- Communication Infrastructure & Services

- CubeSat Market

CubeSat Market Size, Share, and Growth Forecast 2026 - 2033

CubeSat Market by Size (0.25U to 1U, 1 to 3U, 3U to 6U), Sub-system (Structures, Payloads, Power Systems), Application (Earth Observation, Meteorology), End-user (Government and Defense, Commercial), and Regional Analysis, 2026 - 2033

CubeSat Market Size and Trends Analysis

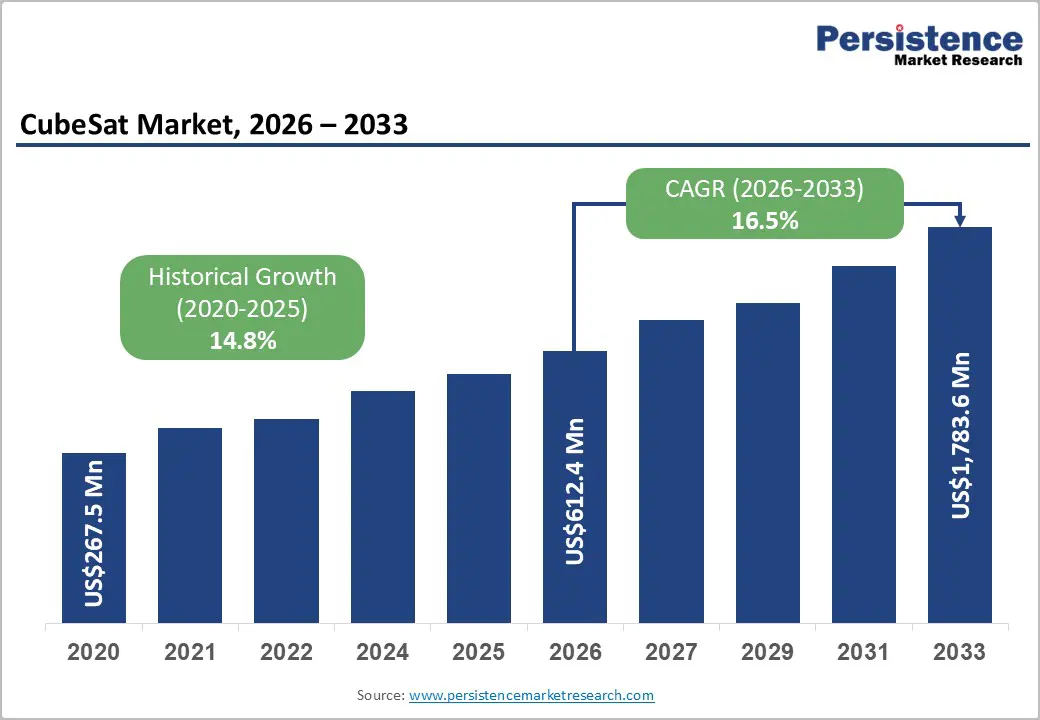

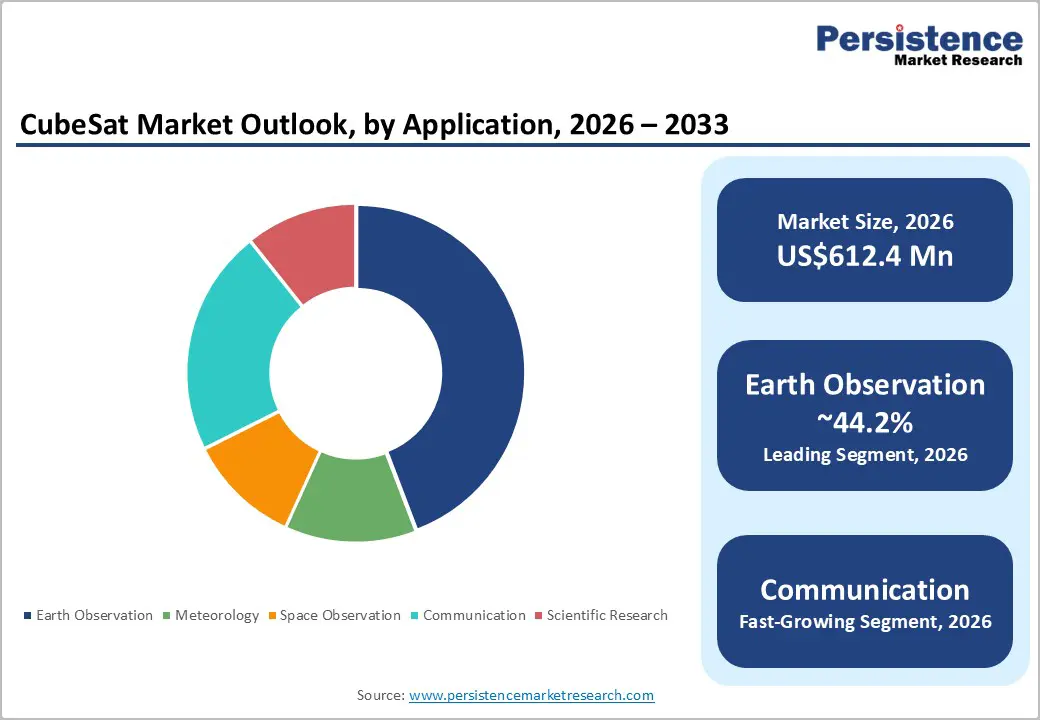

The global CubeSat market size is likely to be valued at US$612.4 million in 2026 and is expected to reach US$1,783.6 million by 2033, growing at a CAGR of 16.5% during the forecast period from 2026 to 2033, driven by the rising demand for high-frequency Earth observation data across agriculture, climate monitoring, and disaster management. Increasing adoption of low-cost satellite constellations for global communication and IoT connectivity is also predicted to boost the market.

Key Industry Highlights:

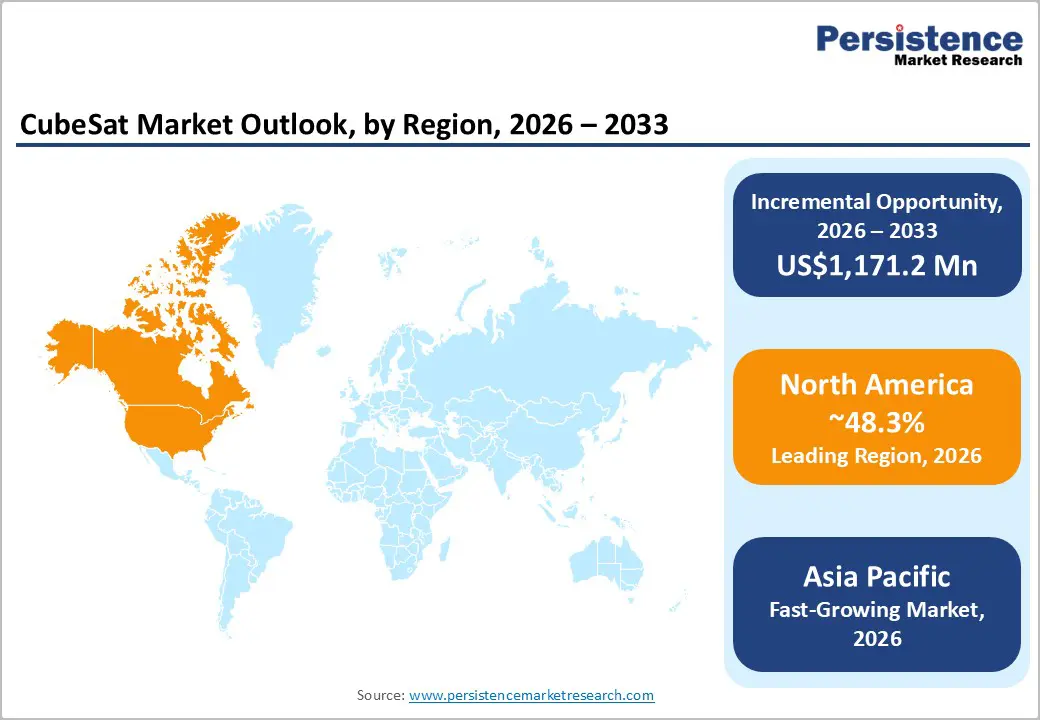

- Leading Region: North America, with about 48.3% share in 2026, spurred by high defense spending and increasing government funding.

- Fast-growing Region: Asia Pacific, owing to rising investments in domestic space programs and increasing demand for regional connectivity.

- Leading Application: Earth observation, approximately 44.2% share in 2026, backed by increasing demand for real-time monitoring in agriculture, climate tracking, and disaster response.

- Dominant End-user: Government and defense, nearly 42.6% in 2026, fueled by increasing reliance on CubeSats for surveillance, secure communication, and tactical intelligence by agencies such as the U.S. Department of Defense.

- Latest Purchase Order: In November 2025, GomSpace North America announced a US$1.5 million component purchase order from a leading global service provider, covering advanced spacecraft subsystem components. These specifically include high-performance nanosatellite power and command systems to support an upcoming satellite mission, with delivery scheduled for the first half of 2026.

