- Automation & Robotics

- Fire Safety Equipment Market

Fire Safety Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Fire Safety Equipment Market by Technology Type (Active Fire Protection Systems, Passive Fire Protection Systems), Solution (Fire Detection, Fire Suppression), Application (Commercial, Industrial, Residential), and Regional Analysis for 2026 - 2033

Fire Safety Equipment Market Size and Trends Analysis

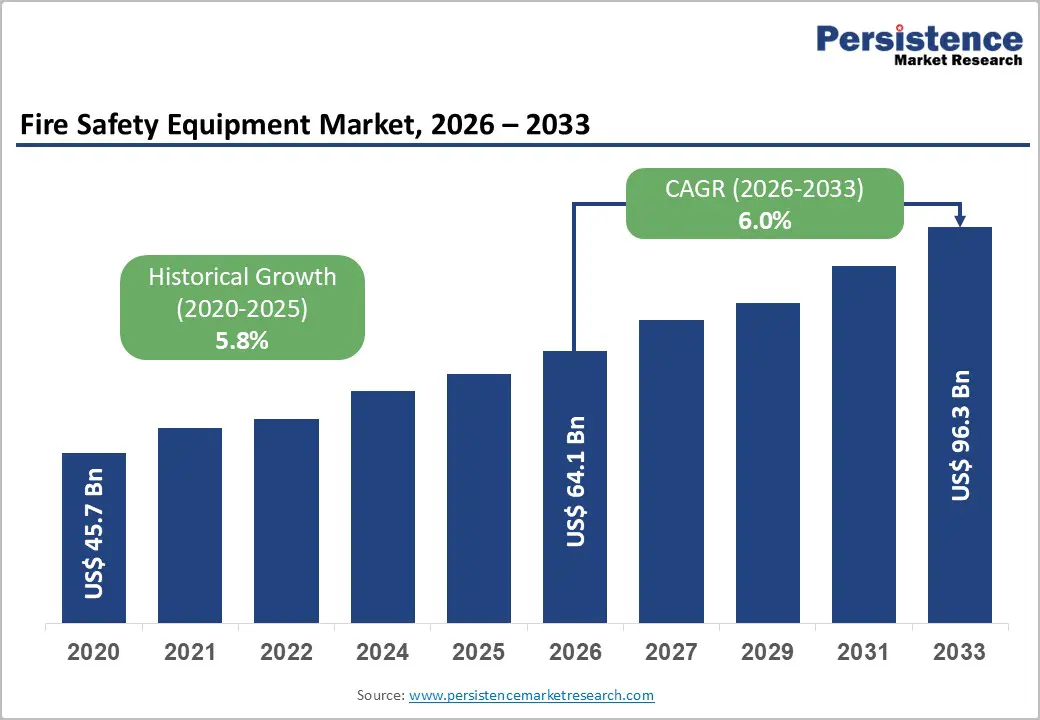

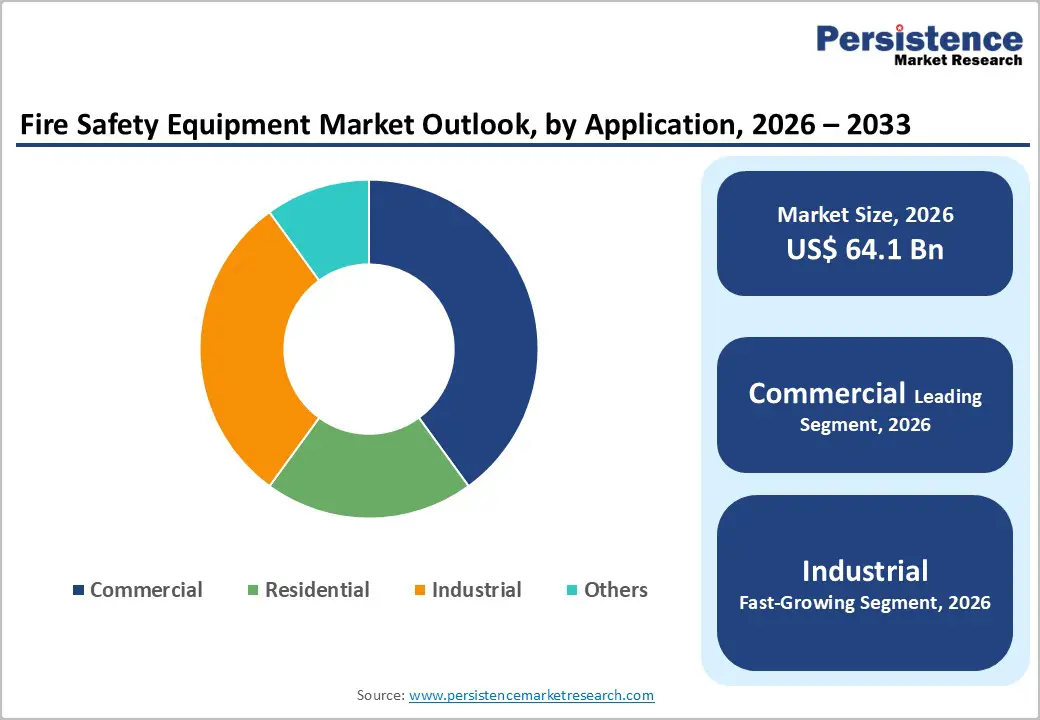

The global fire safety equipment market size is likely to be valued at US$64.1 billion in 2026 and is expected to reach US$96.3 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by stringent regulatory enforcement, rising urban density, and increasing adoption of smart detection and suppression systems across commercial, industrial, and residential sectors.

Fire risk remains a critical concern, with the National Fire Protection Association reporting that U.S. fire departments responded to approximately 1.39 million fires in 2024, resulting in significant life and property losses. The World Health Organization highlights that burns cause over 180,000 deaths annually worldwide, emphasizing the need for advanced prevention infrastructure. Market growth reflects a shift toward integrated, IoT-enabled life-safety systems, with strong momentum in Asia Pacific due to rapid urbanization and infrastructure expansion.

Key Industry Highlights:

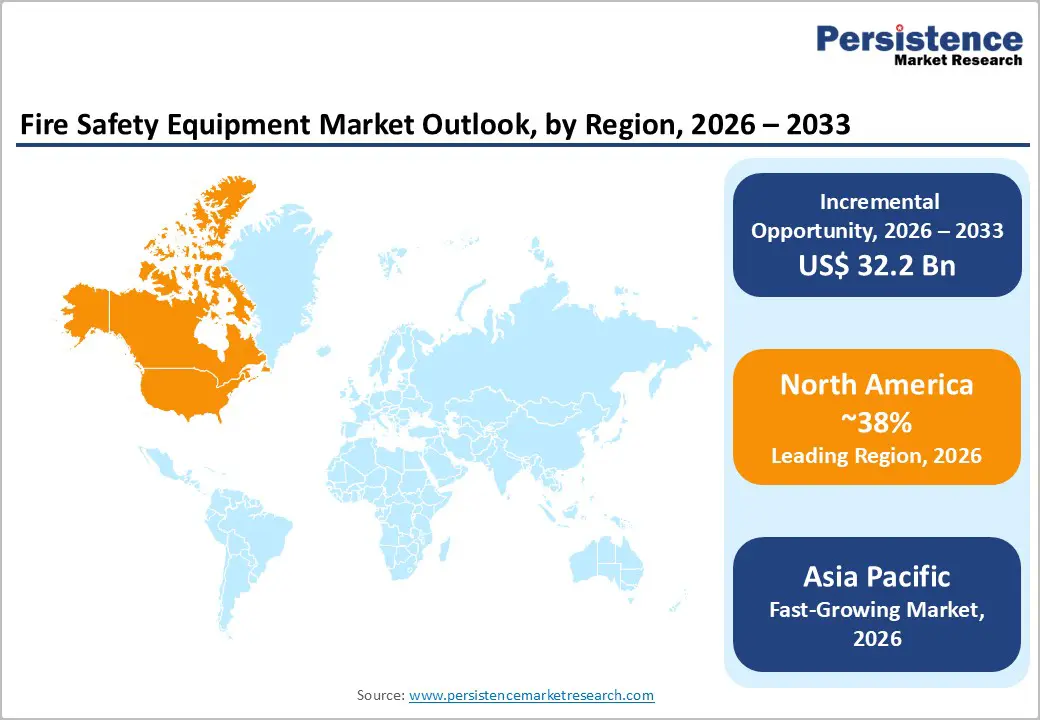

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by stringent fire safety regulations, strong retrofit demand, and widespread adoption of integrated and smart life-safety systems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid urbanization, industrial expansion, and increasing adoption of updated fire safety codes across emerging economies.

- Leading Technology Type: Active fire protection systems are projected to represent the leading technology type in 2026, accounting for 62% of the revenue share, driven by mandatory safety regulations, real-time hazard response requirements, and widespread deployment across commercial and industrial infrastructure.

- Leading Solution: Fire detection is anticipated to be the leading solution, accounting for over 60% of the revenue share in 2026, supported by the need for early warning systems, increasing adoption of smart sensors, and regulatory emphasis on preventive fire safety measures.

- Key Opportunity: The key market opportunity is the shift toward smart, IoT-enabled, and sustainable fire safety systems driven by rapid urbanization, data centers, energy storage growth, and large-scale infrastructure modernization.

DRO Analysis

Driver - Rising Fire-Loss Exposure in High-Density Environments

Rising fire-loss exposure in high-density environments is a key driver of the fire safety equipment market as urbanization and vertical infrastructure development increase occupancy levels and asset concentration. High-rise buildings, commercial complexes, and industrial clusters significantly amplify fire risk due to interconnected systems and rapid fire spread potential.

The National Fire Protection Association reports that U.S. fire departments respond to over 1.3 million fires annually, highlighting persistent exposure risk. Growing population density in cities and expansion of mixed-use infrastructure strengthen demand for advanced detection, suppression, and integrated life-safety systems.

This rising risk environment is also influencing regulatory tightening and insurance-driven compliance across regions. Authorities are mandating stricter installation of fire alarms, sprinklers, and emergency response systems in high-occupancy structures. Industries such as commercial real estate, healthcare, and manufacturing are increasingly prioritizing automated fire protection to reduce operational disruptions and asset losses.

Restraint - Retrofitting Complexity in Occupied Assets

Many older commercial and industrial facilities were not designed for modern fire detection or suppression systems, making integration technically challenging. Constraints such as limited space for wiring, compatibility issues with legacy systems, and compliance alignment with updated codes slow adoption. The International Code Council highlights that continuous code evolution increases complexity for retrofit compliance in aging infrastructure.

This challenge is intensified by cost sensitivity and downtime concerns among building owners. Occupied facilities such as hospitals, offices, and retail centers often avoid extensive retrofit work due to business interruption risks. In industrial environments, production halts during installation can result in significant revenue loss.

Opportunity - Battery-Storage and Data-Center Safety

Battery-storage systems and data-center infrastructure represent a major growth opportunity for the fire safety equipment market due to rising energy transition and digitalization trends. Lithium-ion battery installations in renewable energy storage and electric vehicle ecosystems introduce higher thermal runaway risks, requiring advanced fire detection and suppression technologies.

Hyperscale data centers demand highly reliable, non-water-based fire protection systems to prevent equipment damage and downtime. The National Fire Protection Association (2026) has issued updated guidelines emphasizing specialized suppression and early detection systems for energy storage and high-value digital infrastructure environments.

This opportunity is strengthened by the rapid expansion of cloud computing, AI workloads, and grid-scale energy storage projects. Operators are investing in clean agent suppression systems, gas-based fire control, and AI-enabled thermal monitoring solutions to enhance safety without disrupting operations. Increasing regulatory focus on energy storage safety standards is also accelerating technology adoption.

