- Semiconductor Materials & Components

- Flip Chip Technology Market

Flip Chip Technology Market Size, Share, and Growth Forecast 2026–2033

Flip Chip Technology Market by Bumping Technology (Solder Bump, Copper Pillar Bump, Micro-bump, Gold Bump, Others), Integration Level (2D IC, 2.5D IC, 3D IC), Device Type (Memory, Optoelectronics, Analog & Mixed Signal, CPU, SoC, GPU, Others), Packaging Type, Industry, and Regional Analysis, 2026–2033

Global Flip Chip Technology Market Size and Trend Analysis

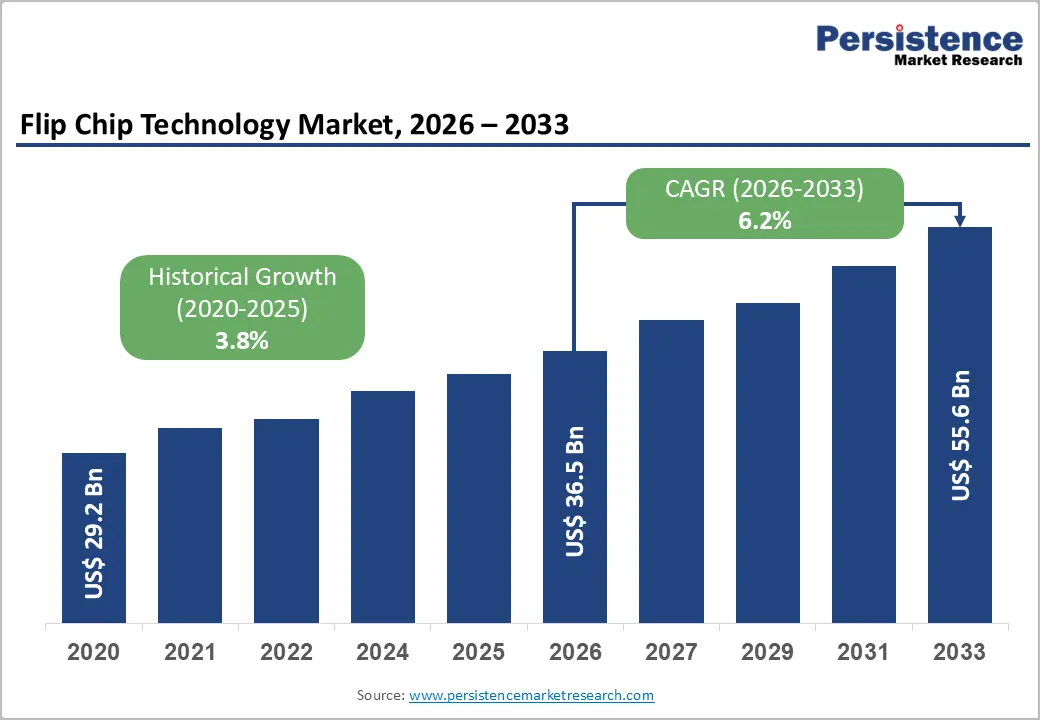

The global flip chip technology market size is expected to be valued at US$ 36.5 billion in 2026 and is projected to reach US$ 55.6 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by the surge in artificial intelligence (AI) and high-performance computing (HPC) workloads, which demand advanced semiconductor packaging solutions offering higher I/O density, lower power consumption, and superior thermal management. Flip chip technology, including copper pillar and micro-bump interconnects, has emerged as the packaging architecture of choice for leading-edge chiplets, GPUs, and SoC designs. The proliferation of 5G infrastructure, the electrification of automobiles, and the miniaturization of consumer electronics further reinforce multi-sector demand.

Key Industry Highlights:

- Leading Bumping Technology: Copper Pillar Bump dominates the market with over 40% share in 2026, valued at more than US$ 14.6 Bn, driven by its superior electrical performance, fine-pitch interconnect capability, and high thermal reliability required for advanced AI, HPC, and mobile chip designs.

- Leading Integration Level: 2D IC holds over 52% market share in 2026, valued at more than US$ 19 Bn, due to its cost-effectiveness, mature manufacturing ecosystem, and continued dominance in mainstream consumer and industrial applications.

- Fast-Growing Integration Level: 3D IC is the fastest-growing segment, driven by increasing demand for ultra-high bandwidth, lower latency, and compact chip architectures in AI, data centers, and advanced computing workloads.

