- Communication Infrastructure & Services

- Smart Cities Market

Smart Cities Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Smart Cities Market by Components (Hardware (Sensors, IoT devices, cameras, smart meters, connectivity infrastructure), Software (platforms, analytics, AI/ML systems, digital twins)), Application (Smart Transportation, Smart Utilities (Energy + Water + Waste), Smart Governance, Smart Building), and Region Analysis for 2026 to 2033

Smart Cities Market Trends & Analysis

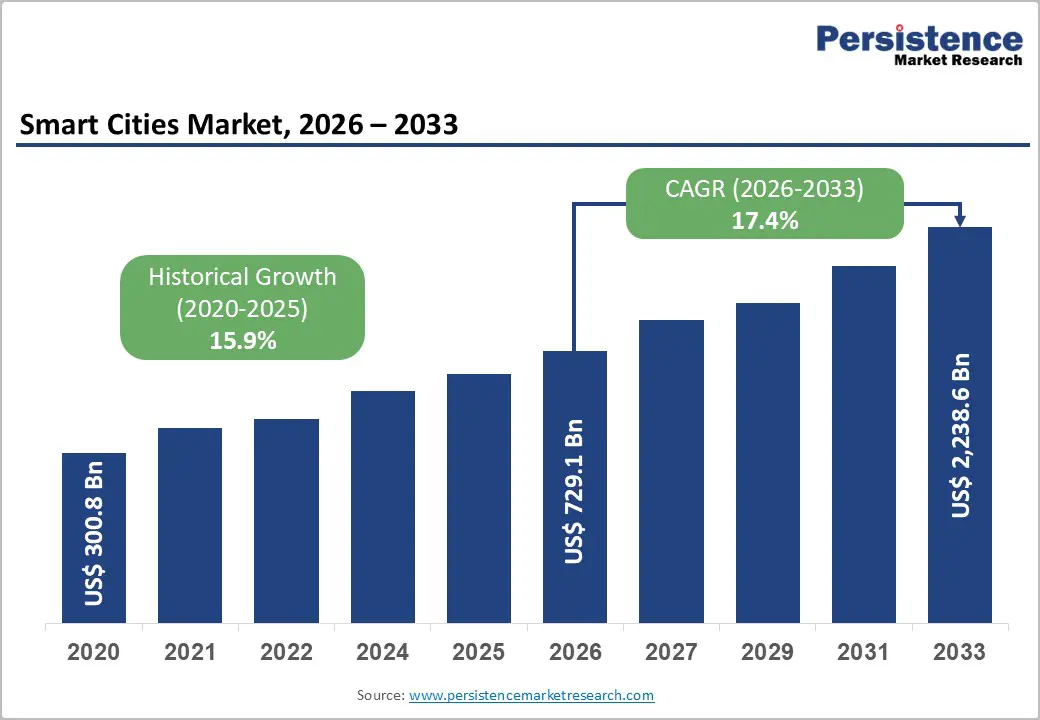

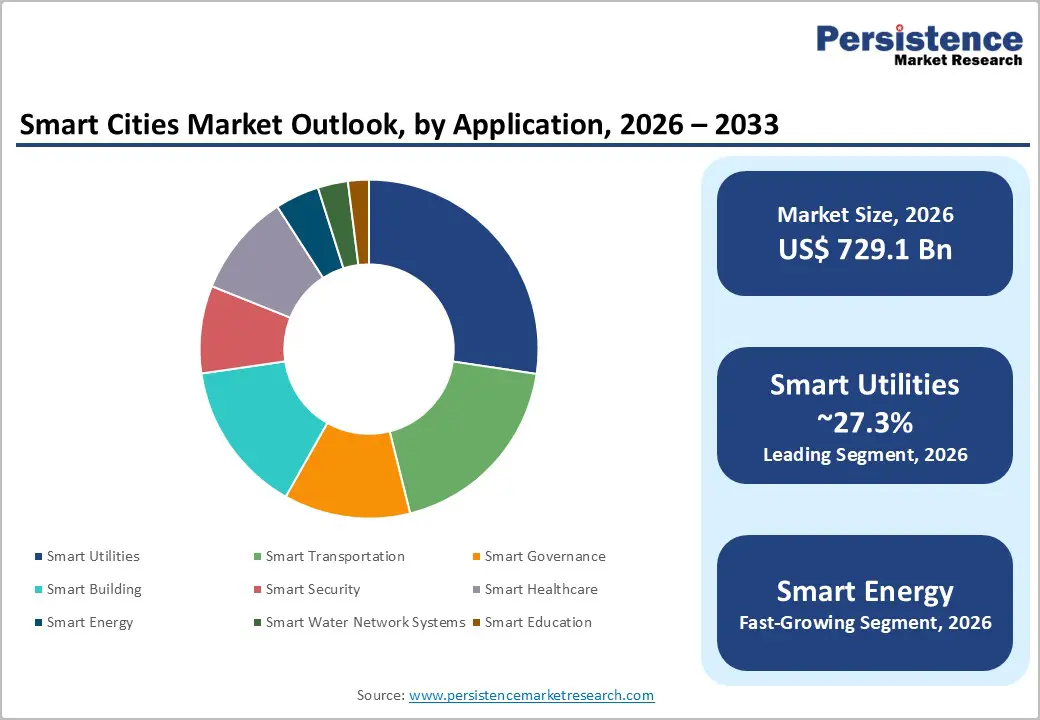

The global smart cities market size is projected at US$ 729.2 billion in 2026 and is projected to reach US$ 2,238.6 billion by 2033, growing at a CAGR of 17.4% between 2026 and 2033. IoT in smart cities alone reached US$ 264.3 Bn in 2025 at 21.3% CAGR; smart utility applications command 27%+ market share; cloud deployments captured 66.3% of smart city infrastructure share in 2025, confirming platform-led urban digital transformation as the market's dominant commercial architecture globally.

Rapid global urbanization, with 68% of the world's population projected to live in urban areas by 2050 (UN DESA), combined with 5G IoT deployment, AI-driven urban analytics, and government-mandated digital infrastructure investment programs are primary growth factors.

Key Industry Highlighst:

- Leading Component: Hardware leads at 38.4% share (US$ 280 Bn) in 2026; Software grows fastest at 20.6% CAGR, driven by AI/ML analytics, digital twin platforms, and cloud-based urban operating system adoption globally.

- Leading Application: Smart utilities leads at 27.3% share (US$ 199 Bn); Smart Energy grows fastest at 20.7% CAGR, driven by renewable grid integration, EV infrastructure expansion, and AI demand-response deployments globally.