DRO Analysis

Driver - Rising Demand for Miniaturization and Commercial Tech

The shift to standardized form factors and off-the-shelf components has fundamentally changed who can build a satellite. With mission budgets typically in the range of US$5 to 10 million and development cycles of just two to three years, CubeSats enable speedy mission turnaround. This is a sharp contrast to the decade-long timelines of traditional spacecraft. The surging availability of Commercial Off-The-Shelf (COTS) components, right from solar panels and reaction wheels to three-axis stabilization systems, has reduced mission costs.

It has freed more resources for scientific payloads. The standardization also eliminates redundant testing. Since additional screening and reliability inspections are not mandatory for COTS parts, satellite subsystem costs drop significantly. This makes space accessible to universities, start-ups, and emerging space nations alike.

Surging Need to Minimize Integration Costs among Rocket Operators

CubeSats rarely need a dedicated rocket. Instead, they travel as secondary payloads on missions already heading to orbit. The development of standardized deployers, such as the CubeSat P-POD, was a critical enabler, allowing dozens of satellites to be integrated safely and efficiently on a single launch vehicle. Companies such as Exolaunch have turned this into a reliable business.

Exolaunch has deployed over 400 satellites across 20 missions with SpaceX and has now secured new multi-year launch contracts extending through 2028. These span sun-synchronous, mid-inclination, and near-polar orbits. In 2023 alone, a record 359 CubeSats were launched, with almost 75% flying on Falcon 9. It demonstrates just how central rideshare has become to CubeSat deployment.

Restraint - Severe Power and Energy Constraints to Limit Growth

A CubeSat's small body directly limits how much power it can generate and store. According to NASA, most CubeSats typically operate within a power range of just 5 to 20 watts, with low power systems used owing to size and weight limits. On a 1U satellite, the total power budget can be as low as 1 to 2 watts, while even a larger 12U unit reaches only 50 to 150 watts. This leaves little room for power-hungry instruments such as high-resolution radars or advanced propulsion.

The power and energy limitations restrict the CubeSat's functionality and data processing capabilities, making compute-intensive missions particularly challenging. NASA's ALBus project is actively trying to address this. It aims to be the first CubeSat to demonstrate a 100-watt power management system, which could open the door to capabilities such as electric propulsion and advanced communications. Until such solutions mature, power remains the primary bottleneck for high-performance CubeSat missions.

Opportunity - Use of CubeSats for Deep Space Exploration

CubeSats are no longer limited to Earth orbit. NASA's MarCO twins were the first to prove this. Launched in 2018, they followed the InSight Mars lander and relayed data back to Earth as it entered the Martian atmosphere. ESA has now taken the concept further. ESA's Hera mission, launched in October 2024, successfully received the first signals from its two CubeSat passengers, Milani and Juventas, marking ESA's first-ever deep-space CubeSat deployment.

The pair will be deployed near the Didymos asteroid system to gather data on the aftermath of NASA's DART impact. They will also test inter-satellite link technology for future distributed mission architectures. ESA's M-Argo satellite, planned for launch in 2025, will become the smallest CubeSat to independently carry out its own interplanetary mission. This is a further sign that deep space is now within reach for small satellites.

Emergence of Swarm Intelligence to Make CubeSats Self-Managing

Rather than operating in isolation, CubeSats are increasingly flying as coordinated networks that make real-time decisions. In a 2024 test aboard CogniSAT-6, a briefcase-sized CubeSat, NASA's JPL demonstrated AI-based Dynamic Targeting. The satellite autonomously scanned its orbital path, processed imagery, and redirected its instrument within 90 seconds, with no human input. Swarm missions take this on a whole new level.

ESA's swarm initiative, which targets first operational missions by 2029, envisions CubeSats autonomously positioning themselves in close-knit formations or physically docking to form larger structures in orbit. Spire Global and Mission Control are also running a year-long demonstration called Persistence, testing deep learning AI aboard a 6U CubeSat for fully autonomous spacecraft operations. Together, these programs show how swarm intelligence is turning CubeSats into resilient, self-managing systems.

Category-wise Analysis

Application Insights

The Earth observation segment is predicted to lead with a share of approximately 44.2% in 2026, as it delivers daily, usable data for agriculture, climate tracking, urban planning, and disaster response. CubeSats make it possible to capture images of the same location multiple times a day, which was not feasible with traditional satellites. The NASA has highlighted that small satellite constellations improve revisit rates significantly, enabling near real-time monitoring of wildfires and floods. The European Space Agency also uses CubeSat-based missions for Copernicus expansion, showing how public agencies rely on frequent Earth data for policy decisions.

