- Metalworking & Fabrication

- Miter Saw Market

Miter Saw Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Miter Saw Market by Product Type (Sliding, Compound, Others), Application (Residential, Commercial, Industrial), Power Source (Electric, Battery-Powered), and Regional Analysis for 2026-2033

Miter Saw Market Share and Trends Analysis

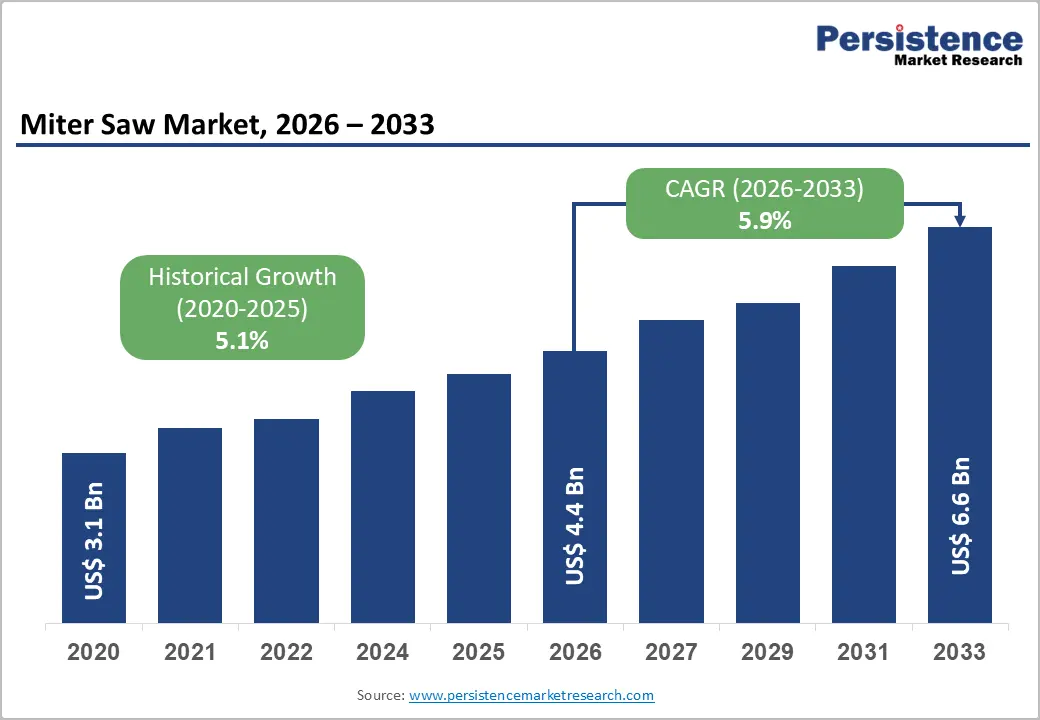

The global miter saw market size is likely to be valued at US$ 4.4 billion in 2026, and is projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period 2026−2033. This robust expansion is underpinned by accelerating residential construction activity, the broad adoption of cordless power tool platforms, and sustained capital investment in professional woodworking and fabrication facilities. Rising contractor productivity requirements, combined with stricter jobsite safety regulations and ergonomic standards, continue to elevate the replacement cycle and drive premiumization across product categories.

