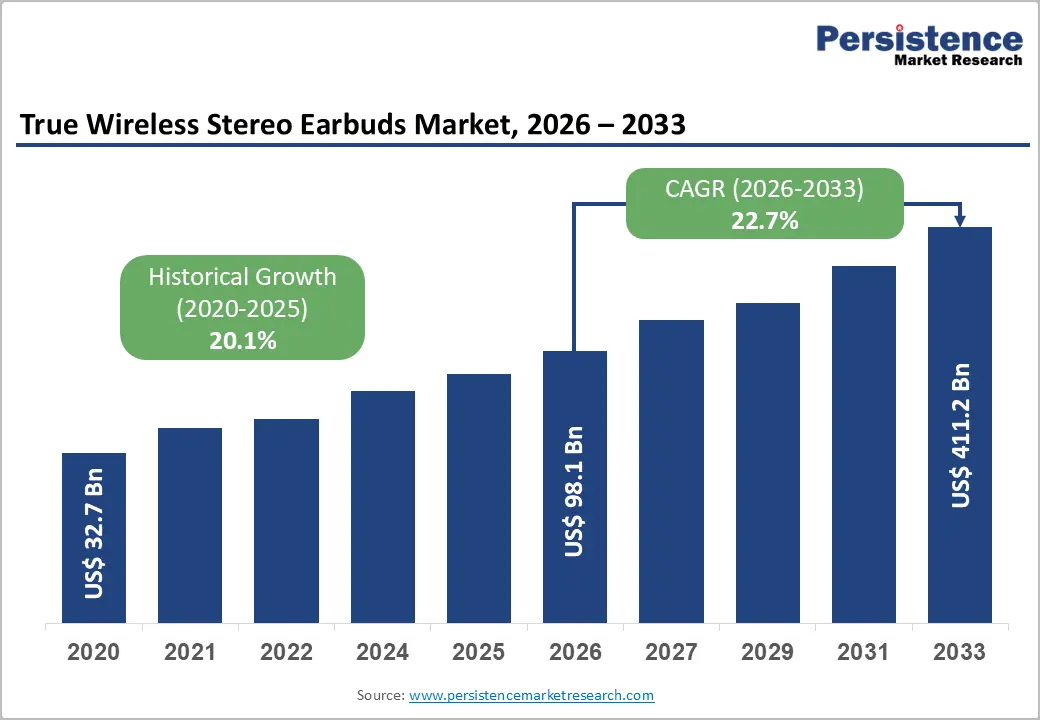

The global true wireless stereo (TWS) earbuds market is projected at US$ 98.1 Bn in 2026 and is expected to reach US$ 411.2 Bn by 2033, growing at a strong CAGR of 22.7% from 2026 to 2033. Global TWS shipments rose 18% YoY in Q1 2025, reflecting sustained demand momentum driven by smartphone ecosystem expansion, Bluetooth 5.3 adoption, and rapid AI-enabled feature upgrades. Asia Pacific remains the key growth hub, accounting for 39% of global demand, underscoring strong regional consumer electronics adoption.

The growth is further supported by a young, tech-savvy user base, with 62% of consumers aged 18-34, along with the widespread adoption of ANC and spatial audio features. When combined with the increasing e-commerce penetration in emerging markets and the ongoing premiumization of products, these elements consistently uphold the industry's long-term growth path and its historical 20.1% CAGR from 2020 to 2026.