- Leading Device Type: SoC (System-on-Chip) leads with over 25% share in 2026, valued at more than US$ 9.1 Bn, supported by widespread adoption in smartphones, IoT devices, and embedded systems due to its high integration and energy efficiency.

- Leading Packaging Type: FC BGA (Flip Chip Ball Grid Array) dominates with over 43% share in 2026, valued at more than US$ 15.7 Bn, driven by its high I/O density, thermal efficiency, and suitability for servers, networking, and high-performance processors.

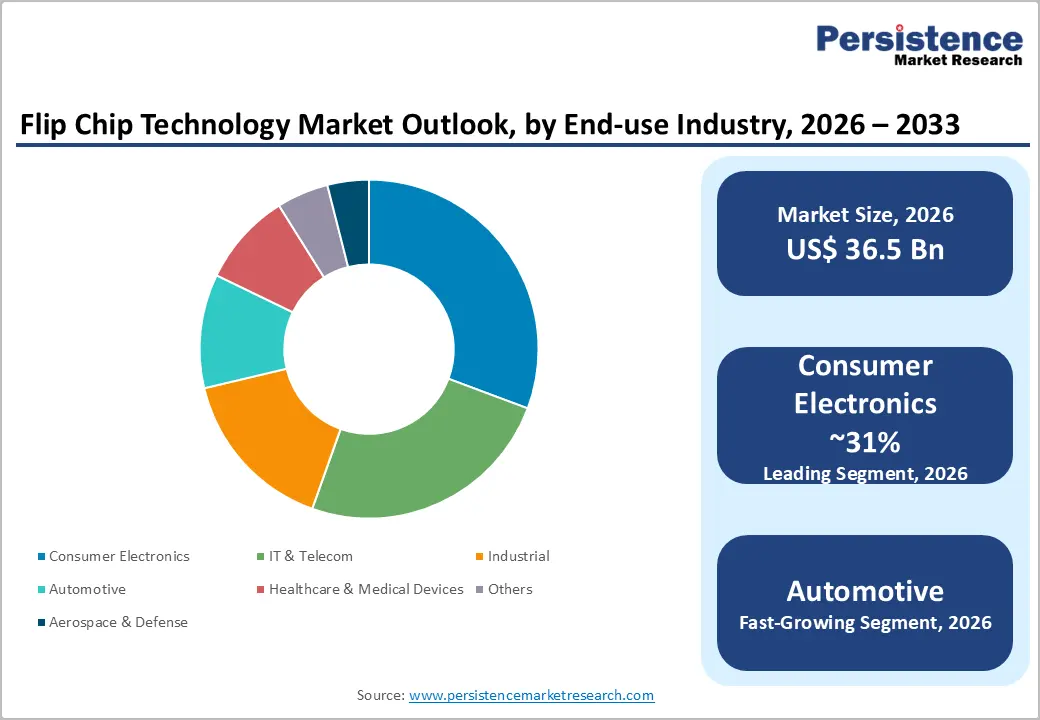

- Leading Industry: Consumer Electronics holds over 31% market share in 2026, valued at more than US$ 11.3 Bn, driven by strong demand for smartphones, laptops, tablets, and wearable devices requiring compact, high-performance chip packaging.

