- Inks, Coatings, Adhesives & Sealants (ICAS)

- Glass Glue Market

Glass Glue Market Size, Share, and Growth Forecast, 2026 - 2033

Glass Glue Market by Product Type (Silicone-Based, Polyurethane-Based, Others), Application (Construction, Automotive, Electronics, Furniture, Others), Distribution Channel (Online Stores, Others), and Regional Analysis for 2026 - 2033

Glass Glue Market Size and Trends Analysis

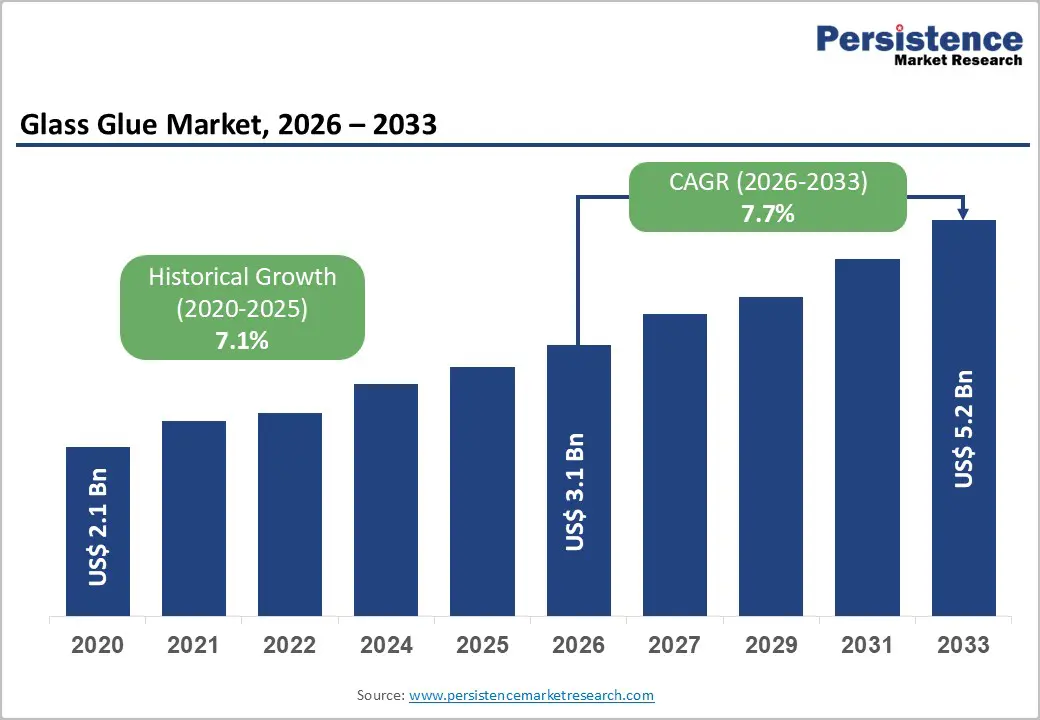

The global glass glue market size is likely to be valued at US$3.1 billion in 2026, and is expected to reach US$5.2 billion by 2033, growing at a CAGR of 7.7% during the forecast period from 2026 to 2033, driven by rising demand for high-performance adhesives in construction, automotive, and electronics industries, along with increasing use of glass in modern architecture and consumer products. Increasing preference for transparent, durable, and fast-curing glass glue solutions remains a major driver of glass glue market growth.

Key Industry Highlights:

