- Automation & Robotics

- SMT Equipment Market

SMT Equipment Market Size, Share, and Growth Forecast 2026 - 2033

SMT Equipment Market by Equipment (Placement Equipment, Inspection Equipment, Soldering Equipment, Screen Printing Equipment, Cleaning Equipment, Rework and Repair Equipment), Application (Consumer Electronics, Telecommunications, Aerospace & Defense, Automotive, Medical, Industrial, Energy & Power Systems), and Regional Analysis for 2026 - 2033

SMT Equipment Market Size and Trend Analysis

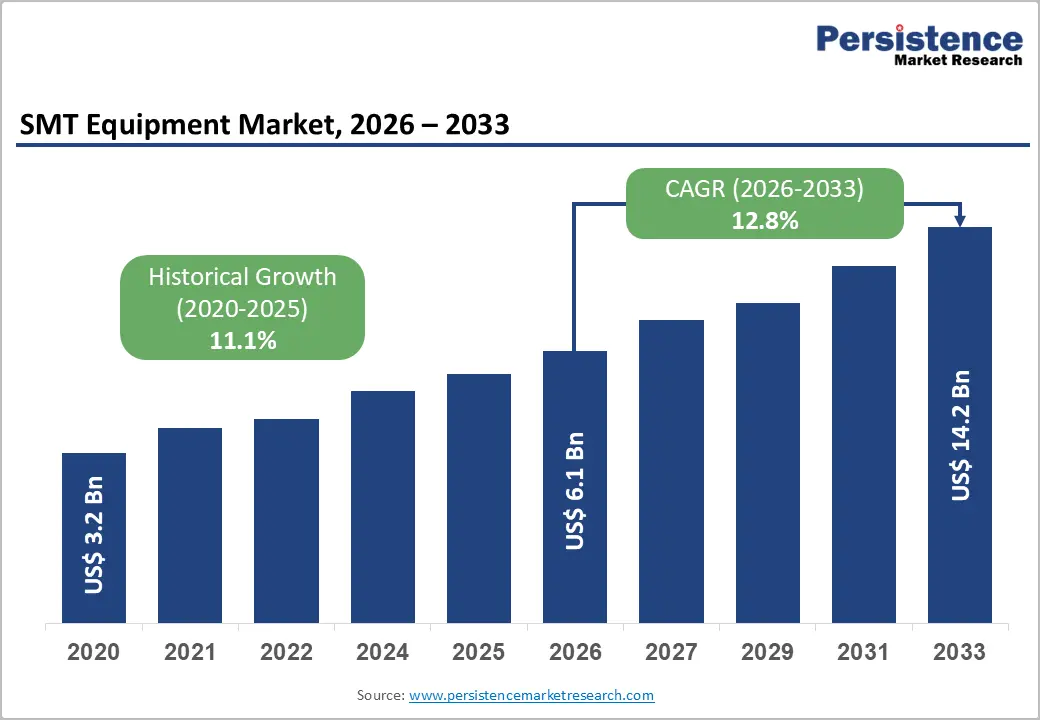

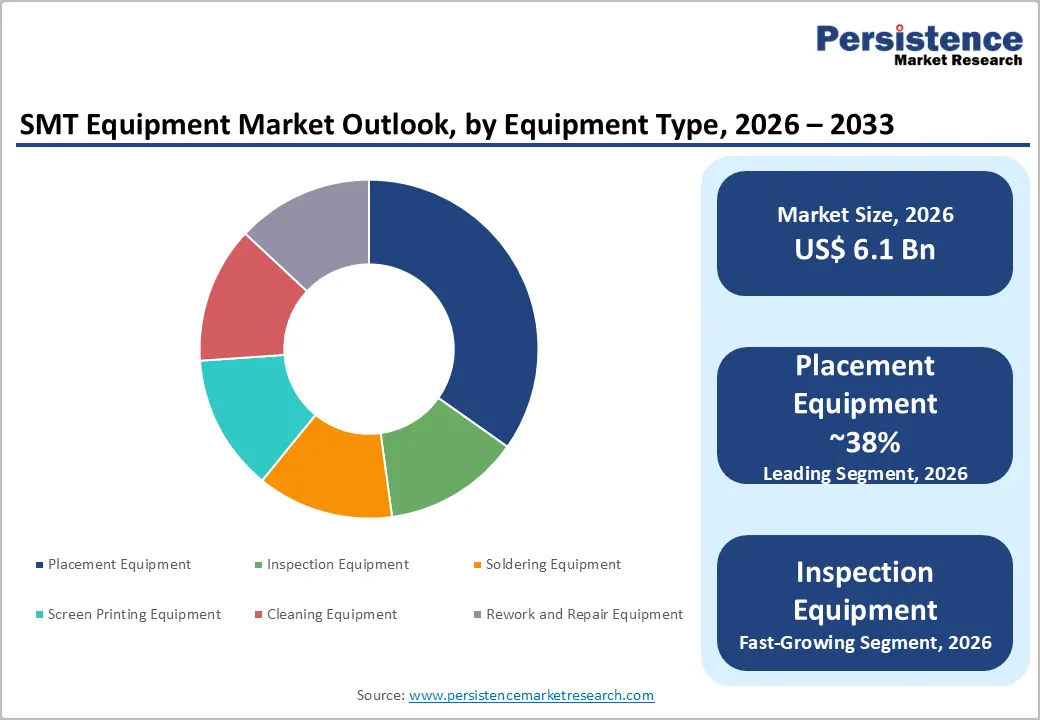

