- Chipsets & Processors

- Edge AI Processor Market

Edge AI Processor Market Size, Share, and Growth Forecast 2026 – 2033

Edge AI Processor Market by Processor Type (Central Processing Units (CPU), Graphics Processing Units (GPU), Application-Specific Integrated Circuits (ASIC), Field Programmable Gate Arrays (FPGA)), Application (Computer Vision, Speech & Audio Processing, Natural Language Processing (NLP / On-device AI), Time-Series & Control Systems, Multimodal AI, Misc.), Device Type (Consumer Devices, Enterprise Devices), and Regional Analysis, 2026–2033

Edge AI Processor Market Size and Trend Analysis

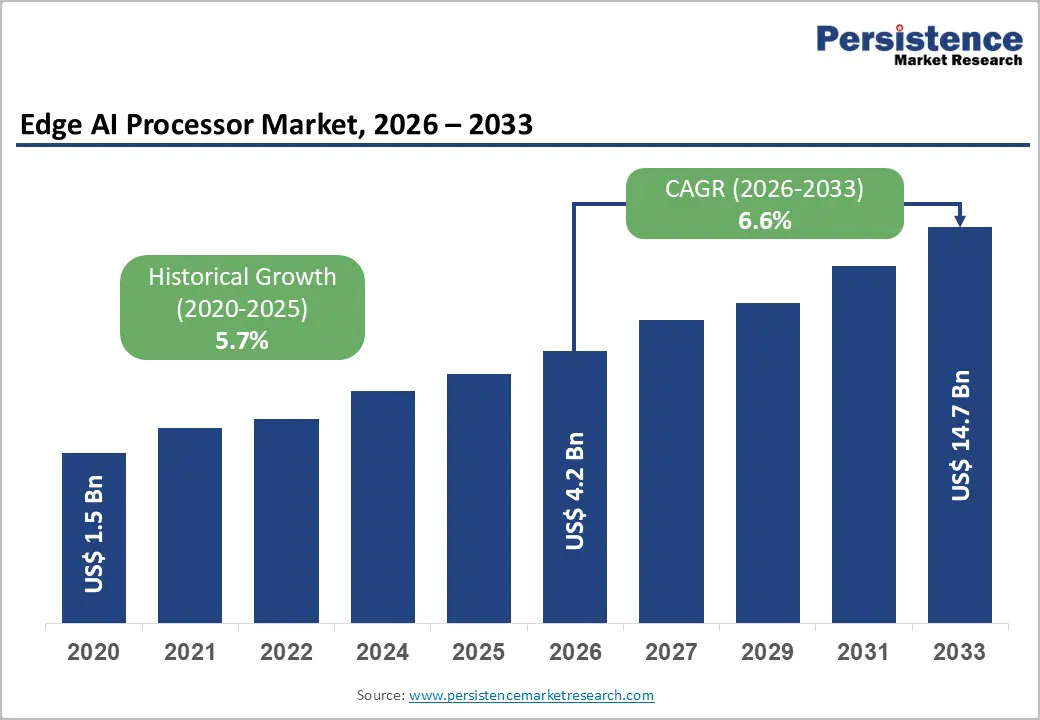

The global Edge AI Processor market size is expected to be valued at US$4.2 billion in 2026 and projected to reach US$14.7 billion by 2033, growing at a CAGR of 19.6% between 2026 and 2033. It is driven by the proliferation of intelligent edge devices, surging demand for low-latency AI inferencing, and increasing deployment of AI workloads outside the cloud.

The rapid commercialisation of 5G networks, with global 5G subscriptions expected to exceed five billion by 2030, according to Ericsson's Mobility Report, is enabling real-time on-device AI processing at scale. Simultaneously, data privacy regulations such as the EU AI Act and GDPR compel organisations to process sensitive data locally, reinforcing the commercial case for edge inference chips.

Key Industry Highlights:

- Leading Region: North America dominates the Edge AI Processor market with approximately 34% market share in 2026, supported by major semiconductor OEMs, the U.S. CHIPS Act, and deep enterprise AI infrastructure investment across defence, healthcare, and retail verticals.