The communication segment is estimated to be the fastest-growing segment in the forecast period, as CubeSats can support low-cost and flexible connectivity solutions, especially in remote regions. Traditional communication satellites are expensive and slow to deploy. CubeSat constellations can be launched quickly and upgraded more often. Start-ups are building CubeSat communication networks for IoT and maritime connectivity. Swarm Technologies, acquired by SpaceX, uses very small satellites to provide low-bandwidth global IoT connectivity at lower cost.

End-user Insights

The government and defense segment is anticipated to dominate with a share of nearly 42.6% in 2026, as CubeSats are now critical for surveillance, reconnaissance, and national security. These satellites can be deployed quickly during conflicts or emergencies, which gives them a tactical advantage. The U.S. Department of Defense has increasingly invested in proliferated low Earth orbit (LEO) constellations to improve resilience against attacks on large satellites. The Space Development Agency is developing a network of small satellites for missile tracking and secure communication.

The commercial segment is expected to remain in the second position in 2026, as companies are finding new ways to monetize satellite data. Businesses no longer rely only on selling satellite hardware. They sell insights derived from data. Industries such as agriculture, logistics, energy, and insurance are using CubeSat data for decision-making. For example, Spire Global provides weather and maritime data using small satellites, which helps shipping companies optimize routes.

Regional Insights

North America CubeSat Market Trends

In 2026, North America will dominate with a share of around 48.3%, backed by well-funded government programs, mature industrial infrastructure, and an unmatched commercial ecosystem. The region is characterized by heavy government sponsorship, especially through NASA's CubeSat Launch Initiative (CSLI) and the U.S. Department of Defense. These sponsor and enable multiple small satellite missions while fostering partnerships with universities and private firms. Over the last four-plus years, NASA's CSLI has selected over 200 missions involving more than 100 organizations across 42 states, DC, and Puerto Rico, with over 150 CubeSats launched under the program.

U.S. CubeSat Market Trends

The U.S. market is attractive as it sits at the intersection of government demand, commercial data services, and academic research and development. Educational institutions are securing NASA grants and DARPA contracts to test CubeSat payloads for interplanetary navigation and AI-backed analytics. This academic-commercial synergy is fast-tracking innovation in propulsion, miniaturized sensors, and autonomous mission capabilities. The commercial side is just as strong. The government continues to be a reliable anchor customer. Planet Lab's NRO renewed its contract for PlanetScope monitoring and SkySat high-resolution tasking under the Electro-Optical Commercial Layer program. The DIU also awarded Planet a contract to boost next-generation commercial satellite technology.

Asia Pacific CubeSat Market Trends

Asia Pacific is anticipated to be the fastest-growing market in the forecast period, as multiple large economies are simultaneously expanding their space programs. Rising engagement from India, Japan, South Korea, and Australia in small satellite development as well as launch initiatives is also expected to propel the market. A surging cohort of regional satellite start-ups is using CubeSat platforms for commercial and educational missions, while efforts to establish sovereign satellite capabilities further catalyze the region's growth.

India's liberalization of private space in 2023, South Korea's increasing constellation ambitions, and Australia's Fleet Space Technologies all add to a region that is building capacity at speed.

Japan CubeSat Market Trends

Japan's market is pushed by institutional deployment channels, corporate investment, and a maturing commercial hub. JAXA has made the International Space Station's Kibo module a regular CubeSat deployment pipeline. In December 2024, JAXA deployed five CubeSats from Kibo, including LignoSat, YODAKA, DENDEN-01, YOMOGI, and ONGLAISAT, under its J-SSOD and J-CUBE programs in partnership with the University Space Engineering Consortium (UNISEC). Corporate interest is also rising sharply. In January 2025, Toyota Motor made a US$44.4 million investment in Interstellar Technologies to extend small satellite launch capabilities.

China CubeSat Market Trends

China is constantly building the infrastructure to become a leading independent space power, and CubeSats are a key part of that push. In 2024, the country set a new record with 68 rocket launches, of which 12 were conducted by private companies, with commercial satellites making up 78.2% of the 257 spacecraft placed into orbit. China is moving from state-led to mixed commercial models. For the first time in 2024, commercial space was included in the country’s government work report, showcasing the beginning of a new era.

Private investment is expanding too. In 2024, Shanghai Spacecom Satellite Technology (SSST) secured approximately US$1.33 billion in its Series A round to build the G60/SpaceSail LEO broadband constellation.