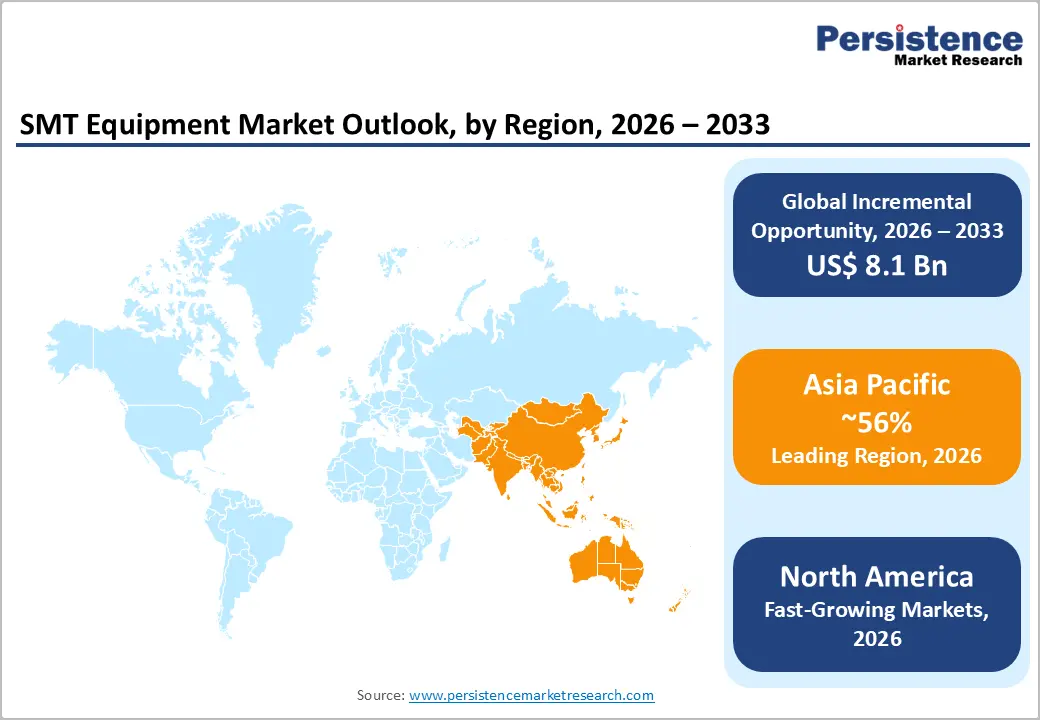

The global SMT equipment market size is expected to be valued at US$ 6.1 billion in 2026 and is projected to reach US$ 14.2 billion by 2033, growing at a CAGR of 12.8% between 2026 and 2033. This exceptional growth trajectory is driven by the accelerating global electrification of vehicles, the proliferation of 5G telecommunications infrastructure, and the semiconductor industry's rapid capacity expansion, each demanding larger and more sophisticated surface mount technology equipment fleets to assemble increasingly complex printed circuit board assemblies (PCBAs).