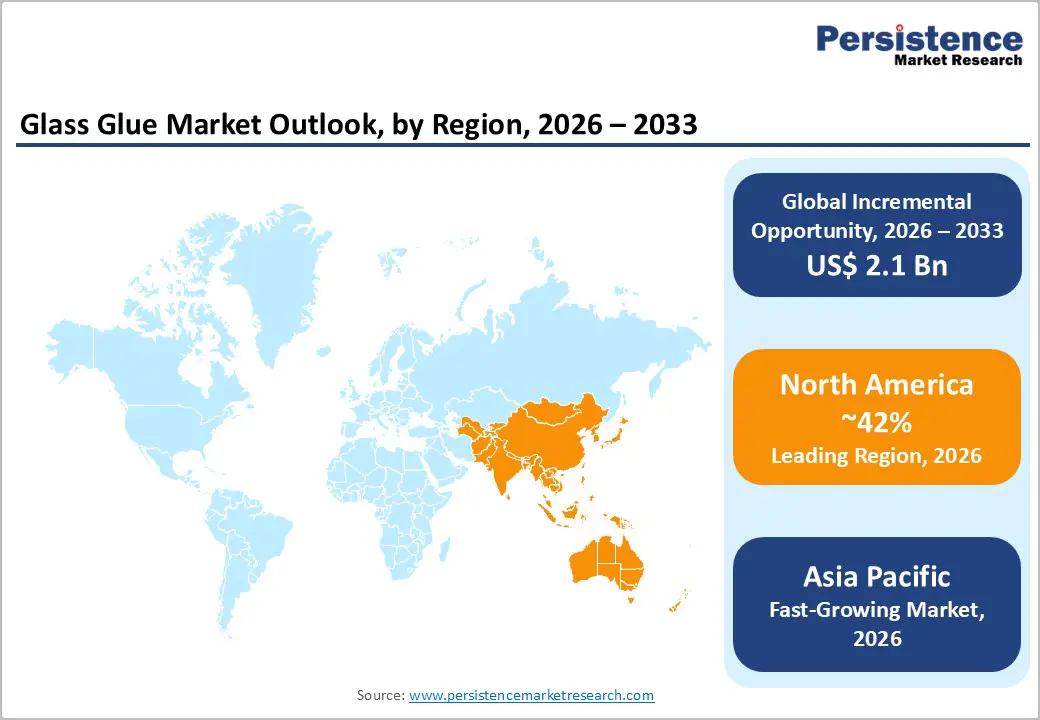

- Leading Region: Asia Pacific, anticipated to account for a 42% market share in 2026, driven by industrialization, urban expansion, and strong demand from construction and infrastructure in China, India, and Japan.

- Fastest-growing Region: Asia Pacific, fueled by urbanization, infrastructure development, and the expanding consumer electronics sector.

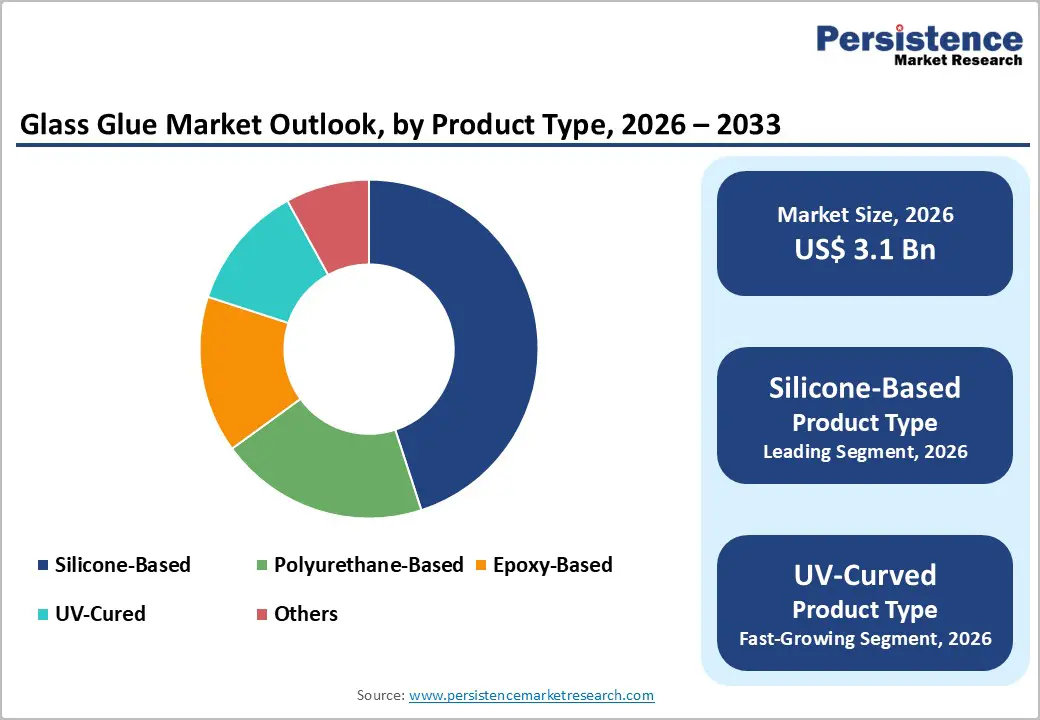

- Dominant Product Type: Silicone-based, to hold approximately 46% of the market share, due to excellent flexibility, transparency, and weather resistance.