Key Highlights Summary

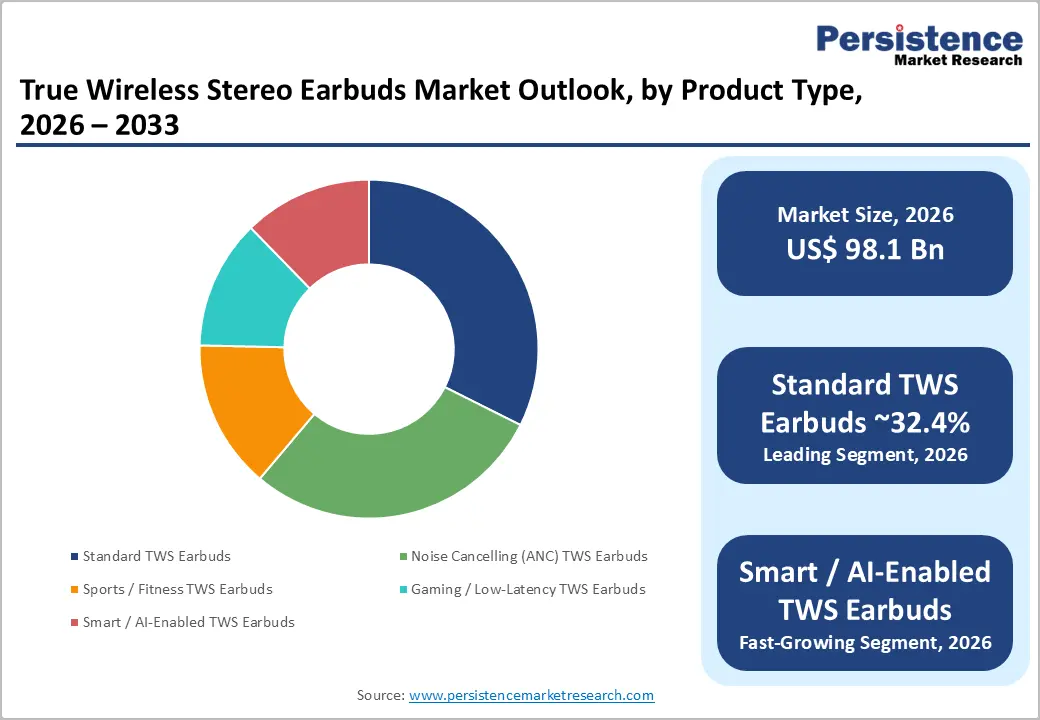

- Leading Product Type: Standard TWS Earbuds lead at 32.4% share; Smart/AI-Enabled TWS grows fastest at 30.2% CAGR, driven by on-device AI, adaptive ANC, biometric sensing, and real-time translation integration across premium TWS platforms.

- Leading Price Band: US$ 101-200 leads at 50.3% share (~US$ 49.4 Bn); Below US$ 100 grows fastest at 30.8% CAGR, driven by Xiaomi, boAt, and Realme delivering ANC features at sub-US$ 50 price points across Asia Pacific.

- Leading Channel: Online Retail/E-commerce leads at 58.6% share (~US$ 57.5 Bn); DTC/Brand Stores grow fastest at 27.5% CAGR, driven by Apple Store, Samsung Experience, and brand-owned e-commerce platform investment acceleration globally.

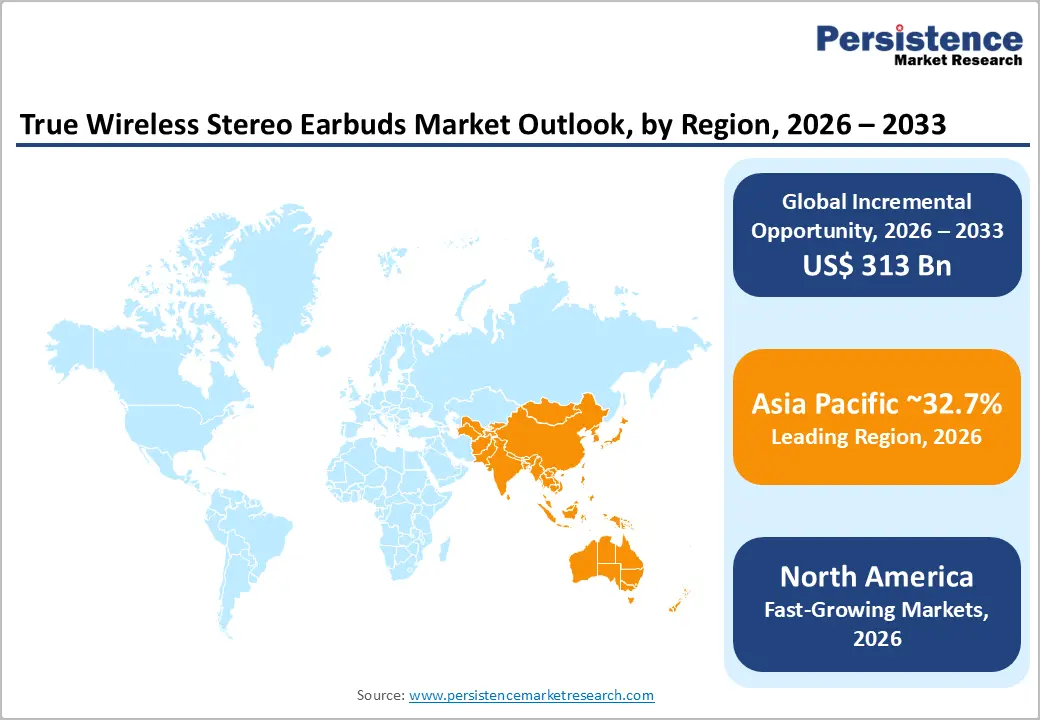

- Regional Leader: Asia Pacific leads at ~39% share and 25.3% CAGR; China holds US$ 26.8 Bn and India US$ 9.1 Bn in 2026, anchored by Xiaomi's 63% YoY shipment growth and boAt's India youth market dominance.