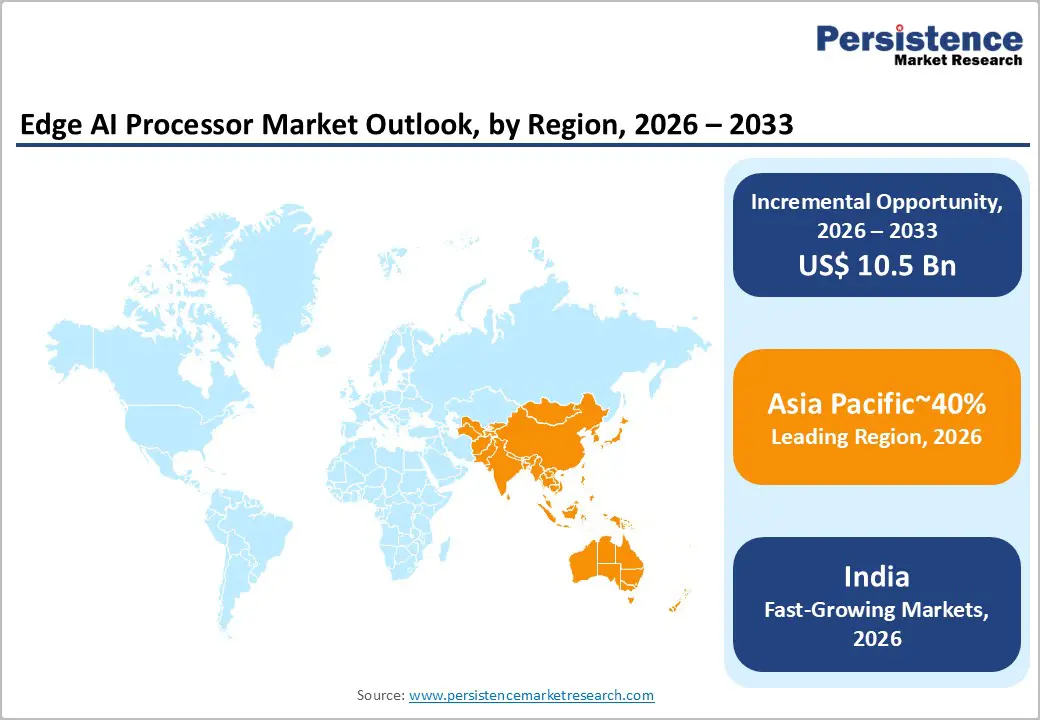

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, registering an estimated CAGR above 22% through 2033, driven by China's domestic chip ambitions, India's semiconductor mission, and mass-market consumer electronics production across South Korea and Taiwan.

