- Semiconductor Materials & Components

- Functional Printing Market

Functional Printing Market Size, Share, and Growth Forecast 2026–2033

Functional Printing Market by Material Type (Conductive Materials, Dielectric Materials, Semiconductor Materials, Functional/Active Materials, Others), Technology (Inkjet Printing, Screen Printing, Flexographic Printing, Gravure Printing, Others), Application (Electronics & Semiconductor, Packaging & Labelling, Healthcare, Energy & Photovoltaics, Automotive, Industrial, Aerospace & Defense, Wearables & Smart Textiles, Others), and Regional Analysis, 2026–2033

Global Functional Printing Market Size and Trend Analysis

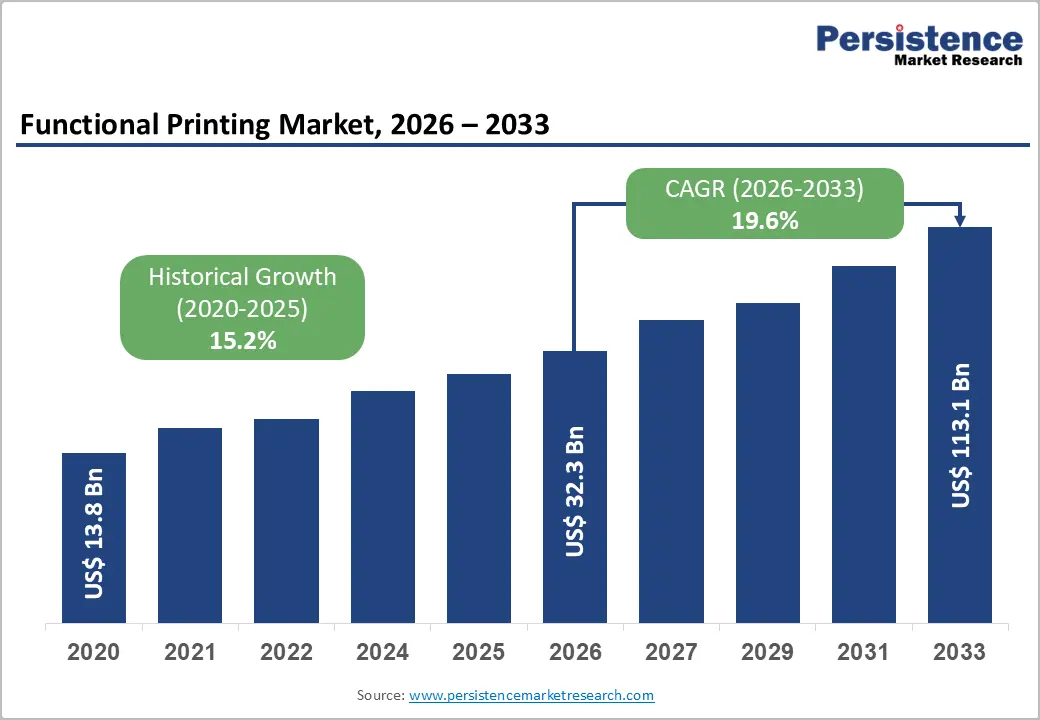

The global functional printing market size is expected to be valued at US$ 32.3 billion in 2026 and is projected to reach US$ 113.1 billion by 2033, growing at a CAGR of 19.6% between 2026 and 2033. This reflects increasing demand for advanced manufacturing techniques that enable cost-effective, scalable, and high-performance material deposition across industries.

The growing use of functional inks in flexible and wearable devices is accelerating innovation in next-generation product design, particularly in healthcare monitoring and smart textiles. Sustained investments from both public and private sectors in areas such as smart packaging and photovoltaic technologies are further boosting market growth.

Key Industry Highlights:

- Leading Material Type: Conductive Materials dominate the market with over 36% share in 2026, valued at more than US$ 11.63 Bn, driven by their essential role in enabling electrical conductivity across applications such as RFID, sensors, photovoltaics, and printed circuits.

