- Medical Devices

- Medical Gloves Market

Medical Gloves Market Size, Share, and Growth Forecast 2026 – 2033

Medical Gloves Market by Product (Examination Gloves, Surgical Gloves, Disposable Gloves, Reusable Gloves), Material (Latex Gloves, Nitrile Gloves, Vinyl Gloves, Neoprene Gloves, Others), End-user (Hospitals, Clinics, Diagnostic Centers, Others), and Regional Analysis, 2026–2033

Medical Gloves Market Share and Trends Analysis

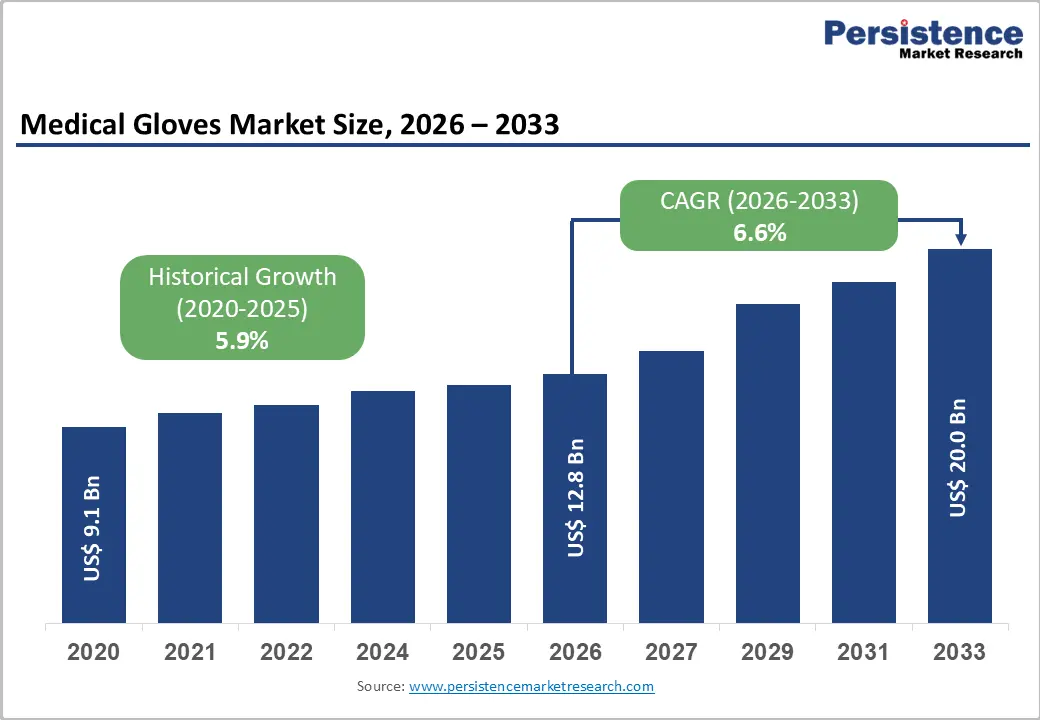

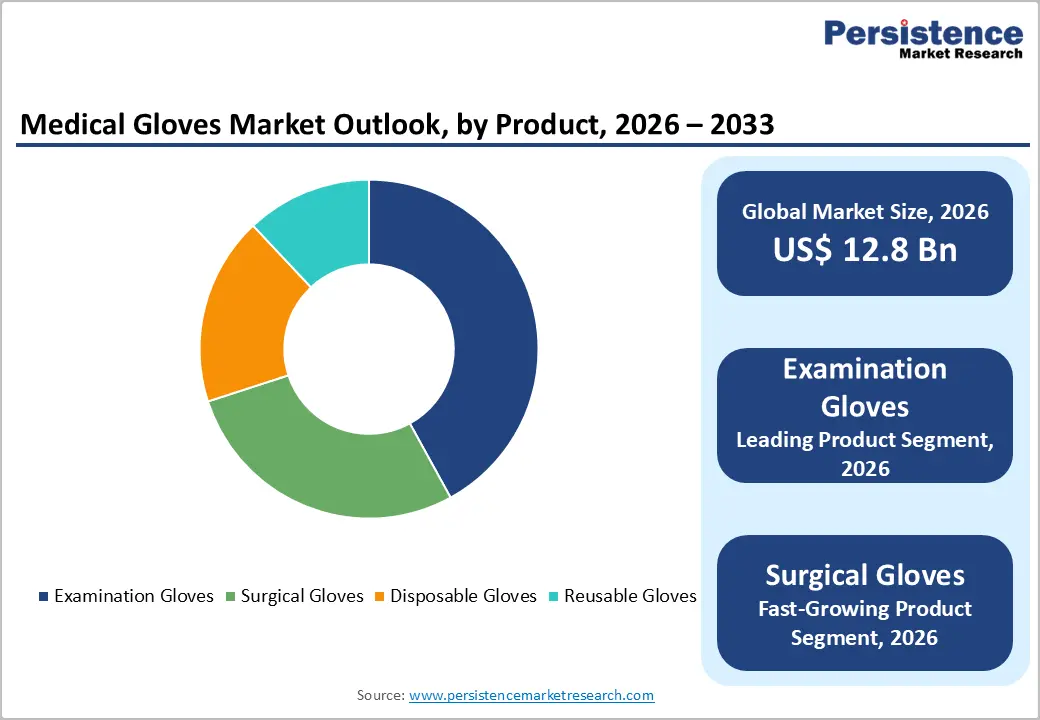

The global Medical Gloves market size is expected to be valued at US$ 12.8 billion in 2026 and projected to reach US$ 20.0 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

It is primarily driven by the continued reinforcement of infection prevention protocols across global healthcare systems, the accelerating expansion of healthcare infrastructure in emerging economies, and heightened regulatory mandates on personal protective equipment (PPE) compliance. The lasting behavioral and institutional shift toward stricter hand hygiene and barrier protection practices, catalyzed by the COVID-19 pandemic and endorsed by institutions including the World Health Organization (WHO) and the U.S. Centers for Disease Control and Prevention (CDC), continues to underpin demand for medical gloves well beyond the post-pandemic normalization period. Rising surgical procedure volumes, growing prevalence of chronic disease, and expanding outpatient care settings collectively drive consumption across all glove categories.

