- Pharmaceuticals

- Diabetic Foot Ulcer Therapeutics Market

Diabetic Foot Ulcer Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Diabetic Foot Ulcer Therapeutics Market by Product Type (Advanced Wound Dressings, Skin Substitutes, Negative Pressure Wound Therapy Devices, Growth Factors), Ulcer Type (Neuropathic Ulcers, Ischemic Ulcers, Neuro-Ischemic Ulcers), End-user (Hospitals, Specialty Clinics, Long-term Care Centers, Ambulatory Surgical Centers), and Regional Analysis, 2026 - 2033

Diabetic Foot Ulcer Therapeutics Market Size and Trend Analysis

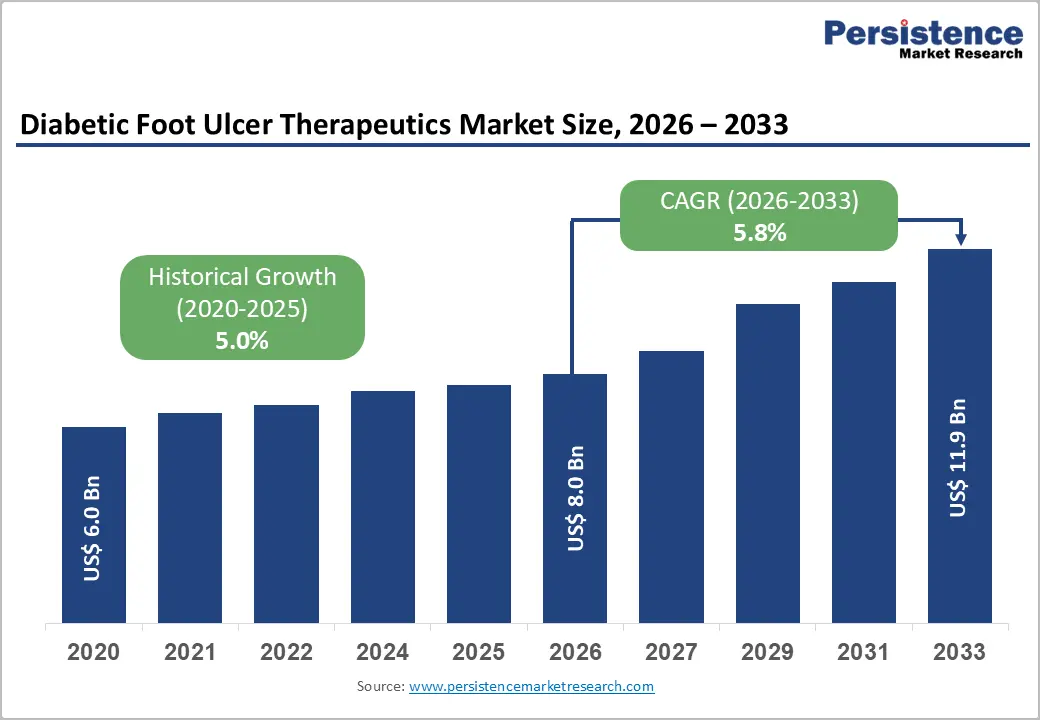

The global diabetic foot ulcer (DFU) therapeutics market size is expected to be valued at US$ 8 billion in 2026 and projected to reach US$ 11.9 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. It is witnessing significant growth due to the rising global burden of diabetes and the increasing prevalence of chronic wounds among diabetic patients. Diabetic foot ulcers are one of the most critical complications of diabetes, often leading to infections, prolonged hospital stays, high treatment costs, and, in severe cases, lower-limb amputations.

The growing diabetic population, especially in emerging economies, has intensified the demand for effective wound management solutions. Advanced treatment options such as skin substitutes, negative pressure wound therapy (NPWT), growth factors, and biologic dressings are gaining strong adoption. Additionally, improved healthcare infrastructure, favorable reimbursement policies, and greater awareness of early wound care management are further supporting market expansion globally.

