- Biotechnology

- Mammalian Cell Banking Market

Mammalian Cell Banking Market Size, Share, and Growth Forecast, 2026 - 2033

Mammalian Cell Banking Market by Cell Type (Chinese Hamster Ovary (CHO) Cells, Baby Hamster Kidney (BHK) Cells, Others), Bank Type (Master Cell Bank (MCB), Others), Application (Biopharmaceutical Production, Others), and Regional Analysis for 2026 - 2033

Mammalian Cell Banking Market Share and Trends Analysis

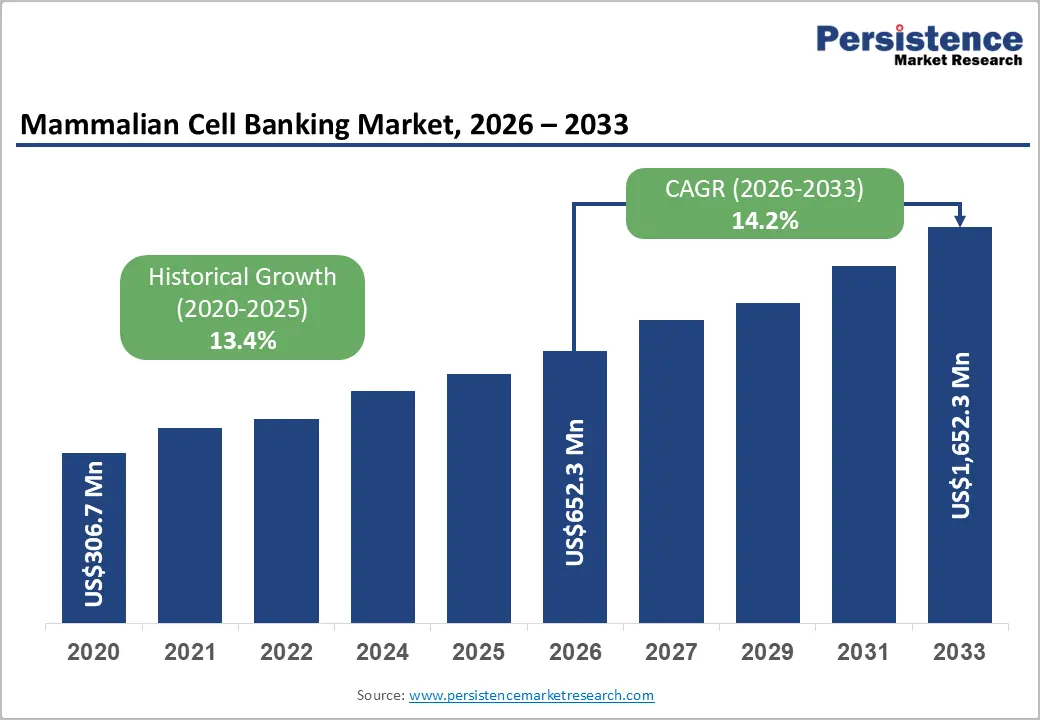