Key Industry Highlights

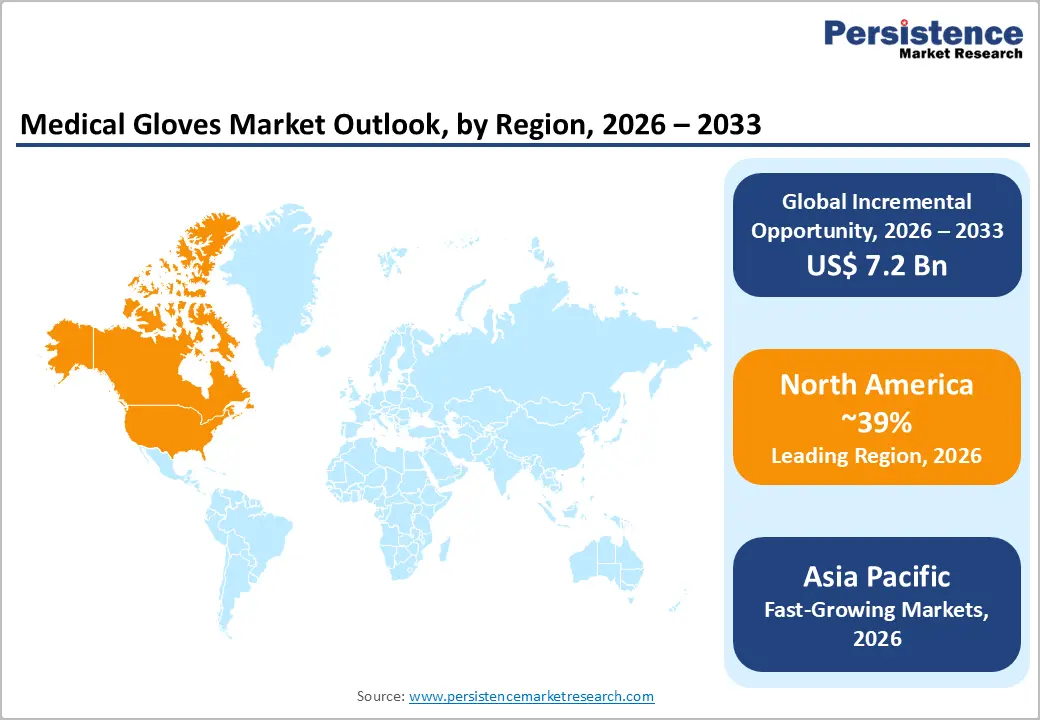

- Leading Region: North America dominated the Medical Gloves market in 2025 with approximately 39% revenue share, driven by stringent FDA and OSHA PPE mandates, high per-capita healthcare spending, and robust institutional procurement across 6,000+ U.S. hospitals.

- Fast-Growing Market: Asia Pacific is the fast-growing regional market for medical gloves, underpinned by China's Healthy China 2030 initiative, India's Ayushman Bharat program, and rapid hospital infrastructure expansion across Southeast Asia through the 2026–2033 forecast period.

- Dominant Product Segment: Examination gloves lead the product category with approximately 42% market share in 2025, driven by high-frequency usage across routine patient care activities and CDC Standard Precautions mandating glove use for all potential blood and body fluid contact scenarios.

- Fast-Growing Product Segment: Surgical gloves are the fast-growing product segment supported by rising global surgical volumes, WHO double-gloving recommendations for high-risk procedures, and innovation in powder-free, indicator, and antimicrobial glove technologies.

Market Dynamics

Drivers - Stringent Infection Control Regulations and Elevated Healthcare Safety Standards

The global emphasis on healthcare-associated infection (HAI) prevention continues to be a primary structural driver for medical glove consumption. According to the WHO, HAIs affect approximately 1 in 10 patients in low- and middle-income countries, with medical gloves constituting a frontline defense within the WHO's Five Moments for Hand Hygiene framework.

Regulatory bodies, including the U.S. Food and Drug Administration (FDA) and the European Commission under the EU Medical Device Regulation (MDR 2017/745), have tightened quality and performance standards for medical gloves, compelling healthcare facilities to procure certified, compliant products. This regulatory environment creates a durable institutional pull that sustains glove demand across hospitals, surgical centers, and outpatient clinics, driving consistent volume growth independent of broader macroeconomic cycles.

Rising Surgical Volumes and Expanding Global Healthcare Infrastructure

The global increase in surgical procedure volumes is a direct and measurable demand driver for surgical and examination gloves. The Lancet Commission on Global Surgery estimated that over 313 million surgical procedures are performed annually worldwide, with a growing unmet need of an additional 143 million procedures required in low- and middle-income countries. Governments across the Asia Pacific, Latin America, and Sub-Saharan Africa are making substantial investments in hospital bed capacity and surgical workforce training under initiatives such as India's Ayushman Bharat program and China's Healthy China 2030 plan. Each surgical procedure generates multiple pairs of glove consumption, making this a highly correlated demand variable that structurally expands the total addressable market for medical gloves through the forecast period.

Restraints - Raw Material Price Volatility and Supply Chain Concentration Risk

The medical gloves market faces persistent exposure to fluctuations in natural rubber latex and nitrile butadiene rubber (NBR) prices, both of which are subject to commodity market dynamics. Malaysia and Thailand collectively account for over 70% of the global natural rubber supply according to the International Rubber Study Group (IRSG), creating significant geographic concentration risk. Disruptions, whether from disease outbreaks affecting rubber plantations, geopolitical events, or logistics constraints, can sharply compress manufacturer margins and trigger supply shortfalls. The COVID-19 pandemic exposed the fragility of this concentrated supply chain when global glove demand surged by an estimated 40% within a single year, overwhelming production capacity and causing price spikes of over 300% for nitrile gloves at peak demand.

