- Communication Infrastructure & Services

- RF Interconnect Market

RF Interconnect Market Size, Share, and Growth Forecast, 2026 - 2033

RF Interconnect Market by Product Type (RF Cables, RF Connectors, Other), Frequency Range (High‑frequency RF interconnects, Very high‑frequency / mmWave interconnects, Others), End‑use Industry, Application, and Regional Analysis for 2026 - 2033

RF Interconnect Market Size and Trends Analysis

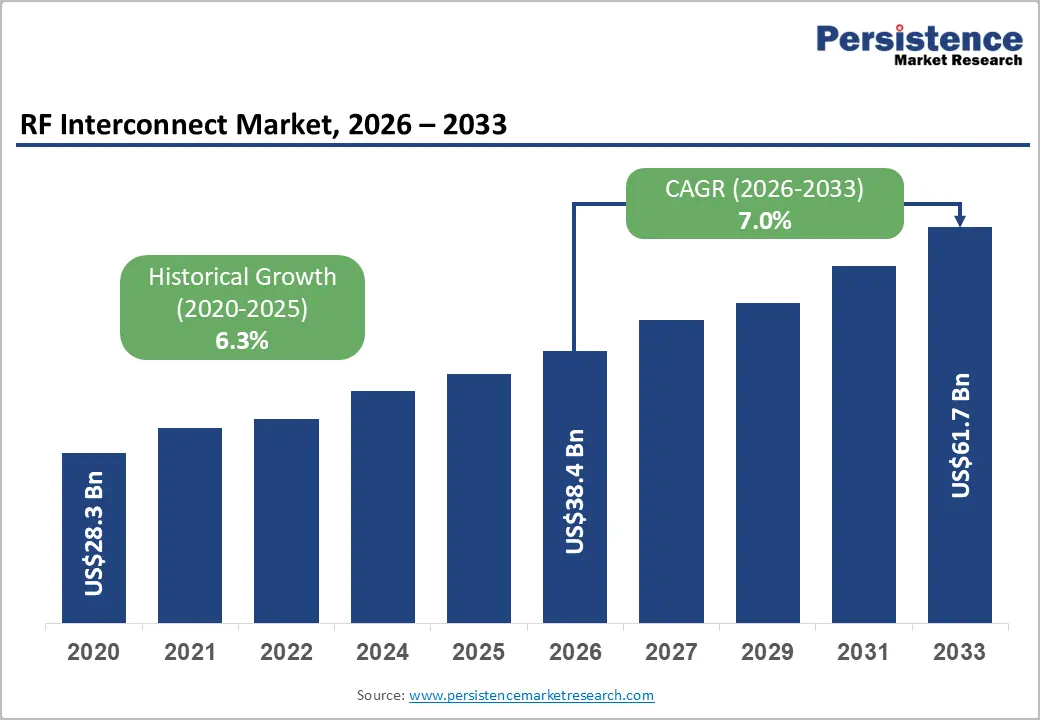

The global RF interconnect market size is likely to be valued at US$38.4 billion in 2026 and is expected to reach US$61.7 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033., driven by rapid deployment of 5G infrastructure, increasing adoption of mmWave technologies, and growing integration of high-frequency communication systems across aerospace, defense, automotive, and industrial applications.

Demand for low-loss, ruggedized, and miniaturized RF interconnect solutions continues to rise as network architectures become denser and more modular. The transition toward advanced radar systems, autonomous mobility, industrial automation, and next-generation wireless communication platforms is also increasing the technical complexity and value contribution of RF interconnect components across global supply chains.