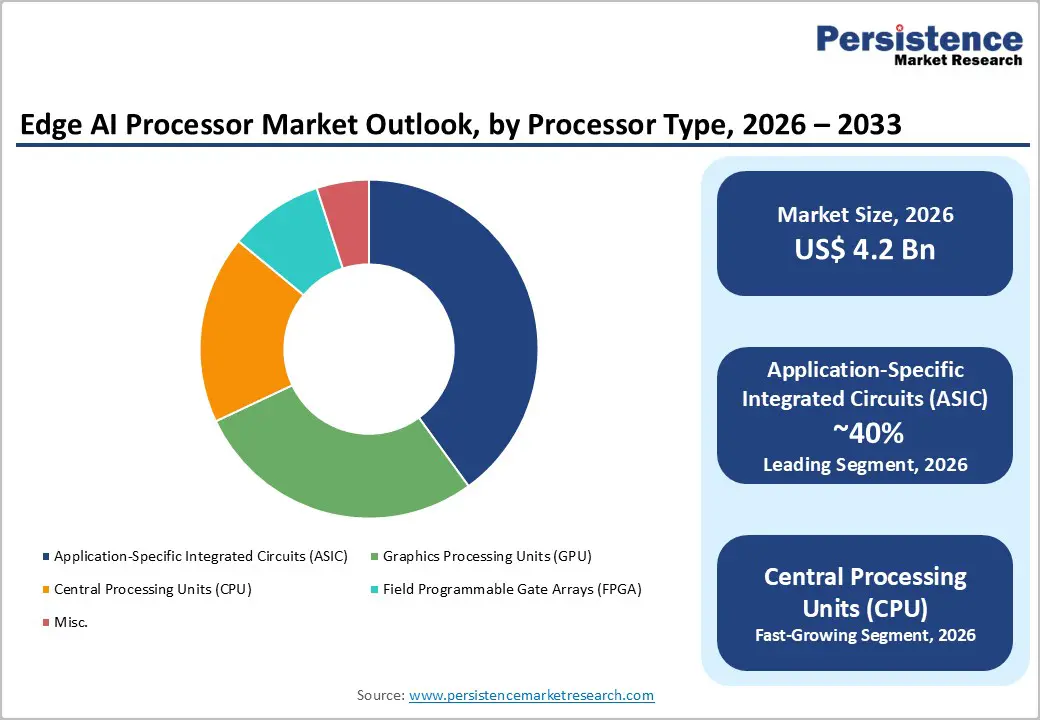

- Dominant Segment: Application-Specific Integrated Circuits (ASICs) lead the Processor Type category with 40% market share in 2026, owing to their unmatched energy efficiency and optimised neural network throughput for high-volume edge inference deployments.

- Fastest Growing Segment: Natural Language Processing (NLP / On-device AI) within the Application category is the fastest-growing segment, propelled by on-device generative AI adoption in smartphones and enterprise edge devices, claiming 15% market share in 2026 with a strong upward trajectory.

- Key Market Opportunity: The automotive ADAS and autonomous vehicle segment presents a high-value opportunity, with regulatory mandates and EV proliferation expected to drive procurement of automotive-grade edge AI processors exceeding 40 million annual vehicle deployments by 2030.

DRO Analysis

Drivers - Widespread Adoption of IoT and Connected Device Ecosystems

The exponential deployment of Internet of Things (IoT) devices is a primary catalyst for edge AI processor demand. According to the International Telecommunication Union (ITU), the number of connected IoT devices is projected to surpass 50 billion globally by 2030. These devices, spanning industrial sensors, smart cameras, autonomous vehicles, and wearables, require localised, real-time AI inference capabilities to function effectively without continuous cloud dependency.

Edge AI processors address these requirements by delivering low-latency, energy-efficient computation directly at the data source. The convergence of shrinking semiconductor process nodes below 5nm and the integration of neural processing units (NPUs) into SoC architectures has enabled AI capabilities in power-constrained edge deployments, significantly broadening the addressable market for specialised edge chips and accelerators.

Stringent Data Sovereignty Regulations and Privacy Mandates

Regulatory frameworks across major economies are fundamentally reshaping AI data processing architectures. The EU AI Act, which entered into force in August 2024, classifies many AI applications in security, healthcare, and critical infrastructure as high-risk, mandating robust data governance and often necessitating local data processing.

The General Data Protection Regulation (GDPR) further restricts cross-border data transfers, compelling enterprises to deploy AI inference at the edge rather than transmitting raw data to centralised servers. A 2024 survey by the Cloud Security Alliance found that 67% of enterprises cited data sovereignty concerns as a key driver for edge infrastructure investment. This regulatory pressure directly drives hardware procurement decisions toward specialised edge AI processors capable of on-device inferencing, boosting demand across healthcare, financial services, and industrial automation sectors.

Restraints - High Development Cost and Design Complexity of Custom Edge Chips

The engineering of custom edge AI processors, particularly Application-Specific Integrated Circuits (ASICs), involves prohibitively high non-recurring engineering (NRE) costs. Tape-out costs for a leading-edge chip at the 5nm node can exceed US$ 50 million, according to IBS (IC Knowledge). This creates a substantial barrier for smaller device OEMs and emerging market entrants who cannot sustain multi-year chip development cycles. Additionally, the shortage of specialised hardware engineers and AI compiler talent compounds time-to-market challenges, limiting the pace at which organisations can iterate on edge AI silicon. This restraint disproportionately affects fabless startups and constrains innovation velocity in the competitive edge processor landscape.

