- Metalworking & Fabrication

- Heli-Coil Thread Inserts Market

Heli-Coil Thread Inserts Market Size, Share and Growth Forecast, 2026 - 2033

Heli-Coil Thread Inserts Market by Application (Aerospace & Defense, Automotive, Industrial Machinery, Electrical & Electronics, Energy & Power, Marine, Medical Devices), Product Type (Free-Running Inserts, Screw-Locking Inserts, Heavy-Duty Inserts, Micro Inserts, Repair Inserts), Material Type, and Regional Analysis for 2026 - 2033

Heli-Coil Thread Inserts Market Share and Trends Analysis

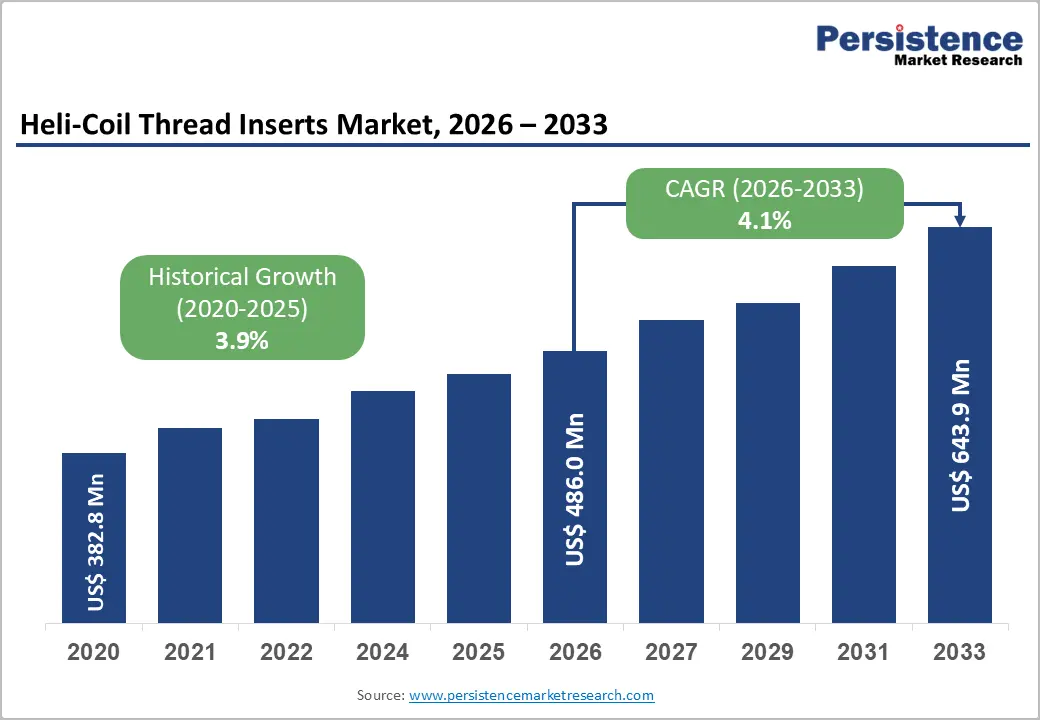

The global heli-coil thread inserts market size is likely to be valued at US$ 486.0 million in 2026 and is projected to reach US$ 643.9 million by 2033, growing at a CAGR of 4.1% during 2026–2033.

The market expansion is primarily driven by rising demand for lightweight fastening solutions, increasing adoption of thread repair inserts in aerospace and automotive manufacturing, and growing industrial maintenance requirements across aging machinery infrastructure. According to industry-aligned insights from manufacturing associations and aerospace regulatory bodies such as FAA and EASA, structural reliability and vibration resistance remain key performance requirements influencing adoption. Additionally, the shift toward high-performance materials in engineering applications continues to strengthen demand for precision-engineered wire thread inserts across global industries.

Key Industry Highlights:

- Dominant Application Segment: Aerospace & defense is expected to lead the heli-coil thread inserts market with an estimated 34% share in 2026, driven by high structural reliability requirements while automotive is projected to be the fastest-growing segment.

