- Automation & Robotics

- Automatic Vehicle Washing System Market

Automatic Vehicle Washing System Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automatic Vehicle Washing System Market by System Type (Tunnel (Conveyor) Systems, Roll-Over / In-Bay Automatic Systems, Self-Service Systems), Installed Location (Fuel Stations / Gas Stations, Dedicated Car Wash Facilities, Shopping Malls & Parking Areas, Airports & Transport Hubs, Hotels & Resorts, Service Stations / Workshops), End Use (Automotive, Railways, Aerospace), and Regional Analysis 2026 - 2033

Automatic Vehicle Washing System Market Trends & Analysis

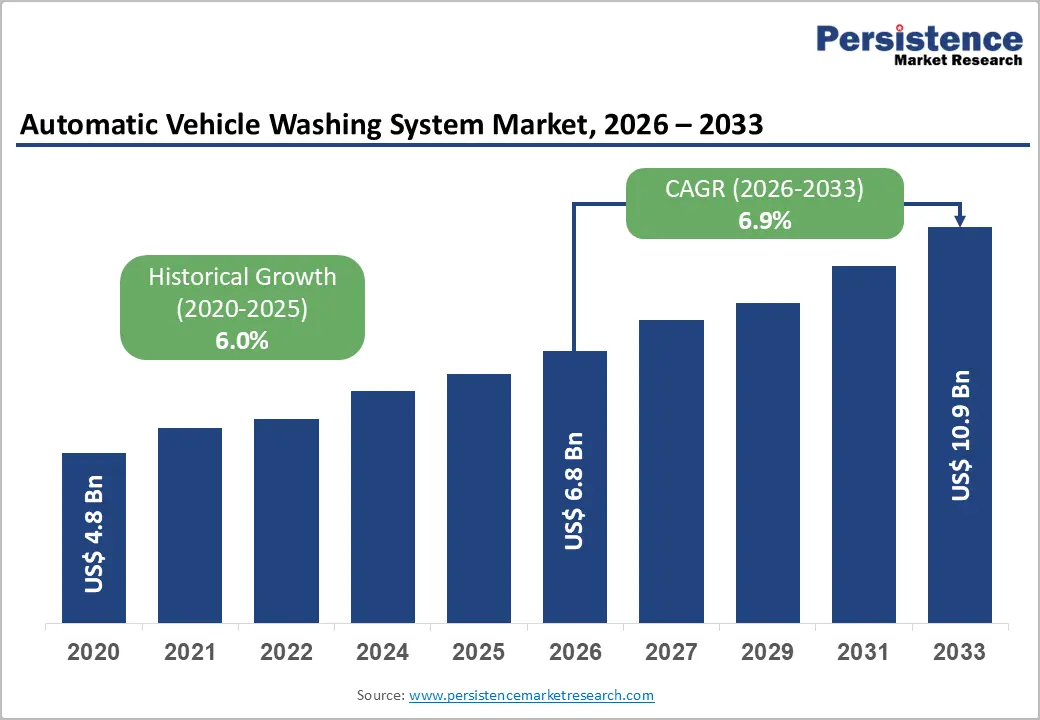

The global automatic vehicle washing system market size is anticipated at US$ 6.8 Bn in 2026 and is projected to reach US$ 10.9 Bn by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

From a driver in suburban Chicago gliding through a 150-car-per-hour express tunnel wash during a lunch break, to a fleet operator in Dubai running automated bus wash systems overnight, and a Japanese railway authority deploying contactless train wash gantries for Shinkansen maintenance, automated vehicle washing is redefining vehicle care efficiency across every transportation segment globally.

Surging global vehicle parc exceeding 1.4 billion units, intensifying wash frequency demand, stringent water conservation regulations compelling the adoption of closed-loop automatic wash systems that consume 60-70% less water than manual alternatives, and subscription-based membership wash business model proliferation generating recurring facility investment are the primary growth drivers. IoT-enabled wash monitoring, touchless sensor technology, and AI-powered water recycling systems are expanding per-installation value and operational efficiency.

Key Industry Highlights

- Leading System Type: Tunnel (Conveyor) Systems lead at 39.2% share; Roll-Over / In-Bay Automatic Systems grow fastest at 7.0% CAGR, driven by compact footprint deployment at fuel stations and urban parking facilities.