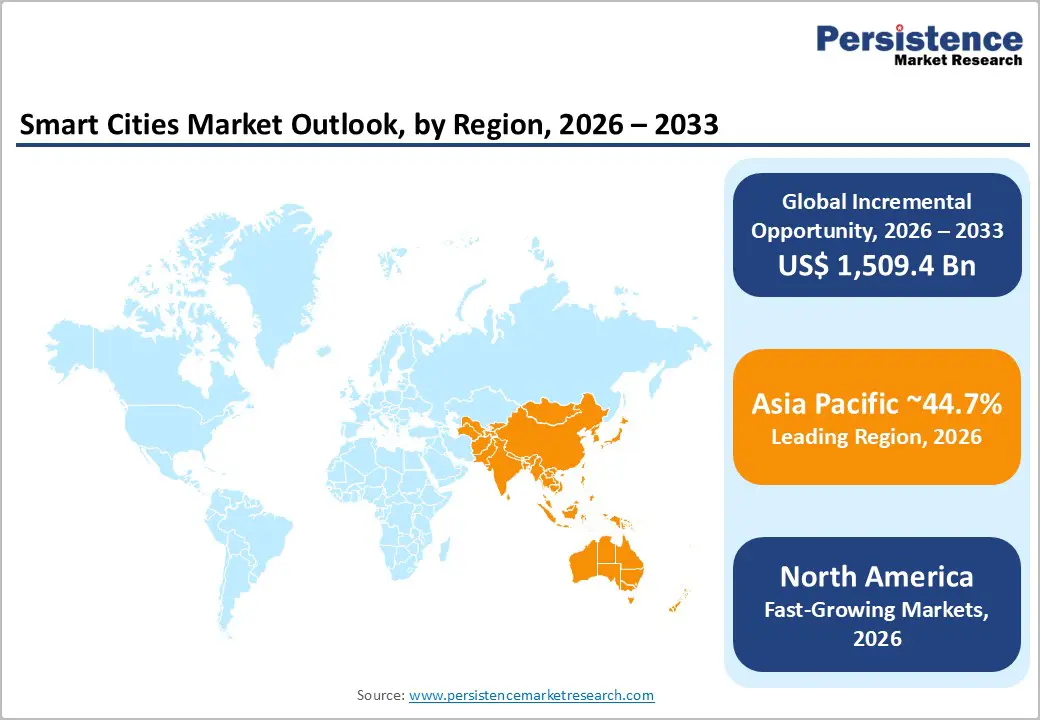

- Regional Leader: Asia Pacific leads at 38.5% share and 19.6% CAGR; China holds US$ 148.9 Bn and India US$ 51.7 Bn in 2026, anchored by government-mandated smart city and renewable energy programs.

- North America Market Scenario: North America is expected to witness 15.8% CAGR with U.S. at US$155.3 Bn in the forecast period.

- Strategic Milestone: Itron-India RDSS partnership targeting 250 million smart meter installations and Huawei's iCOC 3.0 across 30 new city contracts in Middle East and Southeast Asia signal accelerating smart utility hardware procurement.

Market Dynamics Analysis

Drivers - Accelerating Global Urbanization and Government-Mandated Smart City Investment Programs

The UN DESA projects 68% of the global population will reside in urban areas by 2050, adding 2.5 billion more city dwellers, creating unprecedented demand for intelligent urban infrastructure managing traffic, energy, water, and public safety at scale across rapidly expanding municipal boundaries. India, China, and Nigeria collectively account for 35% of projected global urban population growth between 2018 and 2050, positioning them as the world's most concentrated smart city technology procurement opportunities within a defined macro-regional investment horizon.

Government-backed national smart city programs, India's Smart Cities Mission covering 100 designated cities, China's 14th Five-Year Plan committing digital infrastructure investment across 2,000 smart city pilot projects, and the EU's Horizon Europe €95.5 Bn program funding smart urban solutions, translate urbanization pressure into structured, policy-anchored hardware and software procurement cycles that directly expand smart city technology deployment across all application categories globally.

5G Network Deployment and IoT Proliferation Enabling Real-Time Urban Intelligence

The global rollout of 5G networks, delivering speeds up to 100 times faster than 4G and latencies as low as 1 millisecond, provides the essential wireless backbone for smart city IoT ecosystems connecting billions of sensors, cameras, smart meters, and connected vehicles in real time at urban scale. The GSMA projects 5G connections will reach 5.9 billion globally by 2030, with smart city applications including intelligent traffic management, environmental monitoring, and predictive infrastructure maintenance representing the highest-value commercial deployment use cases across advanced urban economies.

India's Department of Telecommunications launched 100 5G Use Case Labs at educational institutions under the national 5G Innovation Initiative, while South Korea's Ministry of Science allocated KRW 390 Bn to smart city 5G integration through 2027. These government-anchored 5G-IoT mandates are directly expanding hardware procurement volumes, particularly connectivity infrastructure, sensors, and smart meters, at metropolitan deployment scale across North America, Asia Pacific, and Europe, embedding 5G connectivity as a foundational smart city infrastructure investment requirement through 2033.