- Product type dynamics: Free-running inserts are anticipated to dominate the market with an estimated 38% share in 2026, while screw-locking inserts are expected to be the fastest growing, supported by high-vibration applications in aerospace and EV systems.

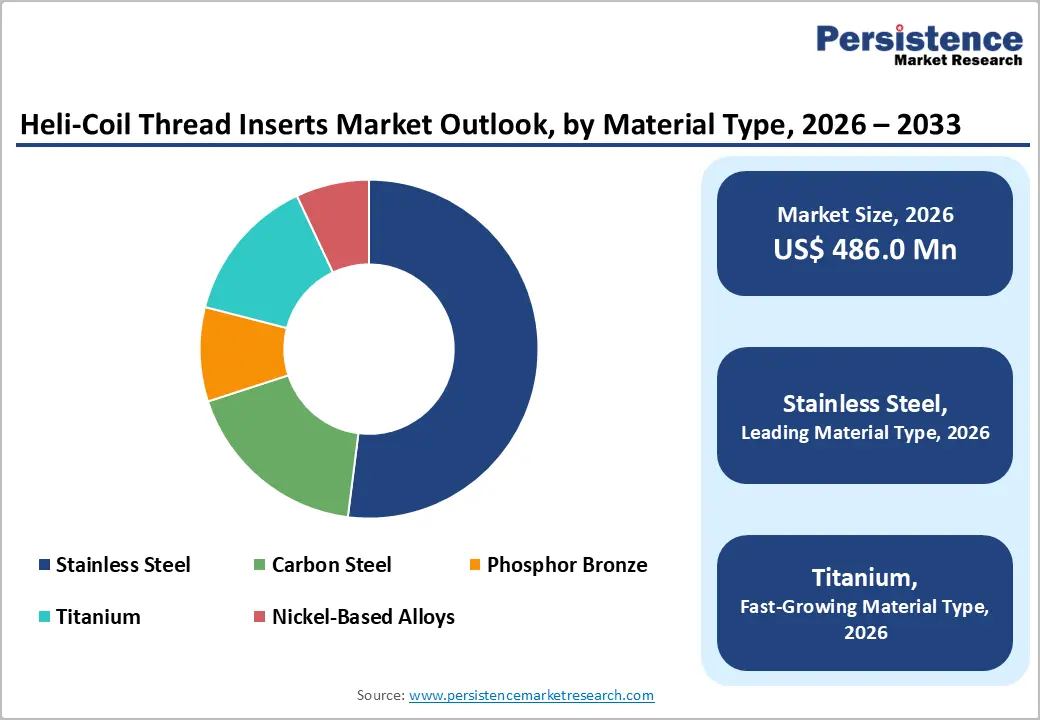

- Material leadership: Stainless steel is expected to hold the largest share at around 52% in 2026 due to wide industrial use, while titanium is projected to grow the fastest, driven by aerospace and EV lightweighting demand.