- Leading Technology: Screen Printing leads with over 30% market share in 2026, valued at more than US$ 9.69 Bn, supported by its ability to deliver thick, durable, and high-conductivity layers for large-scale industrial applications.

- Fastest Growing Technology: Inkjet Printing is the fastest-growing technology, driven by the increasing need for precision, customization, and non-contact printing for flexible and sensitive substrates.

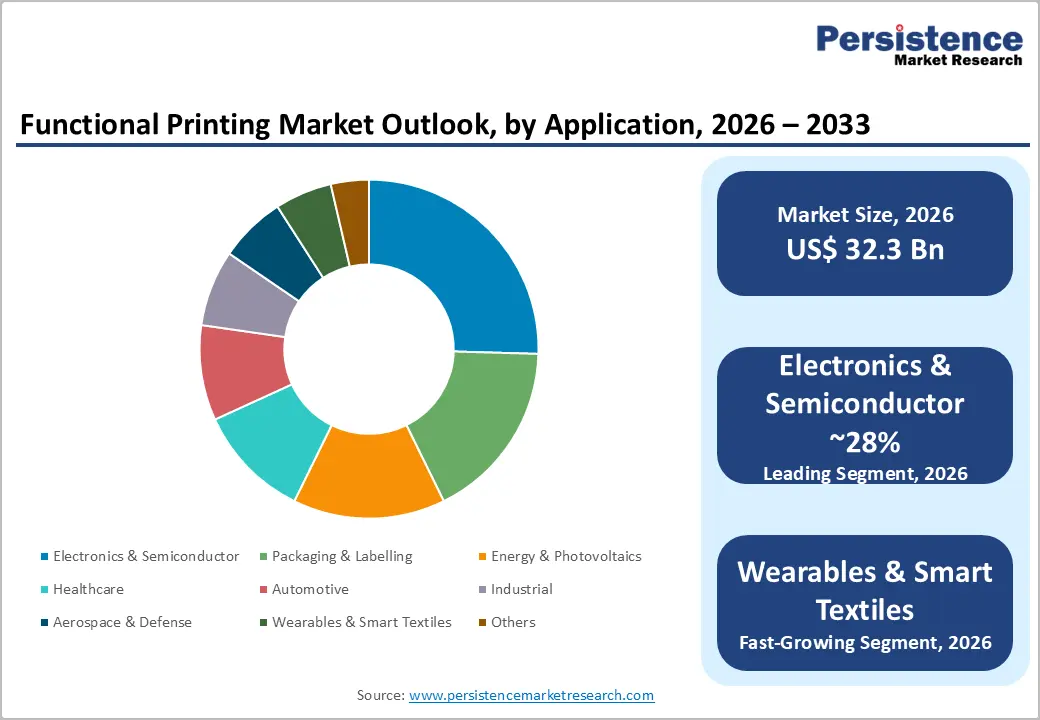

- Leading Application: Electronics & Semiconductor accounts for approximately 28% of the market in 2026, valued at more than US$ 9.04 Bn, driven by demand for miniaturized, cost-efficient, and high-throughput electronic manufacturing.