Restraints - Urban Data Privacy Regulations and Cybersecurity Compliance Delaying Platform Deployments

Smart city platforms, continuously collecting data from millions of IoT sensors, surveillance cameras, smart meters, and connected mobility networks, face expanding urban data privacy and cybersecurity regulatory compliance requirements.

The EU GDPR, India's Digital Personal Data Protection Act 2023, and China's Personal Information Protection Law imposes data localization, consent management, and breach notification mandates that extend smart city platform certification and municipal procurement approval timelines by 12-18 months per jurisdiction, creating deployment delays across software and systems integration programs at city government levels.

Interoperability Gaps and Legacy Municipal Infrastructure Integration Complexity

Smart city deployments require seamless data exchange between heterogeneous systems, legacy SCADA infrastructure, proprietary municipal ERP systems, diverse IoT protocol stacks (MQTT, CoAP, Zigbee, LoRaWAN), and cloud analytics platforms.

The absence of universal interoperability standards creates prohibitive integration complexity, with IEEE P2510 and ITU-T SG20 smart city standards still in active development. Municipal procurement programs navigating fragmented vendor ecosystems without standardized performance benchmarks face cross-system platform rollout delays estimated at 18-24 months at large-scale metropolitan deployments, limiting solution scalability and increasing total implementation risk globally.

Opportunities - Digital Twin City Platforms as Premium Urban Management Infrastructure

Digital twin technology, creating virtual replicas of entire cities with real-time IoT sensor data feeds from transport networks, utility grids, buildings, and public spaces, represents the highest-value software application within the Smart Cities Market. Deloitte estimates the global digital twin market will reach US$ 73.5 Bn by 2027 at 38.4% CAGR, with urban digital twins representing approximately 25% of total addressable market value for smart city software vendors providing AI-enhanced platform services.

Singapore's Virtual Singapore national digital twin program, the EU's Destination Earth climate digital twin initiative, and China's urban digital twin pilots across Shenzhen and Shanghai are establishing commercial validation pathways for city-as-a-service subscription procurement models. Digital twin platforms generate 40-60% higher average contract values than standalone hardware deployments while creating multi-year recurring software revenue streams with deep municipal switching barriers, positioning digital twin adoption as the most structurally differentiated growth opportunity within the Smart Cities software segment globally through 2033.

Smart Grid and Renewable Energy Integration Creating Urban Energy Intelligence at Scale

The global renewable energy transition, with the IEA projecting renewables supplying over 35% of global electricity by 2025, demands smart grid infrastructure including IoT-enabled meters, grid sensors, AI demand-response platforms, and bi-directional energy flow management systems to handle intermittent generation at urban distribution grid scale. The Smart Energy standalone digital grid layer is growing at 20.7% CAGR, the fastest application sub-segment, confirming the structural market expansion opportunity within smart utility infrastructure investment programs globally.

Municipal energy authorities across Europe, China, the U.S., and India are embedding smart grid procurement within national net-zero pathway investment commitments. The U.S. Department of Energy's Grid Modernization Initiative allocated US$ 3.46 Bn to smart grid deployment through 2026, directly expanding smart utility hardware and software procurement volumes at urban scale.

Vendors combining smart meter hardware deployment with cloud-based energy analytics and demand-response platform services are capturing the dual hardware-software revenue opportunity created by the renewable energy transition, creating the market's most scalable commercial growth pathway within the application layers.

Category-wise Analysis

Component Insights

Hardware (sensors, IoT devices, cameras, smart meters, connectivity infrastructure) leads the components segment with a 38.4% market share in 2026, estimated at approximately US$ 280 Bn, anchored by the foundational physical infrastructure deployment requirement preceding any urban analytics or intelligence capability activation. Smart meters, environmental IoT sensors, traffic monitoring cameras, and 5G connectivity nodes represent the highest-volume hardware procurement categories across all city application programs globally.

Software's share is growing rapidly through AI analytics and digital twin platform adoption, but hardware's infrastructure-first deployment sequencing across under-digitized emerging markets in Asia Pacific, Latin America, and the Middle East sustains its revenue segment leadership consistently through 2033.