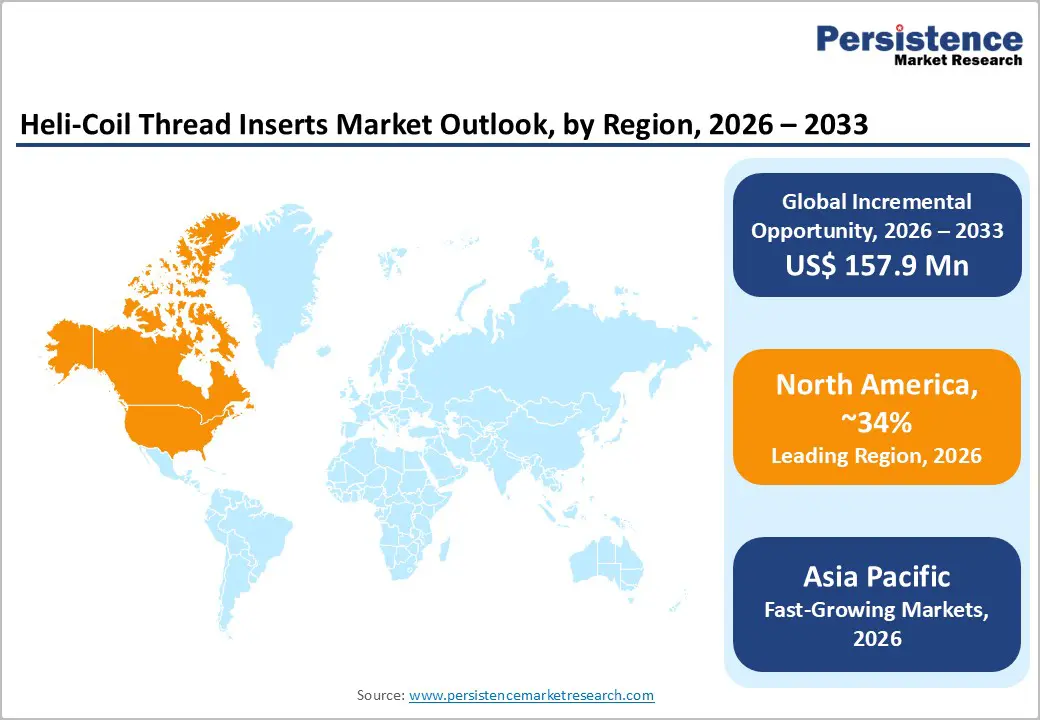

- Regional leadership: North America leads the heli-coil thread inserts market with an estimated 34% share in 2026, Asia Pacific emerge as the fastest-growing regional market due to strong EV manufacturing growth, aerospace outsourcing, and large-scale industrial production in China, India, and Japan.

- Competitive Environment: The market remains moderately consolidated with strong OEM-linked supply chains and competition driven by product innovation and material advancements.

DRO Analysis

Driver - Rising aerospace production ramp-up and certified supply chain expansion strengthens the demand for reliable fastening systems

The heli-coil thread inserts market is gaining strong momentum from rising aerospace production and increasingly strict certification-driven manufacturing standards across global aircraft programs. In 2025–2026, aviation regulators such as the FAA and EASA continue to tighten airworthiness and fatigue-resistance requirements, raising the importance of highly reliable fastening systems in critical aircraft structures. Aircraft OEMs are accelerating production of narrow-body fleets to meet sustained global air travel demand, directly increasing the use of precision thread repair inserts in high-load assembly operations.

At the same time, aerospace supply chains are shifting toward diversified and certified vendor ecosystems to improve resilience and ensure compliance consistency across OEM and MRO operations. This transition is boosting demand for standardized, high-performance fastening components across both new builds and maintenance activities. Additionally, wider adoption of lightweight aluminum-lithium alloys and composite structures is intensifying the need for reinforcement solutions that can withstand vibration and cyclic stress. These combined developments are creating a strong and sustained demand environment for heli-coil thread inserts in aerospace applications.

Restraint - Raw Material Volatility and Aerospace Supply Chain Constraints Intensifying Cost Pressure

Despite strong demand fundamentals, the heli-coil thread inserts market is facing cost pressure from raw material volatility and ongoing aerospace supply chain constraints. Extended lead times for critical inputs continue to disrupt aerospace manufacturing, with bottlenecks across fasteners, forgings, and specialty alloys affecting production schedules. Key materials such as titanium and nickel-based alloys remain in limited supply, driving price instability and procurement uncertainty.

The strict certification and quality compliance requirements from aviation regulators increase sourcing complexity and raise the cost of approved materials. Geopolitical disruptions affecting critical mineral flows further tighten availability, especially for aerospace-grade inputs. As a result, OEMs and suppliers face higher input costs, longer procurement cycles, and reduced inventory flexibility. This creates a challenging environment for small and mid-scale manufacturers, limiting the adoption of premium thread repair inserts in cost-sensitive applications.