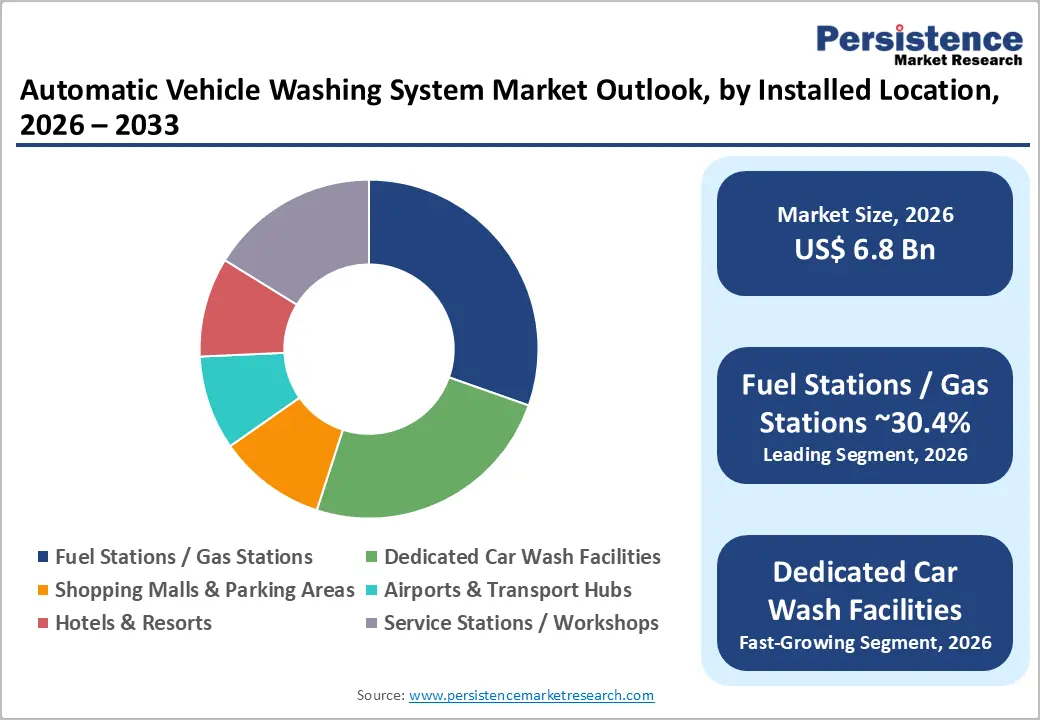

- Leading Installed Location: Fuel Stations / Gas Stations lead at 30.4% share; Dedicated Car Wash Facilities grow fastest at 7.4% CAGR, driven by subscription membership model operator expansion across North America and Europe.

- Leading End Use: Automotive dominates at 90.3% share; Railways (Train Wash Systems) grow fastest at 6.2% CAGR, supported by high-speed rail and metro network expansion investment in China, India, and Europe.

