- Semiconductor Materials & Components

- Discrete Semiconductor Market

Discrete Semiconductor Market Size, Share, and Growth Forecast, 2026 - 2033

Discrete Semiconductor Market by Device Type (Transistors, Diodes, Others), Technology (Silicon‑Based Devices, Gallium Nitride (GaN), Others), Application, Value Chain, and Regional Analysis for 2026 - 2033

Discrete Semiconductor Market Size and Trends Analysis

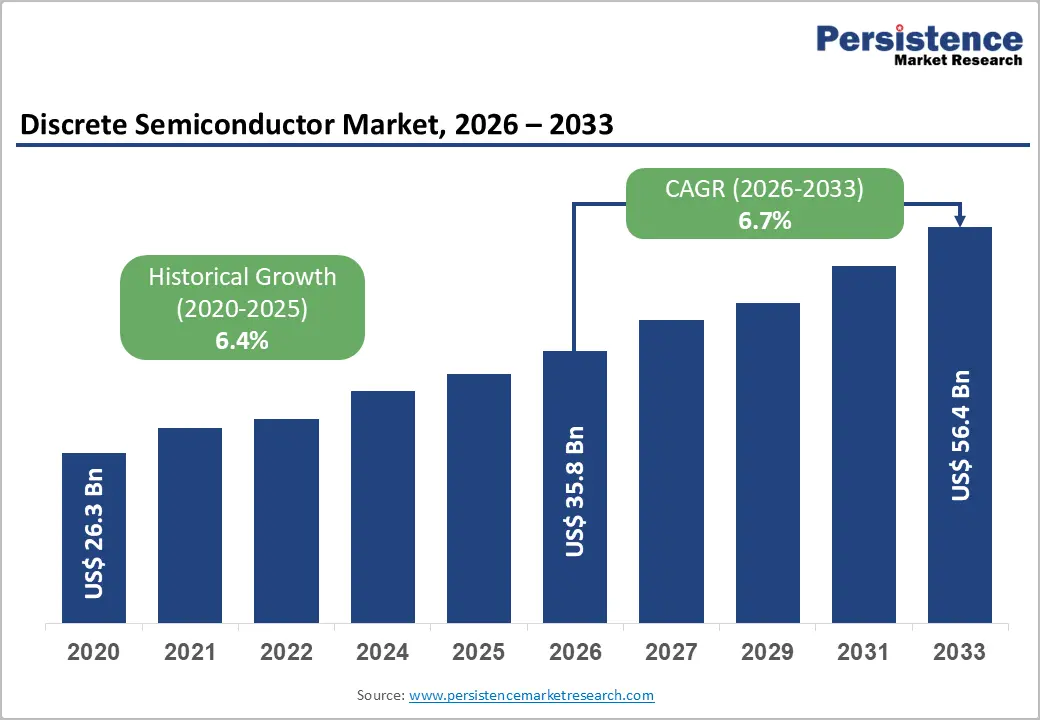

The global discrete semiconductor market size is likely to be valued at US$35.8 billion in 2026 and is expected to reach US$56.4 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033, driven by increasing electrification across automotive systems, rising deployment of renewable energy infrastructure, and growing demand for power-efficient semiconductor architectures in industrial automation and consumer electronics.

Rapid adoption of electric vehicles (EVs), 5G telecommunications infrastructure, and data-center power management systems continues to accelerate demand for high-performance discrete devices such as MOSFETs, IGBTs, and silicon carbide (SiC) components.

Key Industry Highlights:

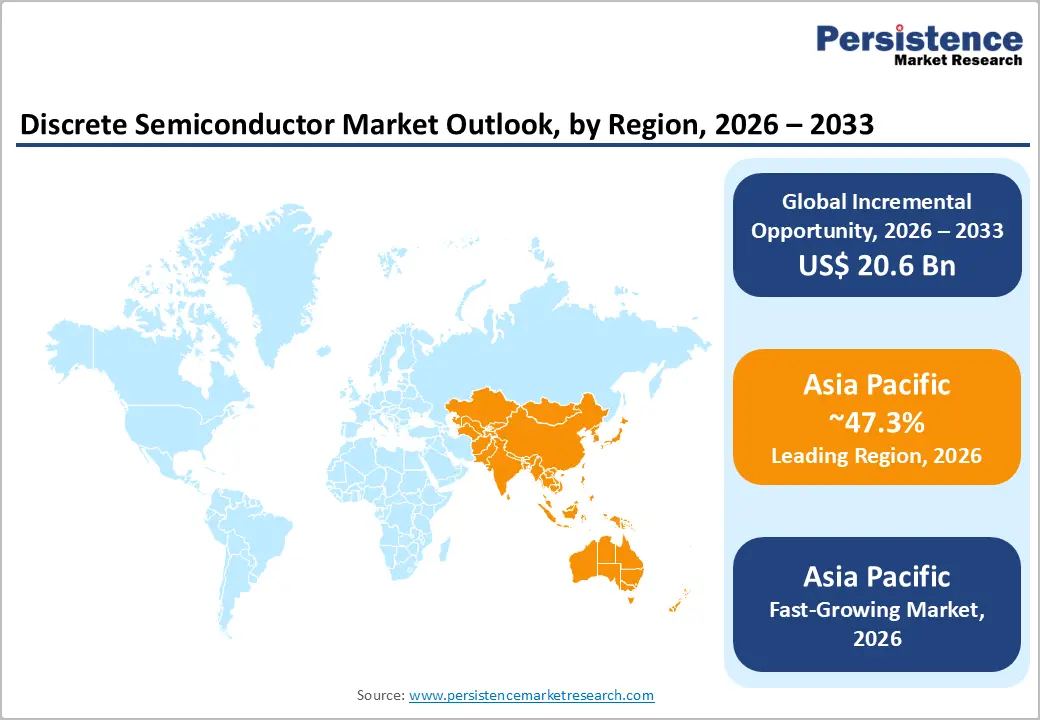

- Leading Region: Asia Pacific is projected to account for approximately 47.3% of the market share, supported by strong electronics manufacturing ecosystems across China, Japan, South Korea, Taiwan, and India.

- Fastest-growing Region: Asia Pacific is projected to expand at an estimated 8-9% CAGR during the forecast period, driven by EV production growth, renewable energy deployment, semiconductor localization initiatives, and increasing industrial automation investments.

