- Oil & Gas

- Oil and Gas Drone Service Market

Oil and Gas Drone Service Market Size, Share, and Growth Forecast, 2026 - 2033

Oil and Gas Drone Service Market by Drone Type (Multi-Rotor, Fixed-Wing, Single Rotor, Hybrid), Application (Inspection, Surveying & Mapping, Others), Operational Use (Pipeline Maintenance, Drilling, Others), and Regional Analysis 2026 - 2033

Oil and Gas Drone Service Market Size and Trends Analysis

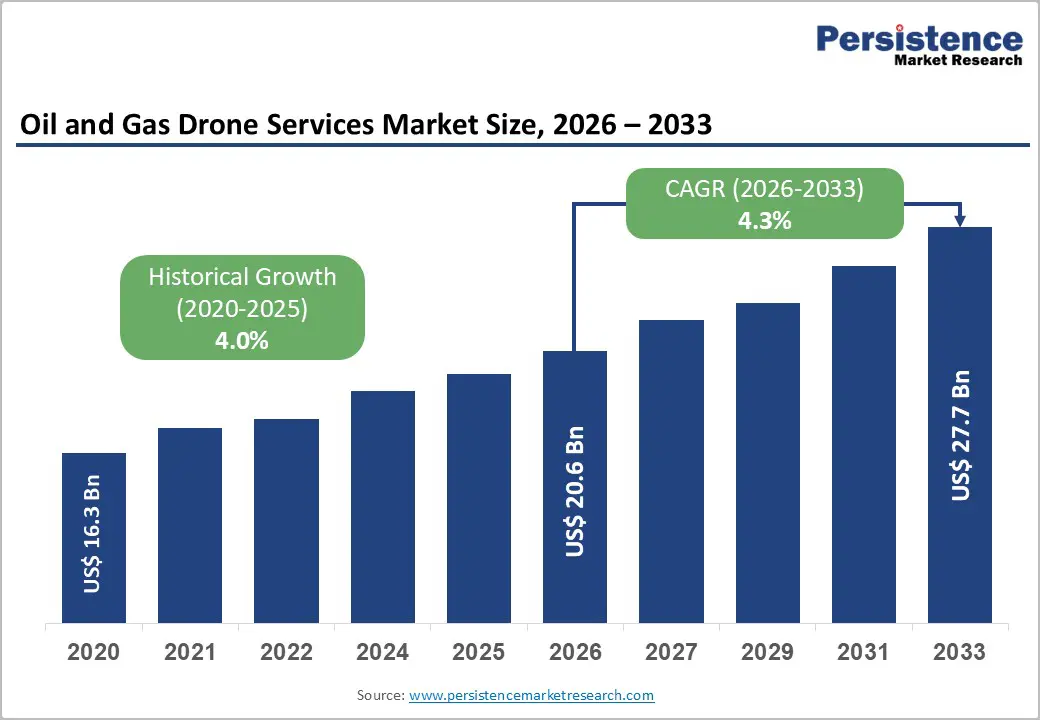

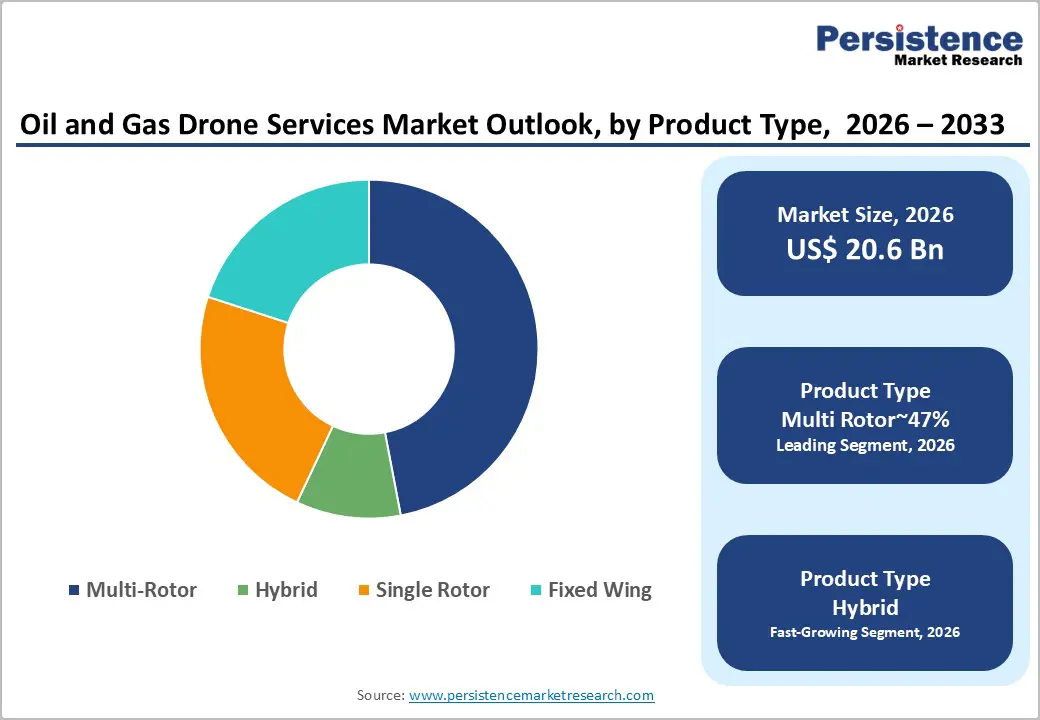

The global oil and gas drone service market size is likely to be valued at US$20.6 billion in 2026 and is expected to reach US$27.7 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by the rising demand for automated inspection solutions.

Operators are increasingly adopting unmanned systems to monitor aging infrastructure across remote locations. Technological advancements in sensor payloads are further accelerating the integration of drones into daily workflows. Regulatory mandates for asset integrity push operators toward remote monitoring solutions that reduce human exposure in hazardous zones.

