- Communication Infrastructure & Services

- Data Center Monitoring Market

Data Center Monitoring Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Monitoring Market by Component (Hardware, Software, Others), Solution (DCIM, Power Monitoring, Others), End-user, Deployment, and Regional Analysis for 2026 - 2033

Data Center Monitoring Market Size and Trends Analysis

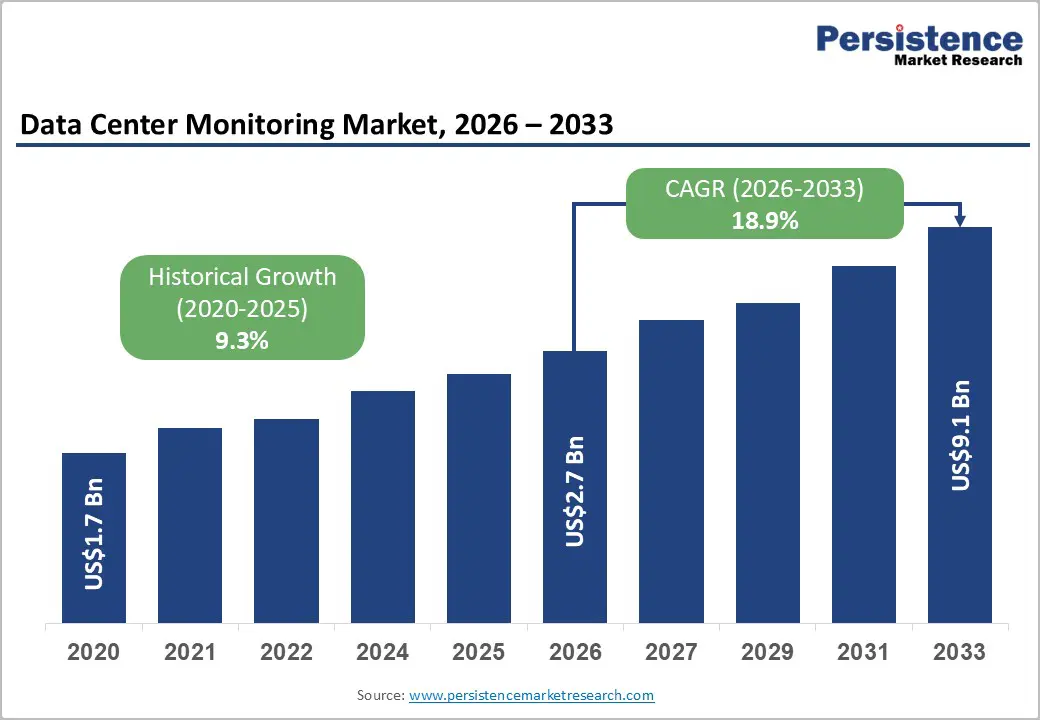

The global data center monitoring market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$9.1 billion by 2033, growing at a CAGR of 18.9% between 2026 and 2033, driven by the rising data-center electricity demand, stricter energy-performance reporting regulations in Europe, and increasing cybersecurity-monitoring requirements across critical digital infrastructure.

The rapid growth of AI workloads is significantly increasing rack power density, making real-time telemetry and predictive monitoring essential for uptime and operational efficiency. Regulatory initiatives related to energy efficiency, carbon disclosure, and operational resilience are also accelerating enterprise investment in advanced monitoring platforms.

Key Industry Highlights:

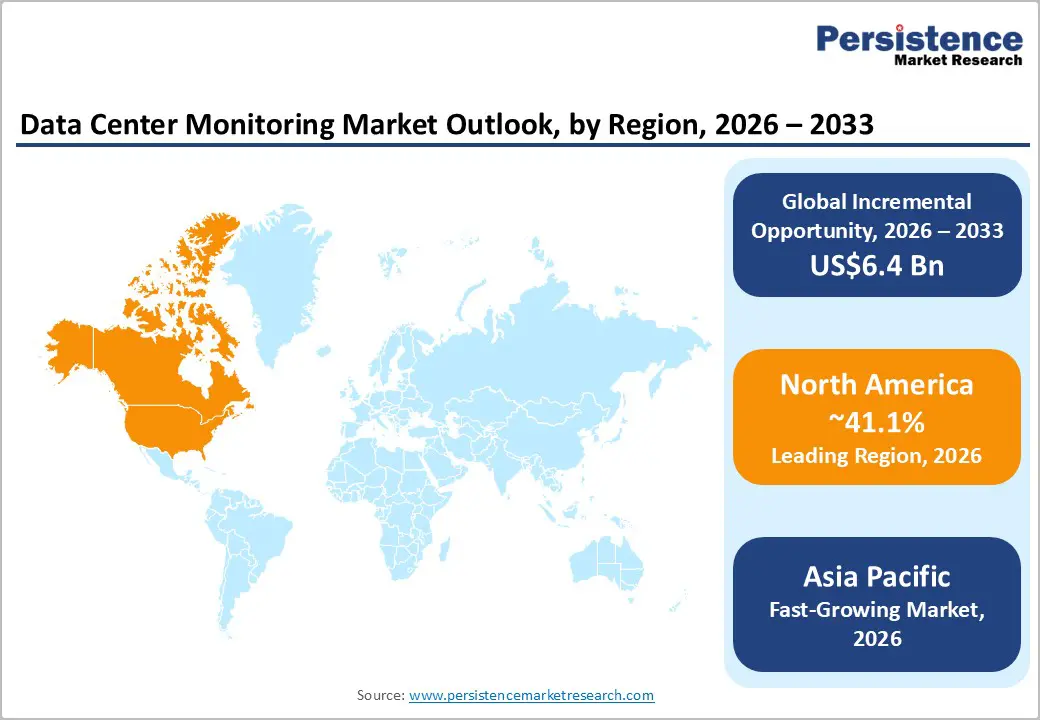

- Leading Region: North America is projected to account for 41.1% market share in 2026, supported by hyperscale infrastructure expansion, advanced cloud adoption, and strong investment in AI-ready data centers across the U.S.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market during the forecast period, driven by rapid digitalization, hyperscale investments, and expanding cloud and colocation infrastructure across China, India, Japan, and ASEAN countries.