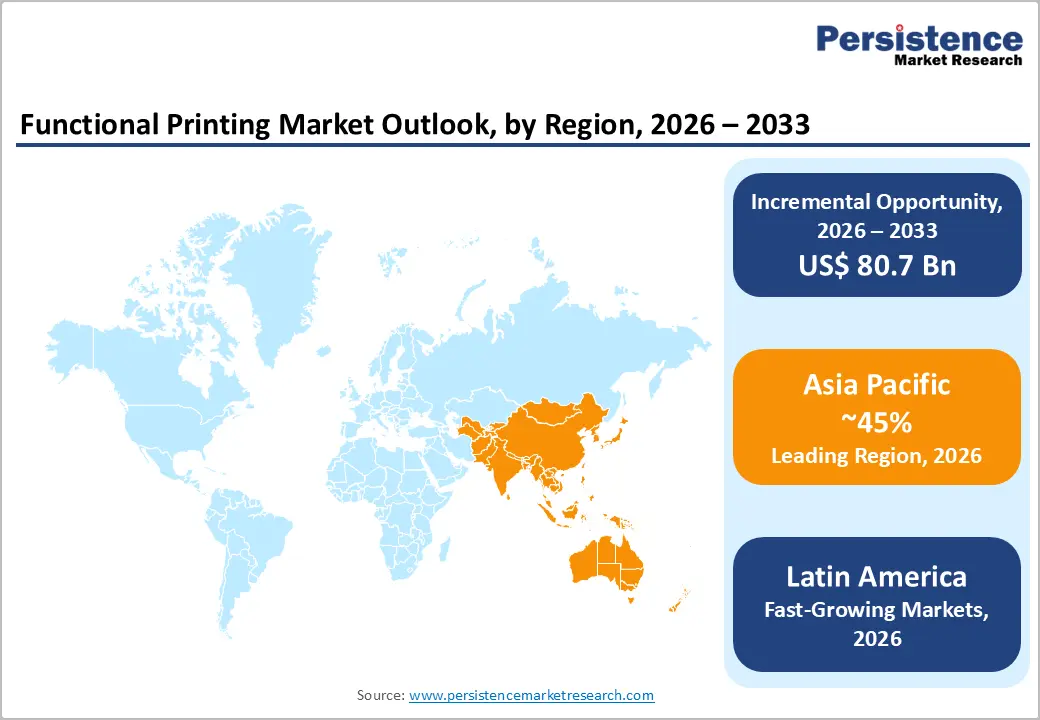

- Leading Region: Asia Pacific dominates the market with over 45% share in 2026, valued at more than US$ 14.53 Bn, driven by strong electronics manufacturing, solar energy expansion, and government-backed initiatives. North America remains a key innovation hub, while the Asia Pacific is also a fast-growing market with a CAGR of 25.1%, supported by large-scale industrialization and policy support.

Market Dynamics

Drivers - Rising Demand for Flexible & Lightweight Electronics

Traditional rigid components are increasingly being replaced by bendable, thin, and lightweight alternatives in devices such as wearables, foldable displays, and smart textiles. Functional printing enables electronic circuits and components to be directly printed onto flexible substrates like plastic films and fabrics. This reduces overall weight and enhances portability and user comfort. It supports innovative product designs that are not feasible with conventional manufacturing methods. For example, India’s electronics exports grew by over 32% in FY2025, indicating strong global demand for lightweight electronic products. As consumer electronics and healthcare devices continue to evolve toward compact and flexible formats, the reliance on functional printing technologies is accelerating.

Policy-Backed Expansion of Renewable Energy and Smart Packaging Infrastructure

Government mandates and regulatory incentives across North America, Europe, and the Asia Pacific are creating structural, policy-driven demand for functional printing in photovoltaic manufacturing and intelligent packaging. The European Union's Packaging and Packaging Waste Regulation, progressively tightening through 2026–2030, is pushing brand owners toward printed smart labels that integrate tamper-evidence, freshness sensing, and track-and-trace functionality directly into packaging substrates. Simultaneously, national solar energy targets, including China's commitment to 1,200 GW of installed renewable capacity by 2030, are accelerating deployment of perovskite and organic photovoltaic cells, where functional printing is the enabling deposition technology. These converging policy signals generate sustained, multi-year demand visibility that reduces adoption risk for equipment and materials suppliers entering the functional printing space.

Restraints - High Capital Intensity and Materials Cost Complexity

The functional printing industry faces a persistent restraint in the form of elevated capital expenditure requirements for precision deposition equipment, combined with the volatile cost profiles of speciality functional inks containing silver, gold, or rare earth compounds. Silver-based conductive inks are the dominant material input for many printed electronics applications, tracking silver commodity prices, which fluctuated by more than 30% between 2022 and 2024, compressing margins for both ink formulators and end-use converters. Smaller manufacturers and emerging-market entrants struggle to absorb these cost swings without passing increases downstream, creating friction in customer acquisition cycles. These materials cost complexity slows adoption in price sensitive.