Key Industry Highlights

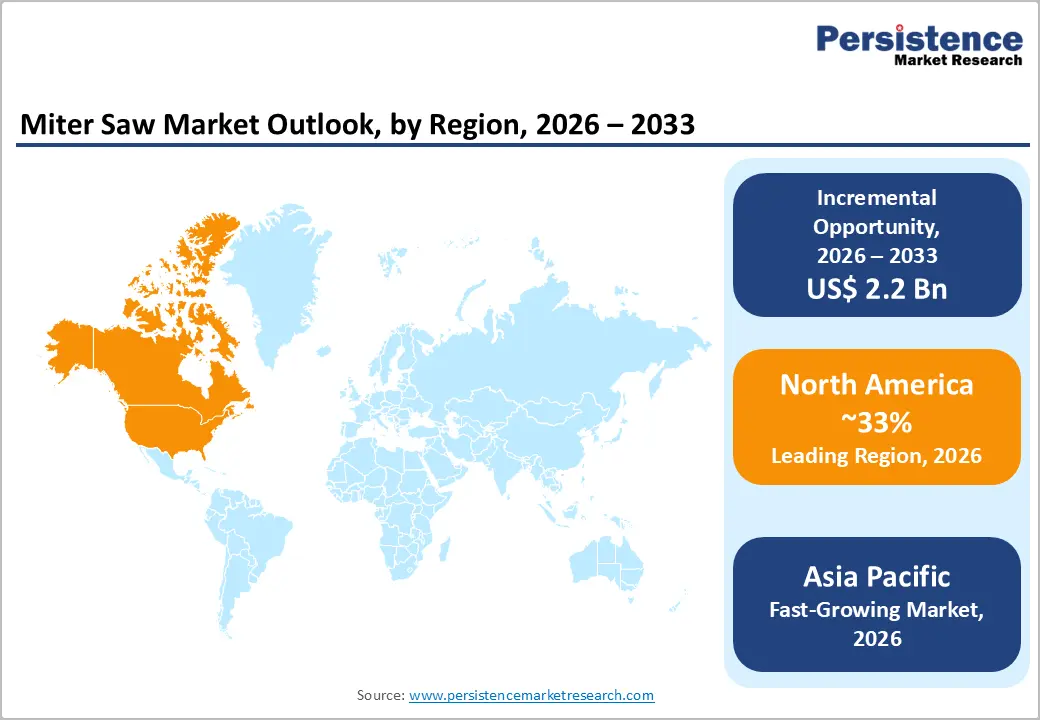

- Dominant Region: North America is expected to command about 33% market share in 2026, supported by strong construction momentum, especially in residential projects

- Fastest-growing Region: The Asia Pacific market is poised to be the fastest-growing during the 2026-2033 forecast period, due to the fast urbanization and massive infrastructure projects.