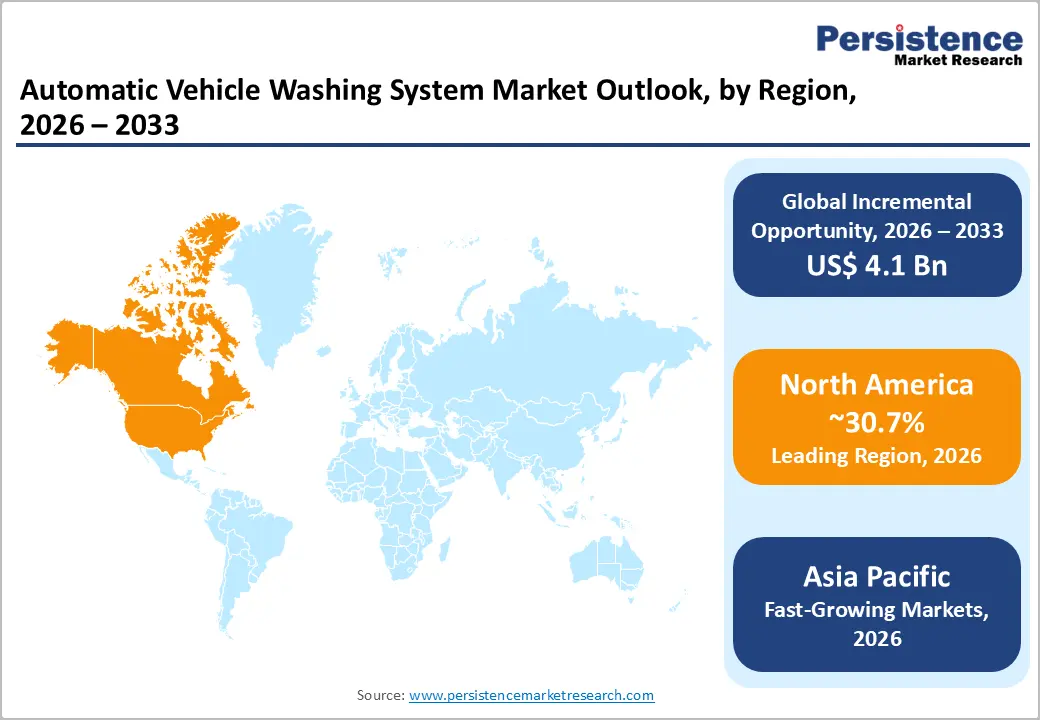

- Regional Performance: North America leads at 30.7% share with the U.S. at US$ 1.5 Bn; Asia Pacific grows fastest at 14.0% CAGR, led by China at US$ 497.3 Mn and India at US$ 245.9 Mn in 2026.

- Strategic Developments: WashTec AG's SoftWash IoT platform expansion (January 2025) and Aerowash AB's robotic aircraft wash deployment at Swedavia airports (June 2024) are setting new benchmarks for digital wash management and aerospace segment diversification.

Market Dynamics Analysis

Market Drivers

Escalating Global Vehicle Ownership and Urban Car Wash Infrastructure Demand

The International Organization of Motor Vehicle Manufacturers (OICA) documented global vehicle production exceeding 93 million units in 2023, with the global vehicle parc surpassing 1.46 billion vehicles, generating compounding annual demand for professional vehicle washing services across urban and suburban markets worldwide.

Rising vehicle ownership rates in emerging economies, China adding 27 million new vehicle registrations in 2023, India recording 4.2 million passenger vehicle sales, are directly expanding the addressable wash service base across markets where automatic system density remains significantly below developed market benchmarks.

The International Carwash Association (ICA) estimates that approximately 72% of vehicle owners in the U.S. use professional car wash services at least once monthly, generating a recurring wash-service demand base that incentivizes investment in automatic systems at fuel stations, dedicated facilities, and retail locations.

Urban densification trends, with McKinsey projecting that 68% of the global population will reside in cities by 2050, are compressing the residential space available for manual home washing while expanding the urban consumer base that relies on professional automatic car wash services, creating sustained, long-term infrastructure investment demand across commercial wash facility operators globally through 2033.

Stringent Water Conservation Regulations Compelling Transition to Closed-Loop Automatic Wash Systems

Municipal and state-level water-use regulations across drought-affected regions in the U.S., EU, and Australia mandate professional car wash water recycling compliance while restricting residential driveway washing, compelling commercial operators to invest in closed-loop automatic wash systems that recycle 80-90% of wash water per vehicle cycle. California's State Water Resources Control Board restrictions on potable water use for vehicle washing, complemented by similar ordinances in Texas, Arizona, and Nevada, have driven the accelerated installation of tunnel and roll-over systems incorporating water reclamation technology since 2022.

The European Union's Urban Wastewater Treatment Directive revision, strengthening effluent quality and volume limits for commercial washing operations across Member States, is driving equipment upgrade investment cycles at European fuel stations and dedicated car wash facility operators transitioning to automatic closed-loop water management systems.

Retail automatic car wash systems consume 60% less water per vehicle than residential manual washing (ICA benchmark data), positioning automatic wash systems as both regulatory compliance infrastructure and environmental responsibility demonstration platforms for fuel station networks, shopping center operators, and fleet wash service providers seeking municipal water use permit compliance across regulated markets globally.

Restraints - Zoning and Land Use Regulatory Barriers Constraining New Automatic Car Wash Facility Development

Automatic car wash facility development, particularly high-throughput tunnel systems requiring 80+ linear feet of building footprint plus stacking lane infrastructure, faces increasingly restrictive municipal zoning regulations governing commercial car wash facility noise levels, lighting, traffic queue management, drainage, and proximity to residential areas across developed markets. U.S. municipalities in California, New York, and Illinois have enacted specific commercial car wash facility development permit requirements that extend approval timelines by 12-24 months.