- Leading Application: The construction segment is projected to dominate with over 40% share in 2026, driven by extensive use in structural glazing and architectural applications requiring durable, weather-resistant, and energy-efficient bonding solutions.

| Key Insights | Details |

|---|---|

|

Glass Glue Market Size (2026E) |

US$3.1 Bn |

|

Market Value Forecast (2033F) |

US$5.2 Bn |

|

Projected Growth CAGR (2026-2033) |

7.7% |

|

Historical Market Growth (2020-2025) |

7.1% |

DRO Analysis

Driver - Increasing Preference for Lightweight and High-Strength Bonding Solutions

The increasing preference for lightweight and high-strength bonding solutions is a significant factor shaping the glass glue market. Traditional fastening methods, such as screws, bolts, and welding, add extra weight and often create stress concentration points that can weaken materials over time. In contrast, glass adhesives distribute stress more evenly across the bonded surface, improving structural integrity and durability. This makes them particularly suitable for applications where both strength and weight reduction are critical.

In industries such as automotive and aerospace, reducing overall weight is directly linked to improved fuel efficiency, lower emissions, and enhanced performance. Glass adhesives enable manufacturers to replace heavier mechanical fasteners while maintaining strong and reliable bonds. Similarly, in construction and architecture, lightweight bonding solutions allow for the design of modern structures with large glass panels, curtain walls, and frameless designs without compromising safety. These adhesives offer flexibility, vibration resistance, and compatibility with different materials, further enhancing their appeal.

Rising Demand from the Construction & Infrastructure Sector

Rapid urbanization and expanding infrastructure projects are significantly boosting the use of glass bonding adhesives across residential, commercial, and industrial construction. Modern architectural designs increasingly incorporate large glass panels, curtain walls, skylights, and facades to enhance natural lighting and aesthetic appeal. In such applications, glass glue plays a crucial role by providing strong, durable, and nearly invisible bonding, enabling sleek and seamless structures.

Unlike traditional fastening methods, adhesives help distribute loads evenly and reduce the risk of stress fractures in glass components. This improves the overall safety and longevity of buildings, especially in high-rise constructions and structures exposed to varying environmental conditions. The growing focus on energy-efficient buildings has increased the adoption of insulated and smart glass systems, where reliable bonding solutions are essential for maintaining thermal performance and structural integrity. Infrastructure development projects such as airports, metro stations, and commercial complexes also rely heavily on glass for both functional and design purposes, further driving adhesive demand.

Restraint - High Cost of Advanced Adhesive Formulations

Advanced glass adhesives often involve complex chemical compositions, such as UV-curable resins, epoxies, and hybrid polymers, which increase production costs. These materials require specialized raw inputs and precise manufacturing processes to achieve properties such as high transparency, strong bonding strength, and resistance to heat, chemicals, and environmental stress. The final product becomes more expensive compared to conventional bonding alternatives.

For many small- and medium-scale manufacturers or cost-sensitive end users, this price difference can act as a barrier to adoption. In industries where margins are tight, companies may prefer traditional fastening methods or lower-cost adhesives, even if performance is slightly compromised. The need for supporting equipment, such as UV curing systems or controlled application environments, can further raise overall implementation costs.

Technical Limitations in Bonding Performance

Achieving reliable adhesion on glass surfaces can be challenging due to variations in surface properties such as coatings, treatments, and smoothness. Certain types of glass, including tempered, laminated, or coated variants, may reduce the effectiveness of adhesives, leading to weaker bonds if not properly treated. Surface contamination, moisture, or improper preparation can further compromise bonding quality.

Environmental factors also play a significant role in performance. Exposure to extreme temperatures, humidity, ultraviolet radiation, or chemicals can gradually degrade adhesive strength over time. In demanding applications such as automotive glazing or exterior building structures, even minor performance inconsistencies can affect long-term durability and safety.

Opportunity - Growing Demand for Eco-Friendly and Bio-Based Adhesives

Environmental concerns and stricter regulations on chemical emissions are encouraging a shift toward safer and more sustainable bonding solutions. Conventional glass adhesives often contain solvents and compounds that release volatile organic compounds (VOCs), which can impact air quality and pose health risks during application. As awareness of these issues increases, industries are actively seeking alternatives that minimize environmental impact without compromising performance.

Manufacturers are responding by developing adhesives derived from renewable resources and formulating products with low or zero VOC content. These eco-friendly options not only help companies comply with environmental standards but also improve workplace safety by reducing exposure to harmful substances. In sectors such as construction and automotive, where sustainability goals are becoming more prominent, the use of greener materials is gaining importance. Consumers are showing a growing preference for environmentally responsible products, influencing purchasing decisions across various industries.