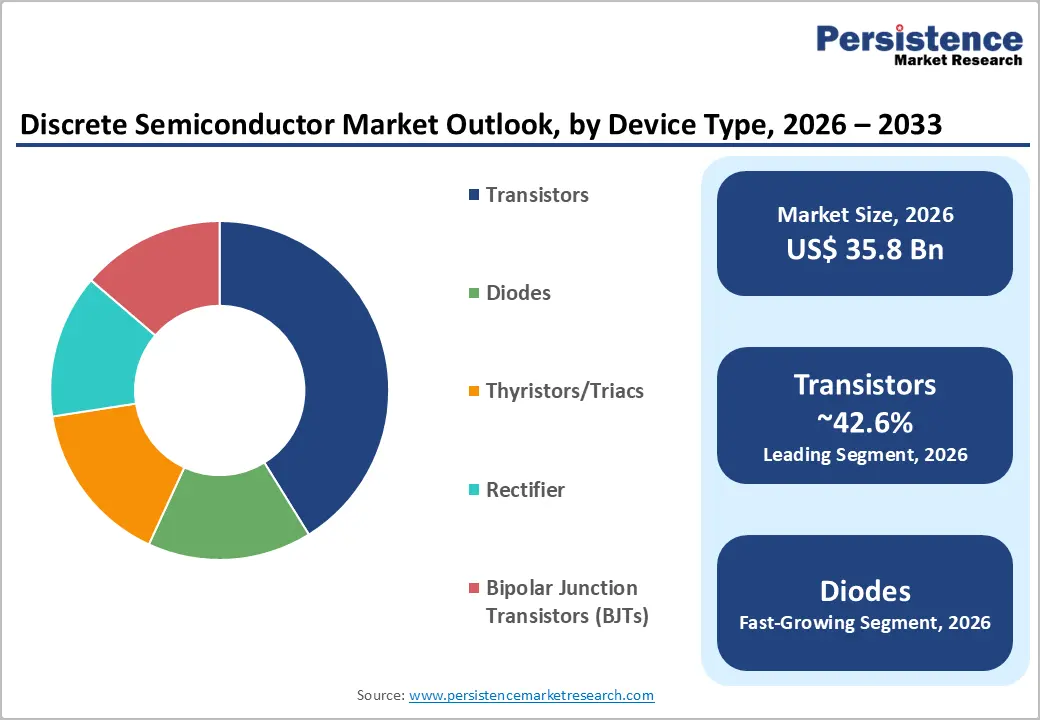

- Dominant Device Type: Transistors are anticipated to account for approximately 42.6% of market share due to widespread adoption across EVs, industrial automation systems, telecommunications infrastructure, and renewable energy applications.

- Leading Technology: Silicon-based devices are estimated to lead with more than 78.8% market share, supported by mature manufacturing infrastructure, cost efficiency, and broad deployment across automotive, industrial, and consumer electronics sectors.

DRO Analysis

Driver - Growing Electrification in Automotive and EV Powertrain Systems

The transition toward electric mobility remains one of the strongest growth drivers for the discrete semiconductor market. Power discrete devices are fundamental in EV traction inverters, battery management systems (BMS), onboard chargers, ADAS modules, DC-DC converters, and 48-V architectures. According to the International Energy Agency (IEA), global electric vehicle sales surpassed 17 million units in 2025, representing sustained double-digit annual growth. This increase directly drives demand for high-voltage MOSFETs, IGBTs, and SiC-based power devices.

Automotive OEMs increasingly require semiconductors capable of handling higher switching frequencies, improved thermal management, and lower energy losses. SiC MOSFET deployment in EV drivetrains significantly improves efficiency and extends driving range, making it strategically important for premium and mass-market EV platforms. Regulatory frameworks such as the European Union’s CO2 emission standards, China’s New Energy Vehicle (NEV) mandates, and U.S. Inflation Reduction Act incentives continue accelerating vehicle electrification investments.

The business impact is substantial because automotive semiconductor content per vehicle is increasing rapidly. Traditional internal combustion vehicles generally contain lower-value power discretes compared with battery electric vehicles, where semiconductor intensity can be two to three times higher.

Expansion of Renewable Energy and Industrial Power Infrastructure

Global investment in renewable energy generation and industrial electrification is increasing demand for high-power discrete semiconductor solutions. The International Renewable Energy Agency (IRENA) reported record additions in solar and wind capacity installations globally, creating strong requirements for power conversion technologies used in solar inverters, energy storage systems, industrial drives, and smart grids. Discrete semiconductors are essential for efficient power conversion and voltage regulation in renewable energy systems. SiC and GaN devices are increasingly adopted because they enable lower switching losses, reduced heat generation, and smaller system footprints. Industrial automation systems also rely heavily on discrete components for motor control, robotics, programmable logic controllers, and factory power systems.

Government initiatives promoting energy efficiency are supporting adoption. For example, the U.S. Department of Energy and the European Commission have implemented industrial efficiency targets encouraging modernization of power electronics infrastructure. Manufacturing sectors in China, Germany, Japan, and South Korea continue expanding smart factory investments, increasing demand for industrial-grade semiconductors with enhanced durability and thermal performance. The market impact extends beyond utilities and manufacturing. Data centers, telecom towers, and edge computing infrastructure require efficient power management systems to reduce operational energy costs. This creates sustained demand for advanced discrete devices across multiple end-use industries.

Restraint - Supply Chain Volatility and High Capital Intensity of Advanced Semiconductor Manufacturing

The discrete semiconductor market remains vulnerable to semiconductor supply-chain disruptions, raw material shortages, and escalating fabrication costs. Manufacturing advanced power semiconductors requires highly specialized fabrication facilities, epitaxy processes, wafer technologies, and packaging systems. SiC wafer production costs remain significantly higher than conventional silicon-based manufacturing due to limited substrate availability and lower production yields.

