- Medical Devices

- Intravenous Infusion Pumps Market

Intravenous Infusion Pumps Market Size, Share, and Growth Forecast, 2026 – 2033

Intravenous Infusion Pumps Market by Product Type (Volumetric Infusion Pumps, Syringe Infusion Pumps, Others), Application (Chemotherapy, Diabetes Management, Pain Management, Others), End-user (Hospitals, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis for 2026 - 2033

Intravenous Infusion Pumps Market Share and Trends Analysis

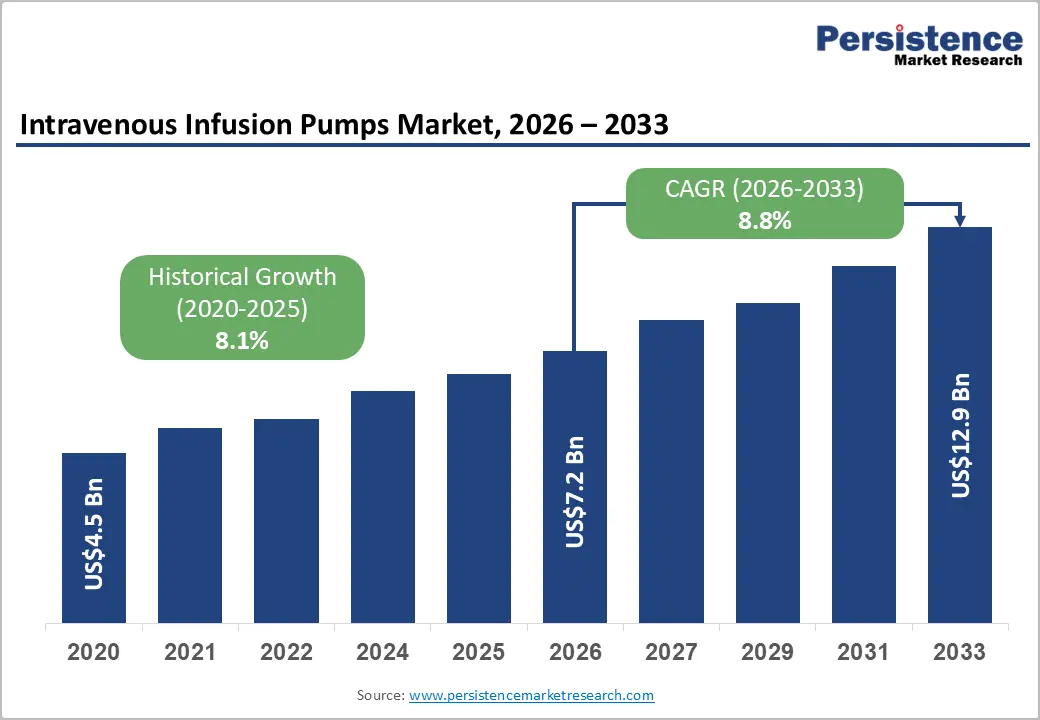

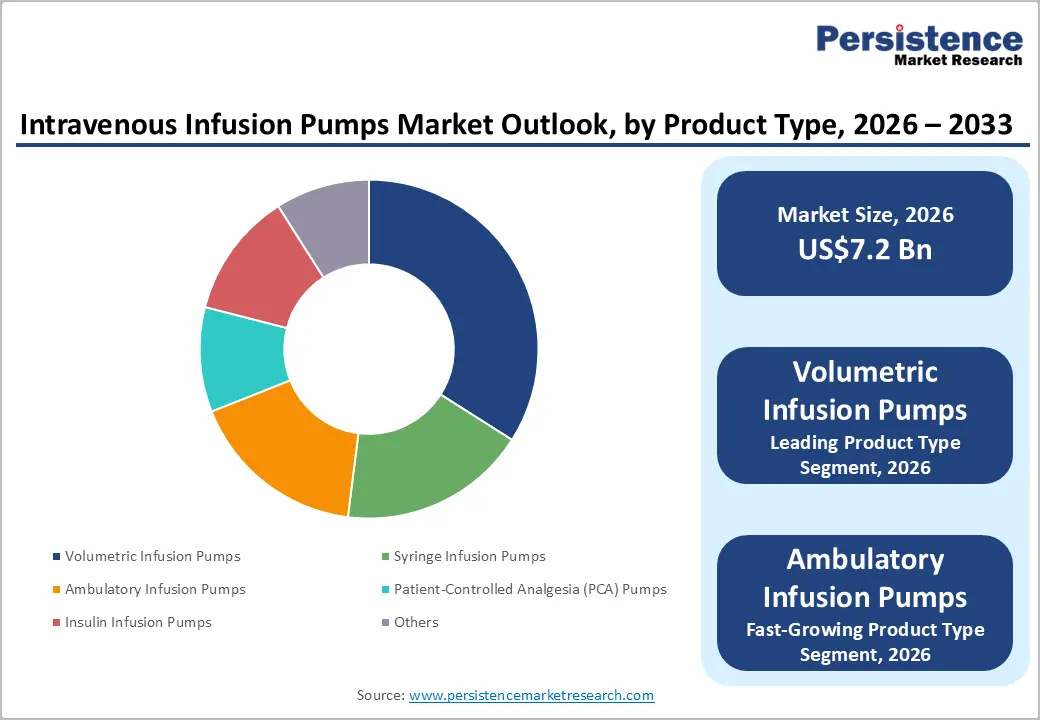

The global intravenous infusion pumps market size is likely to be valued at US$7.2 billion in 2026 and is estimated to reach US$12.9 billion by 2033, growing at a CAGR of 8.8% during the forecast period from 2026 to 2033, driven by rising chronic disease burden, expanding hospital automation, and increasing demand for precise medication delivery systems.

Growing adoption of smart infusion technologies is reshaping medication administration workflows across acute and homecare environments. Aging populations and increasing prevalence of oncology, diabetes, and cardiovascular conditions are accelerating dependence on controlled intravenous therapies.

Key Industry Highlights:

- Leading Product Type: Volumetric infusion pumps are set to hold around 34% revenue share in 2026, driven by increasing utilization within critical care and oncology treatment environments.

- Fastest-Growing Product Type: Ambulatory infusion pumps are projected as the fastest-growing segment, driven by the expansion of home healthcare and portable therapy administration demand.

- Leading Application: Critical care is estimated to hold roughly 31% revenue share in 2026, driven by rising intensive care admissions and demand for precise medication delivery systems.

- Fastest-growing Application: Diabetes management is forecast to record the fastest growth, driven by increasing adoption of connected insulin infusion technologies and chronic disease management programs.

