- Semiconductor Materials & Components

- Advanced IC Substrates Market

Advanced IC Substrates Market Size, Share, and Growth Forecast, 2026 - 2033

Advanced IC Substrates Market by Substrate Type (Flip Chip Ball Grid Array (FCBGA) Substrates, Others), Technology (High‑Density Interconnect (HDI) Substrates, Others), Application, and Regional Analysis for 2026 - 2033

Advanced IC Substrates Market Size and Trends Analysis

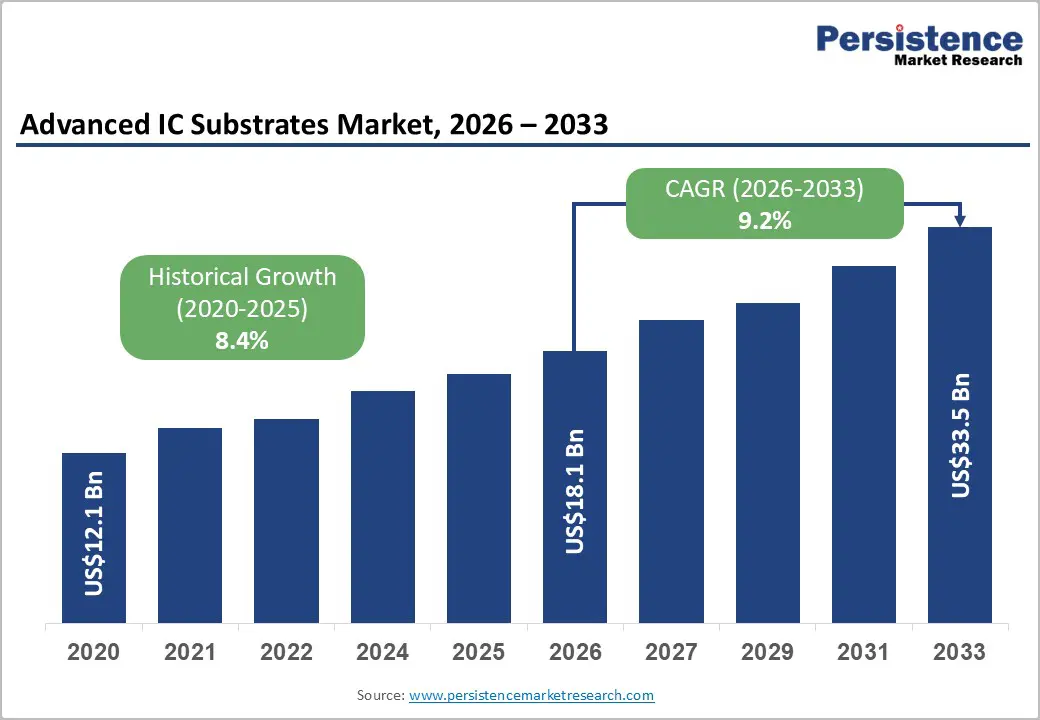

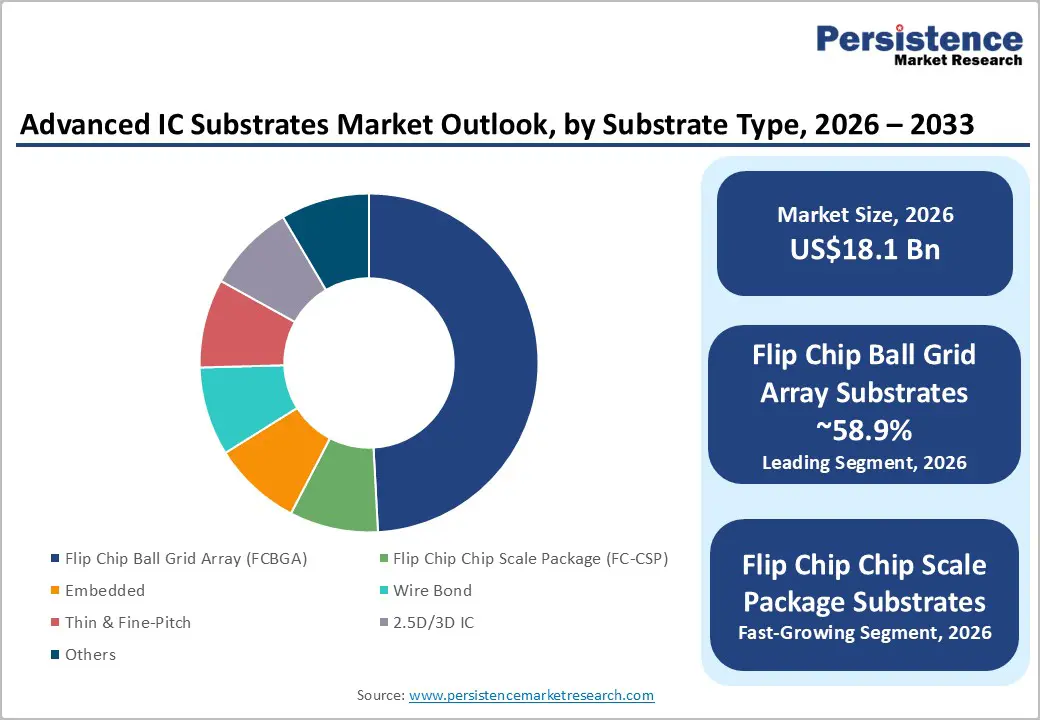

The global advanced IC substrates market size is likely to be valued at US$18.1 billion in 2026 and is expected to reach US$33.5 billion by 2033, growing at a CAGR of 9.2% between 2026 and 2033, driven by the increasing adoption of artificial intelligence (AI) accelerators, high-bandwidth memory (HBM) architectures, chiplet-based processors, and advanced 2.5D/3D semiconductor packaging technologies. These developments are increasing the demand for substrates capable of supporting higher routing density, thermal stability, and electrical performance.

Government-backed semiconductor initiatives in the U.S., Europe, India, Japan, and South Korea are also strengthening domestic packaging and substrate ecosystems. Growth is further supported by rising demand from automotive electronics, 5G infrastructure, cloud computing, and high-performance computing applications.

Key Industry Highlights:

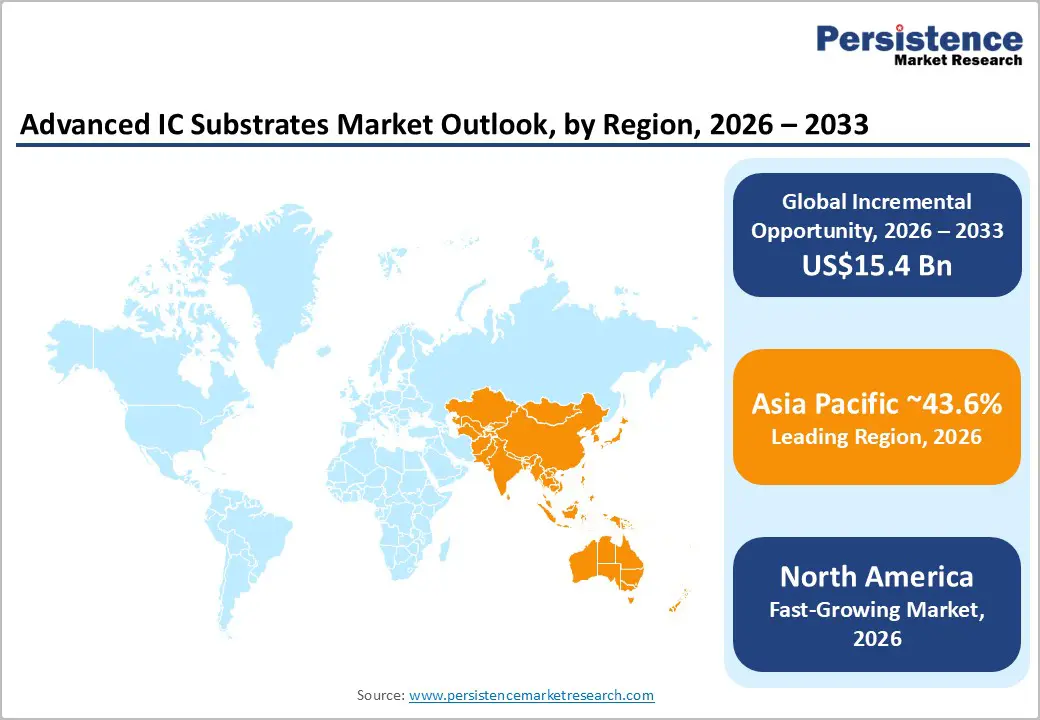

- Leading Region: Asia Pacific is projected to dominate the market with an anticipated 43.6% market share in 2026, supported by strong semiconductor manufacturing ecosystems in Taiwan, Japan, South Korea, and China.

- Fastest-growing Region: North America is projected to register the fastest growth during the forecast period, driven by rising AI infrastructure investments, semiconductor localization programs, and advanced packaging expansion across the U.S.

- Dominant Substrate Type: Flip Chip Ball Grid Array (FCBGA) substrates are anticipated to lead the market with an anticipated over 58.9% market share in 2026, due to strong adoption in AI accelerators, GPUs, CPUs, networking processors, and high-performance computing applications.

- Leading Technology: High-Density Interconnect (HDI) substrates are estimated to account for 47.3% the market share in 2026, supported by widespread usage across smartphones, tablets, networking equipment, and compact high-performance electronic devices.

DRO Analysis

Driver - Rising AI and High-Performance Computing Demand Accelerating Advanced Packaging Adoption

The rapid commercialization of AI infrastructure, cloud computing, and high-performance computing (HPC) platforms is significantly increasing demand for advanced IC substrates. Semiconductor companies are transitioning toward chiplet architectures and advanced packaging technologies such as CoWoS, 2.5D integration, and 3D stacking to improve computing efficiency and bandwidth performance. These architectures require substrates with finer line-and-space capabilities, higher layer counts, and superior thermal management characteristics.

The growth of AI servers and accelerators is directly impacting substrate demand. Advanced processors used in AI training and inference require larger substrate sizes and more complex interconnect structures compared with conventional processors. Semiconductor packaging technologies are also becoming increasingly dependent on ABF-based build-up substrates to support higher I/O density and signal integrity requirements. As data-center operators continue expanding AI infrastructure investments, substrate suppliers are increasing production capacity and investing in next-generation substrate technologies capable of supporting ultra-high-density packaging environments.

Expansion of 5G, EVs, and Industrial Digitalization Broadening Application Scope

The continued expansion of 5G connectivity, electric vehicles (EVs), industrial automation, and edge computing is broadening the demand base for advanced IC substrates beyond consumer electronics and data centers. The increasing deployment of RF modules, ADAS systems, radar sensors, power management devices, and automotive processors is creating sustained demand for high-reliability substrates with low-loss and fine-pitch characteristics.

The automotive industry is becoming an important growth engine for the market as EVs and autonomous driving systems require significantly higher semiconductor content per vehicle. Similarly, industrial automation and smart manufacturing initiatives are increasing the use of advanced processors, networking devices, and industrial IoT systems. These applications require substrates capable of operating under demanding thermal and environmental conditions. As electronic systems become more compact and functionally integrated, manufacturers are prioritizing advanced substrate technologies that can support miniaturization while maintaining long-term reliability and performance stability.

Restraint - Manufacturing Complexity and Supply Chain Concentration Limiting Capacity Expansion

One of the major restraints affecting the advanced IC substrates market is the high manufacturing complexity associated with ultra-fine-pitch substrate production. Advanced AI and HPC applications require line-and-space geometries below 10 micrometers, creating significant process challenges related to yield management, warpage control, material reliability, and thermal performance.