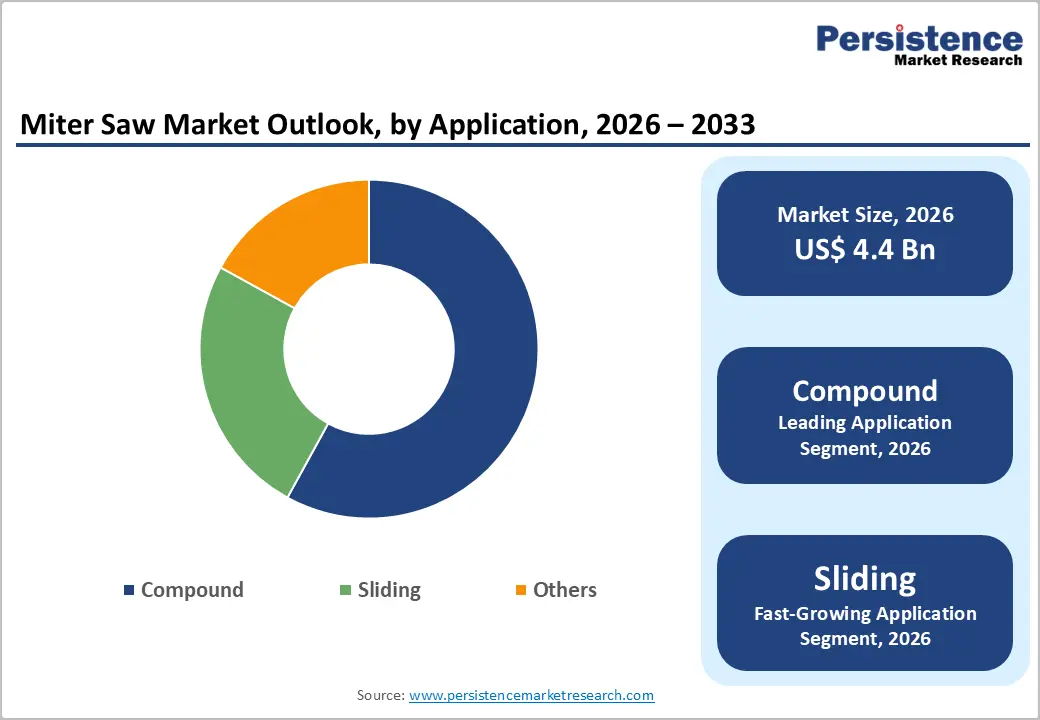

- Leading & Fastest-growing Product Type: Compound is set to lead by holding approximately 58% revenue share in 2026, while sliding is likely to be the fastest-growing segment through 2033.

- Leading & Fastest-growing Application: Residential applications are expected to capture an estimated 48% revenue share in 2026, whereas industrial applications are slated to be the fastest-growing over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Miter Saw Market Size (2026E) | US$ 4.4 Bn |

| Market Value Forecast (2033F) | US$ 6.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

DRO Analysis

Advancements in Precision and Efficiency Technologies

Innovations in miter saw technology drive market growth by improving precision, efficiency, and user satisfaction. Manufacturers integrate features such as laser guides and digital displays to help operators align cuts with exactness. These tools reduce errors during complex angles and bevels, which supports both professional workshops and home projects. Blade designs evolve with sharper edges and durable materials, so users complete tasks faster while minimizing material waste. Operators gain confidence as these enhancements simplify workflows and deliver consistent results across various wood types.

Motor upgrades and dust collection systems further elevate performance and safety standards. Powerful brushless motors provide sustained torque for heavy-duty applications, which prevents overheating during prolonged use. Advanced extraction mechanisms capture debris at the source, so workspaces remain clean and visibility stays clear. This setup protects users from health risks associated with fine particles and extends tool longevity through reduced maintenance needs. Professionals and hobbyists embrace these developments, as they align with demands for versatile, reliable equipment. Overall, such progress positions miter saws as indispensable assets, ready to meet future industry challenges with smarter, safer designs.

Technological Advancement and Cordless Platform Adoption

High-capacity lithium-ion battery systems transform purchase choices in the miter saw market. Platforms such as 20 Volts Maximum (20V MAX), 60 Volts FlexVolt, and 18 Volts/54 Volts FLEXVOLT deliver reliable power for extended runtime. Contractors prefer these cordless options for their portability on job sites. Brushless motors outperform traditional brushed versions by maintaining consistent speed under load. Digital controllers adjust torque in real time, which ensures smooth cuts through tough materials. Users benefit from reduced downtime as batteries swap quickly between tools in a shared ecosystem.

Manufacturers embed smart features to elevate premium models above basic units. Bluetooth connectivity links blade guards to mobile apps for performance monitoring. Electronic brakes stop the blade instantly after each cut, which enhances operator control and safety. Internet of Things (IoT) tracking helps fleet managers locate assets and schedule maintenance. Rental companies adopt these upgrades to minimize losses and extend equipment life. Professionals accelerate tool replacements as older models lag behind these capabilities. This shift creates demand for interconnected systems that streamline workflows and boost productivity across construction teams.

Occupational Safety Regulations and Liability Exposure

Stricter occupational health and safety rules in North America and Europe raise compliance demands on manufacturers and users alike. The Occupational Safety and Health Administration (OSHA) enforces limits on silica dust exposure for tools that cut masonry or composite materials. Miter saws must integrate dust-collection systems to meet these standards. Makers add guard mechanisms and electronic safety interlocks to align with European Union (EU) Machinery Directive updates under Conformance Europe (CE) marking. These requirements ensure operators avoid respiratory risks and accidental injuries during daily operations.