Latex Allergy Concerns and Regulatory Restrictions on Powdered Gloves

The well-documented prevalence of Type I latex hypersensitivity affecting an estimated 1–6% of the general population and up to 12–17% of healthcare workers according to the American College of Allergy, Asthma & Immunology (ACAAI) continues to constrain growth in the natural rubber latex glove segment. Regulatory actions such as the FDA's 2016 ban on powdered surgical and examination gloves in the United States have effectively eliminated a product subcategory while generating transition costs for manufacturers and procurement teams. These restrictions, increasingly mirrored by regulatory bodies in the EU and Japan, redirect demand toward synthetic alternatives but impose reformulation and re-certification burdens on glove manufacturers.

Opportunities - Accelerating Adoption of Nitrile and Synthetic Gloves Amid Latex Substitution

The structural shift away from natural rubber latex toward synthetic nitrile gloves presents a significant and durable opportunity for manufacturers with established nitrile production capacity. Nitrile gloves now account for the majority of new procurement contracts across major healthcare systems globally, driven by superior chemical resistance, consistent quality, and the absence of latex allergy risk. Top Glove Corporation and Hartalega Holdings Berhad have each invested hundreds of millions in high-speed automated nitrile production lines capable of producing over 30 billion gloves annually. As healthcare facilities in Africa, Southeast Asia, and Latin America upgrade their PPE procurement standards, the transition to nitrile represents a high-growth commercial opportunity. Furthermore, innovations in thinner, high-barrier nitrile formulations are expanding applications into previously latex-dominant clinical categories, broadening the addressable market.

Surgical Gloves Innovation and Growth in Emerging Market Healthcare Spending

The surgical gloves segment is the fast-growing product category in the medical gloves market, creating a meaningful commercial opportunity for manufacturers that invest in advanced glove technologies. Innovations, including powder-free, micro-textured formulations, double-gloving indicator systems, and antimicrobial-coated surgical gloves, are generating premium pricing power and clinical endorsement. The Association of PeriOperative Registered Nurses (AORN) and WHO Surgical Safety Guidelines explicitly recommend double gloving for high-risk procedures, structurally increasing glove consumption per procedure. Concurrently, healthcare expenditure in the Asia Pacific is projected to reach US$ 4.9 trillion by 2030, according to the Asian Development Bank (ADB), with surgical capacity expansion directly translating into sustained surgical glove demand. Companies that localize manufacturing in high-growth markets stand to benefit from cost and supply chain advantages.

Category-wise Analysis

Product Insights

The Examination Gloves segment dominates the Medical Gloves market by product type, accounting for approximately 42% of total product revenue in 2025. This leadership is attributable to the high frequency of examination glove usage across a broad spectrum of clinical activities, from routine physical examinations and blood draws to wound care and non-surgical procedures, compared to the more occasion-specific use of surgical gloves. The CDC's Standard Precautions guidelines mandate the use of examination gloves for any patient contact involving potential exposure to blood, body fluids, or mucous membranes, driving consistent high-volume procurement across all healthcare settings. The growing expansion of outpatient clinics, primary care facilities, and diagnostic centers globally further amplifies examination glove volumes, reinforcing this segment's market leadership throughout the forecast period.