Category-wise Analysis

Technology Type Insights

Active fire protection systems are expected to lead the fire safety equipment market, accounting for approximately 62% of revenue in 2026, driven by mandatory safety codes, real-time hazard response needs, and widespread deployment in commercial and industrial infrastructure. These systems include alarms, sprinklers, and centralized control panels that immediately respond during fire events, reducing loss severity. A notable example includes modern high-rise commercial towers in cities, where integrated sprinkler and alarm systems are installed across every floor to ensure instant fire containment and occupant safety compliance.

Passive fire protection systems are likely to represent the fastest-growing segment, supported by increasing retrofit activity and stricter building code upgrades across aging infrastructure. These systems focus on fire resistance through structural compartmentation, fire-rated walls, coatings, and barriers that prevent fire spread and protect structural integrity. For example, retrofitting of aging logistics warehouses in Europe and Asia, where fire-resistant wall systems and structural sealing materials are being added to improve safety standards while minimizing operational disruption.

Solution Insights

Fire detection is projected to lead the market, capturing around 60% of the revenue share in 2026, driven by smart sensing technologies, wireless alarms, and integrated building analytics that enhance real-time hazard identification. For instance, commercial office complexes, where smoke detectors and connected alarm networks are installed throughout HVAC-integrated floors to ensure immediate alerts and rapid evacuation response.

Fire suppression is likely to be the fastest-growing solution, driven by stricter insurance requirements and increasing deployment of automated suppression systems such as gas-based and sprinkler-based technologies. A notable example includes lithium-ion battery storage facilities, where advanced suppression systems are deployed to control thermal runaway incidents and prevent cascading fire damage, ensuring operational safety in high-energy-density environments.

Application Insights

Commercial is expected to lead the fire safety equipment market, accounting for approximately 50% of revenue in 2026, driven by high occupancy buildings, strict regulatory enforcement, and continuous modernization of offices, retail spaces, healthcare, and hospitality infrastructure. The National Fire Protection Association highlights commercial buildings as high-priority environments for integrated fire protection. For example, large shopping malls have interconnected sprinkler systems, and emergency alarm networks are installed to manage high footfall and ensure rapid evacuation during emergencies.

The industrial segment is likely to represent the fastest-growing segment, supported by rising investments in automation, energy infrastructure, and warehouse safety systems, where fire risks are higher due to flammable materials and complex operations. For instance, automated manufacturing plants, where advanced fire detection and suppression systems are integrated into production lines and storage zones to reduce downtime risks and ensure continuous operational safety in high-risk industrial environments.

Regional Insights

North America Fire Safety Equipment Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by strict regulatory frameworks, strong insurance enforcement, and widespread adoption of advanced life-safety systems across commercial and industrial infrastructure. A notable example includes Johnson Controls, which is expanding its intelligent fire detection and integrated building safety solutions across large-scale commercial complexes and data centers.

U.S. Fire Safety Equipment Market Trends

The U.S. dominates the regional market, driven by strict enforcement of NFPA fire codes, insurance-linked compliance, and large-scale adoption of smart fire detection systems. Recent developments include increased installation of IoT-enabled smoke detectors and AI-based building monitoring in commercial towers and data centers.

Canada Fire Safety Equipment Market Trends

Canada is a significant market for fire safety equipment supported by updated national building codes, rising urban construction, and increased awareness of fire safety compliance. Recent trends include stronger adoption of interconnected alarm systems in residential complexes and public infrastructure upgrades in cities such as Toronto and Vancouver.

Europe Fire Safety Equipment Market Trends

Europe is likely to be a significant market for fire safety equipment in 2026, due to stringent EU safety regulations, sustainability-focused construction standards, and the modernization of aging infrastructure across commercial and industrial sectors. For example, Siemens Building Technologies is deploying advanced fire detection and building management systems across smart infrastructure and industrial facilities.

U.K. Fire Safety Equipment Market Trends

The U.K. is a significant market for fire safety equipment, supported by strong regulatory reforms following major fire safety incidents and increasing compliance requirements in residential and commercial buildings. The country has seen widespread replacement of legacy fire systems in high-rise residential towers, public housing, and commercial complexes, supported by stricter enforcement of building safety standards and post-Grenfell regulatory changes.