The market also remains highly concentrated geographically, particularly in Taiwan, Japan, and South Korea, where a limited number of suppliers possess the technological capability to manufacture advanced substrates at a commercial scale. This concentration increases supply chain vulnerability and creates risks related to geopolitical uncertainty, capacity bottlenecks, and long lead times. Semiconductor manufacturers continue to face packaging constraints during periods of strong AI demand, which can delay product launches and increase procurement costs. High capital expenditure requirements for advanced substrate facilities also create barriers for new market entrants.

Opportunity - Glass Core and Next-Generation Substrate Technologies Creating Long-Term Growth Potential

Glass core substrates and next-generation packaging materials are emerging as significant opportunities within the advanced IC substrates market. Semiconductor manufacturers are increasingly evaluating glass-based substrates because they offer superior dimensional stability, lower warpage, improved electrical performance, and better thermal management compared with conventional organic substrates.

As AI accelerators, networking processors, and high-performance computing chips continue increasing in complexity, substrate technologies capable of supporting ultra-large package sizes and higher interconnect density are expected to gain commercial importance. The transition toward panel-level packaging, embedded die technologies, and ultra-low-loss materials is also creating new growth avenues for substrate manufacturers. Companies capable of industrializing glass-core and ultra-fine-pitch substrate platforms are likely to secure strategic advantages in advanced AI and HPC supply chains over the next decade.

Regional Semiconductor Localization Opening New Investment Opportunities

Government-backed semiconductor localization programs across North America, Europe, India, and Southeast Asia are creating substantial opportunities for substrate manufacturers. Multiple countries are offering incentives for semiconductor packaging, substrate manufacturing, and advanced assembly operations to reduce dependence on concentrated Asian supply chains.

The U.S. continues expanding domestic advanced packaging capabilities through CHIPS Act funding, while Europe is strengthening regional semiconductor manufacturing under the European Chips Act. India’s semiconductor incentive programs are encouraging OSAT and packaging investments, and ASEAN countries are positioning themselves as alternative semiconductor manufacturing hubs. These initiatives are increasing opportunities for substrate suppliers to establish localized production facilities, secure long-term supply agreements, and strengthen relationships with semiconductor manufacturers seeking geographically diversified sourcing strategies.

Category-wise Analysis

Substrate Type Insights

Flip Chip Ball Grid Array (FCBGA) substrates are anticipated to account for over 58.9% of the market share in 2026, maintaining leadership due to their extensive use in CPUs, GPUs, AI accelerators, and high-performance networking processors. These substrates support high pin counts, improved thermal dissipation, and superior signal integrity required for AI servers and cloud computing systems. Companies such as Intel, AMD, and NVIDIA increasingly rely on advanced FCBGA substrates for AI GPUs and data-center processors, while suppliers including Ibiden and Shinko continue expanding large-body FCBGA production capacity to support growing HPC demand.

Flip Chip Chip Scale Package (FC-CSP) substrates are anticipated to register the fastest CAGR of over 15% during the forecast period, driven by rising adoption in smartphones, wearables, tablets, RF modules, and compact consumer electronics. The segment benefits from increasing demand for thinner and lighter devices requiring high-density interconnections within smaller package footprints. Apple, Qualcomm, and MediaTek increasingly utilize FC-CSP packaging in advanced mobile processors and 5G chipsets, while suppliers such as LG Innotek are investing in fine-pitch and copper-post packaging technologies to improve miniaturization and electrical performance.

Technology Insights

High-Density Interconnect (HDI) substrates are anticipated to hold the largest share of the market in 2026, supported by their widespread adoption across smartphones, networking devices, tablets, and compact electronic systems. HDI technology enables finer routing, smaller vias, and higher interconnect density, making it critical for miniaturized semiconductor packaging. Leading electronics manufacturers such as Samsung Electronics and Apple continue integrating HDI substrates into premium mobile and computing devices, while networking equipment providers increasingly adopt HDI-based solutions for compact, high-performance communication systems.