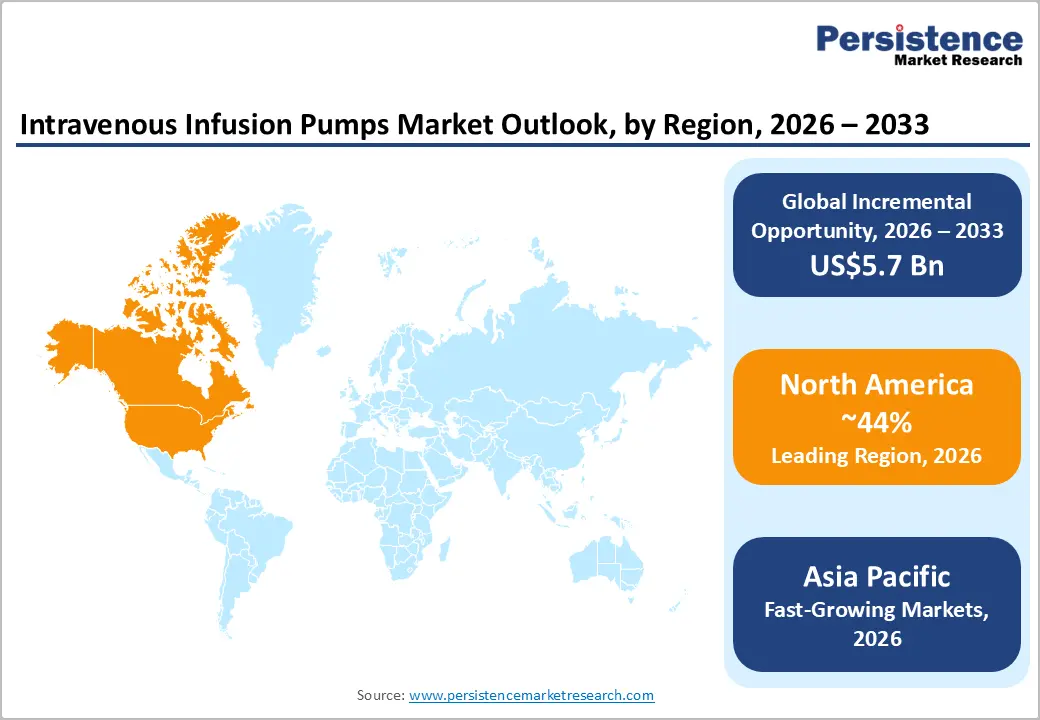

- Regional Leadership: North America is projected to capture roughly 44% of the market share by 2026, while Asia Pacific is also forecast to record the fastest growth due to expanding hospital construction.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Baxter International Inc. and Becton Dickinson and Company leveraging smart infusion ecosystems and interoperability capabilities to strengthen positioning.

DRO Analysis

Driver - Rising Chronic Disease Burden, Increasing Demand for Continuous Drug Delivery

The increasing prevalence of cancer, diabetes, gastrointestinal disorders, and cardiovascular conditions is generating sustained demand for continuous and controlled infusion therapy. Hospitals and specialty clinics are integrating programmable infusion systems to improve dosage precision and reduce manual administration errors. According to the U.S. Centers for Disease Control and Prevention (CDC), nearly 129 million people in the U.S. were living with at least one major chronic disease in 2025, creating long-term demand for infusion-based treatment infrastructure.

Growing utilization of chemotherapy, parenteral nutrition, insulin infusion, and pain management therapies is accelerating the procurement of volumetric and syringe infusion systems. Healthcare providers are prioritizing digital infusion platforms capable of supporting interoperability with electronic health record systems. Integration of smart drug libraries and automated alerts is improving medication safety while reducing adverse drug events in critical care settings. Expansion of chronic disease management programs across outpatient facilities is further strengthening utilization rates.

Restraint - High Device Acquisition and Maintenance Costs Limiting Scalability

Advanced smart infusion systems require substantial capital expenditure associated with software integration, cybersecurity infrastructure, and device calibration. Small healthcare facilities and resource-constrained hospitals face difficulty deploying interoperable infusion platforms at scale. Long replacement cycles are slowing recurring procurement opportunities and limiting rapid technology transition across mid-tier healthcare institutions.

Maintenance expenses linked to software upgrades, battery replacement, and regulatory validation are increasing operational costs for healthcare providers. Supply chain dependence on semiconductor components and precision sensors is creating pricing volatility. Margin pressure is increasing for manufacturers attempting to balance affordability with compliance-driven technology enhancements and cybersecurity investments.

Opportunity - Expansion of Home Healthcare Creating Demand for Portable Infusion Systems

Increasing preference for home-based treatment is creating growth opportunities for ambulatory and wearable infusion technologies. Healthcare systems are shifting non-critical infusion therapies toward outpatient environments to reduce hospitalization costs and improve patient convenience. Portable infusion systems capable of supporting chemotherapy, pain management, and insulin administration are gaining adoption across decentralized care settings.

Manufacturers are developing lightweight, battery-powered infusion platforms with remote monitoring capabilities to support long-duration therapy outside hospitals. Regulatory support for home healthcare reimbursement is strengthening commercialization pathways. Companies investing in compact wireless systems and cloud-connected monitoring tools are expected to strengthen penetration across aging populations requiring long-term therapy management.

Category-wise Analysis

Product Type Insights

Volumetric infusion pumps are anticipated to secure around 34% of the market share in 2026, reflecting widespread utilization across intensive care, oncology, and surgical procedures requiring controlled fluid administration. Hospitals are prioritizing programmable systems capable of delivering multiple therapies accurately. In 2025, ICU Medical Inc. expanded advanced volumetric infusion platforms supporting interoperability, strengthening adoption across high-acuity hospital environments.