Key Industry Highlights

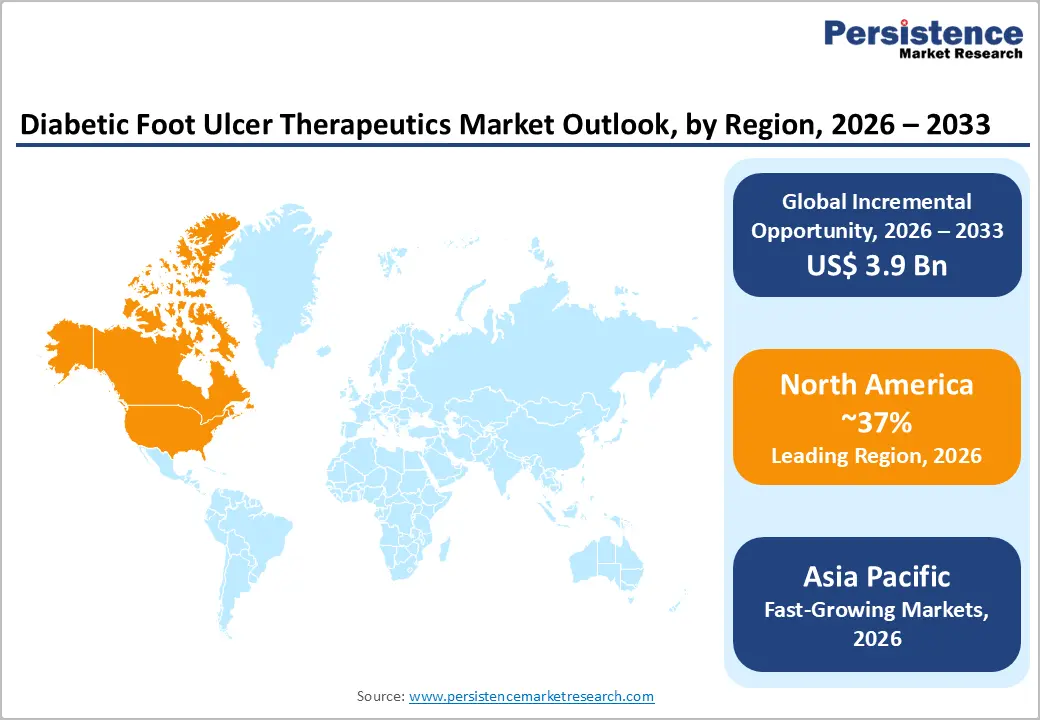

- Leading Region: North America holds a 37% share of the global DFU therapeutics market in 2025, underpinned by high diabetes prevalence, strong reimbursement coverage, and early adoption of advanced wound care technologies.

- Fastest Growing Region: Asia Pacific is projected to register a leading CAGR driven by a rapidly expanding diabetic population exceeding 220 million patients, rising healthcare investment, and improving wound care infrastructure.