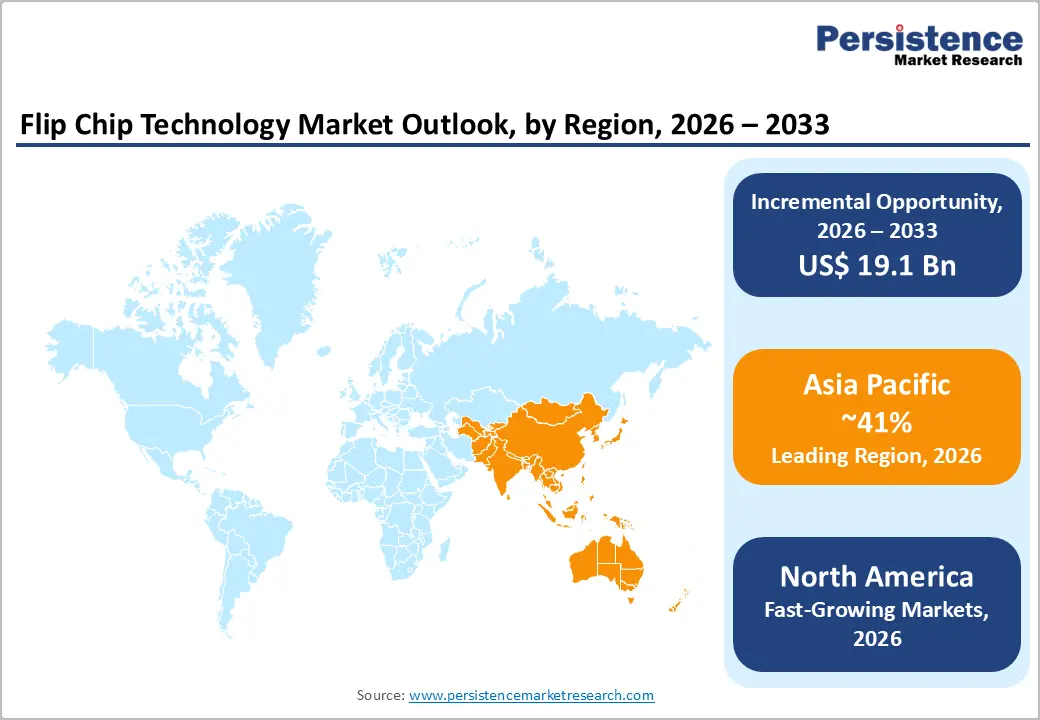

- Leading Region: Asia Pacific dominates with over 41% market share in 2026, valued at US$ 15 Bn, supported by strong semiconductor manufacturing ecosystems in China, Taiwan, South Korea, and Japan, along with cost-efficient OSAT infrastructure.

Market Dynamics

Drivers - Accelerating AI and High-Performance Computing Demand

The exponential growth of artificial intelligence applications encompassing large language models, generative AI, and neural network inference is placing unprecedented demands on semiconductor packaging technologies. Data center operators and hyperscalers are deploying billions of dollars in AI accelerator infrastructure, and flip chip packaging is at the heart of this transformation. Taiwan Semiconductor Manufacturing Company (TSMC) has been aggressively expanding its Chip-on-Wafer-on-Substrate (CoWoS) advanced packaging capacity, increasing from approximately 35,000 wafers per month in late 2024.

Driven by surging demand for AI and high-performance computing applications, the company is projected to scale this capacity to approximately 90,000–130,000 wafers per month by 2026, signaling the scale of investment required. The convergence of chiplet architectures with heterogeneous integration directly elevates demand for fine-pitch flip chip solutions across GPU, CPU, and custom AI silicon designs.

Expansion of 5G and IoT Ecosystems

5G base stations require radio frequency (RF) and millimeter-wave chips manufactured with precise flip chip interconnects to meet exacting signal-integrity and power-efficiency standards. The global number of smartphone users surpassed 5 billion, and smartphones rely extensively on flip chip-packaged processors, baseband chips, and power management ICs. IoT device proliferation spanning industrial sensors, wearables, and smart home devices drives demand for compact, energy-efficient flip chip packages. The combination of 5G rollouts and IoT expansion across North America, Europe, and the Asia Pacific provides sustained, long-horizon demand for flip chip solutions.

Restraints - High Manufacturing Complexity and Elevated Production Costs

The wafer bumping process involving electroplating, photolithography, and underfill dispensing requires specialized equipment and tightly controlled process parameters, increasing capital expenditure requirements for new entrants. The high cost of flip chip substrates, underfill materials, and precision assembly tooling contributes to a price premium over conventional wire-bond packages.

The miniaturization trend is intensifying the complexity of fine-pitch bumping below 40 µm, demanding advanced plating chemistries and inspection systems. For original equipment manufacturers in consumer and industrial electronics, the additional cost layers associated with flip chip packaging can pose a significant barrier to adoption, moderating the pace of technology transitions in price-sensitive end markets.

Thermal and Reliability Challenges from Differential Thermal Expansion

Flip chip assemblies face inherent reliability risks arising from the coefficient of thermal expansion (CTE) mismatch between the silicon die and organic substrate materials. Repeated thermal cycling, common in automotive, aerospace, and industrial applications, induces mechanical stress at the bump interconnects, leading to solder fatigue and potential joint failure. Studies have demonstrated that while eutectic Sn-Bi solder alloys extend thermal-cycling life, their brittleness limits use in high-stress environments.

RoHS compliance mandates have accelerated the adoption of SnAgCu (SAC) lead-free solders, yet differential thermal expansion continues to cause warpage and head-on-pillow defects during reflow, reducing assembly yields. Addressing these reliability concerns requires expensive underfill materials and process optimization, adding time and cost to product qualification cycles, especially in stringent automotive and defense applications.