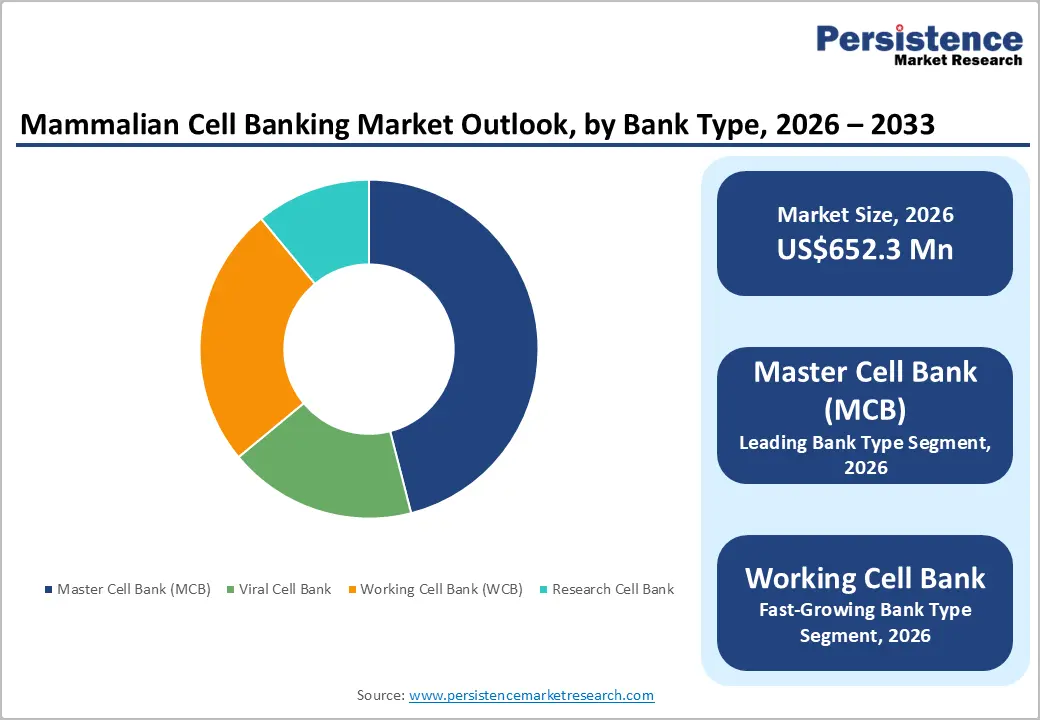

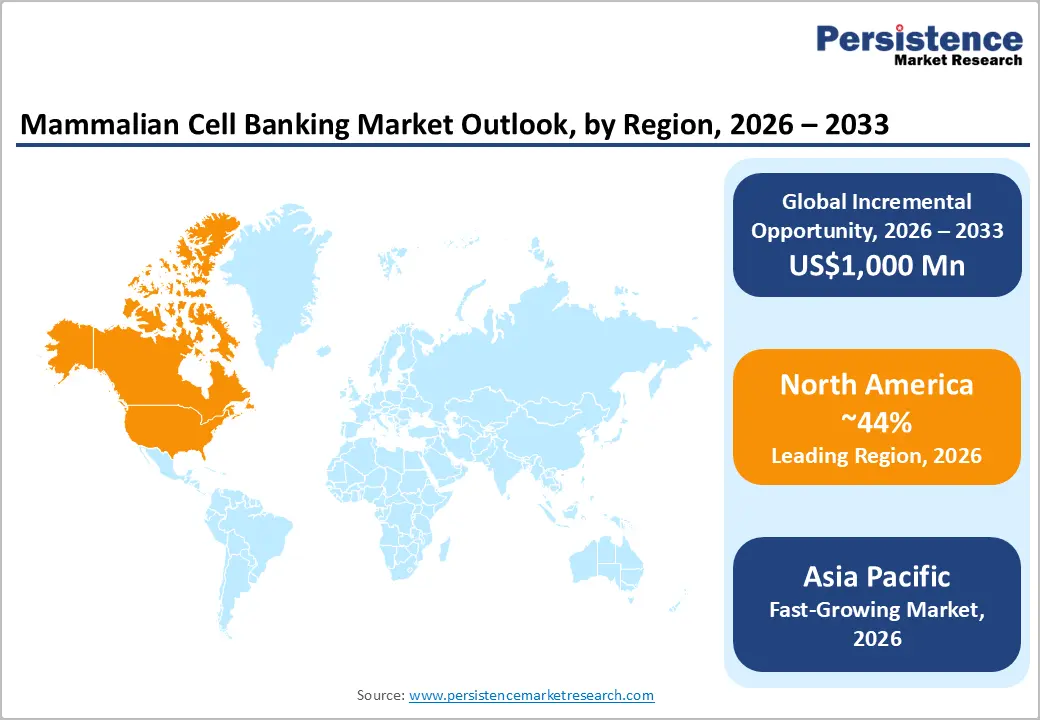

The global mammalian cell banking market size is likely to be valued at US$652.3 million in 2026 and is estimated to reach US$1,652.3 million by 2033, growing at a CAGR of 14.2% during the forecast period from 2026 to 2033, driven by rising biologics manufacturing, accelerating cell and gene therapy commercialization, and expansion of advanced bioprocessing infrastructure.