- Strategic Milestone: Apple's FDA-cleared AirPods Pro 2 hearing aid mode (September 2024) and Xiaomi's 11.5% global share capture in Q1 2025 signal the TWS market's dual-track premium health-sensing and mass-market volume expansion trajectory in the forecast period.

Market Dynamics Analysis

Drivers - Smartphone Ecosystem Proliferation and Removal of 3.5mm Audio Jacks Driving TWS Adoption

The global smartphone installed base surpassed 6.9 billion active units in 2024 (GSMA Intelligence), with the gradual removal of 3.5mm headphone jacks, first popularized by Apple’s iPhone 7 in 2016 and now present in 72% of Android flagships, systematically shifting users from wired headphones to TWS earbuds across all major demographics worldwide. Apple alone shipped over 115 million TWS units in 2024, holding a 23% global share in Q1 2025 (Canalys), underscoring the scale of smartphone-led demand conversion in consumer electronics retail.

The GSMA projects smartphone connections to reach 7.7 billion by 2030, with ongoing feature-phone to smartphone upgrades in India, Southeast Asia, and Sub-Saharan Africa continuously expanding first-time TWS buyer pools. India’s TWS market grew 12% YoY in Q4 2025 (Counterpoint Research), driven by festive demand, product refresh cycles, and AI-enabled upgrades, reinforcing smartphone ecosystem expansion as a consistent, compounding driver of global TWS adoption.

AI Integration and Active Noise Cancellation Mainstream Adoption Accelerating Upgrade Cycles

Active Noise Cancellation (ANC), once confined to premium TWS earbuds priced above US$ 200, has now expanded into the US$ 50-100 mid-range segment, with 78% of newly launched TWS models integrating ANC as Bluetooth 5.3 and advanced audio chipsets from Qualcomm and MediaTek democratize performance at scale. In India, ANC-enabled devices grew 24% YoY in 2025, while spatial audio adoption surged 67% YoY, reflecting strong consumer appetite for premium features and accelerating replacement cycles from 24 months toward 14-18 months globally.

AI-powered TWS earbuds, featuring adaptive noise cancellation, biometric tracking, personalized sound tuning, and on-device voice assistants, represent the market’s highest-value innovation frontier, with the AI TWS segment projected to grow at a 30.2% CAGR in the forecast period. Platforms such as Qualcomm’s S5 and S7 Sound Gen, used in devices like Samsung Galaxy Buds, Sony WF-1000XM5, and Jabra Evolve2, enable continuous over-the-air upgrades, extending product lifecycles while simultaneously increasing average revenue per unit across premium TWS portfolios worldwide.

Market Restraints

E-Waste Regulation and Environmental Compliance Constraints on TWS Product Lifecycle

TWS earbuds, with lithium-ion batteries embedded in non-user-replaceable sealed housings, face expanding e-waste regulatory compliance burdens under the EU's revised Batteries Regulation (EU) 2023/1542, requiring replaceable batteries in personal audio devices from 2027, and the EU Right to Repair Directive mandating repairability standards for consumer electronics. Compliance mandates require fundamental housing and battery architecture redesigns, extending product development cycles by 12-18 months and increasing per-unit bill-of-materials complexity, creating product refresh timeline delays at OEM and brand level across European market-compliant TWS product programs.

Bluetooth Spectrum Congestion and Audio Codec Fragmentation Limiting Multi-Device Interoperability

TWS earbuds operating in the crowded 2.4 GHz ISM band face increasing wireless interference in high-density urban environments, office buildings, public transport, and event venues, causing audio dropouts and connectivity degradation that directly impair consumer satisfaction metrics and drive negative purchase sentiment. The audio codec ecosystem remains fragmented across aptX Adaptive (Qualcomm), LDAC (Sony), AAC (Apple), and LC3 (Bluetooth LE Audio standard), with interoperability gaps between Android OEM and Apple ecosystem devices limiting seamless multi-device switching capability that 38% of TWS consumers identify as a primary purchase-decision criterion, constraining cross-platform brand adoption rates.