Opportunity - EV manufacturing acceleration and supply chain localization driving fastening demand

The heli-coil thread inserts market is benefiting from strong EV manufacturing expansion and continued supply chain localization efforts across major economies. Government-led initiatives, particularly in markets such as India, are supporting EV adoption through production incentives, battery localization programs, and infrastructure development, accelerating large-scale manufacturing growth. At the same time, global OEMs are restructuring supply chains to reduce dependency risks and strengthen regional production ecosystems amid geopolitical uncertainties in critical mineral sourcing.

This shift is increasing demand for thread repair inserts, as EV platforms rely heavily on lightweight aluminum structures in battery housings, motor assemblies, and chassis systems. Growing gigafactory-scale production is further amplifying the need for high-precision fastening solutions suited for automated, high-volume assembly lines. Additionally, localization of advanced materials and manufacturing ecosystems is improving production resilience and consistency. These combined developments are positioning heli-coil thread inserts as a key enabler of scalable, durable, and efficient EV manufacturing growth.

Category-wise Analysis

By Application, Aerospace & Defense Dominate the Heli-coil Thread Inserts Market

The aerospace & defense segment leads the heli-coil thread inserts market with an estimated 33% share in 2026, driven by strict safety requirements and extensive use in aircraft assembly where structural integrity in aluminum airframes is critical. The ongoing narrow-body aircraft production ramp-ups and tighter FAA-led airworthiness compliance standards have strengthened demand for certified fastening systems across OEM and MRO operations. The continued aerospace manufacturing scaling and increasing focus on fatigue-resistant assemblies are reinforcing the use of precision thread repair inserts in critical structures.

The automotive segment is projected to be the fastest growing, supported by accelerating EV production and increased aluminum usage in lightweight vehicle platforms. EV manufacturing expansions and localized gigafactory-scale assembly growth are further boosting demand for high-reliability fastening solutions in battery housings and chassis systems, strengthening long-term market momentum.

By Material Type, Stainless Steel is a Dominant Type

Stainless steel inserts dominate the heli-coil thread inserts market with an estimated 51% share in 2026, driven by corrosion resistance and widespread use across aerospace, automotive, and industrial applications. The rising aircraft maintenance activity and ongoing industrial refurbishment cycles have further reinforced stainless steel as the preferred general-purpose fastening material across high-volume applications. The increased demand for durable and cost-efficient fastening solutions in multi-sector manufacturing is supporting its continued dominance.

Titanium inserts are projected to be the fastest-growing segment, supported by aerospace lightweighting programs and EV structural optimization initiatives. Ongoing aerospace design transitions focused on weight reduction and improved fuel efficiency are accelerating titanium adoption in high-stress aircraft assemblies, while EV manufacturers increasingly integrate lightweight materials to enhance performance and range efficiency.

Regional Analysis

North America Heli-Coil Thread Inserts Market Trends

North America leads the heli-coil thread inserts market with an estimated 34% share in 2026, supported by a strong aerospace manufacturing base and advanced industrial infrastructure in the United States. The sustained production activity across commercial aircraft assembly programs and defense modernization initiatives continues to drive demand for certified fastening systems in high-stress applications. FAA’s continued emphasis on airworthiness directives and structural fatigue monitoring is reinforcing the need for high-reliability thread repair inserts across OEM and maintenance operations.

The U.S. automotive sector is also strengthening demand, with expanding EV platform production and increased use of aluminum-intensive vehicle architectures. Recent federal-level support for domestic manufacturing expansion and semiconductor-linked industrial reshoring is further accelerating investment in automated production systems. Industrial automation adoption across smart factories is enhancing precision assembly requirements, boosting the usage of engineered fastening solutions. The presence of established aerospace and fastening OEM ecosystems continues to reinforce North America’s leadership in high-value applications.

Asia Pacific Heli-Coil Thread Inserts Market Trends

Asia Pacific is the fastest growing region in the heli-coil thread inserts market, expanding at around 5.8% CAGR through 2033, driven by rapid industrialization and large-scale expansion of automotive and aerospace production. China continues to scale high-volume EV production and next-generation manufacturing hubs, supported by industrial policy initiatives promoting advanced materials and localized supply chains. Japan’s precision engineering sector is witnessing steady demand for high-performance fastening solutions in robotics and electronics manufacturing. India is experiencing accelerated growth in defense manufacturing under expanded indigenous production programs, along with increasing automotive localization across global OEM facilities.