Key Industry Highlights

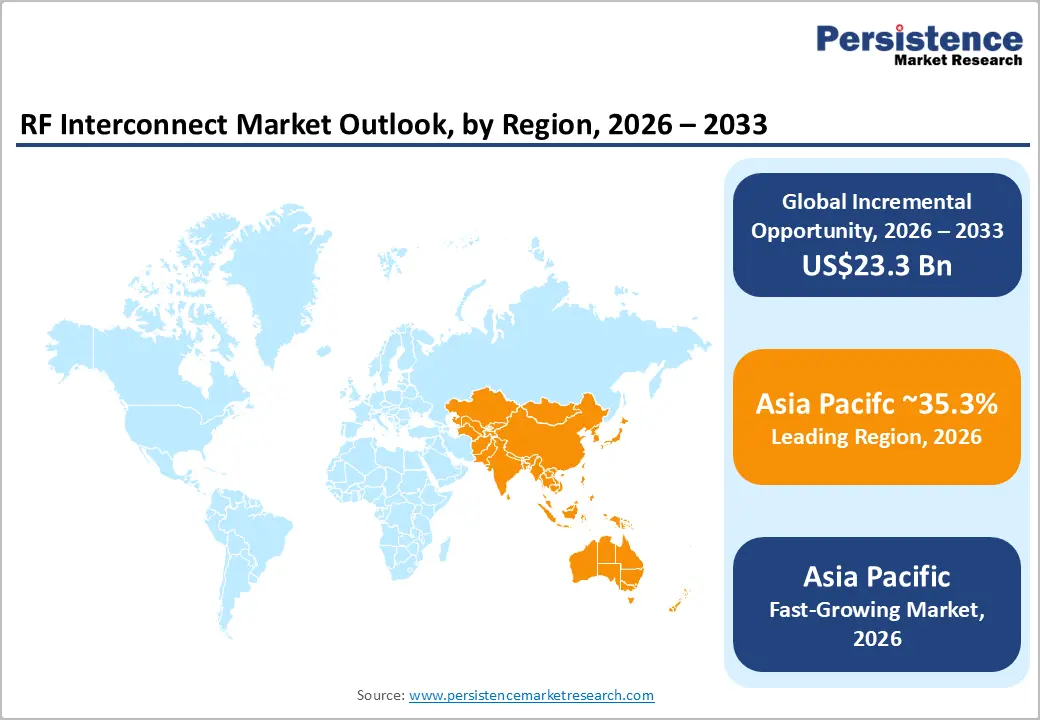

- Leading Region: Asia Pacific is projected to lead with 35.3% of market share in 2026, supported by strong telecom infrastructure expansion, large-scale electronics manufacturing, and growing automotive electronics production across China, Japan, South Korea, and India.

- Fastest-growing Region: Asia Pacific is also projected to register the fastest CAGR during the forecast period, due to accelerating 5G deployment, increasing semiconductor investments, expanding industrial automation, and rising government support for domestic electronics manufacturing and 6G research initiatives.