Technology integration, such as AI-driven analytics, enhances detection accuracy across pipelines and rigs. This convergence sustains procurement momentum as vendors align offerings with compliance needs. Enhanced data processing capabilities support real-time decision-making within complex upstream and downstream environments. The market is expected to grow steadily as infrastructure demand increases.

Key Industry Highlights:

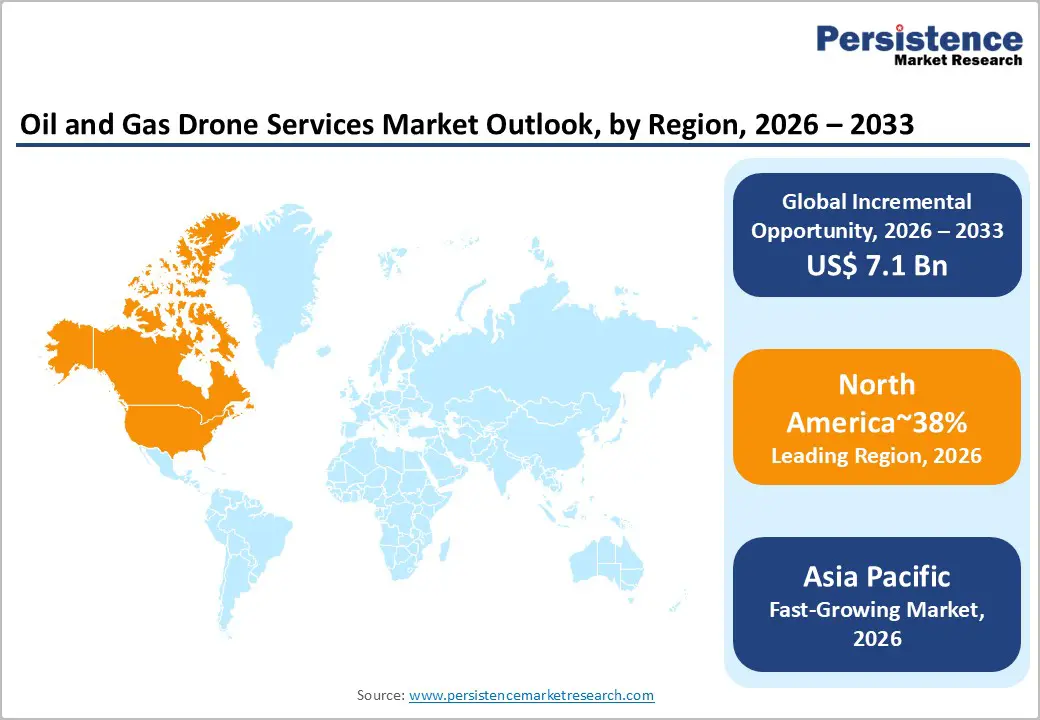

- Leading Region: North America is projected to lead, accounting for approximately 38% share in 2026, supported by extensive pipeline networks, mature regulatory frameworks, and high adoption of VTOL drones.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid infrastructure buildout, increasing offshore exploration, and cost-sensitive operational upgrades.