Market Opportunities

AI-Enabled Health and Biometric Sensing Integration Expanding TWS Value Proposition

TWS earbuds integrated with in-ear biometric sensors, tracking heart rate, SpO2, skin temperature, and activity metrics, are emerging as a distinct wearable health-monitoring category, increasingly overlapping with smartwatch-based health tracking functionality. The global hearables market, including health-sensing TWS devices, is projected to reach US$ 165 Bn by 2033 at a 26.3% CAGR (IDC Worldwide Hearables Tracker), with health-monitoring TWS representing the highest-value average selling price segment within the broader category.

Apple’s AirPods Pro 2, featuring FDA-cleared hearing health functions such as clinical-grade hearing aid mode and hearing tests announced in 2024, sets a regulatory and commercial benchmark for positioning health-sensing TWS as a reimbursable medical device category. For manufacturers, FDA 510(k) clearance for hearing and biometric features unlocks insurance reimbursement pathways, shifting TWS from discretionary electronics to medically relevant health devices and expanding the addressable market by an estimated US$ 25-30 Bn within the health-sensing sub-segment globally by 2033.

Sub-US$ 100 Mass Market Expansion Across Emerging Economies

The Below US$ 100 price band is the fastest-growing TWS segment, expanding at a 30.8% CAGR, driven by rising smartphone penetration in India, Indonesia, Brazil, and Nigeria, which is unlocking hundreds of millions of first-time TWS buyers annually. In this segment, sub-US$ 50 ANC-enabled and high-quality audio offerings have become the core value proposition, reshaping mass-market adoption dynamics across emerging economies.

Xiaomi’s Redmi Buds series, which recorded 63% YoY shipment growth in Q1 2025 and captured 11.5% global market share (Canalys), highlights the commercial strength of sub-US$ 100 positioning at scale. In India, brands such as boAt, Noise, and Realme collectively hold over 45% domestic share in the sub-US$ 50 category, reinforcing the dominance of value-led ecosystems. Models integrating affordable ANC, regional language voice assistants, and extended battery life are best positioned to serve an estimated 500+ million first-time TWS buyers across Asia Pacific, Latin America, and Africa.

Category-wise Analysis

Product Type Insights

Standard TWS Earbuds lead the product type segment with a 32.4% market share in 2026, valued at approximately US$ 31.8 Bn, driven by their broad price-to-performance accessibility across both premium flagship models and high-volume value-tier SKUs in global retail channels. These devices serve the widest consumer base, spanning first-time buyers in emerging markets to ecosystem-loyal users such as Apple AirPods consumers in developed regions, resulting in the highest unit volumes across all distribution channels worldwide.

While ANC and AI-enabled categories are expanding their combined share, Standard TWS continues to dominate through volume-led revenue strength and multi-tier price coverage in the forecast timeline.

Smart/AI-enabled TWS Earbuds represent the fastest-growing product type, expanding at a 30.2% CAGR. The integration of on-device AI capabilities—including adaptive noise cancellation, real-time translation, biometric health tracking, and personalized sound optimization—is accelerating adoption across premium consumer segments globally, positioning AI integration as the key differentiator defining the next generation of TWS earbuds.

Price Band Insights

The US$ 101-200 price band leads the market with a 50.3% share in 2026, valued at approximately US$ 49.4 Bn, serving as the core premium mid-range segment where ANC performance, Bluetooth 5.3 multi-point connectivity, and ecosystem-driven brand loyalty converge at accessible mass-premium pricing. This segment captures the highest-value upgrade cycle, as consumers transition from sub-US$ 100 entry devices to more advanced audio experiences, with models such as Samsung Galaxy Buds, Sony WF-C700N, and Jabra Elite series anchoring competitive positioning.

Despite rising competition from lower price tiers, ANC democratization within this band sustains its revenue leadership over the premium US$ 200+ category.

The Below US$ 100 segment is the fastest-growing price band, expanding at a 30.8% CAGR in the forecast period. Rapid smartphone adoption across emerging markets such as India, Indonesia, and Brazil, combined with aggressive feature migration from brands like Xiaomi, boAt, Noise, and Realme, is enabling ANC availability at sub-US$ 50 price points. This shift is driving large-scale volume expansion and positioning the sub-US$ 100 segment as a key growth engine for global TWS adoption.