In Europe, EU Urban Runoff Directive compliance for wash water drainage systems adds permitting complexity, constraining the deployment velocity of new dedicated facilities and risking an estimated 15-20% reduction in projected greenfield facility openings annually.

Supply Chain Fragility in Precision Wash System Components and Electronic Control Modules

Automatic vehicle washing systems incorporate precision high-pressure pump assemblies, corrosion-resistant brush and foam application modules, programmable logic controllers (PLCs), and IoT-integrated sensor arrays sourced from specialized European and Asian component manufacturers.

The 2021-2023 global semiconductor shortage, which extended component lead times by 18-26 weeks for wash system PLCs and electronic control modules, demonstrated the sector's structural supply chain vulnerability, impacting new system delivery timelines across North American and European operators. Ongoing geopolitical trade policy uncertainty between the U.S. and China risks reintroducing similar supply disruption scenarios for wash system electronic and mechanical precision components through the mid-2030s forecast horizon.

Opportunities - Subscription-Based Membership Wash Model Driving Recurring Revenue and System Utilization Optimization

The subscription-based unlimited wash membership model, pioneered by Mister Car Wash, Driven Brands, and Zips Car Wash across the U.S., is transforming the automatic vehicle washing industry's revenue structure from transactional per-wash pricing toward predictable monthly recurring revenue, while simultaneously increasing average wash facility utilization rates by 35-45% versus non-subscription peer facilities.

The International Carwash Association reports that approximately 80% of U.S. tunnel car wash operators now offer subscription programs, generating average monthly revenue per member of US$25-35, which substantially outperforms single-wash transaction economics. This model is rapidly expanding internationally, with Istobal, WashTec, and Otto Christ deploying subscription architecture across European markets and initial APAC pilot programs emerging in Japan and Australia.

For automatic vehicle washing system manufacturers, the subscription model creates a demand accelerator: subscription program operators require higher-specification, higher-throughput tunnel and roll-over systems to sustain service quality under elevated wash volume commitments. The global subscription car wash service market is estimated to exceed US$ 3.5 Bn by 2030, with automatic system hardware procurement forming the primary capital investment enabler for subscription model expansion across emerging global markets.

Railway and Aerospace Automatic Wash System Expansion as Underserved Institutional Segments

Railway transit authorities and aerospace ground service operators represent structurally underserved segments for automatic vehicle wash systems, where operational hygiene, aerodynamic performance, and passenger perception requirements mandate regular automated exterior cleaning, yet dedicated automatic wash system penetration remains low relative to the automotive segment. Transport for London's fleet of 600+ Elizabeth Line rolling stock units, SNCF's 3,000+ high-speed train fleet in France, and Indian Railways' 13,000+ locomotive fleet collectively represent institutional procurement opportunities for fixed-gantry automated train wash systems that market leaders Westmatic Corporation and Aquarama are actively targeting.

In aerospace ground services, IATA's Airport Handling Manual establishes aircraft exterior cleaning frequency requirements that create recurring demand for automated aircraft wash systems, with Aerowash AB's robotic aircraft washing technology demonstrating a 70% reduction in labor costs compared to manual wash crews at major European hub airports.

The combined Railway and Aerospace automatic wash system addressable market is estimated at US$ 0.8-1.2 Bn by 2030, growing at approximately 6.2% CAGR, representing an incrementally significant diversification opportunity for system manufacturers extending beyond the saturating automotive wash segment into institutional transit and aviation maintenance procurement programs globally.

Category-wise Analysis

System Type Insights

Tunnel (Conveyor) Systems lead the system type segment with a 39.2% share in 2026. Tunnel systems' leadership reflects their decisive throughput advantage, processing 120-180 vehicles per hour versus 10-20 vehicles per hour for Roll-Over / In-Bay systems, making them the economically optimal investment for high-traffic locations including fuel station forecourts, highway service areas, and dedicated car wash facilities generating strong peak-hour vehicle volumes.

Subscription membership programs, now the dominant commercial model for U.S. and increasingly European car wash operators, require tunnel system throughput capacity to remain commercially viable under unlimited wash commitments. Roll-Over / In-Bay systems retain a significant share across compact footprint locations, while Self-Service systems serve price-sensitive consumer segments. The alignment of tunnel systems' commercial and subscription models sustains their dominant position through 2033.