ASEAN countries are also seeing rising inflows of manufacturing investments, particularly in electronics and industrial machinery assembly. Regional governments are actively strengthening infrastructure and export-oriented manufacturing corridors, improving production scalability for precision components. Combined with cost-efficient manufacturing capabilities and expanding gigafactory ecosystems, Asia Pacific is emerging as a dominant global growth hub for thread repair inserts.

Europe Heli-Coil Thread Inserts Market Trends

Europe maintains a strong position in the heli-coil thread inserts market, supported by advanced engineering capabilities and high-value aerospace and automotive ecosystems across Germany, France, and the U.K. In 2025–2026, continued aircraft production stability across European aerospace programs and increased focus on next-generation aircraft efficiency are sustaining demand for certified fastening solutions. EU-wide regulatory emphasis on carbon reduction and material efficiency is driving greater adoption of lightweight structural designs, increasing reliance on precision thread repair inserts.

Germany’s industrial base is undergoing continued automation upgrades in manufacturing facilities, improving demand for high-precision fastening in machinery and equipment refurbishment. France is witnessing steady aerospace supply chain activity linked to advanced aircraft assembly and maintenance operations. The U.K. is seeing rising investment in offshore energy infrastructure and turbine lifecycle maintenance, strengthening demand for durable fastening systems. Additionally, European manufacturing modernization programs are accelerating the adoption of digital production systems and predictive maintenance technologies.

Competitive Landscape

The global heli-coil thread inserts market is moderately consolidated, led by major players such as Stanley Black & Decker (STANLEY Engineered Fastening), Böllhoff Group, Arconic Fastening Systems, and PennEngineering, which together account for a significant share of global revenues. These companies maintain strong positions through long-term OEM contracts in aerospace, automotive, and industrial machinery, supported by certified supply chain integration and strict quality compliance.

The competition is increasingly driven by innovation in lightweight materials, corrosion-resistant alloys, and high-performance thread repair inserts for critical applications. Strong R&D focus and aerospace-grade certifications continue to act as key entry barriers for new participants.

Regional and niche players such as TR Fastenings, Bossard Group, and Würth Group are strengthening their presence through distribution efficiency, customized fastening solutions, and responsive supply capabilities across key industrial markets. High certification requirements, OEM qualification cycles, and material compliance standards continue to restrict new entrants in aerospace and defense applications. However, increasing digital procurement adoption and supply chain partnerships are enabling mid-sized firms to expand their global reach. The market is expected to witness gradual consolidation through acquisitions, strategic alliances, and technology-driven differentiation.

Key Developments:

- In April 2026, Stanley Black & Decker exited the aerospace fastening market through the US $1.8 billion divestment of its Consolidated Aerospace Manufacturing (CAM) business to Howmet Aerospace, marking a strategic shift away from aerospace components toward core industrial tools and equipment.

Companies Covered in Heli-Coil Thread Inserts Market

- Stanley Black & Decker

- Böllhoff Group

- Arconic Fastening Systems

- TR Fastenings

- Bossard Group

- PennEngineering

- Kato Fastening Systems

- ITW Shakeproof

- Fontana Gruppo

- Arnold Umformtechnik

- LISI Group

- Stanley Black & Decker Industrial Division

- E-Z LOK

- Würth Group

- Bajaj Engineering Fasteners Division

Frequently Asked Questions

The global heli-coil thread inserts market is projected to reach US$ 486.0 million in 2026.

Rising aerospace manufacturing, increasing EV production, and growing demand for industrial maintenance drive the heli-coil thread inserts market.

The heli-coil thread inserts market is expected to grow at a CAGR of 4.1% from 2026 to 2033.

Expansion of EV manufacturing, renewable energy infrastructure growth, and industrial automation adoption create strong opportunities in the heli-coil thread inserts market.

Key players include Stanley Black & Decker, Böllhoff Group, Arconic Fastening Systems, PennEngineering, and Würth Group.