Increasing prevalence of chronic diseases and expanding aging populations are strengthening demand for monoclonal antibodies, recombinant proteins, and regenerative therapies, creating long-term requirements for standardized mammalian cell storage platforms.

Key Industry Highlights:

- Leading Bank Type: Master cell bank (MCB) is set to hold around 46% revenue share in 2026, driven by increasing regulatory focus on validated biologics manufacturing.

- Fastest-growing Bank Type: Working cell bank configurations are projected as the fastest-growing segment, supported by continuous consumption requirements within repetitive commercial bioprocessing campaigns.

- Leading Application: Biopharmaceutical production is estimated to hold roughly 48% revenue share in 2026, driven by rising monoclonal antibody commercialization.

- Fastest-growing Application: Gene therapy is forecast to record the fastest growth, driven by increasing regenerative medicine development.

- Regional Leadership: North America is projected to capture roughly 44% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth, due to rapid infrastructure expansion.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Thermo Fisher Scientific and Sartorius leveraging GMP infrastructure and biologics manufacturing integration to maintain competitive positioning.

- Innovation Trends: Technological advancements in cryopreservation systems, automated contamination monitoring, and digital quality management platforms are shaping long-term industry evolution and investment direction.

DRO Analysis

Driver - Escalating Demand for Complex Biologics and Biosimilars

The global surge in biological product development necessitates highly stable and characterized cellular substrates, which directly accelerates the deployment of specialized cell preservation frameworks. The expiration of foundational patents for blockbuster biological products triggers intensive investment in biosimilar alternatives, which requires rigorous biosafety screening and long-term phenotypic stability. According to the United States Food and Drug Administration (FDA) Center for Biologics Evaluation and Research 2025 metric report, investigational new drug applications for complex biological entities increased significantly, requiring standardized cell line management protocols.

Consequently, pharmaceutical entities require scalable, contamination-free storage solutions to ensure phenotypic consistency across multi-decade production cycles. Suboptimal cell lines increase the risk of transactional failures during large-scale bioprocessing operations, causing catastrophic financial losses during clinical manufacturing phases. Standardized repository infrastructure mitigates these risks by providing structurally verified cell lines that comply with evolving international biomanufacturing standards.

Restraint - Supply Chain Constraints in Cryogenic Materials and Equipment

Dependence on liquid nitrogen systems, specialized cryogenic containers, and validated storage consumables creates supply chain vulnerability for mammalian cell banking operations. Delays in the procurement of sterile media, freezing reagents, and monitoring instruments can interrupt production timelines and reduce operational efficiency. Equipment shortages also increase maintenance expenditure and restrict expansion capacity for rapidly growing biologics facilities.

Global transportation limitations for temperature-sensitive biological materials create additional logistical complexity for multinational pharmaceutical companies. Regulatory variations in cross-border biological sample transfer increase documentation requirements and extend approval timelines. Limited availability of specialized cryogenic infrastructure providers also reduces operational flexibility for biotechnology firms pursuing rapid manufacturing scale expansion.

Opportunity - Growth of Personalized Medicine and Regenerative Therapies

Expansion of personalized medicine is creating new commercial pathways for mammalian cell banking providers because individualized therapies require highly controlled storage and traceability systems. Autologous cell therapies and engineered immune cell products depend on long-term preservation of patient-derived biological materials. Healthcare providers are increasing investments in regenerative medicine programs, creating demand for decentralized banking infrastructure integrated with advanced therapy manufacturing facilities.