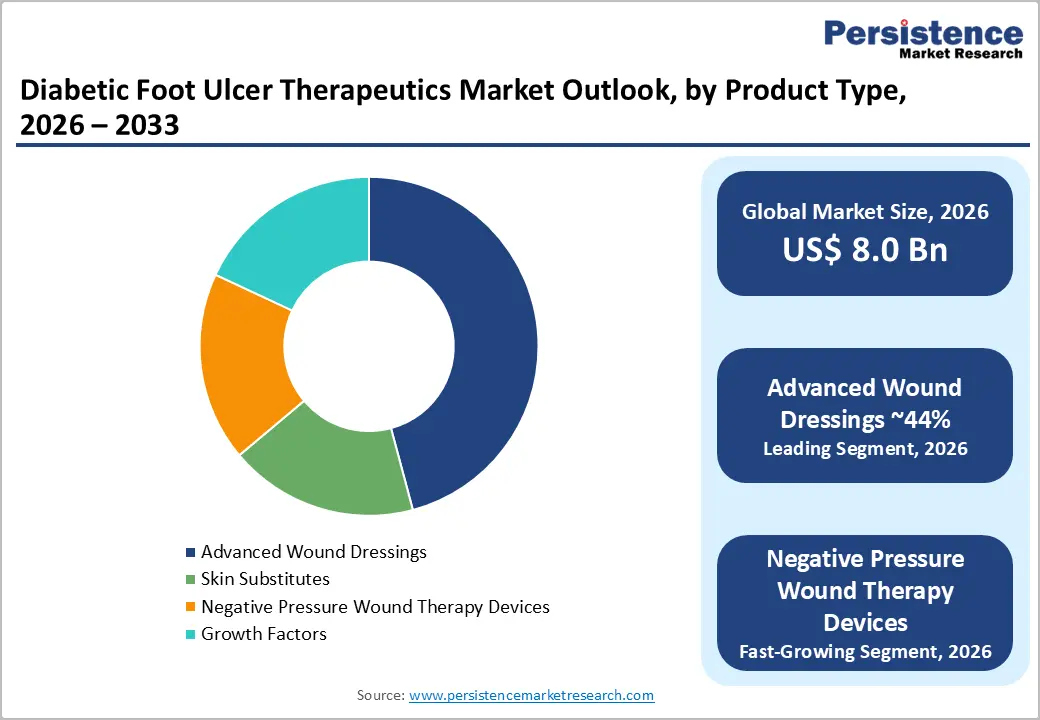

- Dominant Product Segment: Advanced wound dressings account for 44% share in 2026, supported by broad clinical applicability, established reimbursement, and continuous innovation in antimicrobial and smart dressing technologies.

- Fast-Growing Product Segment: Negative pressure wound therapy devices enjoy a high CAGR, driven by strong clinical evidence, expansion into home care settings, and FDA-approved portable device innovations.

- Key Opportunity: Rapidly growing diabetic populations in India, China, and Southeast Asia, combined with government NCD programs and increasing healthcare access, represent a multi-billion-dollar untapped opportunity for DFU therapeutics manufacturers.

Market Dynamics

Drivers - Rising Global Diabetes Burden Fuelling DFU Incidence

The exponential increase in the global diabetic population is one of the most significant catalysts for the DFU therapeutics market. As per the World Health Organization (WHO), diabetes prevalence has nearly doubled since 1980, and the disease now affects more than 422 million adults globally. Clinical literature indicates that ~25% of all diabetic patients will develop a foot ulcer during their lifetime, making DFU one of the most common and costly complications of diabetes.

The American Diabetes Association (ADA) estimates that 50-70% of all non-traumatic lower-limb amputations are associated with diabetic foot disease. These statistics compellingly underscore the urgent clinical need for effective DFU therapeutics, directly translating into sustained market demand for advanced wound dressings, growth factors, and skin substitute products.

Increasing Emphasis on Limb Preservation and Healthcare Cost Reduction

Increasing focus on the reduction of healthcare expenditure related to advanced diabetic foot conditions and limb preservation is projected to boost the global diabetic foot ulcer treatment market. Amputations significantly raise long-term medical costs in addition to causing psychological trauma and physical disability.

The average cost of a significant amputation in the U.S. can surpass US$ 70,000. Management of a diabetic foot ulcer with innovative wound care methods substantially reduces complications and costs. Hence, healthcare institutions and payers are constantly investing in the early-stage therapeutic interventions such as antimicrobial dressings, negative pressure wound therapy (NPWT), and bioengineered skin grafts.

Restraints - High Cost of Advanced Wound Care Products

The elevated cost of advanced DFU therapeutics remains a significant restraint, particularly in low- and middle-income countries. Bioengineered skin substitutes can cost between US$ 500 and US$ 1,500 per application, and full treatment courses may require multiple applications. According to the National Institute for Health and Care Excellence (NICE), advanced wound care represents a disproportionately high share of hospital budgets. Limited insurance coverage or reimbursement in emerging markets restricts access for a large patient population, thereby constraining overall market penetration and slowing volume-based growth in price-sensitive regions such as South Asia and Sub-Saharan Africa.

Patient Non-compliance to Hamper Success of Proven Treatments

A key factor estimated to limit the adoption of diabetic foot ulcer therapeutic strategies is patient non-compliance. Due to lifestyle restrictions or the lack of knowledge, diabetic patients often do not act in accordance with daily wound care instructions, follow-up appointments, or comply with offloading protocols.

Total contact casting is considered highly effective in managing offloading plantar pressure. However, patients tend to discontinue it prematurely as it limits mobility. Regardless of the quality or accessibility of therapeutic interventions, this behavioral aspect is anticipated to lower their efficacy.

Opportunities - Rise of Cell-based Therapies to Enhance Healing Prospects for Complex Ulcers

The ongoing development and commercialization of cell-based therapies and biologics to enhance wound regeneration in non-healing or complex ulcers is anticipated to create a new avenue. Treatments, including recombinant growth factors, mesenchymal stem cells, and Platelet-Rich Plasma (PRP) are showcasing promising results in clinical trials.

Increasing regulatory approval for regenerative medicine is another key factor anticipated to create opportunities for companies to launch new biologic therapies in the market. Anika Therapeutics, for instance, extends its presence in regenerative medicine by developing injectable hyaluronic acid-based therapies. These are extensively studied for wound healing applications, such as diabetic ulcers, by improving tissue regeneration and extracellular matrix formation.