Material Insights

The nitrile gloves segment leads the medical gloves market by material, capturing approximately 46% of material-based market revenue in 2025. Nitrile's dominance stems from its superior combination of puncture resistance, chemical barrier properties, allergy-free composition, and consistent manufacturing quality compared to natural rubber latex. The FDA's 2016 prohibition of powdered latex gloves accelerated institutional switching toward nitrile across U.S. hospitals, a trend widely replicated in the EU, Australia, and Japan. Leading manufacturers, including Hartalega Holdings Berhad, whose NEXT Generation glove plants achieve production efficiencies exceeding 45,000 gloves per hour per line and Ansell Limited, have invested heavily in nitrile capacity, consolidating their material leadership and enabling competitive pricing that further drives adoption across diverse end-user segments.

End-user Insights

The hospitals segment dominates the end-user landscape of the Medical Gloves market, representing approximately 52% of total end-user demand in 2025. Hospitals are the largest single consumers of medical gloves due to the sheer breadth and volume of clinical activities performed within their facilities, encompassing emergency care, intensive care, surgical theatres, diagnostic laboratories, and general wards. A mid-size hospital with 300–500 beds can consume several hundred thousand pairs of gloves per month. The American Hospital Association (AHA) reports over 6,000 registered hospitals in the U.S. alone, representing concentrated institutional procurement. Global hospital capacity expansions particularly across China, India, and Brazil, are systematically scaling institutional glove demand, cementing hospitals as the dominant and fastest-volume end-user segment through 2033.

Regional Insights

North America Medical Gloves Market Trends and Insights

North America leads the global Medical Gloves market, holding approximately 39% of total revenue in 2025. The region's dominance is underpinned by stringent FDA and OSHA regulatory mandates on PPE usage, high per-capita healthcare expenditure, and well-established hospital procurement frameworks. The sustained post-pandemic reinforcement of infection control protocols and growing outpatient surgical volumes continue to generate consistent institutional demand across the region.

U.S. Medical Gloves Market Size

The U.S. accounts for approximately 88% of North America's medical gloves market. With over 36 million inpatient hospital stays annually (American Hospital Association) and a robust ambulatory surgery network, the U.S. generates the world's highest per-facility glove consumption volumes. The FDA's regulatory framework and CMS reimbursement policies for infection prevention practices structurally sustain procurement demand.

Europe Medical Gloves Market Trends and Insights

Europe is the second-largest regional market for medical gloves, supported by harmonized standards under the EU Medical Device Regulation (MDR) and EN 455 glove quality standards. The region's aging population is driving rising volumes of surgical procedures and chronic disease management, sustaining demand. National health services in Germany, France, and the U.K. maintain large centralized procurement programs that provide stable, predictable glove purchasing volumes.

Germany Medical Gloves Market Size

Germany accounts for approximately 21% of European medical gloves revenue, driven by one of Europe's largest hospital networks with over 1,900 hospitals and a strong statutory health insurance (GKV) framework that standardizes PPE procurement. Germany's high surgical procedure volumes and active implementation of the Robert Koch Institute (RKI) infection control guidelines ensure consistent, large-scale glove demand.

U.K. Medical Gloves Market Size

The U.K. represents approximately 18% of the European market revenue. The National Health Service (NHS) is one of the world's largest centralized glove procurement bodies, sourcing through NHS Supply Chain. Post-Brexit, the U.K. has accelerated development of domestic PPE supply chains following the vulnerabilities exposed during the COVID-19 pandemic, with the U.K. The Health Security Agency (UKHSA) is establishing strategic PPE stockpiling protocols.

France Medical Gloves Market Size

France contributes approximately 15% of Europe's medical gloves market revenue. The French Ministry of Health and Santé Publique France govern hospital infection control procurement, ensuring compliant glove standards across the 3,000+ public and private hospitals in the country. France's investment in surgical capacity modernization and its aging population profile sustain structural growth in glove consumption.

Asia Pacific Medical Gloves Market Trends and Insights

Asia Pacific is the fast-growing regional market for medical gloves and is expected to register the highest CAGR during the forecast period. The region is anchored by China, which is simultaneously the world's largest consumer and a growing producer of medical gloves, driven by its Healthy China 2030 initiative and rapidly expanding hospital network. Malaysia and Thailand dominate regional glove manufacturing supply, while India, Japan, South Korea, and Southeast Asia are rapidly scaling domestic demand alongside healthcare infrastructure investments.