Opportunities - Heterogeneous Integration and 3D IC Packaging for AI Accelerators

The transition from monolithic die designs to heterogeneous integration, where multiple chiplets combining logic, memory, and I/O are assembled on a common substrate, creates the most transformative opportunity. TSMC's announcement in March 2025 of an expanded US$ 165 billion investment in the United States, encompassing three new fabrication plants and two advanced packaging facilities, underscores the industrial commitment to next-generation flip chip packaging infrastructure.

The development of 3D IC and 2.5D IC packaging, leveraging through silicon vias (TSVs) and silicon interposers, is forecast to grow at an accelerating rate as leading AI chip companies, including NVIDIA and AMD, scale their chiplet-based product portfolios. Companies offering copper pillar and micro-bump bumping capabilities for sub-10 µm pitches will be positioned at the highest-value segment of the packaging supply chain, capturing premium margins from AI and HPC semiconductor customers.

Automotive Electronics, Electrification, and ADAS Proliferation

The rapid electrification of the global automotive fleet and the growing deployment of Advanced Driver Assistance Systems (ADAS) represent a significant growth vector. Global electric vehicle (EV) sales exceeded 20 million units in 2025 and are expected to maintain strong growth trajectories in the years ahead, driving demand for power electronics, radar sensors, LiDAR modules, and domain control units that utilize flip chip packaging for its superior thermal and electrical performance.

Samsung Electro-Mechanics has developed a new FC-BGA specifically targeting high-performance autonomous driving applications, capable of accommodating over 10,000 bumps in an area comparable to a passport photograph. As automotive-grade qualification standards AEC-Q100 become baseline requirements, flip chip manufacturers investing in robust process controls and reliability testing are well-positioned to capture this fast-growing, high-value end market.

Category-wise Analysis

Bumping Technology Insights

Copper pillar bump is dominant, capturing more than 40% share in 2026 with a value exceeding US$ 14.6 Bn, due to its ability to support higher electrical performance and fine-pitch interconnections required in advanced semiconductor nodes. It provides better current-carrying capability compared to traditional solder bumps, making it suitable for high-performance chips. Its superior thermal and mechanical reliability is critical for devices operating under high power density. It also supports miniaturization trends in mobile and computing devices. Increasing demand for high-speed and low-latency chip communication further strengthens its adoption.

Micro-bumps are expected to experience a rapid growth due to the rising demand for ultra-dense interconnects in advanced packaging architectures. They are essential for 3D stacking and high-bandwidth memory integration. The push toward heterogeneous integration in AI and HPC systems increases their relevance. Their small form factor enables higher I/O density and improved signal performance. Growing need for compact, power-efficient electronics further accelerates their adoption.

Integration Level Insights

2D IC holds over 52% market share in 2026, with a value exceeding US$ 19 Bn, due to its cost-effectiveness and established manufacturing ecosystem. It remains widely used in mainstream semiconductor applications where complexity is moderate. The need for high yield and simpler design cycles supports its continued demand. Many consumer and industrial chips still rely on 2D integration for reliable performance. Its compatibility with legacy systems also sustains its widespread use.

3D IC is expected to grow at the fastest rate due to increasing demand for higher performance and bandwidth density. It enables vertical stacking of components, significantly reducing interconnect delays. This architecture is critical for AI, data centers, and advanced computing workloads. It also improves power efficiency by shortening signal paths. The growing need for compact yet powerful semiconductor solutions drive its rapid adoption.

Device Type Insights

SoC commands the largest market share at over 25% in 2026, with a value exceeding US$ 9.1 Bn, due to its ability to integrate multiple functions, processing, memory, and connectivity on a single chip. This integration reduces power consumption and overall device size. It is widely used in smartphones, IoT devices, and embedded systems. The demand for energy-efficient and high-performance computing solutions supports its dominance. SoC design also simplifies system architecture and reduces manufacturing complexity.

GPUs are expected to have a CAGR of 9.3% due to their critical role in AI, machine learning, and parallel processing workloads. Modern computing applications require massive computational power, which GPUs efficiently deliver. Their usage in gaming, data centers, and scientific computing continues to expand. The rise of generative AI and high-performance analytics further strengthens demand. GPUs are increasingly essential for handling data-intensive workloads.