The International Electronics Manufacturing Initiative (iNEMI) technology roadmap identifies miniaturization, heterogeneous integration, and AI-driven inspection as the defining trends reshaping electronics manufacturing automation solutions through 2030, with surface mount technology equipment investment rising proportionally to electronics production output globally.

Key Industry Highlights:

- 5G Infrastructure Boom: Global 5G connections are projected to reach 5.9 billion by 2030, accelerating procurement of advanced SMT placement systems and PCB assembly lines for telecom, servers, semiconductor packaging, and edge computing hardware manufacturing.

- Semiconductor Investment Surge: The U.S. CHIPS Act, allocating USD 52.7 billion alongside the EU Chips Act and India Semiconductor Mission, is triggering massive semiconductor fab investments, with advanced SMT line investments exceeding USD 5–10 million per facility.

- Automotive Electronics Expansion: Electric vehicles now contain 3,000–5,000 electronic components versus 1,500 in ICE vehicles, structurally increasing SMT equipment demand for ADAS modules, battery systems, inverters, and automotive PCB assembly automation.

- Inspection Segment Growth: Inspection equipment is the fastest-growing SMT category with approximately 15.2% CAGR driven by AI-powered 3D AOI and AXI systems supporting zero-defect automotive and medical electronics manufacturing requirements.

- Placement Equipment Leadership: Placement equipment dominates with nearly 38% market share in 2025 due to its critical role in SMT throughput, high replacement frequency, and premium pricing reaching USD 800,000–1.5 million per system.

- Consumer Electronics Dominance: Consumer electronics account for approximately 34% market share in 2025, supported by large-scale smartphone, wearable, gaming, and smart device production requiring continuous SMT line upgrades every 5–7 years.

- Automotive Segment Acceleration: Automotive applications are projected to grow at approximately 16.5% CAGR through 2033, fueled by EV expansion, ADAS proliferation, IPC Class 3 reliability standards, and increasing electronics manufacturing complexity globally.

- Asia Pacific Supremacy: Asia Pacific leads with approximately 56% global SMT equipment market share in 2025, supported by China’s electronics dominance, India’s PLI-driven manufacturing expansion, and semiconductor investments across South Korea and ASEAN nations.

- India Manufacturing Momentum: India is emerging as the fastest-growing SMT equipment market globally with approximately 17.5% CAGR through 2033, driven by electronics PLI incentives, Apple supply-chain localization, and USD 300 billion manufacturing ambitions.

Market Dynamics

Drivers - 5G Network Rollout and Semiconductor Expansion Are Driving Unprecedented Demand for High-Speed Placement Machines and Advanced PCB Assembly Lines

The global deployment of 5G telecommunications infrastructure and the associated ramp-up of semiconductor fabrication and packaging capacity are generating the most consequential demand cycle in the history of the SMT equipment market, with every new 5G base station, server rack, and advanced chip package requiring dense, high-speed, precision automated PCB assembly systems that constitute the core of the surface mount technology equipment addressable market. The GSMA Intelligence projects that global 5G connections may reach 5.9 billion by 2030, necessitating massive PCBA production for radio units, small cells, and edge computing hardware.

Simultaneously, the U.S. CHIPS and Science Act, committing USD 52.7 billion to domestic semiconductor manufacturing and equivalent programs in the EU Chips Act (EUR 43 billion), India Semiconductor Mission, and Japan's semiconductor reindustrialization program are catalyzing greenfield fab and packaging facility investment that directly drives high-speed placement machine procurement. Each advanced semiconductor packaging line requires multiple automated PCB assembly systems, with per-line SMT equipment investment commonly exceeding USD 5–10 million for advanced configurations, creating large, program-anchored procurement events for SMT equipment suppliers.

Automotive Electrification and ADAS Complexity Are Creating an Expanding SMT Equipment Demand Base in Automotive Electronics Manufacturing

The automotive industry's transition to electric vehicles and advanced driver assistance systems is fundamentally transforming its electronics manufacturing requirements and, with it, its SMT equipment procurement profile. A modern battery electric vehicle (BEV) contains approximately 3,000–5,000 electronic components, per the International Organization of Motor Vehicle Manufacturers (OICA) sector analysis, compared with approximately 1,500 in a conventional internal combustion engine vehicle, a doubling of electronics content that directly translates into expanded electronics manufacturing automation solutions procurement at every automotive Tier-1 supplier and OEM electronics manufacturing facility.