Fragmented Software Ecosystem and Interoperability Challenges

Despite hardware advances, the edge AI software stack remains fragmented, creating deployment friction that dampens market adoption. Multiple competing frameworks, including TensorFlow Lite, ONNX Runtime, and Apache TVM, lack seamless cross-hardware compatibility, requiring developers to invest significant engineering resources in porting and optimizing models for specific silicon targets. A 2024 Linux Foundation AI & Data survey identified software toolchain fragmentation as the second-most cited obstacle to edge AI deployment. Without unified, hardware-agnostic middleware, enterprises face a higher total cost of ownership, inhibiting procurement decisions and slowing market diffusion of edge AI processor solutions across heterogeneous device fleets.

Opportunities - On-Device NLP and Generative AI Inference at the Edge

The emergence of compact large language models (LLMs) and on-device generative AI represents a transformative opportunity for edge AI processor vendors. Apple's deployment of on-device foundation models in iOS 18 and Google's Gemini Nano integration into Android devices signal a fundamental architectural shift toward edge-side natural language processing (NLP).

According to ARM Holdings, over 100 billion ARM-based chips capable of generative AI inference are expected to be deployed by 2030. This trend demands processors with specialised transformer accelerators, high memory bandwidth, and optimized matrix multiplication engines. As consumer and enterprise devices increasingly embed on-device AI assistants, the demand for Field Programmable Gate Arrays (FPGAs) and next-generation ASICs with reconfigurable neural engines is projected to intensify substantially through 2033.

Autonomous Vehicles and Advanced Driver Assistance Systems (ADAS) Deployment

The automotive sector represents a high-value frontier for edge AI processor manufacturers. The Society of Automotive Engineers (SAE) estimates that Level 3 and above autonomous driving systems require real-time AI inference of upwards of 10 petaflops per second, capabilities achievable only through dedicated in-vehicle edge AI chips.

Global electric vehicle (EV) production is projected to surpass 40 million units annually by 2030 per the International Energy Agency (IEA), with nearly all next-generation models incorporating ADAS functionality. NVIDIA's Drive platform and Qualcomm's Snapdragon Ride are already attracting major OEM partnerships. As ADAS mandates expand across the EU, U.S., and China, automotive-grade edge AI processors are poised to emerge as one of the fastest-growing sub-segments within the broader market, generating sustained procurement demand well into the next decade.

Category-wise Analysis

Processor Type Insights

Among all processor types, Application-Specific Integrated Circuits (ASICs) command the leading position in the Edge AI Processor market, accounting for approximately 40% of the total market share in 2026. This dominance stems from the inherently superior performance-per-watt efficiency of purpose-built silicon compared to general-purpose alternatives. ASICs designed for neural network workloads can deliver 10x to 100x greater energy efficiency over traditional CPUs for inference tasks, according to semiconductor research published.

Hyperscalers such as Google (TPU), Amazon (Inferentia), and Apple (Neural Engine) have invested heavily in proprietary ASIC development, normalising the technology across both consumer and enterprise edge devices. The segment's scale advantages and optimised instruction sets for matrix operations make it the preferred architecture for high-throughput, latency-sensitive edge AI deployments.

Application Insights

Within the application landscape, computer vision leads with approximately 38% of the total edge AI processor market share in 2026. The widespread deployment of intelligent surveillance, industrial quality control, retail analytics, and autonomous navigation systems underpins this segment's dominance.

According to the International Data Corporation (IDC), over 1 billion surveillance cameras were operational globally as of 2024, with an increasing proportion integrating AI-based object detection and facial recognition at the device level. Edge inference for computer vision reduces data transmission costs and enables sub-10ms response times critical for real-time applications. The maturity of convolutional neural network (CNN) deployment toolchains and availability of off-the-shelf vision AI chips from vendors such as Intel (Movidius) and Ambarella further consolidate Computer Vision's leading position within the application category.