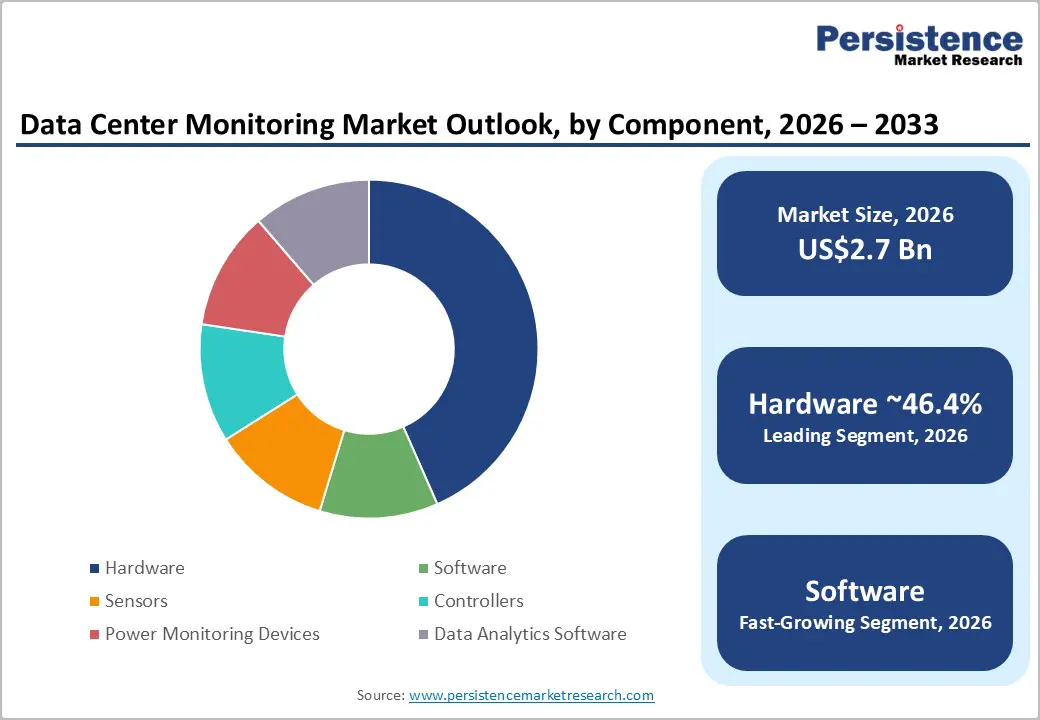

- Dominant Component: Hardware is anticipated to lead with 46.4% of market share in 2026, supported by strong demand for sensors, controllers, intelligent PDUs, environmental monitors, and power-management devices across hyperscale and colocation facilities.

- Leading Solution: DCIM (Data Center Infrastructure Management) is estimated to account for 38.3% of market share in 2026, driven by increasing demand for centralized visibility across power, cooling, network, environmental, and asset-management infrastructure.

DRO Analysis

Drivers - AI Workloads and High-Density Infrastructure Are Driving Demand for Advanced Monitoring

AI training and inference applications are transforming data-center infrastructure requirements. High-performance computing clusters require significantly greater power and cooling capacity than conventional enterprise workloads, increasing the importance of continuous telemetry and predictive infrastructure analytics. Operators now need monitoring systems capable of identifying thermal hotspots, cooling inefficiencies, power fluctuations, and asset utilization trends in real time.

The expansion of hyperscale AI infrastructure is also driving investment in liquid-cooling systems, high-density racks, and modular power architectures, all of which require integrated monitoring capabilities. Monitoring platforms are becoming central to operational decision-making because downtime risks, power inefficiencies, and cooling failures can directly affect revenue generation and service availability. Vendors are increasingly integrating AI-driven analytics, predictive maintenance, and automated fault detection into their monitoring portfolios to support next-generation infrastructure environments.

Compliance, Cybersecurity, and Reliability Requirements Are Expanding Monitoring Budgets

Data-center operators are facing increasing pressure to improve operational transparency, energy accountability, and cybersecurity resilience. Continuous monitoring is now considered essential for maintaining uptime, meeting sustainability targets, and complying with evolving regulatory frameworks. Governments and regulatory agencies are strengthening reporting requirements for energy use, carbon emissions, and infrastructure resilience, particularly in Europe and North America.

Cybersecurity governance frameworks are also emphasizing continuous risk monitoring and operational visibility across critical infrastructure environments. Enterprises are increasingly investing in monitoring systems that provide centralized dashboards, automated incident response, audit trails, and predictive diagnostics. Rising outage frequency and the growing financial impact of downtime are also prompting organizations to prioritize investments in integrated monitoring platforms that improve root-cause analysis and operational reliability.

Restraint - Integration Complexity in Legacy Infrastructure Environments Remains a Major Challenge

Many organizations continue to operate mixed infrastructure environments that combine legacy building-management systems, older power equipment, modern IoT sensors, and multiple software platforms. Integrating these disconnected systems into a unified monitoring architecture can be technically complex and financially demanding. Older facilities often lack interoperability standards, forcing operators to invest heavily in customization, middleware, and specialized integration services.

Implementation timelines can become extended due to compatibility testing, cybersecurity validation, and operational migration risks. Small and mid-sized operators may delay deployments because the upfront integration cost can outweigh short-term operational savings. In addition, brownfield environments frequently require extensive infrastructure modernization before advanced monitoring systems can operate efficiently. These challenges slow adoption rates in certain enterprise and colocation segments despite strong long-term demand fundamentals.

Opportunities - Regulatory Reporting Is Creating a Long-Term Opportunity for Monitoring Software Platforms

Energy-efficiency reporting regulations are creating substantial growth opportunities for monitoring software vendors. Operators increasingly require centralized platforms capable of tracking energy consumption, cooling performance, water utilization, and carbon-efficiency metrics across multiple facilities. Monitoring systems are becoming essential tools for sustainability reporting, compliance auditing, and operational benchmarking.