The International Energy Agency (IEA) reported that global EV sales surpassed 14 million units in 2023, with production scaling rapidly across China, Europe, and North America, each market requiring expanded automotive PCBA production capacity for battery management systems, inverters, ADAS control units, and V2X communication modules. Automotive SMT equipment requirements also impose premium specifications, including lead-free process compatibility, high thermal budget soldering, and IPC-A-610 Class 3 inspection standards that command higher average selling prices and generate more complex replacement and upgrade cycles than standard consumer electronics SMT lines.

Restraints - High Capital Cost and Long Payback Periods Constrain SMT Equipment Investment in Small and Medium Electronics Manufacturers

A complete high-speed SMT production line encompassing screen printer, high-speed placement machine, reflow oven, and automated optical inspection represents a capital investment of USD 800,000 to USD 3+ million for a mid-tier configuration, and significantly more for advanced automotive or aerospace-grade lines. For small and medium electronics manufacturers (SMEs) which constitute the majority of PCBA production units globally by count, this capital threshold creates significant financing barriers that delay line upgrades and constrain adoption of the latest advanced inspection and testing and placement technology generations. The extended return-on-investment periods of 3–7 years for mid-range SMT lines in competitive contract manufacturing environments further suppress investment velocity among price-sensitive buyers in Southeast Asia and South Asia.

Component Miniaturization Challenges Are Increasing Equipment Technical Requirements and Driving Faster Obsolescence of Installed SMT Lines

The semiconductor industry's relentless component miniaturization with passive component dimensions progressing from 0402 to 0201 and now 01005 package sizes, and IC packages transitioning to fine-pitch Ball Grid Array (BGA) and Chip Scale Package (CSP) formats is increasing the technical requirements for placement accuracy and inspection resolution at a pace that outstrips the capability of older installed SMT equipment.

The IPC (Association Connecting Electronics Industries) standards updates continually raise placement accuracy and solder joint inspection thresholds, effectively obsoleting installed equipment that cannot meet new component compatibility requirements within 5–8 years of manufacture. This accelerated obsolescence cycle increases replacement investment pressure for contract manufacturers operating on thin margins, while simultaneously suppressing utilization value of legacy equipment compressing the working asset life and total value realized from each SMT capital investment.

Opportunities - AI-Integrated Automated Optical Inspection (AOI) Systems Represent the Fastest-Growing and Highest-Value-Add SMT Equipment Segment

Advanced inspection and testing equipment particularly AI-powered automated optical inspection (AOI) and automated X-ray inspection (AXI) systems is the fastest-growing equipment segment within the SMT market, driven by the convergence of shrinking component sizes that exceed human visual inspection capability, IPC Class 3 quality requirements in automotive and medical PCBA production, and the AI revolution that is enabling machine vision systems to detect defects with accuracy that consistently surpasses trained human inspectors.

The IPC's J-STD-001 and IPC-A-610 standards define solder quality inspection criteria that require automated inspection for reliable compliance at production throughput rates, establishing a regulatory floor for AOI adoption in quality-conscious manufacturing environments. Companies including Koh Young Technology and Mirtec have published data demonstrating that AI-integrated 3D AOI systems achieve false-call rates below 0.5% dramatically lower than traditional 2D systems while simultaneously detecting defect types invisible to conventional inspection methods. As electronics manufacturers face zero-defect quality requirements in automotive Tier-1 supply chains, investment in advanced inspection and testing infrastructure is transitioning from discretionary quality improvement to mandatory production qualification.

Medical Device Electronics Manufacturing Is an Emerging High-Growth Application Segment Requiring Premium SMT Equipment Specifications

The medical devices application segment is one of the fastest-growing end-uses for SMT equipment, driven by the global expansion of connected health devices, implantable medical electronics, remote patient monitoring systems, and diagnostic imaging equipment all requiring ultra-high-reliability PCBA production that mandates premium-specification SMT equipment configurations. The U.S. Food and Drug Administration (FDA) 21 CFR Part 820 quality system regulation and ISO 13485 medical device quality management standard impose rigorous process validation and traceability requirements on medical PCBA manufacturing that require certified SMT equipment with full process data logging and statistical process control capabilities.