Device Type Insights

Consumer devices represent the dominant segment accounting approximately 68% of the Edge AI Processor market in 2026. The mass-market penetration of AI-enabled smartphones, smart speakers, wearables, and smart TVs creates the largest installed base for edge AI silicon globally.

According to GSMA Intelligence, over 6.8 billion smartphones were in use worldwide in 2024, with leading OEMs including Apple, Samsung, and Qualcomm integrating dedicated NPUs into flagship chipsets. The Consumer Electronics Association (CES) has consistently highlighted on-device AI as a defining product differentiation vector since 2023. High unit volumes and competitive refresh cycles ensure that Consumer Devices retain their dominant market share position throughout the forecast period, even as Enterprise Devices exhibit stronger CAGR performance.

Regional Insights

North America Edge AI Processor Market Trends and Insights

North America leads the global Edge AI Processor market with an estimated 34% share in 2026, driven by robust semiconductor R&D investment, the presence of leading fabless chip designers, and deep enterprise AI adoption. The region benefits from a mature cloud-to-edge migration trend across sectors, including healthcare, defence, and retail, with strong policy support from the U.S. CHIPS and Science Act, allocating US$ 52.7 billion to domestic semiconductor development.

U.S. Edge AI Processor Market Size

The U.S. Edge AI Processor market is estimated at approximately US$ 1,105.1 million in 2026. The country's leadership is anchored by dominant silicon vendors, including NVIDIA, Qualcomm, and Intel, alongside robust enterprise demand for AI-enabled edge infrastructure across autonomous systems, smart manufacturing, and defence applications.

Europe Edge AI Processor Market Trends and Insights

Europe accounts for an estimated 18% of the global Edge AI Processor market in 2026, with growth underpinned by automotive-grade AI chip demand, industrial IoT deployment, and regulatory alignment under the EU AI Act. The region's strong automotive heritage and precision manufacturing ecosystem create favorable conditions for ASIC and FPGA adoption in embedded AI applications. National semiconductor strategies in Germany and France further bolster regional capacity.

Germany Edge AI Processor Market Size

Germany's Edge AI Processor market is estimated at approximately US$ 180.8 million in 2026. The country's globally significant automotive and industrial sectors drive strong demand for automotive-grade edge AI silicon and embedded AI in factory automation systems, supported by Bosch and Infineon Technologies' active investment in edge intelligence platforms.

U.K. Edge AI Processor Market Size

The U.K. Edge AI Processor market is estimated at approximately US$ 135.6 million in 2026. The country's advanced fintech, healthcare AI, and smart city initiatives, alongside ARM Holdings' global IP licensing dominance, support consistent demand for edge AI processor solutions in both consumer electronics and enterprise edge infrastructure applications.

Asia Pacific Edge AI Processor Market Trends and Insights

Asia Pacific is projected to be the fastest-growing region in the Edge AI Processor market through 2033, registering an estimated CAGR above 22%. China leads regional volume shipments through domestic champion firms including Huawei (Ascend) and Cambricon, while Japan, South Korea, and Taiwan contribute through semiconductor manufacturing capabilities. India's expanding electronics manufacturing sector and smartphone-driven consumer AI adoption further accelerate regional demand.

India Edge AI Processor Market Size

India's Edge AI Processor market is estimated at approximately US$ 167.4 million in 2026. The India Semiconductor Mission (ISM) and Production-Linked Incentive (PLI) schemes are catalyzing domestic chip design and manufacturing. With smartphone penetration surpassing 979 million internet users and rising 5G adoption, consumer device demand for on-device AI processing is intensifying rapidly.

China Edge AI Processor Market Size

China's Edge AI Processor market is estimated at approximately US$ 636.3 million in 2026, reflecting the country's massive consumer electronics output, state-backed AI strategy, and extensive smart city deployments. China's 14th Five-Year Plan allocated substantial resources to AI infrastructure, while domestic chip firms continue to advance edge inference silicon capabilities under semiconductor self-sufficiency mandates.