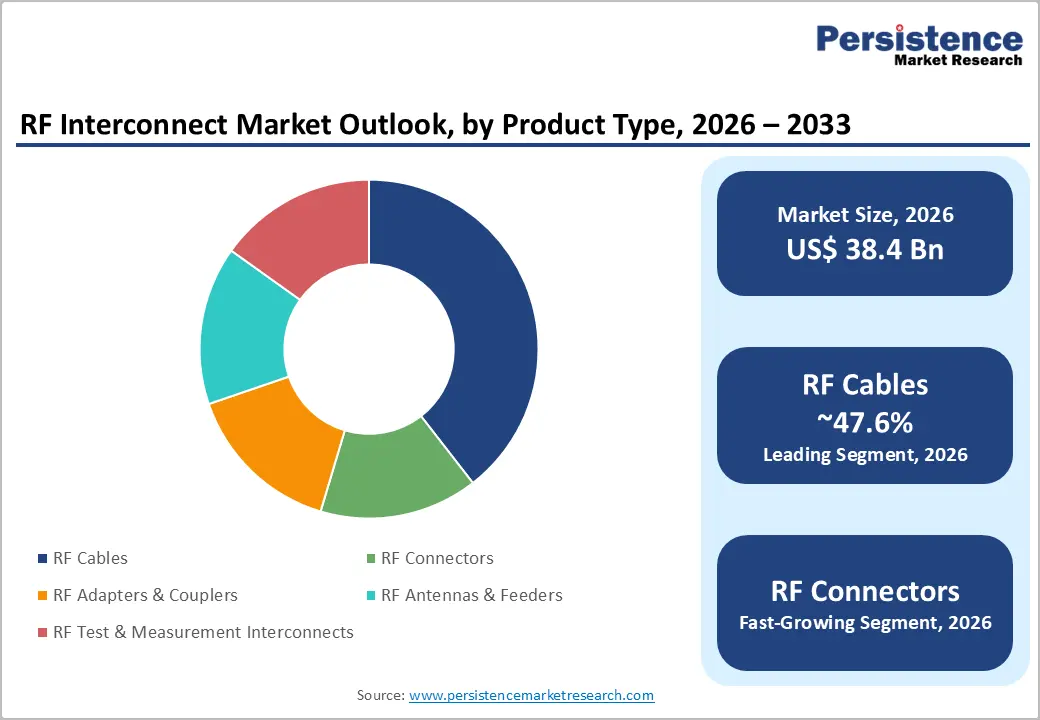

- Dominant Product Type: RF cables are anticipated to account for approximately 47.6% of the market share in 2026, driven by extensive deployment across telecom infrastructure, aerospace communication systems, industrial automation, and RF testing applications.

- Leading End-use Industry: Telecommunications & 5G infrastructure is expected to account for 41.2% of market share in 2026, supported by ongoing deployment of macro cells, small cells, distributed antenna systems, and wireless backhaul infrastructure globally.

DRO Analysis

Driver - Expansion of 5G Infrastructure and Emerging 6G Development

The ongoing deployment of 5G infrastructure across developed and emerging economies is significantly increasing the requirement for RF interconnect components. Telecom operators continue investing in low-band, mid-band, and high-band spectrum networks to support higher bandwidth consumption, enterprise connectivity, and cloud-based applications. Dense network architectures such as small cells, distributed antenna systems (DAS), Open RAN platforms, and edge-computing infrastructure require large volumes of RF cables, connectors, adaptors, feeders, and test assemblies.

The growing focus on 6G research is further accelerating demand for high-frequency interconnect solutions capable of supporting low latency, higher throughput, and advanced antenna technologies. Increased deployment of mmWave systems and beamforming technologies is creating stronger demand for precision-engineered RF assemblies with superior shielding, thermal stability, and signal integrity. As network density rises, the number of interconnect points per site also increases, directly supporting long-term market expansion.

Rising Integration of RF Systems in Automotive, Aerospace, and Defense Applications

Automotive radar systems, aerospace electronics, military communication platforms, and industrial wireless systems are increasing the performance requirements for RF interconnect technologies. Advanced Driver Assistance Systems (ADAS), autonomous vehicles, satellite communication systems, and electronic warfare platforms require highly reliable interconnect solutions capable of operating across high-frequency ranges with minimal signal loss.

The automotive industry is witnessing strong adoption of 77-81 GHz radar systems for collision avoidance, adaptive cruise control, and autonomous navigation. Simultaneously, aerospace and defense sectors continue modernizing radar, avionics, and surveillance infrastructure, increasing the use of ruggedized RF assemblies designed for harsh operating environments. Higher operating frequencies, strict electromagnetic compatibility requirements, and miniaturized electronic architectures are transforming RF interconnects from conventional hardware components into high-value engineered subsystems. This transition is improving average selling prices and strengthening long-term revenue opportunities for manufacturers specializing in precision RF connectivity solutions.

Restraint - High Qualification Costs and Supply Chain Complexity

The RF interconnect market faces structural challenges associated with complex manufacturing requirements, high qualification costs, and supply chain volatility. RF connectors, cables, and assemblies used in telecom, aerospace, and defense applications require strict impedance control, thermal resistance, shielding performance, and durability certifications. These requirements extend product development cycles and increase production costs for manufacturers.