Europe CubeSat Market Trends

Europe is home to several globally competitive manufacturers and benefits from superior institutional demand. Key players include Surrey Satellite Technology (SSTL), GomSpace, AAC Clyde Space, EnduroSat, and NanoAvionics, which have collectively transformed the continent into a formidable manufacturing and systems integration hub. The European Space Agency plays a key facilitative role. According to the European Space Education Resource Office, several university CubeSat projects under ESA's Fly Your Satellite! program selected the 3U form factor between 2020 and 2024 due to standardized structural kits and predictable thermal behavior.

Germany CubeSat Market Trends

Germany is one of Europe's most active players in CubeSat and small satellite development, combining public research investment with commercial mission execution. DLR has been running hands-on CubeSat programs. Its NanoFF mission, funded by DLR and developed by the Technical University of Berlin, deployed two 2U CubeSats in January 2024 to demonstrate precise relative navigation, inter-satellite communication, and autonomous formation-keeping in LEO. Prominent institutions are also influencing standards for satellite ground operations. The German Space Operations Center (GSOC) successfully commanded DLR's PIXL-I CubeSat using the new European EGS-CC ground control system.

U.K. CubeSat Market Trends

The U.K.'s steady growth comes from an unusually dense concentration of small satellite manufacturers, increasing private investment, and supportive government policy. Glasgow alone has become Europe's leading small satellite manufacturing city. Companies such as AAC Clyde Space and Spire Global have built more satellites in Glasgow than in any other European city, supported by the newly launched West of Scotland Space Cluster. It blends research institutions, manufacturers, and the newly licensed SaxaVord Spaceport. AAC Clyde Space's hardware supports 40% of all CubeSat missions globally and is considered to have more hardware in space than any other small satellite provider.

Competitive Landscape

The global CubeSat market is moderately fragmented, with the presence of specialized manufacturers, Earth observation companies, launch integrators, and defense-focused satellite operators. Companies that combine CubeSat production with analytics, imaging subscriptions, AI-supported geospatial intelligence, and launch coordination are gaining strong positioning. Planet Labs is one of the key examples of this transition. Instead of primarily selling hardware, the company monetizes daily Earth imaging data through recurring subscription models used in agriculture, climate monitoring, insurance, and defense applications.

GomSpace, AAC Clyde Space, EnduroSat, and NanoAvionics are competing through modular satellite platforms, propulsion systems, and customizable missions for commercial and government customers. Traditional aerospace giants such as Lockheed Martin and Northrop Grumman are increasingly entering the CubeSat segment to secure military and intelligence contracts. Firms such as Spire Global focus on weather and maritime analytics, while others concentrate on Synthetic Aperture Radar (SAR)-based monitoring that works through clouds and at night.

Key Industry Developments:

- In March 2026, the U.S. National Geospatial-Intelligence Agency (NGA) launched three CubeSats into low-Earth orbit aboard a SpaceX Falcon 9 rideshare mission from Vandenberg Space Force Base. Findings from the three satellites will inform NGA's acquisition strategy for a permanent commercially sourced geomagnetic data collection capability targeted for 2030.

- In March 2026, GomSpace signed a EUR 7.6 million contract with VirtuaLabs to deliver a cluster of satellites for space-based Radio Frequency (RF) environment monitoring. The mission combines GomSpace's flight-proven satellite platforms with VirtuaLabs' expertise in electromagnetic surveillance, with satellite delivery estimated for the first half of 2028.

- In May 2025, Bulgaria-based EnduroSat raised approximately US$49 million in a round led by Founders Fund to extend production of its Gen3 satellite platform in the 200 to 500 kg class and build a new 17,500-square-meter facility in Sofia. The investment came on top of an earlier US$21 million round in February 2025.

Companies Covered in CubeSat Market

- Blue Canyon Technologies

- CU Aerospace L.L.C.

- EnduroSat

- GomSpace

- Innovative Solutions In Space B.V.

- L3Harris Technologies Inc.

- Planet Labs Inc.

- Pumpkin Space Systems

- Space Inventor

- SpaceX

- Others

Frequently Asked Questions

The global CubeSat market is projected to be valued at US$612.4 million in 2026.

The market is expected to reach US$1,783.6 million by 2033.

Key market trends include the shift toward large satellite constellations and increasing focus on data monetization models.

Earth observation is expected to be the leading application with a share of nearly 44.2% in 2026, due to the shift from single large satellites to CubeSat constellations that provide high revisit rates.

The market is expected to grow at a CAGR of 16.5% from 2026 to 2033.

Blue Canyon Technologies, CU Aerospace L.L.C., EnduroSat, and GomSpace are a few key market players.