Roll-Over / In-Bay Automatic Systems are the fastest-growing system type at 7.0% CAGR through 2033. Compact footprint requirements suitable for fuel station and parking facility integration, lower capital investment thresholds compared to tunnel systems, and advances in touchless technology improving wash quality for premium vehicle segments are collectively driving Roll-Over / In-Bay system adoption across emerging markets and space-constrained urban locations globally.

Installed Location Insights

Fuel Stations / Gas Stations lead the installed location segment with a 30.4% share in 2026. Fuel stations retain installed location leadership through their unmatched vehicle visit frequency advantage, capturing impulse wash purchases from the 40+ million daily U.S. fuel station customer visits (American Petroleum Institute data) and equivalent high-frequency traffic across European and Asian fuel retail networks.

Major fuel station networks, including Shell, BP, TotalEnergies, and ExxonMobil, have systematically integrated automatic car wash bays as revenue diversification investments, with IHS Markit data indicating that fuel station car wash operations generate 15-25% of total forecourt retail revenue in high-penetration European markets. Dedicated Car Wash Facilities are growing in share through subscription model expansion, but the convenience of fuel station locations sustains their volume leadership through 2033.

Dedicated Car Wash Facilities are the fastest-growing installed base, with a 7.4% CAGR through 2033. Subscription unlimited wash model expansion, real estate consolidation by multi-site car wash chain operators, including Mister Car Wash and Driven Brands, and purpose-built tunnel facility investment optimizing throughput and service range are driving dedicated facility procurement acceleration across North America and emerging European markets.

End-user Insights

Automotive leads the end-use segment with a 90.3% share in 2026, encompassing Passenger Vehicles, Commercial Vehicles, and Off-Highway Vehicles. Automotive's near-total segment dominance reflects the global vehicle parc of 1.46 billion units, generating an unmatched wash demand base across all automatic system configurations and installed location categories.

Passenger vehicles drive wash visit frequency across consumer-facing facilities, while commercial vehicle fleet operators increasingly mandate automated wash cycles for regulatory compliance, vehicle livery maintenance, and operational efficiency. Off-highway vehicle segments contribute a niche but growing automated wash requirements across mining, construction, and agricultural fleet operations. Railway and Aerospace end uses are expanding but remain structurally volume-subordinate through 2033, due to fleet-unit count differentials.

Railways (Train Wash Systems) is the fastest-growing end use, with a 6.2% CAGR through 2033. Expanding metro rail, high-speed rail, and regional transit network investments across China, India, the EU, and the U.S. are generating new automated fixed-gantry train wash system procurement as transit authorities integrate automated exterior cleaning into rolling stock maintenance protocols for passenger presentation standards.

Regional Market Insights

North America Automatic Vehicle Washing System Market Trends

North America holds the leading 30.7% share of the global Automatic Vehicle Washing System Market in 2025, anchored by the U.S.'s mature subscription car wash industry infrastructure, dense fuel station car wash network, and continuous capital investment by multi-site express tunnel wash chain operators. The ICA's 2024 Car Wash Industry Profile records over 66,000 professional car wash locations across the U.S., with express tunnel formats posting the fastest new-opening growth rate. Water conservation regulation compliance investments across California, Texas, and the Mountain West are further driving upgrades to closed-loop wash water reclamation systems across existing and new facility installations.

U.S. & Canada: Subscription Model Proliferation and Express Tunnel System Leadership

The U.S. market is estimated at ~US$ 1.5 Bn in 2026, driven by Mister Car Wash's 500+ site tunnel system expansion program, Driven Brands' Take 5 Car Wash rollout, and state-level investment in water-use regulation compliance. Canada sustains supplementary tunnel and in-bay system procurement across Petro-Canada and Esso fuel station networks, with subscription membership model adoption accelerating across Ontario and British Columbia urban markets through 2033.

Europe Automatic Vehicle Washing System Market Trends

Europe is expected to reach 6.7% CAGR through 2033, driven by EU wastewater directive compliance requirements, WashTec and Istobal tunnel system expansion programs, and fuel station network automatic wash integration across Germany, France, the U.K., and Spain, sustaining consistent system procurement investment across all major regional markets.