Ambulatory infusion pumps are expected to be the fastest-growing segment, propelled by rising home healthcare utilization and increasing preference for portable therapy administration systems. Compact wireless devices are improving patient mobility during chemotherapy and pain management treatments. In 2026, Fresenius Kabi AG expanded ambulatory infusion offerings focused on outpatient therapy management, supporting broader deployment across decentralized care delivery settings.

Application Insights

Critical care is poised to dominate with a forecast market share of over 31% in 2026, powered by increasing intensive care admissions and demand for precise medication delivery during emergency interventions. Smart infusion systems are improving monitoring accuracy and reducing dosing complications. Baxter International Inc. introduced enhanced ICU-focused infusion software integration capabilities, strengthening adoption across digitally connected hospital environments.

Diabetes management is estimated to be the fastest-growing segment, fueled by increasing insulin-dependent patient populations and rising adoption of wearable infusion technologies supporting continuous insulin delivery. Portable smart pumps are improving therapy personalization and patient convenience significantly. Medtronic plc expanded connected insulin infusion solutions, integrating glucose monitoring analytics, accelerating technology penetration across chronic disease management programs.

End-user Insights

Hospitals are likely to be the leading segment with a projected 52% of the market share in 2026, due to high patient inflow, extensive surgical procedures, and continuous infusion therapy requirements across critical care departments. Large hospitals are prioritizing smart infusion interoperability investments. Becton Dickinson and Company strengthened enterprise infusion connectivity solutions supporting centralized medication management across hospital networks globally.

Home care settings are anticipated to be the fastest-growing segment, fueled by rising demand for outpatient treatment, aging populations, and increasing acceptance of remote patient monitoring technologies. Portable infusion systems are reducing hospitalization requirements for chronic therapies considerably. Moog Inc. expanded wearable infusion pump manufacturing capacity, supporting broader home-based infusion therapy deployment internationally across decentralized healthcare environments.

Regional Insights

North America Intravenous Infusion Pumps Market Trends

North America is expected to lead with an estimated 44% of the market share in 2026, supported by advanced healthcare networks, high healthcare expenditures, and early adoption of integrated technology. Hospital groups prioritize wireless fluid delivery systems to optimize safety protocols and comply with digital health mandates. The expansion of long-term care facilities increases demand for mobile medication delivery systems designed for outpatient environments.

U.S. Intravenous Infusion Pumps Market Insights

The U.S. market is projected to expand steadily, accounting for an estimated 84% of the North America regional market share in 2026, due to strict safety agency oversight. Hospital networks replace legacy systems with smart platforms equipped with advanced cybersecurity and electronic health record integration capabilities. Industry participants, including Becton, Dickinson and Company and Baxter International, leverage institutional supply contracts to maintain extensive hardware installation bases across domestic healthcare systems.

Canada Intravenous Infusion Pumps Market Insights

The Canada market is forecast to achieve consistent growth, capturing an estimated 11% of the regional market share in 2026, driven by provincial government investments. Public health authorities focus on optimizing clinical workflows by procuring unified medication delivery platforms that utilize standardized drug libraries. This process assists overstretched nursing teams while establishing long-term volume hardware procurement partnerships with global medical device manufacturers.

Europe Intravenous Infusion Pumps Market Trends

Europe is expected to secure a substantial market presence, accounting for an estimated 26% of the global market share in 2026 due to public healthcare systems and safety certification frameworks. European medical facilities emphasize the adoption of ecological hardware models that feature durable, reusable internal components to meet institutional sustainability targets.

Germany Intravenous Infusion Pumps Market Insights

The Germany market is expected to remain a primary regional revenue driver, securing an estimated 23% of the Europe regional market share in 2026, supported by specialized intensive care units. German hospital procurement strategies focus heavily on securing high-precision syringes and volumetric systems that integrate smoothly into data analysis architectures. Local entities, such as B. Braun Melsungen AG, utilize localized production advantages to supply custom hardware configurations across Central Europe.