Supply chain concentration within semiconductor materials, specialty metals, and precision electronic components also creates procurement risks. Manufacturers must maintain broader inventories to support multiple frequency bands, connector standards, and application-specific requirements. Rising raw material costs and extended lead times further impact operating margins. For telecom operators and industrial buyers, delayed availability of qualified RF interconnect components can postpone infrastructure rollouts and increase project implementation risks. The combination of technical qualification barriers and global supply chain uncertainty remains a key constraint limiting faster market scalability.

Opportunity - Growth of mmWave and High-Frequency Communication Ecosystems

The increasing commercialization of mmWave communication technologies is creating significant opportunities for RF interconnect suppliers. Frequencies ranging from 24 GHz to 100 GHz are becoming increasingly important across 5G infrastructure, automotive radar, aerospace communication systems, and advanced laboratory testing applications. These high-frequency systems require highly specialized connectors, cable assemblies, waveguides, and precision adaptors capable of maintaining signal stability under demanding operating conditions.

Demand is also increasing for RF test and measurement infrastructure used in calibration, validation, and network optimization. Manufacturers capable of delivering low-loss, high-frequency interconnect solutions with enhanced repeatability and ruggedization are expected to benefit from premium pricing opportunities. As advanced communication systems evolve toward higher bandwidth architectures, the value contribution of RF interconnect technology within overall system design is expected to increase substantially.

Manufacturing Localization and Asia Pacific Expansion

Asia Pacific continues emerging as a strategic manufacturing and demand center for RF interconnect technologies. China, Japan, India, South Korea, and ASEAN countries are investing heavily in telecom infrastructure, semiconductor manufacturing, automotive electronics, and industrial automation. Regional governments are also supporting domestic electronics manufacturing through localization incentives and digital infrastructure initiatives.

India’s growing focus on 6G development and electronics manufacturing expansion is creating favorable conditions for regional RF component sourcing. Manufacturers establishing localized production facilities, engineering support centers, and supply chain partnerships across Asia Pacific are likely to gain competitive advantages through lower logistics costs, faster qualification cycles, and improved customer responsiveness. Growing demand for industrial IoT systems, connected mobility platforms, and wireless communication infrastructure across the region is expected to support long-term market growth opportunities.

Category-wise Analysis

Product Type Insights

RF cables are anticipated to account for approximately 47.6% of the market share in 2026 during the forecast period, maintaining their position as the leading product segment. Their dominance is supported by extensive usage across telecom infrastructure, aerospace communication systems, industrial automation equipment, and RF testing environments. RF cables play a critical role in maintaining signal transmission efficiency between antennas, radios, transmitters, and receiving systems.

Demand for high-performance coaxial and hybrid RF cables is increasing as telecom operators expand 5G networks and upgrade base station infrastructure. For example, low-loss cable assemblies are widely used in Open RAN deployments and distributed antenna systems to improve signal stability. Aerospace and defense applications further support demand for ruggedized RF cable assemblies capable of withstanding vibration, thermal stress, and harsh operating conditions in radar and satellite communication systems.

RF connectors are anticipated to witness the fastest CAGR throughout the forecast period due to rising deployment of compact communication architectures and high-density electronic systems. Miniaturized RF connectors are increasingly used in 5G small cells, automotive ECUs, radar modules, satellite communication equipment, and mmWave testing platforms. The growing shift toward smaller electronic footprints and higher-frequency communication systems is increasing connector density across advanced devices.

Precision connector formats such as SMP, 2.4 mm, and 2.92 mm connectors are gaining wider adoption in aerospace radar systems, automotive ADAS platforms, and high-frequency laboratory testing applications. For instance, automotive radar modules operating at 77-79 GHz require compact, low-loss RF connectors capable of supporting stable signal transmission under vibration-intensive environments. Increasing investments in edge-computing infrastructure and modular communication hardware are expected to further accelerate long-term segment growth.