Compliance efforts create challenges for smaller producers and cost-conscious buyers. Regional manufacturers face higher production expenses, which limit their ability to compete with established brands. End users encounter elevated ownership costs, as basic models require costly upgrades or replacements. Budget-driven segments, such as small contractors and rental fleets, hesitate to invest in advanced units. This dynamic favors premium suppliers who bundle safety features as selling points. Large firms gain market share by offering reliable, regulation-ready tools that reduce long-term liabilities. Overall, these pressures reshape the industry toward innovation in durable safety designs, even as they slow adoption in price-sensitive areas.

Elevated Raw Material and Supply Chain Costs

Miter saw producers encounter ongoing cost challenges from fluctuating prices of key materials. Steel and aluminum alloy values shift unpredictably, which squeezes profit margins for mid-level Original Equipment Manufacturers (OEMs) without fixed supply agreements. Rare-earth magnets, essential for high-performance motors, also face supply inconsistencies due to global demand. Brushless motor controllers and electronic brake components suffer delays from semiconductor constraints. These factors extend production timelines and force makers to seek alternative sourcing options.

Logistics expenses stay above normal levels after recent global disruptions, even as conditions improve. Companies pass these burdens to buyers through higher retail prices, which erodes their edge in price-driven regions. Emerging markets demand affordable tools, so global brands struggle to penetrate without local assembly. Mid-tier firms cut features to maintain volumes, while leaders secure long-term contracts to stabilize costs. This environment pushes the industry toward vertical integration and regional partnerships. Manufacturers who diversify suppliers and optimize designs will navigate these pressures, preserving competitiveness amid volatile inputs and transport realities.

Growth in Smart & Connected Tools

The growing use of smart and connected tools, which fit with Industry 4.0 concepts. IoT allows these saws to gather and process data instantly. Users access real-time details on performance, operation habits, and safety measures. This setup supports predictive maintenance, so teams fix issues before breakdowns occur. Remote oversight lets managers track tools across job sites, which cuts idle time and sharpens cutting workflows for better results. Contractors integrate these systems into daily routines, gaining actionable insights that prevent unexpected failures. Smart functions transform routine tasks into efficient processes. Automated blade calibration adjusts settings without manual input, which ensures precise angles every time.

Remote diagnostics identify problems via apps, so technicians resolve faults off-site and save travel costs. Operators gain productivity as these tools integrate with digital platforms for seamless data sharing. End users, from contractors to workshops, lower expenses through less downtime and longer equipment life. Manufacturers position these innovations as key differentiators, drawing professionals who value reliability and data-driven decisions. Workshops adopt connected units to optimize schedules and reduce waste from poor maintenance. Overall, connected miter saws evolve into strategic assets that boost output, enhance safety, and adapt to modern construction demands across professional and industrial settings.

Precision Automation and CNC Integration

Digital stop systems, laser-guided alignment, and programmable computer numerical control (CNC) interfaces open new possibilities in high-value woodworking and millwork production. Manufacturers target these tools at cabinet shops, stair builders, and architectural millwork firms. Advanced CNC miter saws deliver repeatable precision for intricate designs, which reduces setup times between jobs. Operators align cuts effortlessly with laser markers, while digital stops lock angles instantly for consistent output. Fabricators gain speed as these features handle complex profiles that manual methods struggle to achieve. This technology suits mid-sized operations that seek professional-grade results without large crews.

Software enhancements simplify programming for everyday users, so shops integrate saws into broader production flows. Digital platforms link diagnostics to management systems, which enables real-time adjustments and predictive upkeep. Original equipment manufacturers (OEMs) create connected ecosystems that track performance across machines. This approach builds ongoing revenue through software-as-a-service (SaaS) subscriptions for updates and analytics. Companies strengthen their position by offering seamless integration that locks in customers. Mid-tier fabricators adopt these solutions to compete with bigger players, as intuitive controls lower training needs. Overall, such innovations transform miter saws into smart production hubs, driving efficiency and customization in premium woodworking sectors.