- Leading Drone Type: Multi-Rotor is expected to lead, accounting for approximately 47% share in 2026, driven by superior vertical take-off capabilities, flight stability, and suitability for confined-rig inspections.

- Leading Application: Inspection is anticipated to dominate, accounting for approximately 55% share in 2026, anchored by critical asset integrity requirements and safety mandates, regulatory audits, and real-time data needs.

| Key Insights | Details |

|---|---|

| Oil and Gas Drone Service Market Size (2026E) | US$20.6 Bn |

| Market Value Forecast (2033F) | US$27.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

DRO Analysis

Driver Analysis - Remote Inspection Mandates

Regulatory frameworks mandate frequent inspection of hazardous oilfield assets across upstream operations. Operators increasingly adopt drone-based solutions to reduce personnel exposure and operational downtime costs. This transition elevates demand for stable aerial platforms supporting visual and thermal imaging capabilities. Compliance-driven timelines accelerate procurement cycles for inspection technologies across oilfield environments. Remote inspection enhances operational safety while improving monitoring consistency across distributed asset networks. Technology adoption aligns with stringent regulatory enforcement governing hazardous industrial site inspections. Inspection workflows evolve toward automated aerial systems integrated with analytical processing capabilities.

Sky-Futures, with the Scout API, integrates artificial intelligence into automated pipeline inspection workflows. Advanced analytics enable efficient detection of anomalies across extensive infrastructure networks. Demand for vertical takeoff and landing systems supports extended mission capabilities across remote environments. Autonomous flight solutions reduce inspection duration while improving data accuracy across operational sites. Integration of real-time analytics strengthens decision support within maintenance and monitoring operations. Service models expand through repeat inspection contracts driven by regulatory compliance requirements. Market growth aligns with increasing reliance on reliability-focused remote inspection deployments.

Safety Risk Mitigation in Hazardous Inspections

Elimination of human exposure in hazardous inspection environments drives the adoption of drone-based solutions. Inspection of flare stacks and offshore platforms involves significant risks from heat and elevation. Unmanned aerial systems enable detailed visual access without endangering operational personnel across sites. Enhanced safety protocols accelerate transition toward automated inspection workflows within energy infrastructure. Risk mitigation aligns with corporate responsibility frameworks governing industrial safety and workforce protection. Operational models increasingly prioritize remote inspection to reduce incident probability across hazardous environments. Safety-driven adoption reshapes inspection standards across asset-intensive energy operations.

Collision-resistant drone architectures enable safe navigation within confined industrial structures. Flyability's Elios 3 supports the inspection of complex enclosed environments across industrial assets. Protective cage design prevents structural damage during contact with internal surfaces and equipment. This capability enables accurate wall thickness assessment without requiring human entry into confined spaces. Advanced navigation systems enhance inspection precision within storage tanks and internal infrastructure. Formal validation by industrial bodies strengthens the acceptance of drone-based inspection technologies. Procurement increases as verified safety performance supports deployment across oilfield service ecosystems.

Restraint Analysis - High Capital Expenditure for Specialized Hardware

Acquisition of advanced drone platforms requires significant upfront capital investment across energy service providers. High-end sensors for methane detection and LiDAR mapping increase procurement costs for smaller firms. Ruggedized flight systems designed for extreme weather conditions further elevate total ownership expenses. Ongoing maintenance, including calibration and repair, imposes recurring financial burdens on operators. These cost structures create entry barriers within the competitive drone inspection service landscape. Budget constraints slow transition toward fully automated inspection fleets across energy infrastructure. Capital intensity limits the scalability of advanced unmanned inspection solutions across emerging service providers.

Limited availability of skilled technicians increases operational expenditure for managing specialized drone hardware. Training programs for high-risk operational environments demand time and financial commitment. Rapid innovation cycles accelerate the depreciation of existing drone equipment across service providers. Cost management challenges influence pricing strategies within inspection service contracts. Operational economics constrain the participation of smaller firms within advanced drone service ecosystems. Financial barriers reinforce market concentration among well-capitalized industry participants.