End-use Industry Insights

Telecommunications and 5G infrastructure are anticipated to account for approximately 41.2% of market share in 2026, making them the leading end-use segment. Continuous deployment of macro cells, small cells, distributed antenna systems, and wireless backhaul infrastructure is sustaining strong demand for RF cables, connectors, feeders, and adaptors. The transition toward cloud-native telecom networks and Open RAN architectures is increasing interconnect density and performance requirements.

Telecom operators require highly reliable RF components capable of supporting low latency and high-bandwidth communication. For example, 5G base stations and mmWave small cells require advanced RF cable assemblies and connectors to maintain signal integrity across dense urban deployments. Ongoing network upgrades and maintenance activities across North America, Europe, and Asia Pacific continue supporting recurring demand within the telecom sector.

Automotive electronics and ADAS applications are anticipated to record the fastest CAGR during the forecast period due to increasing adoption of connected mobility and autonomous driving technologies. Vehicle electrification, radar integration, infotainment systems, and vehicle-to-everything (V2X) communication platforms are significantly increasing RF content within modern vehicles.

Automotive manufacturers are increasingly integrating high-frequency radar systems operating at 77-79 GHz for adaptive cruise control, collision avoidance, and autonomous navigation. For instance, premium electric vehicles and advanced driver-assistance platforms now utilize multiple radar sensors connected through compact RF interconnect assemblies. The growing adoption of software-defined vehicle architectures and zonal electronic systems is also increasing the number of RF connection interfaces per vehicle, creating long-term growth opportunities for RF interconnect suppliers.

Regional Insights

North America RF Interconnect Market Trends

North America remains one of the most technologically advanced RF interconnect markets, supported by strong telecom infrastructure investment, aerospace modernization, defense spending, and industrial automation adoption. The region benefits from extensive deployment of 5G infrastructure, increasing Open RAN investments, and growing demand for mmWave communication systems.

U.S. RF Interconnect Market Trends

The U.S. is the largest contributor to the North American RF interconnect market due to extensive 5G deployment, defense communication modernization, and advanced semiconductor manufacturing capabilities. The country maintains strong leadership in aerospace, satellite communication, radar systems, and RF laboratory testing applications. Increasing investments in electronic warfare systems, unmanned platforms, and mmWave infrastructure continue driving demand for ruggedized high-frequency interconnect technologies.

The U.S. telecom industry is also accelerating deployment of small cells, Open RAN architectures, and high-density wireless communication networks. Growing adoption of industrial IoT and factory automation systems is creating additional demand for RF cables and connectors across industrial communication platforms.

Canada RF Interconnect Market Trends

Canada represents a steadily growing RF interconnect market supported by expanding telecom infrastructure, aerospace manufacturing, and industrial automation investment. Increasing deployment of 5G networks and rising adoption of connected industrial systems are contributing to higher demand for RF assemblies and antenna connectivity solutions. The country’s aerospace and defense sectors also support demand for high-reliability RF interconnect technologies used in communication, surveillance, and navigation systems.

Europe RF Interconnect Market Trends

Europe remains a high-value RF interconnect market characterized by strong regulatory harmonization, advanced automotive manufacturing, aerospace expertise, and industrial engineering capabilities. Increasing adoption of ADAS technologies, connected mobility systems, industrial IoT platforms, and Open RAN telecom infrastructure continues driving regional demand for RF cables, connectors, and high-frequency communication assemblies.

Germany RF Interconnect Market Trends

Germany is the leading RF interconnect market in Europe, due to its strong automotive manufacturing base, industrial automation leadership, and advanced engineering ecosystem. Growing integration of radar systems, vehicle connectivity platforms, and autonomous driving technologies is increasing RF component demand across automotive applications. The country’s strong aerospace and industrial IoT sectors also contribute to demand for ruggedized RF assemblies and high-frequency communication systems.

U.K. RF Interconnect Market Trends

The U.K. remains an important market for RF interconnect technologies due to ongoing defense modernization programs, aerospace innovation, and telecom infrastructure expansion. Increasing investments in satellite communication systems, radar technologies, and wireless testing platforms continue supporting demand for advanced RF assemblies. Expansion of Open RAN and next-generation telecom infrastructure is also accelerating adoption of precision RF connectors and cable systems.