Category-wise Analysis

Product Type Insights

Advanced wound dressings dominate the DFU therapeutics market with an estimated 44% market share in 2025. This leadership reflects the widespread clinical adoption of next-generation wound dressings including hydrocolloid, foam, alginate, and antimicrobial silver dressings, that optimize the moist wound healing environment and combat infection.

The Wound Healing Society and European Wound Management Association (EWMA) both recommend advanced moist wound dressings as first-line interventions in DFU management guidelines. Their relatively lower cost versus bioengineered skin substitutes, combined with broad prescriber familiarity and straightforward application, drives high volume usage across hospitals, long-term care centers, and community settings. Ongoing innovations such as sustained-release antibiotic dressings and moisture-sensing smart dressings further reinforce the segment's dominance.

Ulcer Type Insights

Neuropathic Ulcers represent the leading segment within the ulcer type category, accounting for ~60% of all diabetic foot ulcer cases globally, according to clinical studies published in Diabetes Care and the British Journal of Diabetes. Peripheral neuropathy one of the most prevalent chronic complications of diabetes causes loss of protective sensation, mechanical stress, and undetected tissue breakdown, making neuropathic ulcers the predominant DFU subtype encountered in clinical practice.s

Their relatively manageable treatment pathway compared to ischemic ulcers and higher incidence rates ensure a consistently larger patient volume, sustaining demand for tailored therapeutic products such as offloading devices and advanced dressings for neuropathic wound management.

End-user Insights

Hospitals constitute the largest end-user segment in the DFU therapeutics market, commanding an estimated 45% market share in 2025. The dominance of hospitals is attributed to their multidisciplinary wound care teams, access to advanced therapeutic modalities including NPWT systems and surgical debridement, and their capacity to manage complex, infected, or high-risk DFU cases requiring inpatient care. According to the Agency for Healthcare Research and Quality (AHRQ), DFU-related hospitalizations account for billions in annual healthcare costs in the United States alone.

The integration of wound care specialist services within hospital settings, combined with established reimbursement pathways, further cements the hospital segment's leading position across major geographies.

Regional Insights

North America Diabetic Foot Ulcer Therapeutics Market Trends and Insights

North America leads the global DFU therapeutics market with a 37% market share in 2025, supported by a high diabetes prevalence rate, well-established reimbursement infrastructure, strong presence of major wound care companies, and robust clinician adoption of advanced therapeutic modalities. The region also benefits from proactive regulatory support from the U.S. FDA, enabling faster product approvals.

U.S. Diabetic Foot Ulcer Therapeutics Market Size

The United States is poised for ~80% share. With over 37 million Americans living with diabetes (per the Centers for Disease Control and Prevention), DFU is a critical public health issue. Strong Medicare and Medicaid reimbursements for advanced wound care products and NPWT devices further support market growth.

Europe Diabetic Foot Ulcer Therapeutics Market Trends and Insights

Europe holds the second-largest share of the global DFU therapeutics market, driven by well-developed healthcare systems, national diabetes care programs, and strong guideline adherence from bodies such as the EWMA and NICE. Growing elderly diabetic populations and increasing clinical adoption of skin substitutes and bioactive dressings are key regional trends shaping market evolution through 2033.

Germany Diabetic Foot Ulcer Therapeutics Market Size

Germany is the largest European market for DFU therapeutics, contributing ~22% of the regional revenue in 2025. The country's statutory health insurance framework provides strong reimbursement for advanced wound care, and a well-trained network of diabetologists and wound care specialists ensures consistent uptake of innovative products across hospital and outpatient settings.

UK Diabetic Foot Ulcer Therapeutics Market Size

The UK represents ~16% of European market revenue in 2025. The NHS actively supports DFU prevention and management through the National Diabetes Foot Care Programme, which has standardized care pathways and increased utilization of advanced wound dressings and offloading devices across NHS Trusts.

France Diabetic Foot Ulcer Therapeutics Market Size

France accounts for roughly 14% of the European DFU therapeutics market in 2025. Rising diabetes prevalence with over 4 million diabetics according to Santé Publique France and growing state investment in chronic wound care infrastructure, are supporting expanding adoption of skin substitutes and NPWT devices within both public and private hospital networks.

Asia Pacific Diabetic Foot Ulcer Therapeutics Market Trends and Insights

Asia Pacific is the fastest-growing region in the global DFU therapeutics market, driven by the world's largest diabetic population led by China and India, alongside improving healthcare access and rising government health expenditure. China alone has over 140 million diabetic individuals (per IDF), creating massive latent demand for DFU therapeutics as wound care awareness improves.