The growing emphasis on environmental accountability is encouraging organizations to adopt software platforms that can automate KPI reporting, generate compliance dashboards, and support long-term energy-optimization strategies. Vendors that combine power monitoring, environmental analytics, and compliance management into integrated software ecosystems are likely to strengthen recurring subscription revenue opportunities. This trend is particularly significant in Europe, where regulatory harmonization is accelerating demand for standardized reporting frameworks across large-scale data-center operations.

Cloud-Based Monitoring Is Expanding Across Distributed and Edge Infrastructure

The expansion of edge computing, distributed cloud environments, and multi-site infrastructure is increasing demand for cloud-based monitoring platforms. Organizations increasingly require centralized visibility across geographically dispersed assets without relying on large on-site operational teams. Cloud-based monitoring solutions provide scalable infrastructure oversight, remote diagnostics, predictive maintenance capabilities, and centralized analytics.

Operators are also prioritizing subscription-based monitoring services because they reduce deployment complexity and accelerate implementation timelines. The ability to standardize monitoring policies across multiple sites is becoming increasingly valuable for colocation providers, telecom operators, and cloud service providers. As edge infrastructure deployments continue to expand, cloud-native monitoring architectures are expected to become a major long-term growth driver for the market.

Category-wise Analysis

Component Insights

Hardware is anticipated to account for 46.4% of the market share in 2026. The dominance of hardware reflects the infrastructure-intensive nature of data-center monitoring systems. Sensors, controllers, intelligent PDUs, environmental monitors, and power-management devices form the operational foundation of modern monitoring architectures. Large-scale facilities require dense deployment of telemetry hardware to monitor temperature, humidity, airflow, power consumption, and equipment performance in real time.

Demand remains particularly strong in hyperscale and colocation facilities where operators must maintain continuous visibility into power and thermal conditions. Hardware deployment is also increasing alongside investments in liquid cooling systems, modular infrastructure, and high-density AI clusters. As a result, physical monitoring equipment continues to represent a critical entry point for integrated monitoring deployments.

Software represents the fastest-growing component segment, due to the increasing need for predictive analytics, automation, and centralized operational intelligence. Operators are shifting from reactive monitoring toward AI-assisted optimization and predictive maintenance strategies. Modern monitoring software platforms now provide asset discovery, dependency mapping, workflow automation, anomaly detection, and capacity forecasting capabilities.

The shift toward distributed infrastructure environments is further accelerating software demand because centralized orchestration is more efficient than manually managing multiple sites. Software vendors are increasingly offering subscription-based platforms that combine monitoring, analytics, and reporting capabilities into unified operational ecosystems. This transition is helping operators improve infrastructure efficiency, reduce downtime risk, and optimize energy consumption across large-scale deployments.

Solution Insights

DCIM (Data Center Infrastructure Management) is estimated to hold 38.3% of the market share in 2026. DCIM platforms provide centralized visibility across power systems, cooling infrastructure, network environments, space utilization, and asset management. Their ability to integrate multiple operational functions into a single management layer makes them highly valuable for hyperscale and colocation facilities.

Operators increasingly rely on DCIM solutions to optimize capacity planning, improve energy efficiency, and support compliance reporting. The growing complexity of AI-ready infrastructure is further increasing demand for integrated management platforms that can correlate operational data across multiple infrastructure domains. DCIM solutions also play an important role in predictive maintenance and operational automation initiatives, strengthening their position within the broader monitoring ecosystem.

Power monitoring is emerging as the fastest-growing solution segment because electricity consumption has become one of the most critical operational concerns for data-center operators. AI workloads are significantly increasing rack-level power density, forcing organizations to improve visibility into electrical distribution systems and energy utilization patterns.