U.K. Intravenous Infusion Pumps Market Insights

The U.K. market is likely to experience structured growth, capturing an estimated 18% of the Europe regional market share in 2026 as the public health sector executes procurement programs. Financial allocation strategies privilege hardware vendors that offer comprehensive maintenance contracts and long-term cost guarantees for essential administration consumables. This centralized purchasing methodology accelerates the elimination of non-connected legacy pumps, establishing a baseline requirement for network-linked systems.

Asia Pacific Intravenous Infusion Pumps Market Trends

Asia Pacific is forecast to be the fastest-growing market for intravenous infusion pumps, stimulated by public healthcare investments, rapid construction of hospital networks, and rising safety standards. Government health initiatives aim to improve critical care access within secondary cities, generating a great demand for medical equipment. Domestic manufacturing facilities lower baseline procurement costs, making advanced fluid delivery systems accessible to budget-conscious regional clinics.

China Intravenous Infusion Pumps Market Insights

The China market is projected to grow at a rapid rate, capturing an estimated 35% of the Asia Pacific regional market share in 2026, due to policy mandates that incentivize domestic production. Regional healthcare networks integrate automated fluid delivery systems into newly built emergency centers to manage escalating acute care patient volumes efficiently. Domestic participants, such as Shenzhen Mindray Bio-Medical Electronics, expand market share by offering cost-competitive, technologically advanced platforms tailored for rapid deployment.

Japan Intravenous Infusion Pumps Market Insights

The Japan market is expected to show steady progression, representing an estimated 22% of the Asia Pacific regional market share in 2026, driven by an urgent societal requirement to manage elderly demographics. The Ministry of Health, Labour and Welfare enforces strict safety verification protocols, forcing manufacturers to design mistake-proof user interfaces that minimize operational risks. This specialized regulatory environment accelerates the institutional deployment of advanced, wearable insulin and ambulatory analgesic delivery platforms.

Competitive Landscape

The global intravenous infusion pumps market is moderately fragmented, with distinct global participants competing alongside regional medical technology providers to secure institutional hospital contracts. Strategic positioning depends on holding proprietary compatibility rights for high-volume consumable administration sets, which ensures steady long-term post-hardware revenue streams.

Key industry participants shaping the global operational landscape include Becton, Dickinson and Company, Baxter International Inc., B. Braun Melsungen AG, ICU Medical, Inc., and Fresenius Kabi AG. These organizations maintain market leadership by leveraging global manufacturing footprints, extensive regulatory compliance portfolios, and capital resources dedicated to continuous software development.

Key Industry Developments:

- In October 2025, Becton Dickinson and Company launched the AI-enabled BD Incada Connected Care Platform, integrating infusion pump connectivity and analytics, reinforcing advancement in smart intravenous infusion management and hospital workflow optimization.

- In May 2025, Penlon launched a new infusion system range featuring advanced infusion and syringe pumps, reinforcing the expansion of smart intravenous infusion technologies focused on safer and more precise medication delivery.

- In April 2025, ICU Medical Inc. received U.S. FDA 510(k) clearance for Plum Solo and updated Plum Duo precision IV pumps, reinforcing advancement in smart intravenous infusion pump accuracy and connected medication delivery systems.

Companies Covered in Intravenous Infusion Pumps Market

- Becton, Dickinson and Company

- Baxter International Inc.

- B. Braun Melsungen AG

- ICU Medical, Inc.

- Fresenius Kabi AG

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Medtronic plc

- Insulet Corporation

- Smiths Medical (ICU Medical)

- Moog Inc.

- Avanos Medical, Inc.

- Arcomed AG

- Micrel Medical Devices SA

Frequently Asked Questions

The global intravenous infusion pumps market is projected to reach US$7.2 billion in 2026.

Increasing chronic disease prevalence, expanding critical care infrastructure, and rising adoption of smart medication delivery systems are driving growth in the intravenous infusion pumps market.

The intravenous infusion pumps market is poised to witness a CAGR of 8.8% from 2026 to 2033.

Expansion of home healthcare services, integration of artificial intelligence-enabled smart infusion systems, and growing demand for portable ambulatory infusion devices are creating key opportunities in the intravenous infusion pumps market.

Some of the key market players include Becton, Dickinson and Company, Baxter International Inc., B. Braun Melsungen AG, ICU Medical, Inc., and Fresenius Kabi AG.