The World Health Organization (WHO) has projected global medical device market growth to accelerate through the decade driven by aging populations across developed economies and expanding healthcare access in emerging markets creating a sustained demand trajectory for high-specification medical-grade SMT equipment. Manufacturers who develop SMT equipment variants specifically validated for ISO 13485 process environments with IQ/OQ/PQ documentation packages are positioned to command 20–35% price premiums over standard commercial-grade equivalents in this high-value, rapidly growing segment.

Category-wise Analysis

Equipment Type Insights

Placement Equipment (also referenced as high-speed placement machines in the electronics manufacturing automation solutions context) leads the SMT equipment segment with approximately 38% market share in 2025, reflecting the central role of component placement in the SMT assembly process and the high capital value of modern high-speed chip shooters and flexible placement machines that form the throughput-determining bottleneck in every SMT production line. Modern high-speed placement machines from ASM Pacific Technology (ASMPT), Fuji Corporation, and Yamaha Motor can place 50,000–100,000 components per hour (CPH) at accuracies of ±25–50 microns performance specifications that are being progressively tightened as component miniaturization continues.

Placement equipment's market share leadership is sustained by its position as the highest-value single investment in a typical SMT line premium multi-gantry system for advanced applications reaching USD 800,000–1.5 million per unit and by the fastest replacement cycle driven by throughput and accuracy obsolescence. The global proliferation of automated PCB assembly systems in new EV battery electronics and 5G infrastructure manufacturing facilities is generating consistent large-order placement equipment procurement globally.

Inspection Equipment is the fastest-growing SMT equipment category, projected at approximately 15.2% CAGR through 2033, significantly above the market average, driven by AI-powered 3D AOI and AXI technology investment, automotive Tier-1 zero-defect quality mandates, and the FDA's traceability requirements for medical PCBA manufacturing, which are structurally compelling inspection system upgrades at every quality-driven production facility.

Application Insights

Consumer Electronics leads the application segment with approximately 34% market share in 2025, anchored by the global consumer electronics industry's scale with the Consumer Technology Association (CTA) reporting total U.S. consumer technology revenue exceeding USD 480 billion in 2023 and Asia Pacific consumer electronics production operating at even larger scale and by its position as the original high-volume driver that established the SMT industry's current equipment architecture and supply chain. Smartphones, tablets, smart TVs, gaming consoles, and wearables are each manufactured on high-speed SMT lines that collectively represent the world's largest installed SMT equipment base by unit count.

Consumer electronics OEMs and their EMS (electronics manufacturing services) partners including Hon Hai Precision (Foxconn), Pegatron, and Flex Ltd. operate some of the world's highest-utilization SMT lines, creating consistent volume-level replacement and upgrade procurement for placement and soldering equipment on 5–7 year refresh cycles. Surface mount technology equipment serving consumer electronics lines also drives the broadest range of component compatibility requirements from micro-passive 01005 chips to large RF connectors sustaining demand for flexible placement systems capable of handling the full component range.

Automotive is the fastest-growing application segment, projected at approximately 16.5% CAGR in the forecast period driven by the EV electronics content expansion and ADAS system proliferation that is structurally doubling automotive electronics content per vehicle and compelling Tier-1 suppliers to invest in new high-specification SMT production capacity meeting IPC Class 3 and AEC-Q100 automotive electronics reliability standards.

Regional Insights

North America SMT Equipment Market Trends

North America is experiencing a structural SMT equipment investment revival, driven by the U.S. CHIPS and Science Act's USD 52.7 billion semiconductor manufacturing investment and the broader reshoring of advanced electronics manufacturing from Asia. New semiconductor packaging facilities including Intel's Ohio fab complex, TSMC's Arizona wafer fabs, and Samsung's Texas facility are each requiring substantial SMT and advanced packaging equipment procurement. The region's automotive electrification investment with GM, Ford, and Stellantis each investing tens of billions in EV manufacturing is expanding automotive electronics assembly capacity that requires premium-specification SMT equipment.

North America's medical device industry the world's largest by revenue is a consistent high-value SMT equipment buyer, with FDA 21 CFR Part 820 and ISO 13485 quality system requirements driving preference for validated, documentation-rich SMT equipment platforms. The growing defense and aerospace electronics manufacturing base, requiring IPC Class 3 PCBA production, further sustains demand for precision placement and inspection equipment at above-average selling prices.