Category-wise Analysis

Product Type Insights

Compound is anticipated to command approximately 58% of the miter saw market revenue share in 2026. Their unique ability to perform miter and bevel cuts at the same time makes them the top choice for professionals. Carpenters, trim installers, and finish contractors rely on these tools for daily tasks such as framing, crown molding, and custom woodwork. Operators rotate the table for precise angle adjustments and tilt the head for bevels, which saves time on complex jobs. This versatility handles intricate projects that basic saws cannot match, so teams complete work faster with fewer errors. Contractors prefer these models for their balance of power and portability on active sites.

Sliding is likely to be the fastest-growing segment during the 2026-2033 forecast period. The sliding rail mechanism extends the cutting range to handle wide boards, which suits demanding applications in modern workshops. Users process larger materials without sacrificing bench space, unlike bulkier panel saws. This design combines miter, bevel, and slide functions into one unit, so operators tackle diverse projects with a single tool. Prefabricated construction teams adopt them for rapid framing and assembly lines. Architects and furniture makers value the precision for custom elements such as baseboards and panels. Growth accelerates as these saws integrate with production workflows that prioritize speed and accuracy.

Application Insights

Residential applications are likely to dominate in 2026, securing around 48% of the miter saw market share, owing to strong demand from framing, trim carpentry, flooring installation, and cabinetry tasks. Home builders use miter saws for precise angular cuts on studs and joists, which ensures tight joints in new constructions. Trim specialists create flawless miters for crown molding and baseboards, elevating room finishes. Flooring crews achieve perfect bevels for transitions and thresholds that blend seamlessly with existing surfaces. Cabinet makers produce accurate face frames and shelves, where exact angles prevent gaps in assemblies. These applications dominate residential markets as homeowners renovate kitchens and expand living spaces.

Industrial is expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by adoption in furniture manufacturing, flooring production, window and door fabrication, and architectural millwork. Increasing automation in mid-size woodworking facilities and the shift toward lean manufacturing principles minimizing waste through precision cutting are key demand drivers. The adoption of CNC-integrated miter cutting stations in production environments is upgrading average selling prices and driving volume among OEM equipment suppliers. Regulatory mandates on production safety and dust control further incentivize investment in premium, compliant equipment.

Regional Insights

North America Miter Saw Market Trends

North America is set to claim roughly 33% of the miter saw market value in 2026, fueled by strong construction momentum, especially in residential projects. Builders maintain steady activity across single-family homes and multi-unit developments, which creates consistent demand for reliable cutting tools. Professionals use these saws for framing, trim installation, and finish work, ensuring projects meet tight schedules and quality expectations. Home renovation trends amplify this need, as homeowners upgrade kitchens, bathrooms, and outdoor spaces with custom wood elements. The United States drives the bulk of this regional strength through its vibrant construction sector and widespread woodworking applications.

Contractors favor miter saws for their precision in angular cuts, which supports everything from roof rafters to decorative moldings. Technological upgrades, such as laser guides and cordless power, enhance performance on job sites. Major manufacturers maintain headquarters, factories, and distribution centers here, which speeds up product availability and innovation cycles. Retail chains stock diverse models for professionals and hobbyists alike. Rental services provide access to premium units without large investments. This combination of active building, advanced features, and established infrastructure positions North America for ongoing market influence. Local regulations encourage safe, efficient tools that align with industry standards, further solidifying the region's role.

Europe Miter Saw Market Trends

Europe is poised to emerge as a vital regional market for miter saws, powered by consistent expansion in renovation and remodeling projects. Homeowners and businesses refresh older structures, which generates steady needs for precision cutting tools. Workers handle tasks such as updating kitchens, installing new flooring, and modernizing commercial interiors with custom wood features. Builders prioritize miter saws for their ability to create clean angles that enhance overall finish quality. This focus on upgrades sustains demand across urban centers and suburban areas, where property values depend on professional craftsmanship.