India Diabetic Foot Ulcer Therapeutics Market Size

India holds ~18% of the Asia Pacific DFU therapeutics market in 2025. With over 77 million diabetics and a high unmet need in wound care, the market is poised for rapid expansion. Increasing penetration of specialty clinics, government NCD programs, and the growing private healthcare sector are supporting product adoption across urban and semi-urban geographies.

Japan Diabetic Foot Ulcer Therapeutics Market Size

Japan represents ~20% of the Asia Pacific market in 2025, benefiting from an aging population, universal healthcare coverage, and high adoption of advanced wound care technology. The Japan Diabetes Society actively promotes DFU management guidelines, supporting consistent uptake of approved advanced dressings and NPWT systems across the country's extensive hospital network.

Competitive Landscape

The global DFU therapeutics market exhibits a moderately consolidated competitive landscape, with multinational medtech corporations such as Smith & Nephew Plc., 3M Health Care, Mölnlycke Health Care AB, and Medtronic Plc holding significant market share through broad product portfolios and extensive distribution networks. Key competitive strategies include strategic acquisitions, product portfolio expansion into biologics and advanced skin substitutes, and geographic expansion into emerging markets.

Companies are increasingly investing in digital wound management solutions and smart dressings to differentiate their offerings and enhance clinical outcomes, a trend that is expected to intensify competitive dynamics through the forecast period.

Key Developments

- In March 2026, Smith+Nephew announced the launch of ALLEVYN COMPLETE CARE Foam Dressing, designed with proprietary technologies and supported by extensive scientific data and strong clinical evidence.

- In February 2025, PolarityBio, headquartered in Utah, declared that the company’s SkinTE bagged Breakthrough Therapy Designation (BTD) from the U.S. FDA for the treatment of Wagner Grade 1 diabetic foot ulcers. The designation offered new opportunities to gain access to development pathways, rising engagement with the FDA, and improved regulatory support.

- In February 2025, researchers at the First Affiliated Hospital of Anhui Medical University, China, found that the wound granulation tissues of diabetic foot ulcer patients who received negative pressure wound therapy for a week exhibited a steep surge in FGF7 protein expression and a significant decrease in miR-155 expression.

- In January 2025, RION Co. Ltd., based in Japan, announced the completion of patient enrolment in its Phase II clinical trial for Purified Exosome Product (PEP) in the treatment of diabetic foot ulcers. This represents an important leap in the company’s goal to develop innovative therapies for the management of chronic wounds.

Diabetic Foot Ulcer Therapeutics Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 6.0 Billion |

| Current Market Value (2026) | US$ 8.0 Billion |

| Projected Market Value (2033) | US$ 11.9 Billion |

| CAGR (2026 - 2033) | 5.8% |

| Leading Region | North America, 37% market share in 2025 |

| Dominant Product Type Segment | Advanced Wound Dressings, ~44% market share in 2025 |

| Top-Ranking Ulcer Type Segment | Neuropathic Ulcers, ~60% market share in 2025 |

| Incremental Opportunity (2026 - 2033) | US$ 3.9 Billion |

Companies Covered in Diabetic Foot Ulcer Therapeutics Market

- ConvaTec Group Plc

- B Braun Melsungen AG

- Acelity L.P. Inc.

- Molnlycke Health Care AB

- 3M Health Care

- Smith & Nephew Plc.

- Coloplast Corp.

- Medline Industries, LP

- Medtronic Plc

- Others

Frequently Asked Questions

The global diabetic foot ulcer therapeutics market is expected to be valued at US$ 8.0 billion in 2026.

Key demand drivers include rising global diabetes prevalence, growing awareness of advanced wound care, innovations in skin substitutes and NPWT, and improved reimbursement support.

North America leads the diabetic foot ulcer therapeutics market with around 37% share, supported by high diabetes prevalence, strong infrastructure, and reimbursement policies.

Major growth opportunities include expanding NPWT use in home care and rising demand across Asia Pacific and Latin America due to growing diabetic population.

Leading companies operating in the global market include ConvaTec Group Plc, Smith & Nephew Plc., Mölnlycke Health Care AB, 3M Health Care, Medtronic Plc, B. Braun Melsungen AG, among others, competing through product innovation, geographic expansion, and strategic partnerships.