Build-up and multilayer organic substrates are anticipated to witness the fastest growth during the forecast period, driven by increasing demand from AI accelerators, cloud data centers, advanced CPUs, and networking infrastructure. These substrates provide higher routing density and enhanced electrical performance required for chiplet architectures and heterogeneous integration platforms. Companies including NVIDIA and TSMC are accelerating the adoption of advanced build-up substrate technologies for AI-focused CoWoS and 2.5D packaging applications. Substrate manufacturers are also investing in low-loss materials and ultra-fine-pitch technologies to address evolving AI and HPC packaging requirements.

Regional Insights

North America Advanced IC Substrates Market Trends

North America is anticipated to emerge as the fastest-growing regional market for advanced IC substrates during the forecast period, supported by rising investments in AI infrastructure, advanced semiconductor packaging, and domestic supply chain localization. The region is witnessing increasing demand for high-performance substrates used in AI accelerators, cloud computing processors, networking equipment, aerospace electronics, and advanced defense systems.

U.S. Advanced IC Substrates Market Trends

The U.S. represents the largest market in North America due to its strong semiconductor design ecosystem, hyperscale data-center expansion, and federal semiconductor incentives. AI infrastructure investments by major cloud service providers are increasing demand for advanced packaging technologies and high-density substrates used in GPUs, CPUs, and AI accelerators. States such as Arizona, Texas, and California are becoming major semiconductor packaging hubs as companies expand domestic assembly, packaging, and testing operations. The country also benefits from the presence of leading semiconductor companies, including NVIDIA, AMD, Intel, Qualcomm, and Broadcom, all of which rely heavily on advanced substrate technologies.

Canada Advanced IC Substrates Market Trends

Canada is gradually strengthening its position within the semiconductor ecosystem through investments in AI research, photonics, and advanced electronics manufacturing. Government support for innovation and semiconductor R&D is encouraging collaboration between research institutions and electronics manufacturers. Demand for advanced IC substrates in Canada is increasing across telecommunications, industrial automation, and aerospace applications.

North America benefits from a strong innovation ecosystem comprising semiconductor designers, AI infrastructure developers, defense contractors, and cloud computing companies. However, the region still faces challenges related to workforce availability, packaging ecosystem maturity, and manufacturing scale compared with Asia Pacific.

Europe Advanced IC Substrates Market Trends

Europe is strengthening its role in the advanced IC substrates market through increasing investments in automotive electronics, industrial automation, aerospace technologies, and semiconductor localization initiatives.

Germany Advanced IC Substrates Market Trends

Germany remains the leading market in Europe due to its dominant automotive manufacturing industry and advanced industrial automation sector. The country is witnessing increasing semiconductor demand from EV powertrains, ADAS platforms, autonomous driving systems, and factory automation technologies. German automotive manufacturers continue integrating high-performance semiconductor systems into next-generation electric and connected vehicles, driving demand for advanced IC substrates.

U.K. Advanced IC Substrates Market Trends

The U.K. is expanding semiconductor innovation capabilities through investments in compound semiconductors, aerospace electronics, telecommunications infrastructure, and AI computing technologies. Growing demand for advanced networking systems, defense electronics, and industrial AI applications is supporting substrate demand growth across the country.

Asia Pacific Advanced IC Substrates Market Trends

Asia Pacific remains the leading regional market for advanced IC substrates, accounting for approximately 43.6% of market share in 2026. The region benefits from its highly integrated semiconductor manufacturing ecosystem, mature packaging infrastructure, advanced materials supply chain, and concentration of leading substrate manufacturers.

Taiwan Advanced IC Substrates Market Trends

Taiwan represents the most important advanced IC substrate manufacturing hub globally due to its leadership in semiconductor foundry services and advanced packaging technologies. The country is home to major substrate suppliers and semiconductor manufacturers supporting AI accelerators, HPC processors, and advanced networking devices. Rising AI server demand is significantly increasing substrate production capacity and advanced packaging investments across Taiwan.