Software (platforms, analytics, AI/ML systems, digital twins) is the fastest-growing component at 20.6% CAGR. AI/ML urban analytics, real-time city operating platforms, and digital twin management systems are accelerating software adoption as municipalities transition from physical infrastructure deployment toward data intelligence monetization, extracting measurable operational value from connected urban asset networks across transportation, energy, and governance application domains globally.

Application Insights

Smart utilities (Energy + Water + Waste) lead the application segment with a 27.3% market share in 2026, estimated at approximately US$ 199 Bn, anchored by the universal, non-discretionary requirement for smart energy grid management, water distribution network monitoring, and intelligent waste logistics optimization across all urban centers globally. IoT-enabled smart meters, grid sensors, and water pipeline monitoring systems generate the broadest cross-market hardware and software procurement mandate within any single smart city application.

Smart Transportation's growing EV fleet and autonomous vehicle infrastructure investments will competitively narrow revenue gaps through 2033, but Smart Utilities' operational continuity imperative and regulatory utility efficiency mandates sustain its segment leadership firmly.

Smart Energy (standalone digital grid layer) is the fastest-growing application segment at 20.7% CAGR through 2033. National net-zero commitments, renewable energy grid integration requirements, EV charging infrastructure expansion, and AI-powered demand-response platform deployments across Europe, North America, and Asia Pacific are collectively driving Smart Energy application adoption at an accelerating pace, establishing it as the application segment's most dynamic growth engine by 2033.

Regional Market Insights

North America Smart Cites Market Trends

North America is likely to achieve a prominent growth accounting for approximately 22% of global smart cities market share, anchored by federal digital infrastructure mandates, 5G network leadership, and dense private technology ecosystems driving AI-powered urban platform adoption across U.S. and Canadian metropolitan programs.

U.S. Market Leadership, Regulatory Framework & Innovation Ecosystem

The United States likely accounts for approximately US$ 155.3 Bn in 2026, anchored by the Infrastructure Investment and Jobs Act's US$ 65 Bn broadband and smart grid allocation, directly expanding municipal smart city hardware and software procurement volumes. Cisco, IBM, Microsoft, and Oracle dominate competitive platform deployment across U.S. smart transportation, governance, and utility programs.

Canada contributes through federal Smart City Challenge-funded programs across Toronto, Montreal, and Vancouver metropolitan innovation networks, establishing North America's regulatory and competitive leadership as the premium technology-specification smart city deployment benchmark.

Europe Smart Cities Market Insights

Europe is likely to a 21.7% share of the global smart cities market in 2026, estimated at approximately US$ 158.2 Bn, growing steadily through EU Horizon Europe urban innovation funding, GDPR-compliant smart city data governance frameworks, and national digital infrastructure investment programs across Germany, France, the U.K., and Spain.

Germany, U.K., France & Spain: Regulatory Harmonization and Premium Platform Deployment

Germany leads Europe at approximately US$ 47.1 billion in 2026, anchored by Siemens AG smart infrastructure, SAP urban analytics, and Deutsche Telekom 5G smart city network leadership. France's Grand Paris smart mobility initiative and Barcelona superblocks intelligent transportation model contribute globally referenced application deployments. The EU Smart Cities and Communities initiative funds smart city pilots across 370 European cities, creating structured, compliance-driven procurement demand across hardware and software segments.

Europe's growth is reinforced by digital twin city adoption, REPowerEU renewable smart grid mandates, and EU Energy Performance of Buildings Directive compliance, collectively sustaining structured procurement demand across smart utility and smart building application layers through 2033.

Asia Pacific Smart Cities Market Insights

Asia Pacific is the fast-growing market at 19.6% CAGR, commanding approximately 38.5% of global share in 2025, driven by China's 14th Five-Year Plan digital city investments, India's Smart Cities Mission, and ASEAN national digital economy frameworks creating the world's most concentrated smart city deployment expansion zone.