Innovation in automated cryopreservation platforms and artificial intelligence-based monitoring systems is improving storage reliability and reducing contamination risk. Companies can strengthen revenue generation through specialized banking services for CAR-T therapies, stem cell applications, and tissue engineering products. Government support for regenerative medicine commercialization is encouraging infrastructure investments across biotechnology clusters and clinical research institutions.

Category-wise Analysis

Cell Type Insights

Chinese hamster ovary (CHO) cells are anticipated to secure around 42% of the mammalian cell banking market share in 2026, reflecting strong adoption in monoclonal antibody and recombinant protein manufacturing due to high productivity and regulatory acceptance. Lonza and FUJIFILM Diosynth Biotechnologies continue expanding CHO-based production platforms for commercial biologics manufacturing.

Human embryonic kidney (HEK) cells are expected to be the fastest-growing segment, propelled by expanding applications in viral vector production, gene therapy development, and vaccine manufacturing. Thermo Fisher Scientific increased HEK-based bioprocessing support capabilities for advanced therapy developers during recent expansion initiatives.

Bank Type Insights

Master cell bank (MCB) is poised to dominate with a forecast market share of over 46% in 2026, powered by growing regulatory emphasis on standardized biologics manufacturing and long-term genetic stability validation. Sartorius strengthened GMP-compliant master banking capabilities through advanced contamination monitoring technologies supporting biologics developers. Centralized storage systems, reproducible production characteristics, and enhanced traceability standards are supporting widespread integration within commercial biopharmaceutical manufacturing environments.

Working cell bank (WCB) setups are estimated to be the fastest-growing segment, fueled by the direct utilization of these vials in routine commercial manufacturing batches. A high-throughput bioreactor facility producing therapeutic proteins thaws individual working vials continuously to initiate sequential production campaigns. This high consumption rate drives repetitive replication and optimization activities across commercial bioprocessing operations.

Application Insights

Biopharmaceutical production is likely to be the leading segment with a projected 48% of the mammalian cell banking market share in 2026, due to rising monoclonal antibody manufacturing and commercial biologics expansion across pharmaceutical facilities. FUJIFILM Diosynth Biotechnologies expanded mammalian cell culture capacity during 2025 to strengthen large-scale biologics production capabilities.

Gene therapy is anticipated to be the fastest-growing segment, fueled by increasing clinical approvals, rising investment in regenerative medicine, and expansion of viral vector manufacturing capabilities. Made Scientific announced facility expansion initiatives during 2025 to support commercial-stage cell therapy production requirements.

Regional Insights

North America Mammalian Cell Banking Market Trends

North America is expected to lead with an estimated 44% of the mammalian cell banking market share in 2026, supported by the extensive density of established biopharmaceutical enterprises and advanced clinical infrastructure. The region exhibits high adoption rates for automated cryogenic systems, driving operational efficiency in centralized cell repositories.

U.S. Mammalian Cell Banking Market Insights

The U.S. market is likely to be the primary regional revenue driver, projected to sustain high infrastructure investments due to expanding FDA approvals for novel cell-based therapeutics. Domestic contract manufacturing entities actively increase single-site cryogenic capacities to capture rising clinical demands.

Canada Mammalian Cell Banking Market Insights

The Canadian market is forecast to record steady growth driven by expanding public-private partnerships in bio-manufacturing infrastructure. Increased federal allocations toward domestic pandemic preparedness and vaccine production platforms expand localized host line storage capacities.

Europe Mammalian Cell Banking Market Trends

Europe maintains a prominent market position due to highly integrated healthcare delivery networks and robust biosimilar development pipelines. The region operates under harmonized European Medicines Agency directives that mandate complete genetic characterization and traceability for biological cell substrates. Enhanced focus on automated sample management minimizes contamination profiles within large-scale multi-user storage facilities.

Germany Mammalian Cell Banking Market Insights

The Germany market is expected to dominate continental Europe due to its advanced bioprocess engineering capabilities and extensive industrial manufacturing footprint. The strategic partnership finalized in April 2025 between Sartorius and Mabion S.A. to scale mammalian cell biopharmaceutical development demonstrates the regional focus on integrated processing.