Technical Scalability and Print Quality Consistency Barriers

Translating laboratory-proven functional printing processes into high-volume, repeatable manufacturing remains a significant technical restraint, particularly for semiconductor and active-layer deposition, where nanometre-scale uniformity determines device performance. Yield rates in printed organic semiconductor manufacturing still lag behind silicon-based alternatives by a factor of 2–3x at comparable production volumes, according to industry data from process engineering assessments. The challenge compounds when manufacturers attempt to migrate from batch to roll-to-roll continuous production, where maintaining ink rheology, substrate tension, and drying kinetics simultaneously across wide web widths introduces new failure modes.

Opportunities - Integration of Functional Printing in Next-Generation Healthcare Diagnostics and Drug Delivery

Printed biosensors, electrochemical test strips, and transdermal drug delivery patches represent application categories where the cost-per-unit economics of high-speed functional printing versus cleanroom microfabrication create decisive competitive advantages for healthcare device manufacturers.

Companies with existing relationships in the in-vitro diagnostics supply chain should prioritise the development of biocompatible functional ink formulations certified under FDA 21 CFR and CE IVD regulatory frameworks, as regulatory pre-clearance increasingly functions as a market access prerequisite. The global push for decentralised healthcare, accelerated by post-pandemic infrastructure investment in Asia Pacific and Latin America, is expanding the installed base of point-of-care devices and creating recurring demand for printed diagnostic consumables.

Wearable Technology and Smart Textile Platforms as a Structural Growth Vector

Smart textiles are expanding at a pace, driven by commercial adoption from sportswear brands, military procurement programmes, and eldercare monitoring applications. Companies best positioned to capture this opportunity are those investing in elastomeric conductive ink formulations and hybrid printing-lamination processes that survive repeated mechanical deformation and industrial laundering cycles.

The emergence of ISO/TR 23383 and related international standards for electronic textiles signals that the regulatory infrastructure for commercial-scale smart textile deployment is maturing, reducing customer qualification timelines. Firms that establish reference installations with tier-one apparel manufacturers or defence integrators before 2027 will create substantial switching-cost advantages that compress competitive entry in subsequent years.

Category-wise Analysis

Material Type Insight

Conductive materials account for over 36.0% of the global functional printing market in 2026, reaching approximately US$11.63 billion, as they fulfill the core requirement of enabling electrical conductivity across all printed electronic applications. From RFID antennas and touch sensors to photovoltaic cells and electromagnetic shielding, the need for efficient signal transmission, energy flow, and circuit formation makes conductive materials indispensable. Their widespread adoption is driven by the universal requirement for reliable, scalable, and low-cost electronic functionality across industries such as consumer electronics, automotive, and energy, ensuring sustained and diversified demand.

Functional/active materials represent the fast-growing segment, fueled by the increasing need for intelligent, responsive, and interactive functionalities in next-generation applications. Growing demand for real-time health monitoring, smart packaging with condition sensing, and adaptive display technologies is accelerating the adoption of materials capable of sensing, reacting, or changing properties based on external stimuli. As industries shift toward personalization, automation, and enhanced user interaction, the need for such advanced functionalities continues to rise.

Technology Insights

Screen printing is likely to account for over 30% of market share in 2026, exceeding over US$ 9.69 billion. End-use sectors such as photovoltaics, automotive electronics, and membrane switches require robust electrical conductivity, durability, and long lifecycle performance, which in turn necessitate the use of high-viscosity inks like silver pastes and dielectric materials. It uniquely fulfills this requirement by enabling uniform, thick film deposition without compromising throughput, thereby ensuring cost-efficiency in high-volume manufacturing. Industries demand process reliability and compatibility across diverse substrates, further reinforcing screen printing’s position as the preferred solution for standardized, large-scale production environments.