China, India, Japan & ASEAN: Myopia Epidemic and Manufacturing Scale Advantage

China is likely to account for US$ 148.9 Bn in 2026, driven by Alibaba Cloud's City Brain AI platform, Huawei Smart City OS deployments, and state-directed smart utility grid investments across 500+ pilot cities under national digital economy programs.

India’s initiatives for Smart Cities Mission 2.0 implementations and Itron's 250 million smart meter RDSS partnership. Japan sustains Fujitsu and Hitachi smart city digital twin leadership across 20 designated Super City framework pilot zones, while ASEAN nations' digital economy masterplans expand smart transportation and utility procurement across Vietnam, Thailand, and Indonesia.

Asia Pacific's manufacturing cost advantages, government EV infrastructure mandates, and rapidly urbanizing middle-class populations make it the most strategically consequential region for smart city hardware volume and software platform investment through 2033.

Competitive Landscape

The global Smart Cities Market is moderately fragmented, with Cisco, Siemens, IBM, Huawei, and Microsoft collectively holding approximately 30-35% of global platform and infrastructure revenue in 2026. Key differentiators include AI-driven urban operating platform depth, interoperability with legacy municipal systems, end-to-end IoT-to-cloud infrastructure stacks, and cybersecurity compliance certifications. City-as-a-Service and smart city platform-as-a-service subscription models are gaining traction as emerging procurement preferences.

AI platform innovation, geographic expansion into Asia Pacific and Middle East urban development programs, and strategic acquisitions targeting IoT analytics and digital twin capability integration define dominant competitive strategic themes across all major smart city market participants through 2033.

Strategic Developments

- In May 2025, Microsoft expanded its Azure IoT smart city digital twin platform to 12 new Asia Pacific cities, including Kuala Lumpur, Bangkok, and Ho Chi Minh City, investing US$ 2.2 Bn in ASEAN cloud and AI infrastructure to support national smart city program digital twin deployments.

- In September 2024, Siemens AG completed the acquisition of Danfoss's smart building energy management division, integrating Danfoss's urban thermal grid and district energy management IoT platforms into Siemens's Smart Infrastructure portfolio, strengthening smart utility solutions for European municipal energy programs.

- In November 2024, Huawei expanded its Intelligent City Operations Center (IOC) and City Intelligent Twins platform, integrating AI, digital twins, and real-time IoT data into a unified urban management system, deployed across 200+ cities in 40+ countries, including major rollouts in the Middle East and Asia-Pacific.

Companies Covered in Smart Cities Market

- Cisco Systems, Inc.

- Siemens AG

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- Schneider Electric SE

- Honeywell International Inc.

- ABB Ltd.

- Alphabet Inc. / Google (Sidewalk Labs)

- Oracle Corporation

- Ericsson AB

- Hitachi, Ltd.

- Thales Group

- Itron, Inc.

- Fujitsu Limited

Frequently Asked Questions

The smart cities market is valued at US$ 729.2 Bn in 2026, projected to reach US$ 2,238.6 Bn by 2033, with an incremental opportunity of US$ 1,509.4 Bn.

Accelerating global urbanization adding 2.5 billion urban dwellers by 2050, government-mandated digital infrastructure investment programs, and 5G-enabled IoT deployment creating real-time urban intelligence capability are the primary structural growth drivers.

The smart cities market is projected to grow at a CAGR of 17.4% from 2026 to 2033, building on a historical CAGR of 15.9% from 2020 to 2026.

Digital twin city platform adoption as managed municipal services and smart grid renewable energy intelligence infrastructure deployment under national net-zero programs represent the most actionable high-value growth opportunities through 2033.

Cisco, Siemens, IBM, Huawei, Microsoft, Schneider Electric, Honeywell, ABB, Oracle, Ericsson, Hitachi, Thales, Itron, and Fujitsu are the leading global Smart Cities Market participants.