Geopolitical tensions involving semiconductor trade restrictions between the U.S. and China continue influencing global sourcing strategies and equipment procurement. Lead-time volatility for semiconductor-grade materials, including high-purity silicon wafers and gallium compounds, also affects production schedules. According to industry assessments from SEMI and Deloitte, semiconductor fabrication facilities require multibillion-dollar capital expenditures and extended commissioning timelines, creating barriers for new entrants.

Automotive and industrial customers increasingly demand supply-chain localization and dual sourcing strategies, forcing manufacturers to maintain higher inventory levels and diversify production footprints. These structural challenges can pressure operating margins, especially for mid-sized semiconductor suppliers competing against vertically integrated market leaders with stronger economies of scale.

Opportunity - Rapid Commercialization of Gallium Nitride (GaN) Power Devices

Gallium Nitride (GaN) technology presents a major opportunity for the discrete semiconductor market due to its superior switching efficiency, higher power density, and compact design characteristics. GaN devices are increasingly deployed in fast chargers, consumer electronics, telecom power systems, aerospace electronics, and electric mobility infrastructure. The consumer electronics sector has become an early commercialization platform for GaN technology. Smartphone and laptop manufacturers are adopting GaN-based fast chargers capable of delivering higher power output with smaller form factors. Telecom infrastructure providers are also deploying GaN RF devices in 5G base stations because of improved frequency performance and lower energy consumption.

Governments supporting next-generation communications and energy-efficient electronics indirectly strengthen GaN adoption. Semiconductor companies are increasing R&D investment to improve wafer scalability and reduce manufacturing costs. As production yields improve and packaging technologies mature, GaN devices are expected to penetrate industrial automation and EV charging applications more aggressively. This transition creates opportunities for both integrated device manufacturers (IDMs) and specialized power semiconductor firms.

Localization of Semiconductor Manufacturing and Strategic Government Incentives

National semiconductor policies are creating substantial opportunities for discrete semiconductor manufacturing expansion. Governments across the U.S., Europe, India, Japan, and South Korea are implementing semiconductor incentive programs aimed at reducing dependence on concentrated Asian supply chains.

The U.S. CHIPS and Science Act, the European Chips Act, and India’s Semiconductor Mission are encouraging investments in fabrication plants, packaging facilities, and semiconductor R&D ecosystems. These initiatives support long-term growth for discrete semiconductor manufacturing, especially in automotive and industrial applications where supply-chain security has become strategically important.

The opportunity extends beyond fabrication capacity. Semiconductor testing, advanced packaging, wafer processing, and substrate manufacturing are receiving increased investment attention, enabling broader value-chain expansion and regional ecosystem development.

Category-wise Analysis

Device Type Insights

Transistors are anticipated to account for 42.6% of the market share in 2026, due to strong demand across automotive electronics, industrial automation, telecommunications, and consumer electronics. MOSFETs and IGBTs are widely used in EV drivetrains, charging systems, renewable energy inverters, and data-center power management applications. Companies such as Infineon Technologies, ON Semiconductor, STMicroelectronics, and Toshiba continue expanding high-efficiency automotive-qualified transistor portfolios to support electrification and energy-efficiency trends.

Diodes are projected to be the fastest-growing segment, driven by increasing adoption in EV charging infrastructure, renewable energy systems, industrial electronics, and power supplies. Fast recovery diodes and Schottky diodes are gaining traction due to lower power losses and superior switching efficiency. Rising photovoltaic installations and expansion of advanced energy-management systems are further accelerating demand for high-performance rectifier solutions. Other important device categories include thyristors, triacs, BJTs, and RF discrete devices used in industrial control systems, lighting infrastructure, 5G networks, and aerospace communication equipment.

Technology Insights

Silicon-based discrete semiconductor devices are anticipated to account for 78.8% of market share in 2026, due to their cost efficiency, mature manufacturing ecosystem, and broad adoption across automotive, industrial, and consumer electronics applications. Silicon MOSFETs, diodes, and BJTs remain widely deployed in power supplies, appliances, industrial automation systems, and automotive electronics. Manufacturers continue improving silicon device efficiency through advanced packaging and thermal optimization technologies. Companies including Infineon Technologies, Vishay Intertechnology, and STMicroelectronics are expanding silicon-based power semiconductor portfolios to support mainstream industrial and automotive applications.