Packaging Type Insights

FC BGA holds over 43% market share in 2026, with a value exceeding US$ 15.7 Bn, due to its ability to support high I/O density and strong thermal performance. It is essential for high-performance processors used in servers, networking, and computing systems. The flip chip architecture improves electrical efficiency and signal integrity. It also supports high power dissipation requirements in advanced chips. Its reliability in demanding environments ensures continued strong adoption.

FC SiP is expected to grow rapidly due to increasing demand for compact, multifunctional electronic modules. It enables integration of multiple components such as sensors, RF, and logic in a single package. This is particularly important for wearable devices and IoT applications. Its ability to reduce system size while improving performance is a key driver. The trend toward device miniaturization strongly supports its expansion.

Industry Analysis

Consumer Electronics holds over 31% market share in 2026, with a value exceeding US$ 11.3 Bn, due to strong demand for smartphones, laptops, tablets, and wearable devices. These products require compact, high-performance chips with low power consumption. Flip chip technology enables miniaturization while improving processing speed and efficiency. Rapid product refresh cycles in this industry further sustain demand. The focus on enhanced user experience and connectivity drives continuous innovation.

Automotive is expected to grow at the fastest rate due to increasing adoption of EVs, ADAS, and autonomous driving systems. These applications require highly reliable and thermally stable semiconductor packaging. Advanced driver systems depend on high-speed processing and real-time data handling. The shift toward electrification and smart mobility increases semiconductor intensity per vehicle. Safety, durability, and performance requirements make flip chip technology highly essential in this sector.

Regional Insights

North America Flip Chip Technology Market Trends and Insights

North America accounts for 30% of the global flip chip technology share in 2026, exceeding the value of US$ 11 billion due to strong demand for high-performance computing, AI hardware, and advanced semiconductor packaging. The region benefits from the rapid expansion of data centers, cloud infrastructure, and 5G deployment, all of which require high-density chip interconnect solutions.

Rise in adoption of miniaturized consumer electronics such as smartphones, wearables, and gaming devices is further accelerating demand for flip chip integration. In addition, investments in heterogeneous integration and advanced packaging technologies are strengthening regional capability. Government-backed initiatives to localize chip manufacturing are also boosting advanced packaging adoption.

The United States flip chip technology market is expected to reach over to US$ 9 Billion, driven by surging demand for AI accelerators, high-performance GPUs, and advanced automotive electronics. The growth is strongly supported by increasing semiconductor fabrication and packaging investments under domestic manufacturing incentive programs. The expansion of electric vehicles and autonomous driving systems is creating an additional need for high-reliability chip interconnect technologies. Rising complexity in chip architecture, especially in 3D ICs and system-in-package designs, is further pushing flip chip adoption.

Europe Flip Chip Technology Market Trends and Insights

Europe is expected to exceed the value over US$6.6 billion by 2026, due to the strong expansion of advanced semiconductor packaging and miniaturized electronics. The region’s increasing focus on electric vehicles, autonomous driving systems, and high-performance computing is accelerating the adoption of flip chip solutions for improved electrical performance and thermal efficiency. Growing investments in semiconductor manufacturing and R&D, particularly under EU chip initiatives, are further strengthening the ecosystem. Europe’s emphasis on energy-efficient and high-reliability electronic systems is supporting steady growth across key end-use industries.

Germany flip chip technology market is reaching over to US$ 1.6 billion value in 2026, underpinned by its strong automotive electronics base and leadership in industrial automation. The country’s dominance in electric vehicle production and advanced driver-assistance systems (ADAS) is significantly increasing the need for high-performance packaging technologies such as flip chips.

The United Kingdom Flip Chip Technology market value is expected to exceed over US$ 1.1 Billion by 2026, shaped by rapid growth in aerospace, defense electronics, and fintech-driven data infrastructure. The UK’s expanding focus on high-speed computing, cloud data centers, and next-generation communication networks is further driving adoption of advanced semiconductor packaging solutions.

Asia Pacific Flip Chip Technology Market Trends and Insights

Asia Pacific accounts for over 41% of market share in 2026, representing US$ 15 Billion, and is the fastest-growing region in the Flip Chip Technology market with a projected CAGR of 10.4% through 2033, due to presence of semiconductor manufacturing ecosystems in China, South Korea, Taiwan, and Japan, which collectively support large-scale advanced packaging demand. Increasing investments in consumer electronics production and automotive electronics integration are further strengthening regional demand. The region benefits from cost-efficient manufacturing capabilities, high-volume assembly lines, and proximity to leading OSAT providers, making it a global production hub.