Data Security and Cybersecurity Vulnerability Risks

The integration of drones into enterprise networks introduces vulnerabilities to data privacy and cybersecurity. Unmanned platforms transmit sensitive infrastructure data through wireless and cloud communication channels. Unauthorized interception risks expose critical energy assets to potential breaches and industrial espionage. Government procurement policies increasingly reflect concerns regarding the origin and security of drone hardware. Encryption protocols and secure data-handling frameworks are now mandatory across industrial drone service contracts. These security requirements elevate technical complexity within deployment and operational management processes. Cybersecurity considerations reshape architecture design across connected drone inspection ecosystems.

Stringent data sovereignty regulations require localized storage and processing for sensitive operational datasets. Garuda Aerospace adapts industrial drone systems to comply with regional security mandates. Ensuring the integrity of aerial data during transmission remains a key engineering challenge. Clients demand validation of secure software architectures before enabling access to critical infrastructure networks. Enterprise-grade cloud security solutions enhance the protection of inspection data across operational workflows. Advanced cybersecurity frameworks support risk mitigation within connected drone ecosystems. Security-driven compliance continues to influence adoption and deployment strategies across the energy sectors.

Opportunity Analysis - AI-Driven Predictive Maintenance and Digital Twins

Integration of aerial inspection data with artificial intelligence enables predictive maintenance across energy infrastructure. Machine learning algorithms analyze large image datasets to detect early structural degradation patterns. This capability enables operators to address faults before they escalate into costly equipment failures. Digital twin frameworks create virtual replicas for continuous monitoring and scenario-based asset management. Transformation of raw inspection data into actionable intelligence enhances long-term infrastructure planning. Data-driven maintenance models improve reliability and lifecycle optimization across distributed energy assets. Operational strategies increasingly depend on intelligent analytics for proactive asset health management.

Cyberhawk with iHawk applies machine learning for prioritizing maintenance based on real-time asset conditions. Automated analysis reduces reliance on manual inspection workflows across engineering teams. Faster anomaly detection improves response times within field operations and maintenance planning. High-quality aerial data acquisition strengthens analytical model accuracy across inspection ecosystems. Integration of analytics platforms enhances coordination between inspection data and maintenance execution. Predictive insights support efficient allocation of resources across asset management programs. Technology convergence creates new service revenue opportunities within data-driven inspection frameworks.

Methane Quantification Push

Stricter emission reporting frameworks increase demand for precise methane quantification technologies. Regulatory mechanisms emphasize accurate mass balance measurement rather than simple leak detection approaches. Carbon pricing structures incentivize operators to deploy calibrated airborne sensing platforms across infrastructure networks. This requirement elevates the adoption of certified drone systems capable of delivering compliance-grade environmental data. Utilization is expanding across midstream operations, where emissions accountability is increasingly regulated. Measurement accuracy directly influences reporting credibility under evolving environmental governance standards. Operational practices shift toward data-validated emissions tracking across energy value chains.

Advanced sensing technologies enable parts-per-million-level measurement accuracy across inspection workflows. Operators integrate optical gas imaging compliant platforms to meet stringent verification requirements. Swarm-based drone deployments enhance plume modeling and dispersion analysis across large infrastructure areas. Data-driven emission tracking supports regulatory reporting and environmental accountability frameworks. Technology adoption improves monitoring accuracy and regulatory compliance. Regulatory-driven demand is expanding service opportunities in methane quantification and monitoring ecosystems.

Category-wise Analysis

Drone Type Insights

Multi-Rotor is expected to lead the market, accounting for approximately 47% share in 2026, underpinned by superior maneuverability and stable hovering capabilities. These systems are essential for detailed visual inspections of vertical structures such as flare stacks and cooling towers. Vertical take-off and landing features enable deployment from small platforms or cluttered industrial environments without runways. Operators prioritize these drones for high-resolution photography and thermal imaging in confined or complex plant layouts. DJI with the Matrice 350 RTK and Flyability with the Elio 3 demonstrate the versatility of multi-rotor architectures in hazardous zones. Advanced flight controllers and obstacle-avoidance systems further enhance operational reliability during close-proximity missions. This structural alignment with asset-specific inspection needs sustains the segment's dominant market position.