- U.S. SMT Equipment Market Share

The United States commands approximately 81% of the North American SMT equipment market, positioned at the center of the most consequential electronics manufacturing reshoring cycle in decades. U.S. SMT equipment demand grows at approximately 13.2% CAGR through 2033 above the global average driven by CHIPS Act-funded semiconductor facility build-outs, automotive EV electronics supply chain localization, and the medical device industry's ISO 13485-compliant manufacturing expansion. The U.S. market's premium specification requirements including Class 3 inspection, full traceability, and process validation documentation translate into higher average selling prices per SMT equipment unit than any other geographic market globally, sustaining revenue growth above unit volume growth rates.

Europe SMT Equipment Market Trends

Europe is a precision-engineering-led SMT equipment market where the automotive industry's electrification investment and the EU Chips Act's EUR 43 billion semiconductor manufacturing commitment are creating a sustained investment cycle in advanced PCB assembly and inspection equipment. Germany's world-class automotive supply chain, led by Bosch, Continental, and ZF Friedrichshafen, is investing extensively in automotive-grade SMT production capacity as EV electronics complexity escalates. The European Chips Act's investment in semiconductor packaging and assembly capacity in Germany, the Netherlands, and France is generating parallel SMT equipment procurement for wafer-level and advanced packaging applications.

Europe's medical device industry, with Germany, the UK, and France hosting globally significant medical electronics manufacturers, sustains demand for ISO 13485-validated SMT equipment at premium specifications. The EU's progressive implementation of the Medical Device Regulation (MDR EU 2017/745) is compelling medical device manufacturers to upgrade production equipment and process validation documentation, creating structured upgrade demand for certified SMT equipment platforms across European medical electronics production facilities.

- Germany SMT Equipment Market Landscape

Germany holds approximately 26% of the Europe SMT equipment market the region's largest national share anchored by the global concentration of automotive electronics Tier-1 suppliers in the country's industrial heartland. Bosch, Continental, Infineon, and OSRAM operate large automotive-grade SMT production facilities that are undergoing systematic capacity expansion and specification upgrades for EV and ADAS electronics manufacturing. Germany's SMT equipment segment grows at approximately 13.5% CAGR through 2033, driven by the parallel automotive and EU Chips Act investment cycles. German SMT equipment manufacturers including ERSA add a supply-side technology development dimension to the country's market position.

- U.K SMT Equipment Market Landscape

The United Kingdom accounts for approximately 15% of the European SMT equipment market, with demand concentrated in aerospace electronics the UK's GKN Aerospace, BAE Systems, and Rolls-Royce operate IPC Class 3 SMT production facilities for avionics and propulsion control electronics and the medical device manufacturing sector, where the UK hosts significant global medical electronics manufacturers requiring ISO 13485-validated assembly equipment. The UK SMT equipment market is likely to grows at approximately 12.8% CAGR with EV automotive electronics investment from Jaguar Land Rover and battery gigafactory suppliers adding a new growth vector to the established aerospace and medical base.

- France SMT Equipment Market Landscape

France represents approximately 12% of the European SMT equipment market, driven by its defense electronics manufacturing base including Thales, Safran, and MBDA SMT production for avionics, missile guidance, and radar systems and the growing semiconductor investment under the EU Chips Act that is expanding French semiconductor packaging capacity at STMicroelectronics and Soitec facilities. France's SMT market grows at approximately 12.5% CAGR through 2033, with defense electronics' IPC Class 3 requirements sustaining premium equipment specifications.

- Italy SMT Equipment Market Landscape

Italy holds approximately 10% of the European SMT equipment market, with demand driven by its strong industrial electronics manufacturing sector and growing energy and power systems electronics production for inverters, converters, and smart grid control equipment. Italian industrial automation companies including Leonardo and power electronics specialists are investing in SMT line upgrades to support higher-power-density PCB assembly for renewable energy inverter manufacturing an above-market-growth application aligned with Italy's NRRP clean energy investment programs.

Asia Pacific SMT Equipment Market Trends

Asia Pacific is the dominant SMT equipment market with approximately 56% global market share in 2025, anchored by the world's largest consumer electronics, semiconductor, and telecommunications manufacturing base concentrated in China, South Korea, Taiwan, and Japan. China's electronics manufacturing sector the world's largest by output operates the highest concentration of SMT equipment globally, with contract manufacturing giants including Foxconn, Luxshare, and BYD Electronics operating thousands of SMT production lines across their industrial parks.