India Medical Gloves Market Size

India is among the fast-growing markets in the Asia Pacific, estimated to hold approximately 12% of regional revenue in 2026. Ayushman Bharat has expanded healthcare coverage to over 500 million beneficiaries, driving hospital utilization and glove consumption. India's domestic manufacturers, including Ansell's local supply network and emerging domestic producers, are scaling production to meet growing clinical demand.

Competitive Landscape

The medical gloves market is highly competitive, driven by rising healthcare demand, strict infection control standards, and increasing awareness of personal safety. Manufacturers focus on product quality, durability, comfort, and allergy-free materials such as nitrile and neoprene to strengthen market presence. Continuous investment in automation and large-scale production helps improve supply efficiency and reduce costs. Sustainability is also becoming a major focus, with growing demand for biodegradable and eco-friendly glove options.

Key Developments:

- In April 2026, the Japanese government announced the release of 50 million medical gloves from its national stockpile to healthcare institutions facing supply shortages. The move was taken to ease concerns over disrupted medical supply chains caused by the Middle East crisis and rising shortages of petroleum-based raw materials such as naphtha, which is essential for glove production.

- In April 2025, INTCO Medical unveiled its new Syntex™ synthetic disposable latex gloves, offering advanced performance that surpasses traditional natural latex gloves.

- In January 2024, Kimberly-Clark introduced its latest Kimtech Polaris nitrile exam gloves, specifically designed for laboratory use. These new gloves offer enhanced durability, improved comfort, and superior protection.

Global Medical Gloves Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 9.1 Billion |

|

Current Market Value (2026) |

US$ 12.8 Billion |

|

Projected Market Value (2033) |

US$ 20.0 Billion |

|

CAGR (2026–2033) |

6.6% |

|

Leading Region |

North America, 39% market share (2025) |

|

Dominant Category (Product) |

Examination Gloves, ~42% market share (2025) |

|

Top-ranking Material |

Nitrile Gloves, ~46% market share (2025) |

|

Incremental Opportunity |

US$ 7.2 Billion (2026–2033) |

Companies Covered in Medical Gloves Market

- Top Glove Corporation

- Hartalega Holdings Berhad

- Ansell Limited

- Kossan Rubber Industries Bhd

- Supermax Corporation Berhad

- Semperit AG Holding

- Cardinal Health

- Medline Industries

- Mölnlycke Health Care

- B. Braun

- 3M

- Kimberly-Clark Corporation

- INTCO Medical

Frequently Asked Questions

The global medical gloves market size is estimated to be valued at US$ 12.8 billion in 2026.The global medical gloves market size is estimated to be valued at US$ 12.8 billion in 2026.

The primary demand drivers include stringent infection prevention mandates enforced by the WHO, CDC, FDA, and EU MDR; rising global surgical volumes driven by aging populations and expanding access to care; growing healthcare infrastructure in emerging markets; and the accelerating substitution of latex gloves with nitrile alternatives due to allergy concerns and performance advantages.

North America is the leading regional market, accounting for approximately 39% of global medical gloves revenue in 2026.

Two principal opportunities exist: (1) the ongoing latex-to-nitrile material substitution trend, which offers manufacturers with nitrile production scale significant revenue growth across all geographies; and (2) the Surgical Gloves segment, which is the fastest growing product category driven by rising surgical volumes estimated at 313 million+ procedures annually per the Lancet Commission on Global Surgery and premium innovation in double-gloving indicator and antimicrobial formulations.

The market is led by Malaysian manufacturing giants, including Top Glove Corporation (world's largest glove manufacturer), Hartalega Holdings Berhad, Kossan Rubber Industries Bhd, and Supermax Corporation Berhad. Western healthcare companies including Ansell Limited, Mölnlycke Health Care, 3M, Cardinal Health, and B. Braun.