Competitive Landscape

The global Edge AI Processor market exhibits a moderately consolidated structure, with a handful of established semiconductor leaders commanding significant market shares while a dynamic cohort of specialised AI chip startups competes in niche verticals. NVIDIA, Qualcomm, Intel, and Apple collectively account for a substantial portion of revenue, leveraging extensive developer ecosystems and vertical integration advantages.

Key strategic differentiators include proprietary neural processing unit (NPU) architectures, software-hardware co-optimization, and automotive/industrial certification attainment. Emerging players such as Hailo and Syntiant are gaining traction through ultra-low-power inference innovations, driving competitive fragmentation in the sub-1W edge AI segment. Strategic M&A activity and fabless design partnerships with TSMC and Samsung Foundry are prominent expansion levers employed across market participants.

Key Developments:

- In March 2026, NVIDIA introduced advanced edge AI platforms, including the Jetson Orin and IGX Thor, enabling real-time data processing and autonomous decision-making in highly constrained environments. These capabilities support on-device analytics, sensor data processing, and anomaly detection, extending predictive maintenance applications to remote and mission-critical systems such as satellites and industrial infrastructure, where continuous monitoring and failure prediction are essential.

- In March 2026, Intel launched its Intel® Core™ Series 2 processors with real-time deterministic performance, alongside an expanded Edge AI portfolio, enabling mission-critical edge applications with integrated AI acceleration. The platform supports continuous monitoring, real-time data processing, and anomaly detection in industrial and healthcare environments, strengthening the foundation for predictive maintenance systems that rely on low-latency analytics and reliable edge computing infrastructure.

Global Edge AI Processor Market - Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 1.5 Billion |

|

Current Market Value (2026) |

US$ 4.2 Billion |

|

Projected Market Value (2033) |

US$ 14.7 Billion |

|

CAGR (2026–2033) |

19.6% |

|

Leading Region |

North America, 34% market share (2026) |

|

Dominant Processor Type |

Application-Specific Integrated Circuits (ASIC), 40% market share (2026) |

|

Top-ranking Application |

Computer Vision, 38% market share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 10.5 Billion (Absolute Dollar Growth) |

Global Edge AI Processor Market Report Coverage

|

Report Attributes |

Details |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

Companies Covered in Edge AI Processor Market

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- Intel Corporation

- Apple Inc.

- Google LLC (Alphabet Inc.)

- Amazon Web Services, Inc. (AWS Inferentia)

- Huawei Technologies Co., Ltd.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- ARM Holdings plc

- Ambarella, Inc.

- Hailo Technologies Ltd.

- Syntiant Corp.

- Cambricon Technologies Corporation

- Lattice Semiconductor Corporation

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

Frequently Asked Questions

The global Edge AI Processor market is estimated to be valued at US$ 4.2 Billion in 2026. This valuation reflects robust adoption across consumer electronics, automotive, and industrial IoT sectors, underpinned by the rapid transition from cloud-centric AI workloads to distributed on-device inference architectures.

The primary demand drivers include the proliferation of IoT-connected devices, expected to exceed 50 billion by 2030 per ITU estimates, stringent data privacy regulations such as GDPR and the EU AI Act mandating local data processing, and the commercial rollout of 5G networks enabling ultra-low-latency edge AI applications across autonomous systems and smart infrastructure.

North America is the leading region in the Edge AI Processor market, holding approximately 34% market share in 2026. The region benefits from the concentration of major semiconductor designers, strong enterprise AI infrastructure investment, and the U.S. CHIPS and Science Act's US$ 52.7 billion allocation to domestic semiconductor innovation and manufacturing.

The most significant opportunity lies in the autonomous vehicles and ADAS segment, where mandatory regulatory requirements across the EU, U.S., and China are driving procurement of automotive-grade edge AI processors. With global EV production expected to surpass 40 million annual units by 2030 per the IEA, and Level 3 plus vehicles requiring real-time on-device AI inference exceeding 10 TOPS, this vertical represents a high-value, sustained growth avenue for processor vendors.

The key market participants include NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Advanced Micro Devices, Inc., Mythic AI.