U.K. Mammalian Cell Banking Market Insights

The U.K. market is likely to be driven by significant institutional investments into genomic medicine and advanced cell therapy development. The growth of specialized biotechnology hubs across the region increases the cumulative volume of unique therapeutic cell lines requiring long-term security. Localized regulatory frameworks designed to expedite innovative therapies accelerate the transition of cell banks from research phases into clinical manufacturing status.

Asia Pacific Mammalian Cell Banking Market Trends

Asia Pacific is forecast to be the fastest-growing market for mammalian cell banking, stimulated by rapid biomanufacturing infrastructure expansion and lower operational cost structures. The regional landscape shifts toward the integration of advanced single-use bioreactor technologies, which increases the frequency of manufacturing cell line setups. Growing regulatory harmonization with international standards encourages multinational biopharmaceutical firms to establish regional production bases.

China Mammalian Cell Banking Market Insights

The China market is anticipated to record rapid expansion driven by national strategic initiatives focused on biopharmaceutical self-sufficiency. Localized development of therapeutic monoclonal antibodies and cell-based vaccines requires massive scaling of host cell line archives, particularly CHO and Vero derivatives.

Japan Mammalian Cell Banking Market Insights

The Japanese market is expected to experience steady advancement supported by an advanced regenerative medicine landscape and high institutional expertise in stem cell technologies. Regional research groups utilize precise cryogenic methods to manage induced pluripotent stem cell repositories for therapeutic evaluation.

Competitive Landscape

The global mammalian cell banking market is moderately fragmented, characterized by participation from multinational bioprocessing companies, contract development and manufacturing organizations, and specialized cryopreservation service providers. Competition is centered on GMP compliance, contamination control capabilities, storage scalability, and integration of automated monitoring technologies. Leading participants include Thermo Fisher Scientific Inc., Sartorius AG, Merck KGaA, Charles River Laboratories, and Lonza Group AG.

Strategic investments in biologics infrastructure and advanced therapy manufacturing are strengthening competitive differentiation across the industry. Companies are expanding cryogenic storage capacity, digital quality management systems, and viral vector production capabilities to support growing commercial demand. Partnership agreements, facility expansion projects, and integrated outsourcing solutions are increasing operational scale and reinforcing long-term positioning within biopharmaceutical manufacturing ecosystems.

Key Industry Developments:

- In September 2025, Sartorius Stedim Biotech expanded GMP transfection reagent production capacity in France, reinforcing supply chain reliability and advanced infrastructure development for cell therapy manufacturing.

- In May 2025, Made Scientific announced a 12,000 sq. ft. expansion of its Princeton GMP facility, reinforcing commercial-scale advanced cell therapy manufacturing capacity.

Companies Covered in Mammalian Cell Banking Market

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Merck KGaA

- Lonza Group AG

- Charles River Laboratories International, Inc.

- WuXi Biologics

- FUJIFILM Diosynth Biotechnologies

- STEMCELL Technologies Inc.

- PromoCell GmbH

- Corning Incorporated

- Bionova Scientific

- BioReliance Corporation

- Oxford Biomedica plc

- Samsung Biologics

- Charles River Laboratories

Frequently Asked Questions

The mammalian cell banking market is projected to reach US$652.3 million in 2026.

Increasing biologics production, expanding cell and gene therapy development, and rising regulatory focus on GMP-compliant biomanufacturing drive the mammalian cell banking market.

The mammalian cell banking market is poised to witness a CAGR of 14.2% from 2026 to 2033.

Expansion of personalized medicine, outsourced bioprocessing services, and advanced cryopreservation technologies creates key growth opportunities in the mammalian cell banking market.

Some of the key market players include Thermo Fisher Scientific Inc., Sartorius AG, Merck KGaA, Lonza Group AG, Charles River Laboratories International, Inc., and WuXi Biologics.