Inkjet printing is a fast-growing technology, due to the increasing need for precision, flexibility, and customization in next-generation applications. Emerging sectors such as healthcare diagnostics, flexible electronics, and personalized packaging require non-contact deposition methods capable of handling sensitive, irregular, or flexible substrates without material damage. The shift toward mass customization and variable data printing has created a strong demand for digitally controlled, tool-less manufacturing processes, where inkjet printing offers a clear advantage by eliminating the need for physical masks or screens.

Application Analysis

Electronics & semiconductors are likely to account for approximately 28% of the global Functional Printing market in 2026, equivalent to US$ 9.04 billion, driven by the need for cost-efficient, high-throughput, and miniaturized electronic manufacturing. Functional printing enables precise circuit patterning, lightweight integration, and reduced material wastage compared to conventional fabrication methods. It also supports scalable production of antennas, interconnects, and display components. These capabilities directly address industry demands for performance, efficiency, and design flexibility.

Wearables & Smart Textiles represent the fastest growing application, fueled by the need for continuous health monitoring and seamless device integration into daily life. Functional printing enables flexible, stretchable, and biocompatible electronics suited for body-conformal applications. The demand is further supported by the defense and fitness sectors requiring real-time data tracking. Traditional rigid electronics fail to meet these needs, accelerating the adoption of printed solutions.

Regional Insights

North America Functional Printing Market Trends and Insights

North America is expected to be valued at over US$ 5.81 billion in 2026, supported by strong demand from advanced electronics, healthcare devices, and aerospace manufacturing. The region benefits from highly developed innovation ecosystems such as Silicon Valley, Research Triangle Park, and the Greater Boston corridor, where collaboration between startups and established firms accelerates material and process innovation. Government initiatives like the CHIPS and Science Act and programs led by the U.S. Department of Energy are driving investments in domestic manufacturing and printed electronics infrastructure.

The United States Functional Printing Market dominates the regional market, contributing over 82.0% share with value reaching US$ 4.77 billion in 2026, driven by strong capabilities in semiconductor packaging, medical device manufacturing, and flexible electronics commercialization. The demand is especially concentrated in electronics and healthcare, where OEMs are leveraging printed functional layers to enable lightweight, compact, and advanced product designs. Consistent funding from the U.S. Department of Defense for applications such as wearable battlefield sensors and conformal antennas ensures stable demand.

Asia Pacific Functional Printing Market Trends and Insights

Asia Pacific dominates the global functional printing market in 2026, accounting for more than 45.0% share valued at US$ 14.53 billion, and is projected to grow at a CAGR of 25.1% through 2033, driven by the region’s massive electronics manufacturing base across China, Japan, and South Korea, alongside rising adoption in solar energy and wearable electronics. Strong government backing, including China’s industrial transformation frameworks and India’s Production Linked Incentive (PLI) schemes, is accelerating investments in printed electronics infrastructure.

China leads the Asia Pacific market with value exceeding to US$ 5.67 Billion in 2026, supported by its scale in solar cell manufacturing, consumer electronics, and packaging production. Japan value is expected to reach at US$ 2.62 Billion, driven by its expertise in precision printing equipment, specialty inks, and organic electronics, with strong applications in healthcare diagnostics and automotive electronics. South Korea totaling US$ 2.03 Billion value by 2026, anchored by its dominance in OLED display manufacturing and semiconductor packaging. These three countries collectively form the technological backbone of the regional market, driving innovation and large-scale adoption of functional printing technologies.

India and Southeast Asia are emerging as key high-growth markets within the region. India is expected to reach over US$ 1.45 Billion value in 2026, supported by expanding electronics manufacturing, pharmaceutical packaging demand, and government-led digitization initiatives such as smart cities and RFID adoption. Southeast Asia growth is driven by manufacturing relocation trends. Countries like Vietnam, Thailand, and Malaysia are attracting global investments as companies diversify supply chains beyond China.