Monitoring platforms capable of tracking real-time energy consumption, voltage fluctuations, and power quality metrics are becoming essential for infrastructure optimization and compliance with sustainability standards. Operators are also using power-monitoring tools to improve capacity planning, reduce energy waste, and support carbon-reduction initiatives.

Regional Insights

North America Data Center Monitoring Market Trends

North America is projected to lead the market with approximately 41.1% market share in 2026, supported by strong hyperscale investment activity, advanced cloud infrastructure adoption, and rapid AI-driven capacity expansion.

U.S. Data Center Monitoring Market Trends

The U.S. represents the largest market within the region and is projected to grow at a CAGR of 19.2% during the forecast period. The country benefits from a highly mature digital ecosystem, large-scale enterprise cloud adoption, and continuous investment in AI-ready hyperscale infrastructure. Major technology companies are expanding data-center campuses across Virginia, Texas, Arizona, and Oregon, increasing the need for predictive maintenance, thermal optimization, intelligent power-monitoring systems, and centralized DCIM platforms.

The U.S. is also witnessing growing investment in liquid cooling technologies and high-density computing environments, both of which require advanced telemetry and real-time environmental monitoring. Enterprises are increasingly implementing integrated monitoring architectures to improve uptime reliability, support cybersecurity compliance, and optimize energy utilization.

Sustainability initiatives and carbon-efficiency goals are further strengthening demand for advanced monitoring software that tracks power usage effectiveness (PUE), cooling efficiency, and environmental KPIs. The region’s emphasis on operational resilience, combined with rising outage-prevention requirements, is expected to maintain North America’s position as the most technologically advanced and commercially mature regional market for premium monitoring solutions.

Canada Data Center Monitoring Market Trends

Canada is emerging as an important secondary market due to increasing cloud adoption, favorable climate conditions for energy-efficient cooling, and rising investment in sustainable digital infrastructure. Provinces such as Ontario and Quebec are attracting colocation and hyperscale investments due to reliable renewable energy availability and lower cooling costs.

Canadian operators are increasingly deploying intelligent monitoring systems to improve energy efficiency, support regulatory compliance, and manage distributed infrastructure environments. The country’s focus on green data center development and operational sustainability is expected to create long-term demand for power-monitoring and environmental management platforms.

Europe Data Center Monitoring Market Trends

Europe is experiencing strong market growth driven by increased focus on sustainability compliance, energy efficiency, and infrastructure transparency.

Germany Data Center Monitoring Market Trends

Germany represents one of the region’s most significant markets, supported by industrial digitalization initiatives, enterprise cloud migration, and expanding colocation infrastructure. German operators are increasingly investing in centralized monitoring systems capable of tracking energy consumption, cooling performance, carbon utilization metrics, and operational efficiency across large-scale facilities. The country’s strong manufacturing and industrial technology base is accelerating the adoption of predictive maintenance systems and automated infrastructure management platforms.

Data-center operators are also prioritizing intelligent cooling systems and energy analytics to improve sustainability performance and reduce operational costs. Germany’s role as a major European connectivity hub is expected to continue supporting long-term investment in advanced monitoring solutions.

U.K. Data Center Monitoring Market Trends

The U.K. remains a leading European market due to high enterprise cloud adoption and continued expansion of colocation capacity. London continues to serve as a major connectivity and hyperscale hub, increasing demand for DCIM solutions, environmental monitoring systems, and AI-driven infrastructure analytics.

Operators are focusing heavily on operational resilience, cybersecurity governance, and energy-efficiency optimization as enterprise workloads become increasingly distributed. The UK market is also benefiting from strong financial services digitization and increasing demand for edge computing infrastructure. Monitoring platforms that support remote diagnostics, predictive maintenance, and multi-site operational visibility are seeing significant adoption across colocation and enterprise facilities.

Asia Pacific Data Center Monitoring Market Trends

Asia Pacific is projected to be the fastest-growing regional market due to rapid digitalization, expanding internet penetration, and large-scale infrastructure investment across China, India, Japan, and Southeast Asia.