China flip chip technology market is expected to surpass US$ 6.3 Billion value by 2026, driven by aggressive semiconductor self-sufficiency initiatives. The country is heavily investing in domestic chip packaging and advanced assembly capabilities to reduce reliance on imports. Increasing demand for AI processors and automotive electronics is reinforcing long-term market expansion.

South Korea flip chip technology market is expected to account for over US$ 2.7 Billion of the value in 2026, supported by its leadership in memory semiconductors and advanced chip packaging. Major players are focusing on high-density packaging solutions for DRAM, NAND, and logic chips used in next-generation devices. Strong export demand for smartphones, displays, and consumer electronics continues to fuel flip chip integration. The country is also investing heavily in HBM (High Bandwidth Memory) and AI chip packaging technologies.

India flip chip technology market is expected to grow rapidly due to expanding electronics manufacturing under initiatives like Make in India and the Production Linked Incentive (PLI) scheme. Rising domestic demand for smartphones, consumer electronics, and automotive electronics is driving packaging technology adoption. The country is increasingly attracting global semiconductor players for assembly, testing, and packaging operations. Growth in design-led manufacturing and increasing semiconductor R&D investments are strengthening the ecosystem.

Competitive Landscape

The global flip chip technology market exhibits a moderately consolidated structure at the leading-edge segment, where leading players dominate advanced packaging for AI and HPC applications, while the broader market remains fragmented across diverse end-user segments and packaging tiers. Key competitive strategies include aggressive capacity expansion and the formation of strategic partnerships along the supply chain.

Major differentiators include process node leadership, proprietary bump pitch capabilities, substrate technology, and qualification for automotive-grade applications. Emerging business models include foundry-led packaging services, OSAT (Outsourced Semiconductor Assembly and Test) consolidation, and the formation of ecosystem consortia for standardization of heterogeneous integration interfaces, reflecting the industry's shift toward collaborative development of next-generation flip chip architectures.

Key Developments:

- In March 2026: ASE is increasing its investments in advanced packaging capacity to meet surging demand driven by AI chips and high-performance computing. The company is expanding capabilities in technologies such as 2.5D and 3D integration to support complex chiplet-based architectures. This move reflects strong growth in advanced packaging requirements from AI and data center applications.

- In December 2025: TSMC is expanding its CoWoS advanced packaging capacity significantly to meet strong demand from AI chips and high-performance computing customers, particularly ASIC and GPU makers. The expansion also involves increased collaboration and capacity utilization across OSAT partners to address ongoing supply constraints in advanced semiconductor packaging.

Companies Covered in Flip Chip Technology Market

- Taiwan Semiconductor Manufacturing Company

- Intel Corporation

- Samsung Electronics

- United Microelectronics Corporation

- Texas Instruments

- SK Hynix

- Micron Technology

- GlobalFoundries

- Semiconductor Manufacturing International Corporation

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- Renesas Electronics

- Analog Devices

- Others

Frequently Asked Questions

The global flip chip technology market is valued at US$ 36.5 Billion in 2026 and is projected to reach US$ 55.6 Billion by 2033, growing at a CAGR of 6.2% over the forecast period, due to the increasing need for advanced semiconductor packaging to support high-performance computing and miniaturized electronic devices.

The growth is driven by rising demand for high-speed, high-density chip interconnects in AI, 5G, and consumer electronics. The need for improved thermal performance, reduced signal loss, and compact device architectures is further accelerating adoption of flip chip packaging.

2D IC segment holds the largest share over 52% in 2026, as it remains widely used in mainstream semiconductor packaging. Its dominance is supported by cost efficiency, mature manufacturing ecosystems, and strong demand from consumer electronics and automotive applications.

Asia Pacific leads with more than 41% share & US$ 15 Bn value in 2026, due to strong semiconductor manufacturing bases in countries like China, Taiwan, and South Korea. High concentration of OSAT providers and increasing chip production demand support regional dominance.

The key opportunity lies in advanced packaging for AI chips, HPC systems, and next-generation mobile devices. Growing investments in heterogeneous integration and chiplet architectures are creating new demand for high-performance flip chip solutions.

The leading companies in the Flip Chip Technology market include Taiwan Semiconductor Manufacturing Company, Intel Corporation, Samsung Electronics, United Microelectronics Corporation, Texas Instruments, SK Hynix, Micron Technology, among others.