The region's leadership is being reinforced by a new investment cycle driven by China's semiconductor self-sufficiency drive under its 14th Five-Year Plan, South Korea's semiconductor and display manufacturing expansion, and India's Production-Linked Incentive (PLI) scheme for electronics manufacturing that is attracting first-time SMT equipment investment from Apple supply chain partners and EV battery manufacturers establishing Indian production operations. ASEAN nations Vietnam, Thailand, and Malaysia are expanding electronics manufacturing capacity attracting supply chain diversification investment from global OEMs.

- China: World's Largest SMT Equipment Deployment and Domestic Manufacturing Base

China holds approximately 44% of the Asia Pacific SMT equipment market, representing the world's single largest national SMT equipment procurement and installed base. China's SMT market grows at approximately 13.8% CAGR by 2033, driven by semiconductor self-sufficiency investment, EV electronics manufacturing expansion with BYD, CATL, and NIO scaling electronics assembly capacity and the domestic SMT equipment industry's rapid quality improvement enabling import substitution at mid-tier performance levels. Shenzhen remains the world's highest-density SMT equipment deployment geography by any measurable metric.

- India: PLI-Driven Electronics Manufacturing and SMT Equipment Adoption Surge

India accounts for approximately 8% of the Asia Pacific SMT equipment market and is the region's fastest-growing country market at approximately 17.5% CAGR through 2033 the highest national growth rate globally. India's PLI scheme for electronics manufacturing with approved incentives exceeding INR 40,000 crore has attracted Apple supply chain manufacturers including Foxconn, Pegatron, and Tata Electronics to establish large-scale SMT production in Tamil Nadu and Andhra Pradesh, generating their largest first-wave SMT equipment procurement events. India's domestic electronics manufacturing ambition targeting USD 300 billion in output by 2026 per MeitY is creating the most dynamic new SMT equipment market globally.

- South Korea: World-Class Semiconductor and Display SMT Innovation Hub

South Korea represents approximately 14% of the Asia Pacific SMT equipment market, operating the world's most technically advanced semiconductor and display electronics manufacturing ecosystem through Samsung Electronics, SK Hynix, and LG Electronics. South Korea's SMT equipment procurement is characterized by the highest average selling price per unit globally driven by advanced packaging, OLED display, and HBM memory module assembly requirements that specify the most capable placement and inspection equipment available. The South Korean segment grows at approximately 13.2% CAGR through 2033, with advanced inspection and testing system upgrades for chip-on-board and heterogeneous integration applications driving above-market growth.

Competitive Landscape

The global SMT equipment market is moderately consolidated at the top equipment tier, with ASM Pacific Technology (ASMPT), Fuji Corporation, Yamaha Motor (IM Division), Panasonic Connect, and JUKI Corporation collectively commanding an estimated 55–60% of placement equipment revenue sustained through decades of precision engineering investment, comprehensive global service networks, and deep OEM integration with major EMS and ODM manufacturers.

Advanced inspection equipment is more fragmented, with Koh Young Technology, Mirtec, Orbotech (KLA), and SAKI Corporation competing on AI algorithm capability and 3D measurement precision. Strategic themes include AI-driven machine learning integration for adaptive process optimization, Industry 4.0 connectivity platforms enabling MES integration, and software-as-a-service line management subscription models. Chinese domestic competitors including Yamaha-Dongguan and Shenzhen Gks are intensifying mid-tier competition, pressuring Japanese and Korean incumbents to accelerate premium technology differentiation.

Key Developments:

- In May 2025, Lumel S.A. expanded its manufacturing capabilities by launching its fourth SMT (Surface-Mount Technology) production line for electronics assembly. The new investment significantly enhances production capacity while improving precision, quality control, and operational flexibility in electronics manufacturing. Supported by European Union funding under the FENG.01.01-IP.01-003E/23 program, the expansion represents a strategic advancement in Lumel’s automation portfolio, particularly supporting the development of technologically advanced solutions such as the CZIP series medium-voltage protection relays.