Latin America Functional Printing Market Trends and Insights

Latin America is expected to reach over US$ 1.94 billion, with demand concentrated in packaging, labelling, and emerging renewable energy applications. The growth is largely driven by the region’s expanding FMCG sector, which is adopting smart packaging for traceability and brand differentiation. While infrastructure gaps and currency volatility in key economies such as Brazil and Mexico constrain rapid adoption, the market is steadily progressing. Increasing manufacturing sophistication and alignment with global supply chains are expected to support consistent growth.

Brazil dominates the regional landscape with an over 52.0% share, surpassing value US$ 1.01 billion in value in 2026, driven by strong demand across automotive, pharmaceuticals, and food packaging sectors. Regulatory frameworks such as those implemented by ANVISA are accelerating adoption of printed authentication and track-and-trace solutions, alongside growth in solar energy applications. Mexico accounts for over US$ 0.50 billion value by 2026, benefiting from its integration into North American supply chains and nearshoring trends under the USMCA. Expansion in automotive electronics and printed sensor technologies is expected to drive growth in Mexico’s functional printing market.

Competitive Landscape

The Functional Printing market is moderately fragmented at the global level with pockets of concentrated competition in specific material and technology sub-segments. Leading companies compete primarily on the basis of materials innovation capability, printing system integration depth, and regulatory compliance infrastructure particularly in healthcare and aerospace application tiers, where qualification cycles create durable competitive moats. The dominant strategic themes shaping competition include vertical integration into ink-equipment-application bundles, geographic expansion into high-growth Asia Pacific markets, and strategic licensing of proprietary ink formulations to accelerate adoption without direct capital deployment.

Key Developments

- In April 2026, ELEGOO showcased advanced 3D printing solutions and real-world applications, including dental, jewelry, and consumer products. The event RAPID + TCT 2026 highlighted how large-format and high-precision printing systems enable lightweight, customizable, and scalable production. These developments reinforce the growing role of printing technologies in functional and flexible component manufacturing.

- In November 2025, HP Inc. announced advancements in additive manufacturing that reduce production costs by up to ~20% while improving efficiency, making printed functional components more commercially viable. The introduction of high-reusability materials and scalable digital manufacturing networks supports sustainable, on-demand production, aligning closely with the evolving functional printing ecosystem.

Companies Covered in Functional Printing Market

- BASF

- HP Inc.

- Samsung Electronics

- DuPont de Nemours

- E Ink Holdings

- Molex

- Durst Group

- EFI

- Bobst Group

- Agfa-Gevaert Group

- Fujifilm Dimatix

- Xaar plc

- Mark Andy

- Nissha Co., Ltd.

- Others

Frequently Asked Questions

The global Functional Printing market is valued at US$ 32.30 Billion in 2026 and is projected to reach US$ 113.06 Billion by 2033, growing at a CAGR of 19.6% over the forecast period, driven by the need for cost-efficient, flexible, and scalable manufacturing in electronics, healthcare, and energy applications.

The growth is fueled by the shift toward printed electronics that reduces material waste and enables flexible designs. Government-driven demand for smart packaging and renewable energy is accelerating large-scale adoption.

Conductive Materials lead with over 36% share as they are essential for creating electrical pathways in all printed electronics applications, from sensors to solar cells. The growing need for lightweight and low-cost electronic components directly drives their demand, as no functional device can operate without reliable conductivity layers.

Asia Pacific dominates with more than 45% share, supported by strong electronics manufacturing, solar capacity, and policy incentives. The region’s integrated supply chains and investments drive rapid expansion.

The opportunities lie in printed biosensors for healthcare and smart textiles, driven by cost advantages and rising demand for decentralized solutions.

The leading companies in the Functional Printing market include HP Inc., BASF, DuPont de Nemours, Fujifilm Dimatix, Agfa-Gevaert Group, Xaar plc, E Ink Holdings, Samsung Electronics, Heraeus Group, and Sun Chemical Corporation, among others.