China Data Center Monitoring Market Trends

China represents the region’s largest market, supported by national technology modernization initiatives and continued investment in hyperscale and AI-ready data-center campuses. The country is significantly expanding cloud infrastructure capacity to support AI development, industrial digitalization, and enterprise cloud migration.

Chinese operators are increasingly investing in intelligent monitoring systems to improve energy efficiency, reduce downtime risks, and optimize power utilization across high-density computing environments. The rapid deployment of edge-computing infrastructure and government-backed digitalization programs is further strengthening demand for centralized monitoring platforms and predictive-maintenance technologies.

Japan Data Center Monitoring Market Trends

Japan remains a strategically important market due to its strong focus on operational resilience, disaster recovery preparedness, and energy-efficient infrastructure development. Japanese operators are prioritizing intelligent cooling systems, automated environmental monitoring, and advanced power management platforms to support high-reliability digital infrastructure.

The country’s emphasis on uptime reliability and operational continuity is increasing investment in predictive analytics and AI-assisted monitoring solutions. Japan’s mature enterprise technology landscape and ongoing digital transformation initiatives are expected to support stable, long-term demand for advanced data center monitoring technologies.

India Data Center Monitoring Market Trends

India is emerging as one of the region’s fastest-growing markets due to rising cloud adoption, enterprise digitalization, expanding internet penetration, and increasing demand for colocation services. Major metropolitan areas such as Mumbai, Chennai, Hyderabad, and Bengaluru are witnessing large-scale investments in hyperscale and colocation facilities. Operators are deploying intelligent monitoring systems to improve operational scalability, optimize energy consumption, and support high-density infrastructure environments.

Government initiatives supporting digital infrastructure development and data localization requirements are also driving increased investment in data centers. The rapid growth of AI workloads, fintech platforms, e-commerce ecosystems, and telecom data traffic is expected to accelerate long-term demand for DCIM, power monitoring, and environmental management solutions across India.

Competitive Landscape

The global data center monitoring market remains moderately fragmented, with competition distributed across infrastructure providers, software vendors, and specialized monitoring companies. Major players compete across hardware, DCIM software, power monitoring, predictive analytics, and environmental management solutions.

Leading companies are prioritizing AI-driven analytics, recurring software revenue, cloud-based monitoring services, and integrated infrastructure ecosystems. Strategic partnerships, predictive-maintenance capabilities, sustainability reporting tools, and operational automation are becoming key competitive differentiators across the market.

Key Industry Developments:

- In August 2025, Vertiv acquired Waylay NV to strengthen its AI-driven monitoring, predictive maintenance, and operational intelligence capabilities for data-center power and cooling systems.

- In November 2025, Schneider Electric launched new EcoStruxure data-center solutions engineered for high-density AI and accelerated computing environments, including liquid-cooling-ready rack systems, prefabricated modular architectures, and AI-focused monitoring infrastructure.

Companies Covered in Data Center Monitoring Market

- Schneider Electric

- Vertiv

- Eaton

- ABB

- Siemens

- Johnson Controls

- Cisco Systems

- IBM

- Huawei Technologies

- Sunbird Software

- Nlyte Software

- Device42

- FNT Software

- Panduit

- CommScope

- Delta Electronics

Frequently Asked Questions

The global data center monitoring market is likely to be valued at US$2.7 billion in 2026.

The data center monitoring market is expected to reach approximately US$9.1 billion by 2033.

Key trends include the rapid adoption of AI-driven predictive analytics, expansion of hyperscale and edge data centers, increasing deployment of cloud-based monitoring platforms, rising investment in intelligent power monitoring, and growing focus on sustainability reporting and energy optimization.

Hardware is expected to be the leading component segment, accounting for approximately 46.4% market share in 2026. The segment is supported by strong demand for sensors, controllers, intelligent PDUs, environmental monitoring devices, and power-management systems across hyperscale and colocation facilities.

The data center monitoring market is projected to grow at a CAGR of 18.9% between 2026 and 2033.

Major companies operating in the market include Schneider Electric, Vertiv, Eaton, ABB, and Siemens.