Germany Fire Safety Equipment Market Trends

Germany dominates the regional market, driven by its strong industrial base, strict fire safety regulations, and advanced manufacturing sector. The country is witnessing increased deployment of automated fire suppression systems in automotive, chemical, and engineering industries. The government’s focus on upgrading industrial safety infrastructure and reducing workplace hazards is supporting demand.

Asia Pacific Fire Safety Equipment Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the fire safety equipment industry in 2026, driven by rapid urbanization, large-scale infrastructure development, and increasing enforcement of fire safety regulations across emerging economies. For example, Honeywell International, Inc., is expanding its advanced fire safety and building automation solutions across Asia Pacific smart cities and industrial projects.

China Fire Safety Equipment Market Trends

China dominates the regional market, driven by massive urbanization, rapid industrial expansion, and large-scale infrastructure development, including smart cities, metro networks, and high-rise commercial complexes. The country is witnessing strong adoption of advanced fire detection and suppression systems integrated with IoT-based monitoring and centralized building management platforms.

India Fire Safety Equipment Market Trends

India is a significant market for fire safety equipment, supported by rapid urbanization, expanding commercial real estate, and stricter enforcement of fire safety norms under the National Building Code (NBC). The market is witnessing strong adoption of fire detection and alarm systems in IT parks, residential high-rises, and metro infrastructure projects. Recent regulatory tightening after several urban fire incidents has increased compliance-driven installations across public buildings and hospitals.

Competitive Landscape

The global fire safety equipment market exhibits a moderately fragmented structure, driven by the presence of multinational corporations, regional manufacturers, and specialized safety solution providers competing across detection, suppression, and integrated life-safety systems. The market is characterized by strong regulatory influence from fire codes and building safety standards, which compels companies to continuously upgrade product offerings with smart, connected, and IoT-enabled technologies.

With key leaders including Honeywell International, Inc., Johnson Controls, Siemens Building Technologies, Robert Bosch GmbH, and Eaton, the industry shows strong consolidation in advanced fire safety technologies. These players compete through innovation in smart fire detection, cloud-based monitoring platforms, integrated building automation systems, and AI-driven risk analytics.

Key Industry Developments:

- In April 2026, Fireaway Inc. announced the launch of its UltraSense™ Environmental Sensing Platform, designed for clean energy fire protection applications, including battery energy storage systems (BESS), solar, and wind infrastructure. The system focuses on early detection of fire risks by monitoring environmental and electrical anomalies such as temperature changes, humidity variation, and battery off-gassing.

- In April 2026, Jactone Products Ltd introduced its new Eco PLUS Fluorine-Free Fire Extinguishers, marking a significant shift toward environmentally sustainable fire safety solutions. The new range eliminates PFAS-based chemicals while maintaining high-performance fire suppression capabilities for Class A and Class B fires.

Companies Covered in Fire Safety Equipment Market

- Eaton

- Gentex Corp.

- Halma plc

- Hochiki Corp.

- Honeywell International, Inc.

- Johnson Controls

- Napco Security Technologies, Inc.

- Nittan Company Ltd.

- Robert Bosch GmbH

- Siemens Building Technologies

- Space Age Electronics

- United Technologies Corp.

Frequently Asked Questions

The global fire safety equipment market is projected to reach US$64.1 billion in 2026.

The fire safety equipment market is driven by stringent fire safety regulations, rising urbanization, increasing fire incidents, and growing adoption of smart and automated fire detection and suppression systems across commercial, industrial, and residential infrastructure.

The fire safety equipment market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

Key market opportunities in the fire safety equipment market include the rising demand for smart IoT-based fire safety systems, rapid expansion of data centers and battery energy storage infrastructure, and increasing retrofit upgrades in aging commercial and industrial buildings.

Eaton, Gentex Corp., Halma plc, Hochiki Corp., Honeywell International, Inc., Johnson Controls, and Napco Security Technologies, Inc. are the leading players.