Gallium Nitride (GaN) devices are projected to be the fastest-growing technology segment, due to advantages including faster switching speeds, compact size, reduced energy loss, and superior thermal efficiency. Adoption is increasing rapidly in fast chargers, telecom infrastructure, aerospace electronics, and high-performance industrial systems. Companies such as Navitas Semiconductor and EPC are accelerating the commercialization of GaN-based power devices for next-generation energy-efficient applications. Meanwhile, Silicon Carbide (SiC) devices continue gaining traction in EV traction inverters and renewable energy systems because they improve battery efficiency and power density.

Regional Insights

North America Discrete Semiconductor Market Trends

North America represents a strategically important market for discrete semiconductors due to strong automotive innovation, advanced industrial infrastructure, and large-scale investment in semiconductor manufacturing localization.

U.S. Discrete Semiconductor Market Trends

The U.S. dominates the North American discrete semiconductor market due to strong demand from EV manufacturing, aerospace electronics, defense systems, renewable energy infrastructure, and hyperscale data centers. Government initiatives such as the CHIPS and Science Act are accelerating investments in semiconductor fabrication, packaging, and R&D activities to strengthen domestic supply-chain resilience.

Major semiconductor companies are expanding production of SiC and GaN power devices for EV platforms, charging systems, and AI infrastructure. States including Arizona, Texas, and New York continue attracting large-scale semiconductor fabrication investments, while Silicon Valley remains a global semiconductor design and innovation hub.

Canada Discrete Semiconductor Market Trends

Canada contributes to the regional market through semiconductor research, industrial electronics development, and advanced manufacturing technologies. The country benefits from strong academic research ecosystems and growing investments in AI infrastructure and clean energy systems.

Canadian industries are increasingly deploying power semiconductors across industrial automation, renewable energy, and telecommunications applications. Government support for advanced manufacturing and technology innovation is also strengthening semiconductor R&D capabilities.

Europe Discrete Semiconductor Market Trends

Europe remains a significant discrete semiconductor market supported by strong automotive manufacturing, industrial automation leadership, and energy transition initiatives.

Germany Discrete Semiconductor Market Trends

Germany remains the leading discrete semiconductor market in Europe due to its globally competitive automotive manufacturing and industrial automation sectors. Rising EV production is significantly increasing demand for IGBTs, MOSFETs, and SiC power devices used in traction inverters, charging infrastructure, and energy management systems.

German industrial manufacturers are also accelerating deployment of robotics, motion-control systems, and smart manufacturing technologies that require advanced power semiconductors. Government-backed semiconductor initiatives and the European Chips Act are further supporting investments in regional semiconductor manufacturing and R&D.

U.K. Discrete Semiconductor Market Trends

The U.K. maintains strong market positioning in semiconductor design, telecommunications infrastructure, and compound semiconductor technologies. Increasing adoption of GaN and RF semiconductor devices across telecom, aerospace, and defense applications is supporting market growth.

The country also benefits from advanced research capabilities and growing investments in semiconductor innovation, particularly in high-frequency communication systems and AI-driven industrial electronics.

France Discrete Semiconductor Market Trends

France is witnessing rising demand for discrete semiconductors across aerospace electronics, renewable energy systems, and industrial automation applications. The country’s aerospace and defense industries remain major consumers of high-performance semiconductor technologies.

French companies are also increasing investments in EV infrastructure, renewable energy deployment, and energy-efficient industrial systems, driving demand for power discretes and advanced semiconductor materials.

Asia Pacific Discrete Semiconductor Market Trends

Asia Pacific remains the leading and fastest-growing regional market for discrete semiconductors, accounting for approximately 47.3% of market share. The region is projected to expand at a regional CAGR of roughly 8.7% during the forecast period.

China Discrete Semiconductor Market Trends

China remains the dominant market within Asia Pacific due to its large-scale electronics manufacturing ecosystem and extensive demand across automotive, telecom, industrial, and consumer electronics sectors. Government-backed semiconductor self-sufficiency initiatives continue driving investments in local fabrication, advanced packaging, and semiconductor materials production.