Distribution Channel Insights

Online retail/e-commerce leads the distribution channel segment with a 58.6% market share in 2026, valued at approximately US$ 57.5 Bn, driven by platform ecosystems such as Amazon, Flipkart, Tmall, and JD.com that enable global product accessibility, price transparency, and review-led purchase decisions at scale. The TWS category strongly aligns with digital-first buying behavior, with around 72% of consumers researching specifications online before purchase, while doorstep delivery models reduce reliance on in-store audio trials across mass-market price tiers.

Although offline retail remains important for premium product auditioning and carrier-bundled sales, e-commerce continues to dominate across all regions and price bands.

Direct-to-Consumer (DTC) and brand-owned stores represent the fastest-growing distribution channel, expanding at a 27.5% CAGR. Leading ecosystems such as Apple Store, Samsung Experience Stores, Sony Style outlets, and proprietary online storefronts are increasingly prioritizing direct customer engagement, higher margin capture, and first-party data ownership. This shift is accelerating as major TWS brands strengthen DTC strategies to reduce dependency on third-party marketplaces and enhance long-term brand loyalty and lifecycle monetization.

Regional Market Insights

North America

North America is set to achieve a 20.7% CAGR, capturing about 26% of the global TWS market share by 2025. This growth is driven by Apple's strong ecosystem, high-income consumers willing to pay for premium ANC and AI earbuds, and a mature e-commerce infrastructure. Factors such as brand loyalty, early tech adoption, and the integration of spatial audio and health-tracking features further solidify the region’s leadership, while competitive marketing from various audio brands spurs premium segment growth.

U.S. True Wireless Stereo Earbuds Market

The U.S. True Wireless Stereo market is projected to reach nearly US$23.7 billion in 2026, driven by strong ecosystem-led demand from leading brands and high consumer adoption of premium wireless audio devices. The market is anchored by Apple Inc., which continues to hold a dominant global share in the TWS segment, along with strong integration of Samsung Electronics Co., Ltd. across Android ecosystems. Increasing regulatory alignment through FCC Bluetooth device certification and FDA hearing-health frameworks is further expanding the role of TWS devices into regulated wellness and assistive-hearing applications, supporting higher average selling prices and broader product positioning.

Canada contributes additional demand through strong premium consumer electronics adoption and robust offline retail networks led by major electronics retailers such as Best Buy. Regional growth is further reinforced by rising AI-enabled health-sensing TWS adoption, expanding medical-grade audio use cases, and accelerated direct-to-consumer investments by leading brands, including Apple, Samsung, and Bose, across North American retail ecosystems.

Europe True Wireless Stereo Earbuds Market

Europe holds 21.6% share of the global TWS Market in 2026, estimated at approximately US$ 21.2 Bn, driven by strong premium audio brand heritage, high ANC adoption rates among urban commuter populations, and regulatory frameworks under EU Battery Regulation 2023/1542 accelerating sustainable TWS product architecture innovation across Germany, U.K., France, and Spain, alongside rising streaming music penetration, strong smartphone ecosystem integration, omnichannel retail expansion, and increasing demand for recycled-material-based and repairable audio devices across major EU markets.

Germany True Wireless Stereo Earbuds Market

The Germany TWS (True Wireless Stereo) market is projected to reach nearly US$7.7 billion in 2026, making it the leading market in Europe. Growth is supported by strong premium audio demand, high urban adoption of ANC-enabled devices, and a mature consumer electronics ecosystem. The presence of global and regional leaders such as Sennheiser electronic GmbH & Co. KG and strong enterprise audio penetration through brands like Jabra further reinforce Germany’s position as a hub for high-quality audio innovation. In addition, strong e-commerce penetration via platforms like Amazon.de continues to support premium and mid-range TWS sales across diverse consumer segments.

The U.K. maintains strong premium market momentum driven by Apple and Sony dominance through major retail channels such as John Lewis and Currys PC World. Meanwhile, France and Spain contribute significantly through mid-range demand led by brands like Samsung and JBL, distributed via Fnac and El Corte Inglés electronics networks. EU regulatory frameworks, including Right to Repair and Battery Regulation mandates, are accelerating sustainable product design and circular economy adoption, strengthening Europe’s position as a premium innovation hub for TWS devices.