- March 2025: ASMPT launched its SIPLACE SX Ultra high-speed placement system featuring AI-powered adaptive placement optimization achieving 120,000 CPH with ±15 micron placement accuracy, targeting 5G RF module and advanced automotive ECU assembly applications globally.

- October 2024: Koh Young Technology introduced its Zenith Ultra 3D AOI system incorporating generative AI defect detection achieving false-call rates below 0.3% setting a new industry benchmark for advanced inspection performance in IPC Class 3 automotive and medical PCBA manufacturing environments.

- May 2024: Fuji Corporation announced a strategic partnership with Siemens Digital Industries to integrate Fuji's SMT equipment control data with Siemens Opcenter MES, enabling real-time PCBA process traceability and quality analytics across complete SMT production lines for automotive Tier-1 manufacturer customers.

Companies Covered in SMT Equipment Market

- ASMPT Limited

- Fuji Corporation

- Yamaha Motor Co. Ltd. (IM Division)

- Panasonic Connect Co. Ltd.

- JUKI Corporation

- Koh Young Technology

- Mirtec Co. Ltd.

- Orbotech Ltd. (KLA Corporation)

- SAKI Corporation

- ERSA GmbH

- Heller Industries

- Mycronic AB

- Nordson Corporation (Asymtek)

- Rehm Thermal Systems GmbH

Frequently Asked Questions

The global SMT equipment market is valued at approximately US$ 6.1 billion in 2026, growing from US$ 3.2 billion in 2020 at a historical CAGR of 11.1% (2020–2025). The market is projected to reach US$ 14.2 billion by 2033, expanding at a CAGR of 12.8% representing an incremental opportunity of US$ 8.1 billion driven by semiconductor manufacturing reshoring, 5G network rollout, and automotive electrification requiring expanded electronics manufacturing automation solutions globally.

The primary demand drivers are the U.S. CHIPS and Science Act (USD 52.7 billion) and EU Chips Act (EUR 43 billion) semiconductor manufacturing investments generating greenfield SMT equipment procurement events, GSMA Intelligence's projection of 5.9 billion 5G connections by 2030 driving automated PCB assembly systems investment for base station PCBA production, and the IEA's documentation of 14 million EV sales in 2023 compelling automotive Tier-1 suppliers to invest in IPC Class 3-capable SMT production capacity.

Placement Equipment leads with approximately 38% market share in 2026. Modern high-speed placement machines from ASMPT, Fuji Corporation, and Yamaha Motor achieve 50,000–100,000 CPH at ±15–50 micron accuracy capabilities that define the throughput and quality ceiling of every SMT production line globally. Placement equipment's dominance is reinforced by its position as the highest per-unit capital investment in a typical SMT line and by the fastest technology obsolescence cycle driven by component miniaturization and accuracy requirement escalation.

Asia Pacific leads the global SMT equipment market with approximately 56% market share in 2026. China is the dominant country within the region at approximately 44% of Asia Pacific revenue, operating the world's largest consumer electronics and EV battery electronics SMT equipment installed base. South Korea contributes world-leading semiconductor and display SMT technology demand, and India is the fastest-growing national market at approximately 17.5% CAGR driven by PLI scheme-backed Apple supply chain manufacturers establishing large-scale SMT operations.

The highest-impact opportunity is AI-powered Automated Optical Inspection (AOI) system adoption, where companies including Koh Young Technology and Mirtec are demonstrating false-call rates below 0.5% in production deployments significantly below legacy 2D systems. As automotive IPC Class 3 zero-defect requirements and FDA 21 CFR Part 820 medical device traceability mandates structurally compel inspection system upgrades, AI-integrated inspection equipment is transitioning from competitive differentiation to mandatory production qualification creating above-market-growth procurement demand at premium price points through 2033.

The leading companies in the global SMT equipment market include ASMPT Limited, Fuji Corporation, Yamaha Motor (IM Division), Panasonic Connect, JUKI Corporation, Koh Young Technology, Mirtec Co., Ltd., Orbotech (KLA), SAKI Corporation, ERSA GmbH, Mycronic AB, and Nordson Corporation (Asymtek). Market leaders compete on placement accuracy and CPH throughput, AI inspection algorithm capability, Industry 4.0 MES integration depth, and the breadth of IPC class certification with ASMPT and Fuji commanding the largest global installed bases by cumulative unit volume.