Expansion of Smart Glass and Advanced Glazing Technologies

The increasing adoption of intelligent and energy-efficient glass solutions is creating new requirements for advanced bonding technologies. Smart glass, which can adjust its transparency based on light, heat, or electrical signals, is being widely used in modern buildings, vehicles, and electronic displays. These applications demand adhesives that provide strong bonding while maintaining optical clarity and not interfering with the glass’s functional properties.

Advanced glazing systems used in construction focus on improving insulation, noise reduction, and energy efficiency. Multi-layered glass panels and coated surfaces require adhesives that can bond different layers securely without degrading performance over time. This creates a need for specialized formulations that offer durability, weather resistance, and compatibility with treated glass surfaces. In automotive and transportation sectors, advanced glazing is increasingly used for panoramic roofs, windshields, and windows to enhance design and passenger comfort. Adhesives must therefore withstand vibrations, temperature fluctuations, and long-term exposure to environmental stress.

Category-wise Analysis

Product Type Insights

Silicone-based glass glue is anticipated to dominate, accounting for 46% share in 2026, driven by its excellent flexibility, strong adhesion, and superior resistance to temperature variations, moisture, and UV exposure. These properties make it highly suitable for demanding applications in construction, automotive, and electronics. Silicone adhesives maintain long-term durability without cracking or losing bonding strength, even under harsh environmental conditions. Their ability to bond dissimilar materials and accommodate thermal expansion enhances reliability in structural and glazing applications. DOWSIL™ 982 Silicone Insulating Glass Sealant, produced by Dow, is engineered for structural and insulating glass applications, offering strong, long-lasting, and weather-resistant bonding between glass and metal surfaces.

UV-cured represents the fastest-growing segment, due to its ability to cure rapidly when exposed to ultraviolet light, significantly reducing production time. This instant curing capability improves manufacturing efficiency and supports high-speed assembly processes, especially in electronics, automotive, and glass fabrication industries. These adhesives also provide strong, precise, and transparent bonds, making them ideal for applications where clarity and accuracy are critical. Fasto UV92 High Strength UV Curable Adhesive, offered by Fasto Adhesives, is formulated for glass bonding applications that require strong adhesion, optical clarity, and high precision. It quickly hardens upon exposure to UV light, allowing faster assembly and enhancing overall efficiency in industrial manufacturing processes.

Application Insights

The construction segment is projected to dominate with over 40% of the share in 2026, fueled by its widespread use in structural glazing and architectural applications. Glass adhesives are essential for bonding large panels in façades, curtain walls, skylights, and interior partitions, enabling modern, seamless building designs. They provide strong, durable, and weather-resistant bonds that enhance structural integrity and safety. The growing focus on energy-efficient buildings and advanced glazing systems increases the need for reliable bonding solutions. DOWSIL™ 995 Silicone Structural Sealant, produced by Dow Inc., is extensively utilized in construction for structural glazing applications, including the bonding of glass panels in façades and curtain wall systems. It delivers strong adhesion between glass and metal substrates while retaining flexibility to endure wind pressure, temperature variations, and environmental stress.

The electronics segment is the fastest-growing application, supported by the increasing demand for advanced display technologies and touchscreen devices. Glass adhesives play a critical role in bonding components in smartphones, tablets, laptops, and televisions, where precision and optical clarity are essential. As devices become thinner and more compact, manufacturers require adhesives that provide strong bonding without adding bulk. DELO PHOTOBOND UV adhesives developed by DELO Industrial Adhesives. These products are extensively used in electronics manufacturing for bonding glass components in displays, touch panels, and optical devices. They provide rapid curing within seconds, excellent optical clarity, and precise application, making them well-suited for compact and high-performance electronic products.

Regional Insights

North America Glass Glue Market Trends

North America is experiencing steady growth driven by strong demand across the construction, automotive, and electronics industries. In the construction sector, increasing adoption of modern architectural designs featuring large glass panels, curtain walls, and energy-efficient glazing systems is boosting the use of high-performance adhesives. The region’s focus on sustainable building practices is also encouraging the use of low-VOC and environmentally friendly glass bonding solutions.

In the automotive industry, the shift toward lightweight vehicles and electric mobility is accelerating the use of advanced adhesives for bonding windshields, sunroofs, and windows. These adhesives help improve fuel efficiency and structural performance while reducing vehicle weight. The growing electronics sector, supported by demand for high-quality displays and smart devices, is contributing to increased adoption of precision glass bonding technologies. Technological advancements, including UV-curable and fast-setting adhesives, are gaining traction due to their efficiency and compatibility with automated manufacturing processes. Furthermore, strict regulatory standards related to safety and environmental impact are pushing manufacturers to innovate and develop safer, more durable formulations.