Asia Pacific

Asia Pacific is the leading and fastest-growing region at 25.3% CAGR commanding approximately 39% of global TWS market share in 2025, driven by the world's largest smartphone consumer base, rapidly expanding youth-demographic middle class, and manufacturing scale advantages concentrating global TWS hardware production across China, Vietnam, and India, with strong penetration of music streaming platforms, aggressive price competition in entry-level segments, and expanding ODM/OEM supply chain integration supporting global exports.

China & India True Wireless Stereo Earbuds Market

The China TWS (True Wireless Stereo) market is projected to reach nearly US$26.8 billion in 2026, driven by massive consumer electronics scale, strong smartphone ecosystem integration, and rapid premium audio adoption across a digitally connected population. Growth is strongly supported by leading ecosystem players such as Xiaomi Corporation and Huawei Technologies Co., Ltd., alongside dominant e-commerce distribution channels including JD.com and Tmall that enable wide product accessibility across more than a billion consumers.

Rising demand for ANC-enabled earbuds, ecosystem-based device pairing, and premium audio experiences continues to reinforce China’s leadership in both volume and value segments of the global TWS market.

India's market for audio devices is expanding rapidly, valued at approximately US$9.1 billion, thanks to brands like boAt, Noise, and Realme targeting the sub-US$50 segment. Active noise cancellation (ANC) adoption is growing over 24% year-on-year. Meanwhile, Japan excels in the premium segment with Sony’s WF-1000XM series and JVC’s high-end offerings, while ASEAN countries like Indonesia, Vietnam, and Thailand are emerging as key markets due to increasing smartphone usage and first-time TWS adoption.

Competitive Landscape

The global TWS Earbuds Market is moderately concentrated at the premium tier, with Apple, Samsung, and Sony collectively holding approximately 50-55% of global revenue share, while the mid-to-value segment remains intensely fragmented across Xiaomi, boAt, Realme, JBL, and 200+ regional brands. Key differentiators include proprietary audio processing chips, spatial audio algorithms, ecosystem lock-in depth, and AI health sensing capability. Subscription-based hearing health and audio personalization service models are emerging as new revenue streams.

AI audio innovation, geographic mass-market expansion into sub-US$ 100 emerging market segments, DTC brand store investment, and health-sensing regulatory clearance programs define dominant competitive strategic themes across all major TWS market participants globally.

Strategic Developments

- In September 2024, Apple Inc. secured FDA clearance for AirPods Pro 2 clinical-grade hearing aid mode, the first over-the-counter hearing aid TWS earbud, repositioning premium TWS earbuds as reimbursable medical hearing health devices, fundamentally expanding Apple's regulatory-approved health audio addressable market globally.

- In March 2025, Xiaomi Corporation launched its Redmi Buds 6 Pro with on-device AI adaptive ANC across 30 markets simultaneously, achieving 63% YoY shipment growth in Q1 2025 (Canalys) and capturing 11.5% global TWS market share, displacing Samsung as the second-largest TWS shipper globally.

Companies Covered in True Wireless Stereo Earbuds Market

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Sony Corporation

- Xiaomi Corporation

- Bose Corporation

- Jabra (GN Audio A/S)

- Sennheiser Electronic GmbH

- JBL (Harman International / Samsung)

- boAt (Imagine Marketing Ltd.)

- Huawei Technologies Co., Ltd.

- Realme (BBK Electronics)

- Anker Innovations (Soundcore)

- Skullcandy Inc.

- Nothing Technology Limited

- OnePlus (BBK Electronics)

Frequently Asked Questions

The market is valued at US$ 98.1 Bn in 2026, projected to reach US$ 411.2 Bn by 2033, with an incremental opportunity of US$ 313.1 Bn.

Smartphone ecosystem proliferation removing 3.5mm audio jacks, AI-powered ANC democratization across sub-US$ 100 price bands, and youth-demographic TWS adoption across Asia Pacific emerging markets are the primary growth drivers.

The market is projected to grow at a CAGR of 22.7% from 2026 to 2033, building on a historical CAGR of 20.1% from 2020 to 2026.

AI-enabled health and biometric TWS sensing expanding into FDA-cleared hearing health device categories and sub-US$ 100 mass market expansion across 500+ million first-time buyers in India, ASEAN, and Africa are the highest-value growth opportunities.

Apple, Samsung, Sony, Xiaomi, Bose, Jabra, Sennheiser, JBL, boAt, Huawei, Realme, Anker (Soundcore), Skullcandy, Nothing Technology, and OnePlus are the leading global TWS market participants.