Hybrid is expected to be the fastest-growing segment, driven by the growing need for long-range surveillance and vertical take-off flexibility. These platforms merge the endurance of fixed-wing designs with the hovering precision of multi-rotor systems for complex missions. Energy companies are seeking solutions that can cover hundreds of miles of pipeline while still performing detailed point inspections. This dual-capability reduces the total number of specialized drones required for diverse regional monitoring tasks. Airobotics with Optimus System and American Robotics with Scout System exemplify the trend toward versatile, long-endurance autonomous platforms. Ongoing enhancements in power management and aerodynamic efficiency are expanding the operational scope of hybrid unmanned vehicles. As midstream operators prioritize wide-area oversight, hybrid systems are gaining significant traction across modern energy landscapes.

Application Insights

Inspection is anticipated to lead, accounting for approximately 55% of the market in 2026, supported by the critical nature of asset integrity management. Maintaining high-value infrastructure requires frequent and detailed assessments to prevent catastrophic failures or environmental incidents. Drones provide a non-destructive testing method that significantly reduces the time and cost of traditional manual inspections. Utilization remains anchored in the ability to capture real-time data from elevated or dangerous locations without halting production. Cyberhawk, with iHawk and Mistras Group, with specialized aerial inspection services, addresses these core industrial requirements through integrated data workflows. Enterprise-level demand for digital audit trails further strengthens the adoption of drone-based inspection protocols. This convergence of safety mandates and operational efficiency reinforces the segment's leadership within energy markets.

Methane leak detection is projected to be the fastest-growing, driven by tightening international emissions standards and corporate decarbonization goals. Modern sensor technologies allow unmanned platforms to visualize invisible gas plumes and quantify leak rates with high precision. This capability is becoming essential for compliance with new environmental regulations regarding atmospheric discharge from oilfields. Companies are moving away from episodic ground surveys toward continuous, automated aerial monitoring to identify leaks immediately. Percepto with Air Max and DJI with specialized gas sensing payloads lead the transition toward autonomous emission oversight. Integration with cloud-based reporting platforms supports transparent sustainability tracking for large-scale energy operations. As environmental accountability intensifies, demand for specialized methane quantification services is accelerating across the value chain.

Regional Insights

North America Oil and Gas Drone Service Market Trends

North America is expected to remain the leading regional market, accounting for approximately 38% of the market share in 2026, supported by high concentrations of aging infrastructure and early adoption of automated technologies. The region's dominance is anchored in a well-established regulatory framework that increasingly permits sophisticated commercial drone operations. Extensive pipeline networks and large-scale offshore facilities in maritime zones necessitate frequent and detailed inspection routines to maintain safety standards. High labor costs further drive the shift toward autonomous systems capable of performing complex data collection with minimal personnel requirements. Leading energy companies are actively integrating unmanned aerial vehicles into their standard maintenance and emergency response protocols.

The US is expected to anchor regional momentum through sustained investments in autonomous drone systems and supportive flight regulations. The recent surge in FAA waivers for BVLOS operations is accelerating the deployment of drones for long-range pipeline monitoring across remote states. American Robotics with Scout System is positioned to benefit from these regulatory shifts by providing fully automated flight solutions for industrial sites. Major domestic energy producers are prioritizing drone use to meet new environmental mandates for methane leak detection and quantification. This alignment between government policy and corporate investment is projected to sustain consistent market expansion within the country.

Asia Pacific Oil and Gas Drone Service Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid energy infrastructure buildout and industrial modernization accelerate market expansion. The region's growth is anchored in massive investments in new pipeline projects and offshore exploration across emerging maritime sectors. Governments are increasingly supporting the adoption of digital technologies to enhance the efficiency and safety of national energy production. A large volume of new facility construction offers opportunities to immediately integrate drone-based surveying and mapping during the initial phases of development. Cost-driven adoption is further supported by the presence of numerous hardware manufacturers and software developers within the region.

China is anticipated to lead the regional acceleration through significant government-led initiatives focused on digital oilfield development and automated monitoring. The country's vast inland and offshore energy assets are increasingly being managed using sophisticated unmanned systems for routine integrity checks. DJI, with its Matrice 350 RTK, remains a key technology provider, leveraging its strong domestic presence to set industrial standards. India is driving regional dynamics through ONGC initiatives to deploy drones for patrols on aging networks. Regulatory easing under DGCA supports BVLOS trials in refineries. Percepto with Sparrow aligns with localization bids for GAIL pipelines. Investment forecasts point to procurement surges in midstream segments.

Europe Oil and Gas Drone Service Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in environmental compliance and asset premiumization. The region's market is characterized by strict sustainability mandates that require frequent and highly accurate monitoring of carbon emissions. Older offshore assets in the northern maritime zones demand intensive structural inspections to ensure continued safe operation and longevity. Vendors are focusing on delivering high-end service models that integrate advanced data analytics and predictive maintenance capabilities. Institutional support for green energy transitions is also influencing the types of drone technologies deployed within the sector.