Europe Glass Glue Market Trends

Europe market growth is characterized by strong innovation, sustainability focus, and advanced industrial demand. The increasing emphasis on environmentally friendly adhesives is driven by strict regulations on emissions and chemical safety. Manufacturers are actively developing low-VOC, solvent-free, and bio-based formulations to comply with regulatory standards and support sustainable practices.

The region also benefits from a well-established automotive industry, particularly in countries including Germany, France, and the UK, where glass adhesives are widely used in vehicle glazing, electric vehicles, and advanced display integration. The growing adoption of lightweight materials and structural bonding is encouraging the replacement of mechanical fasteners with adhesives to improve efficiency and design flexibility. In the construction sector, demand is rising for modern architectural designs, including glass façades and energy-efficient buildings. Adhesives are increasingly used in prefabricated and unitized glazing systems, supporting faster installation and improved performance. Technological advancements such as UV-curable and hybrid adhesives are gaining popularity due to their fast curing, durability, and compatibility with automated manufacturing processes.

Asia Pacific Glass Glue Market Trends

Asia Pacific is projected to dominate and be the fastest-growing, capturing 42% of revenue share in 2026, powered by strong industrialization, urban expansion, and increasing manufacturing activities. Countries such as China, India, and Japan are experiencing high demand for glass adhesives due to large-scale construction projects and infrastructure development. The rising adoption of modern architectural designs, including glass façades and high-rise buildings, is significantly boosting the use of advanced bonding solutions.

The region is also a global hub for electronics manufacturing, with increasing production of smartphones, displays, and consumer devices driving demand for precision glass bonding adhesives. The expanding automotive sector, particularly the growth of electric vehicles, is accelerating the use of lightweight and durable adhesive solutions for glass components. The region is witnessing a shift toward cost-effective and high-performance adhesives to support mass production. Manufacturers are focusing on developing fast-curing and easy-to-apply formulations that enhance efficiency in automated production lines. Growing awareness of environmental concerns is gradually encouraging the adoption of low-VOC and eco-friendly adhesives.

Competitive Landscape

The global glass glue market is highly competitive, with major players continuously striving to strengthen their market position through innovation and performance enhancement. Companies such as 3M Company, Henkel AG & Co. KGaA, and Sika AG focus on developing advanced adhesives with improved transparency, durability, and bonding strength to meet evolving industry needs.

Firms such as H.B. Fuller Company, Dow Inc., and Wacker Chemie AG emphasize sustainable and low-VOC formulations to align with environmental regulations. Meanwhile, Bostik SA and Avery Dennison Corporation leverage strong global distribution networks to expand their reach across construction and industrial sectors. Companies such as Illinois Tool Works Inc. and Momentive Performance Materials Inc. invest in technological advancements and customized solutions.

Key Industry Developments:

- In June 2025, Henkel showcased its latest advances in adhesives, functional coatings, thermal management, and sealing solutions as key enablers of safer, more efficient, and more sustainable EV batteries. The company enhanced these core technologies with AI-powered simulation and debonding innovations, enabling OEMs and battery manufacturers to reduce development cycles and costs, improve performance, and support circularity across the battery lifecycle.

- In May 2025, Sika Industry USA announced the introduction of Sikaflex® P2G Premium, a new high-performance solution designed to complement its industry-leading primerless AGR product line. Sikaflex® P2G Premium delivered a 3-hour Minimum Drive-Away Time (MDAT), optimized performance at elevated temperatures, a short cut-off string, and excellent decking and glass-slip properties. By eliminating the need for pretreatment of glass or frit, the product enabled technicians to simplify the windshield replacement process.

Companies Covered in Glass Glue Market

- 3M Company

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Dow Inc.

- Bostik SA

- Permatex Inc.

- Loctite (Henkel)

- Gorilla Glue Company

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Avery Dennison Corporation

- Ashland Global Holdings Inc.

- Illinois Tool Works Inc.

Frequently Asked Questions

The global glass glue market is projected to reach US$3.1 billion in 2026.

The growing preference for lightweight and high-strength bonding solutions is driving the glass glue market, as traditional fasteners add weight and create stress points.

The glass glue market is poised to witness a CAGR of 7.7% from 2026 to 2033.

Environmental concerns and strict emission regulations are driving the shift toward safer, sustainable bonding solutions.

Key players in the glass glue market include 3M Company, Henkel AG & Co. KGaA, Sika AG, Dow Inc., and H.B. Fuller Company.