Germany, U.K., France & Spain: Regulatory Compliance and Fuel Network Integration

Germany's market is estimated at ~US$ 606.7 Mn in 2026, anchored by WashTec AG's Augsburg-headquartered product development leadership, Otto Christ AG's premium tunnel system installations at Shell and Aral fuel stations, and high consumer car wash utilization rates across Germany's 49 million registered vehicle population. The U.K. sustains strong in-bay and tunnel system procurement across BP, Asda, and Tesco networks. France contributes to TotalEnergies' automatic wash facility investment, while Spain's Istobal SA serves Mediterranean regional operators with tunnel and roll-over system deployments through 2033.

Asia Pacific Automatic Vehicle Washing System Market Trends

Asia Pacific is the fastest-growing region at 14.0% CAGR through 2033, driven by rapidly expanding vehicle ownership in China and India, greenfield automatic car wash facility development supporting emerging urban middle-class vehicle care service demand, and railway transit authority automatic train wash system procurement aligned with high-speed rail network expansion programs.

China, India, Japan & ASEAN: Greenfield Infrastructure Buildout and Fleet Wash Compliance

China's market is estimated at ~US$ 497.3 Mn in 2026, driven by SINOPEC and CNPC's expansion of petrol station automatic wash bays and the proliferation of urban dedicated car wash facilities across Tier 1 and Tier 2 cities. India's market, at ~US$ 245.9 Mn, is growing through the integration of Indian Oil and HPCL's fuel retail networks and compliance with Bharat NCAP commercial vehicle wash requirements.

Japan sustains mature penetration across ENEOS and Cosmo Energy networks, while ASEAN markets, Indonesia, Thailand, and Vietnam, represent high-growth greenfield deployment opportunities through 2033.

Competitive Landscape

The global Automatic Vehicle Washing System Market is moderately fragmented, with WashTec AG, Istobal SA, and PDQ Vehicle Wash Systems collectively holding an estimated 30-35% combined revenue share, differentiating through modular tunnel system configurations, water reclamation integration, and IoT-enabled wash management platforms. Subscription model-aligned system design, touchless sensor precision, and fleet service contracts are emerging as key business model differentiators beyond hardware supply.

Water-efficient system technology investment, IoT-connected wash performance monitoring platform development, geographic expansion into Asia Pacific and Middle East emerging markets, and strategic multi-site car wash chain partnership programs define the dominant competitive strategic themes across the global automatic vehicle washing system landscape through 2033.

Key Developments

- In September 2024, Istobal SA expanded its manufacturing and distribution footprint in Brazil, establishing a Latin American regional service and assembly center targeting fuel station network operators across Brazil, Colombia, and Argentina with Roll-Over and Tunnel automatic wash system deployments.

- In June 2024, Aerowash AB secured a contract with Swedavia Airport Services to deploy its robotic aircraft exterior wash system across Stockholm Arlanda and Gothenburg Landvetter airports, reducing aircraft exterior cleaning labor consumption by 68% versus manual wash crew operations.

Companies Covered in Automatic Vehicle Washing System Market

- WashTec AG

- Istobal SA

- Otto Christ AG

- PDQ Vehicle Wash Systems

- Sonny's Enterprises LLC

- MacNeil Wash Systems

- Ryko Solutions Inc.

- Coleman Hanna Carwash Systems

- Daifuku Co. Ltd.

- KKE Wash Systems Pvt. Ltd.

- Westmatic Corporation

- Aquarama

- Aerowash AB

- EHRLE GmbH

- Oasis Car Wash Systems

Frequently Asked Questions

The automatic vehicle washing system market is valued at US$ 6.8 Bn in 2026, projected to reach US$ 10.9 Bn by 2033.

Surging global vehicle parc demand, water conservation regulatory mandates compelling closed-loop system adoption, and subscription-based membership wash business model proliferation, generating recurring automatic system investment are the primary structural growth drivers.

The automatic vehicle washing system market is projected to grow at a CAGR of 6.9% from 2026 to 2033.

Subscription unlimited wash model infrastructure expansion driving tunnel system procurement and railway and aerospace institutional automatic wash system market development represent the highest-value addressable growth opportunities through 2033.

WashTec AG, Istobal SA, Otto Christ AG, PDQ Vehicle Wash Systems, Sonny's Enterprises, MacNeil Wash Systems, Ryko Solutions, Daifuku, Westmatic, Aerowash AB, and KKE Wash Systems are the leading global participants.