Norway is expected to anchor European demand through its leadership in offshore oil and gas technology and maritime safety standards. The country's extensive deep-water operations rely on sophisticated unmanned systems for subsea and surface inspections in harsh environmental conditions. Flyability's Elios 3 has found significant application at Norwegian offshore facilities for confined-space inspections of ship hulls and tanks. Regulatory bodies in the country are at the forefront of certifying drone technologies for critical industrial use cases. Ongoing investments in offshore platform modernization are likely to sustain the demand for premium aerial and underwater drone services.

Competitive Landscape

The oil and gas drone service market remains fragmented, with participation spanning specialized operators and integrated technology providers such as DJI, Cyberhawk, and Percepto. Market structure is shaped by diverse operational requirements, regional regulatory constraints, and the need for customized sensor payloads across upstream and midstream assets. These players exert influence through advanced UAV platforms, proprietary analytics software, and long-term service contracts with energy majors. Solutions like DJI Matrice 350 RTK, Cyberhawk iHawk, and Percepto Air Max establish benchmarks for inspection reliability, autonomy, and compliance monitoring.

Competitive positioning reflects vertical differentiation through payload specialization and software-driven analytics rather than broad service standardization. Premium providers emphasize autonomous navigation, AI-enabled defect detection, and non-destructive testing capabilities for offshore and hazardous sites. Companies such as Flyability and Sky-Futures advance niche inspection solutions tailored to confined and high-risk environments. Value-oriented participants leverage standardized drone platforms to deliver cost-efficient surveillance and mapping services across extensive pipeline networks. Industry dynamics include acquisitions targeting sensor innovation and digital twin integration. Platform evolution increasingly centers on automated reporting, predictive maintenance analytics, and ecosystem partnerships.

Key Industry Developments:

- In April 2026, ZenaTech and other active DaaS players were highlighted for rapid expansion as the Drone-as-a-Service market approached a US$13 billion valuation. The industry shift toward "renting" rather than "buying" drones allows oil and gas companies to access the latest sensors (LiDAR, thermal) without high capital expenditure.

- In March 2026, Ondas Holdings secured a strategic investment in Unusual Machines (UMAC), a manufacturer of drone parts, to strengthen its supply chain for autonomous systems. This investment ensures a resilient supply of critical drone components (inventory) for Ondas' industrial drone fleets, mitigating risks of global supply chain disruptions.

- In December 2025, AIRO Group Holdings expanded its operations into the YMX Innovation Zone in Quebec to develop medium-lift cargo drones for industrial logistics. The move enables the delivery of critical parts and sensors to remote oil and gas sites, reducing downtime for "middle-mile" industrial logistics.

Companies Covered in Oil and Gas Drone Service Market

- DJI Enterprise

- Percepto

- Cyberhawk

- Flyability

- American Robotics

- Airobotics

- Exyn Technologies

- Skydio

- AeroVironment

- Volatus Aerospace

- Sky-Futures

- Teledyne FLIR

- Garuda Aerospace

- VideoRay

- Quantum-Systems

- PrecisionHawk

Frequently Asked Questions

The oil and gas drone service market is projected to be valued at US$20.6 billion in 2026 and is expected to reach US$27.7 billion by 2033, driven by increasing adoption of automated inspection systems and regulatory mandates for asset integrity across hazardous energy infrastructure.

Remote inspection is a primary driver as it reduces human exposure to hazardous environments while improving operational efficiency. Drone-based systems enable real-time monitoring of pipelines, rigs, and offshore assets, aligning with stringent regulatory compliance requirements and lowering downtime and maintenance costs.

The oil and gas drone service market is forecast to grow at a CAGR of 4.3% from 2026 to 2033, reflecting steady demand for AI-enabled inspection, predictive maintenance, and methane monitoring solutions across upstream and midstream operations.

North America is the leading regional market, accounting for approximately 38% share, supported by extensive pipeline infrastructure, advanced regulatory frameworks, and early adoption of autonomous drone technologies for inspection and surveillance.

The market is fragmented, with key players including DJI, Cyberhawk, Percepto, Flyability, and American Robotics, competing through advanced UAV platforms, AI-driven analytics, and long-term service contracts with energy operators.