Germany, the United Kingdom, and France lead demand within Europe due to their deep-rooted woodworking traditions and strict quality requirements. German manufacturers and carpenters rely on these tools for high-precision millwork in furniture and cabinetry production. U.K. renovators use them for trim and stair installations that match historic building styles. French artisans apply miter saws in architectural details and interior fit-outs, ensuring seamless integration with existing designs. Established trade practices emphasize durable, accurate equipment that meets EU safety norms. Local distributors stock advanced models with dust extraction and ergonomic designs. Renovation incentives from governments encourage investments in reliable tools.

Asia Pacific Miter Saw Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing miter saw market, driven by fast urbanization and massive infrastructure projects. Cities expand at a rapid pace, which spurs construction of housing complexes, roads, and public facilities. Developers rely on these tools for framing large structures and installing structural beams with exact angles. Governments invest heavily in transportation networks and smart city initiatives, creating ongoing needs for efficient cutting equipment on job sites. Workers process timber and engineered materials to meet ambitious timelines in high-density urban zones. Homeowners embrace do-it-yourself culture for personal projects, from building decks to crafting furniture.

The emerging economies of China, India, and ASEAN fuel this growth through rising disposable incomes and shifting consumer habits. Local builders upgrade workshops with versatile miter saws to handle diverse tasks such as trim work and cabinet assembly. Manufacturers establish factories in the region to serve growing demand with affordable, durable models. Retail outlets stock cordless and compact units that suit both professionals and hobbyists. Infrastructure booms generate bulk orders for heavy-duty saws, while residential trends boost entry-level sales. This combination of large-scale development and grassroots adoption positions the Asia Pacific for explosive expansion.

Competitive Landscape

The global miter saw market structure is moderately consolidated, dominated by leading players such as DeWalt, Bosch, Makita, Milwaukee Tool, and Metabo HPT. These players collectively capture 58-63% of the market share. Regional specialists, private-label distributors, and Chinese OEM brands dominate the remaining market share in a fragmented landscape. Competition intensifies around battery platform compatibility, advanced blade designs, effective dust management systems, and digital connectivity options.

Asian manufacturers ramp up pricing pressure in entry-level and mid-range categories, forcing global players to sharpen cost structures. Buyers weigh ecosystem integration against affordability, which accelerates consolidation among premium brands. This dynamic pushes innovation in value-added features while challenging smaller entrants to differentiate through niche specialization or localized production.

Key Industry Developments

- In November 2025, Makita launched the LS1110F 10-inch slide compound miter saw, featuring a compact, lightweight design with a 13-amp direct-drive motor delivering up to 4,500 rpm for precision cutting. Designed for construction and woodworking professionals, the saw offers enhanced cutting capacity, multiple miter/bevel angles, and improved portability, positioning it as a versatile, cost-efficient solution for jobsite applications.

- In April 2025, DEWALT unveiled the 20V MAX XR 12-inch double bevel sliding miter saw (DCS785), setting a new benchmark in cordless cut capacity within its lineup. The tool delivers high productivity with regenerative braking for improved runtime, up to 371 cuts per charge, advanced dust capture (~97%), and full compatibility with 20V MAX and FLEXVOLT battery systems.

Companies Covered in Miter Saw Market

- DeWalt

- Bosch Power Tools

- Makita Corporation

- Milwaukee Tool

- Metabo HPT

- Festool GmbH

- RIDGID

- Ryobi

- Craftsman

- Evolution Power Tools

- SKIL

- Rexon Industrial Corp.

- TECCPO

- WEN Products

- Grizzly Industrial

Frequently Asked Questions

The global miter saw market is projected to reach US$ 4.4 billion in 2026.

The market is being driven by technological upgrades in cordless power, and smart features oriented towards enhancing efficiency.

The market is poised to witness a CAGR of 5.9% from 2026 to 2033.

Major opportunities lie in the burgeoning economies of Asia Pacific that offer growth through urbanization and manufacturing hubs.

DeWalt, Bosch, Makita, Milwaukee Tool, and Metabo HPT are some of the key players in the market.