Japan Advanced IC Substrates Market Trends

Japan maintains a strong competitive position in substrate materials, precision manufacturing, ceramic packaging technologies, and semiconductor process equipment. Japanese companies are heavily involved in high-end substrate production used in AI, automotive, and industrial semiconductor applications. The country also plays a critical role in supplying advanced materials and manufacturing technologies for global semiconductor packaging ecosystems.

China Advanced IC Substrates Market Trends

China remains one of the world’s largest semiconductor consumption and electronics manufacturing markets despite ongoing supply chain restructuring efforts. The country continues investing heavily in domestic semiconductor production, advanced packaging, and electronics manufacturing capabilities. Demand for advanced substrates is increasing across AI servers, consumer electronics, EVs, and telecommunications infrastructure.

Asia Pacific benefits from workforce specialization, mature semiconductor infrastructure, close integration between fabs and packaging facilities, and strong government support for semiconductor manufacturing. These advantages are expected to maintain the region’s leadership position in the advanced IC substrates market throughout the forecast period.

Competitive Landscape

The global advanced IC substrates market is moderately concentrated at the high-performance end while remaining fragmented across broader commercial applications. Leading substrate suppliers in Taiwan, Japan, and South Korea dominate ultra-fine-pitch and AI-grade substrate manufacturing capabilities due to their technological expertise, manufacturing scale, and long-standing semiconductor customer relationships.

Leading market participants are prioritizing advanced packaging innovation, substrate miniaturization, regional manufacturing expansion, and AI-focused technology development. Companies are increasing investments in build-up substrate technologies, glass-core research, low-loss materials, and advanced thermal management solutions. Strategic partnerships with semiconductor manufacturers and OSAT providers remain critical for securing long-term supply agreements and technology qualification opportunities.

Key Industry Developments:

- In April 2026, AT&S Austria Technologie & Systemtechnik AG announced advancements in glass-core substrate technology designed for artificial intelligence, high-performance computing, high-speed communication, and photonics applications, while expanding manufacturing integration capabilities at its Leoben facility.

- In December 2025, Rapidus Corporation announced ongoing development of panel-level packaging on glass substrates for next-generation AI and HPC processors, focusing on large-format glass-panel substrate technologies to support advanced multi-chiplet semiconductor architectures.

Companies Covered in Advanced IC Substrates Market

- Ibiden Co., Ltd.

- Unimicron Technology Corp.

- Shinko Electric Industries Co., Ltd.

- Samsung Electro-Mechanics

- Kinsus Interconnect Technology Corp.

- ASE Technology Holding Co., Ltd.

- AT&S Austria Technologie & Systemtechnik AG

- LG Innotek Co., Ltd.

- Daeduck Electronics Co., Ltd.

- Shennan Circuits Co., Ltd.

- Kyocera Corporation

- Nan Ya PCB Corporation

- Simmtech Co., Ltd.

- TOPPAN Holdings Inc.

- Zhen Ding Technology Holding Limited

- Taiwan Union Technology Corporation (TUC)

Frequently Asked Questions

The global Advanced IC Substrates Market is anticipated to be valued at US$18.1 billion in 2026.

The advanced IC substrates market is expected to reach approximately US$33.5 billion by 2033.

Key trends include increasing adoption of AI accelerators, chiplet architectures, 2.5D/3D semiconductor packaging, HBM integration, advanced build-up substrates, glass-core technologies, and rising demand from EVs, 5G infrastructure, and cloud data centers.

Flip Chip Ball Grid Array (FCBGA) substrates represent the leading segment, accounting for over 58.9% market share due to strong demand from AI servers, GPUs, CPUs, and high-performance computing applications.

The advanced IC substrates market is projected to grow at a CAGR of 9.2% between 2026 and 2033.

Major companies include Ibiden Co., Ltd., Unimicron Technology Corp., Shinko Electric Industries Co., Ltd., Samsung Electro-Mechanics, and ASE Technology Holding.