Asia Pacific RF Interconnect Market Trends

Asia Pacific is both the largest and fastest-growing RF interconnect market, accounting for approximately 35.3% of market share in 2026. The region benefits from large-scale electronics manufacturing, telecom infrastructure expansion, automotive production growth, and increasing industrial automation investment. Strong manufacturing ecosystems across China, Japan, South Korea, India, and Southeast Asia continue supporting large-scale production of RF communication equipment and electronic components.

China RF Interconnect Market Trends

China remains the dominant RF interconnect market in Asia Pacific, due to its large-scale telecom infrastructure deployment, electronics manufacturing leadership, and expanding semiconductor ecosystem. Massive investments in 5G base stations, data centers, and wireless communication hardware continue driving demand for RF connectors, antenna systems, and cable assemblies. The country also benefits from strong domestic production capabilities across telecom equipment and automotive electronics.

Japan RF Interconnect Market Trends

Japan maintains a strong position in high-frequency communication technologies, automotive electronics, and advanced semiconductor packaging. Demand for precision RF interconnect solutions is increasing across automotive radar systems, industrial robotics, aerospace communication equipment, and laboratory testing applications. The country’s emphasis on engineering precision and miniaturized electronics continues supporting innovation within high-performance RF connectivity systems.

Competitive Landscape

The global RF interconnect market remains moderately fragmented, with competition distributed among several global connectivity and precision engineering companies. Market competition is shaped by technological expertise, frequency performance capabilities, product reliability, customization capacity, and qualification standards rather than pure pricing strategies. Major participants maintain strong positions across telecom, aerospace, automotive, industrial automation, and defense applications. Competitive differentiation increasingly depends on miniaturization capabilities, mmWave expertise, ruggedized product design, and global manufacturing presence.

Leading companies are prioritizing miniaturization, ruggedization, localization, and high-frequency innovation to strengthen market competitiveness. Strategic investments are increasingly focused on mmWave technologies, automotive radar systems, aerospace-grade assemblies, and next-generation telecom infrastructure. Manufacturers are also expanding regional production capabilities to reduce supply chain risks and improve customer responsiveness.

Key Industry Developments

- In March 2026, TE Connectivity announced the launch of its 56G MezzaWave connectors and cable assemblies, designed to support high-density applications such as edge AI, industrial automation, robotics, aerospace, and defense systems.

- In September 2025, HUBER+SUHNER AG launched a new VITA 67.3 RF interconnect portfolio built on its proprietary solderless MINIBEND technology, targeting aerospace and defense applications requiring compact, blind-mate RF connectivity.

Companies Covered in RF Interconnect Market

- Amphenol Corporation

- TE Connectivity

- Molex LLC

- HUBER+SUHNER AG

- Rosenberger Group

- Radiall SA

- Samtec Inc.

- Smiths Interconnect

- W. L. Gore & Associates

- Times Microwave Systems

- Carlisle Interconnect Technologies

- Pasternack Enterprises

- Fairview Microwave

- Quantic Electronics

- L-com Global Connectivity

- Junkosha Inc.

Frequently Asked Questions

The global RF interconnect market is anticipated to be valued at approximately US$38.4 billion in 2026.

The RF interconnect market is projected to reach nearly US$61.7 billion by 2033.

Major trends influencing the market include rapid deployment of 5G and emerging 6G infrastructure and rising adoption of mmWave and high-frequency RF technologies.

RF cables remain the leading product segment, accounting for approximately 47.6% of market share, due to widespread use across telecom infrastructure, aerospace communication systems, industrial automation, and RF testing applications.

The RF interconnect market is projected to grow at a CAGR of approximately 7.0% between 2026 and 2033.

Some of the major companies include Amphenol Corporation, TE Connectivity, Molex LLC, HUBER+SUHNER AG, and Rosenberger Group.