The country is also expanding deployment of SiC and GaN devices across EVs, renewable energy systems, telecom infrastructure, and industrial automation platforms.

Japan Discrete Semiconductor Market Trends

Japan remains a major semiconductor market supported by leadership in automotive electronics, semiconductor materials, and industrial automation systems. Japanese manufacturers are key suppliers of power semiconductor technologies, semiconductor production equipment, and advanced industrial electronics.

Demand for SiC-based power devices is increasing across EVs, renewable energy systems, and factory automation applications. The country also continues investing in next-generation semiconductor research and advanced manufacturing technologies.

India Discrete Semiconductor Market Trends

India is emerging as one of the fastest-growing semiconductor markets due to rising electronics manufacturing, EV adoption, renewable energy investments, and government-backed semiconductor incentive programs. Initiatives such as the India Semiconductor Mission and PLI schemes are attracting international investments in semiconductor manufacturing and assembly operations.

Demand for discrete semiconductors is increasing across automotive electronics, industrial automation, telecom infrastructure, and consumer electronics applications.

Competitive Landscape

The global discrete semiconductor market remains moderately consolidated, with major global players collectively accounting for a significant portion of total revenue. Leading companies including Infineon Technologies, ON Semiconductor, STMicroelectronics, Toshiba, Mitsubishi Electric, and Vishay Intertechnology maintain strong positions across automotive, industrial, and consumer electronics applications.

Market leadership is largely determined by manufacturing scale, power semiconductor expertise, automotive qualification capabilities, and R&D investment intensity. While large integrated device manufacturers dominate high-volume production, specialized suppliers continue competing effectively in RF, microwave, and protection-device segments.

Leading semiconductor companies prioritize wide-bandgap technology innovation, automotive supply-chain partnerships, and regional manufacturing expansion. Strategic differentiation increasingly depends on vertical integration, energy-efficient semiconductor architectures, advanced packaging capabilities, and long-term OEM relationships. Companies are also investing aggressively in SiC substrate manufacturing, GaN commercialization, and localized production ecosystems to strengthen resilience and reduce geopolitical supply-chain exposure.

Key Industry Developments:

- In May 2025, Infineon Technologies AG introduced its new CoolSiC™ JFET product family designed for solid-state power distribution systems, targeting AI data centers, industrial safety systems, automotive battery disconnect switches, and advanced circuit protection applications.

- In January 2025, ON Semiconductor Corporation completed the acquisition of Qorvo’s Silicon Carbide JFET technology business for US$115 million, expanding its EliteSiC portfolio and strengthening its position in AI data-center power supplies, industrial energy storage systems, and EV battery disconnect applications.

Companies Covered in Discrete Semiconductor Market

- Infineon Technologies AG

- ON Semiconductor Corporation

- STMicroelectronics

- Toshiba Electronic Devices & Storage Corporation

- Mitsubishi Electric Corporation

- Vishay Intertechnology

- Nexperia

- ROHM Co., Ltd.

- Renesas Electronics Corporation

- Diodes Incorporated

- Fuji Electric Co., Ltd.

- Littelfuse, Inc.

- Wolfspeed, Inc.

- Semikron Danfoss

- Taiwan Semiconductor Manufacturing Company

- Hitachi Power Semiconductor Device, Ltd.

Frequently Asked Questions

The global discrete semiconductor market is estimated to be valued at US$35.8 billion in 2026.

The market is projected to reach approximately US$56.4 billion by 2033.

Key trends shaping the market include rapid adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) technologies for high-efficiency power applications and increasing semiconductor demand from electric vehicles and charging infrastructure.

Transistors represent the leading segment, accounting for approximately 42.6% of market share, due to extensive deployment in automotive electronics, industrial systems, consumer electronics, and telecom infrastructure.

The global market is projected to grow at a CAGR of 6.7% between 2026 and 2033.

Major companies include Infineon Technologies AG, ON Semiconductor Corporation, STMicroelectronics, and Toshiba Electronic Devices & Storage Corporation.