- Chipsets & Processors

- Consumer Standard Logic IC Market

Consumer Standard Logic IC Market Size, Share, and Growth Forecast, 2026 - 2033

Consumer Standard Logic IC Market Technology Type (CMOS, BiCMOS, Others), Consumer Application (Smartphones, Wearables/Hearables, Home Automation), Distribution Channel ((Direct OEM, Distributor), and Regional Analysis 2026 - 2033

Consumer Standard Logic IC Market Size and Trends Analysis

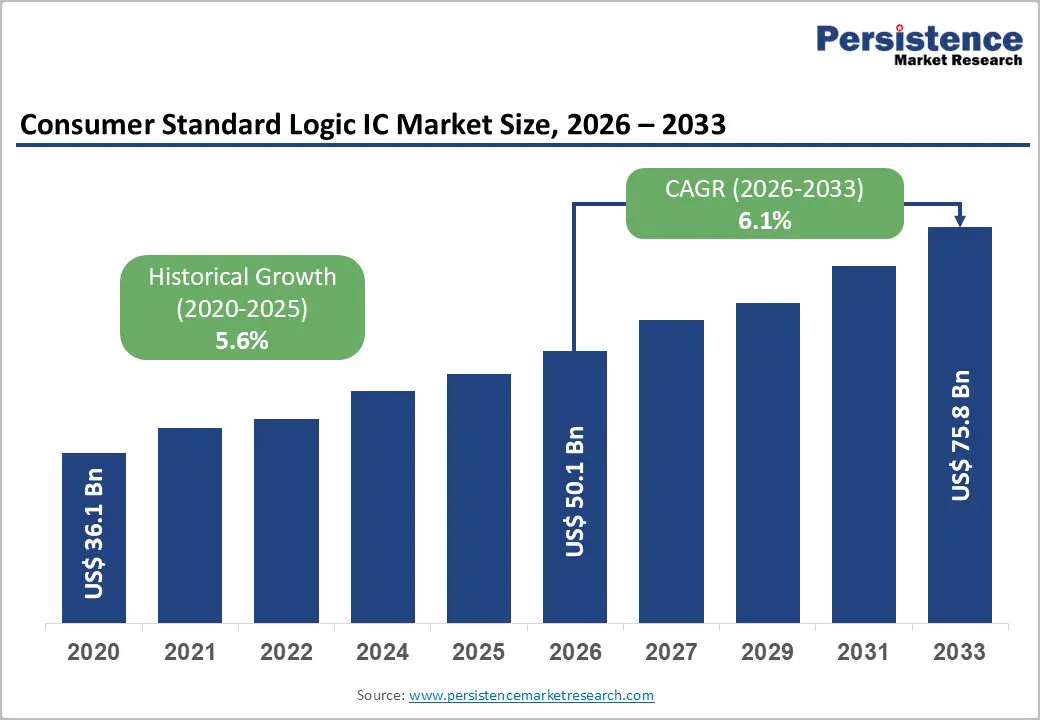

The global consumer standard logic IC market size is likely to be valued at US$50.1 billion in 2026 and is expected to reach US$75.8 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by the aggressive integration of 5G communication modules in consumer devices and the surging demand for miniaturized power-efficient components in the burgeoning wearable electronics sector.

Technological shifts to advanced CMOS nodes support energy-efficient devices, while APAC manufacturing hubs drive volume production. Furthermore, the transition toward smart home ecosystems is mandating a higher volume of standard logic gates and level shifters to ensure interoperability between disparate hardware components.

Key Industry Highlights:

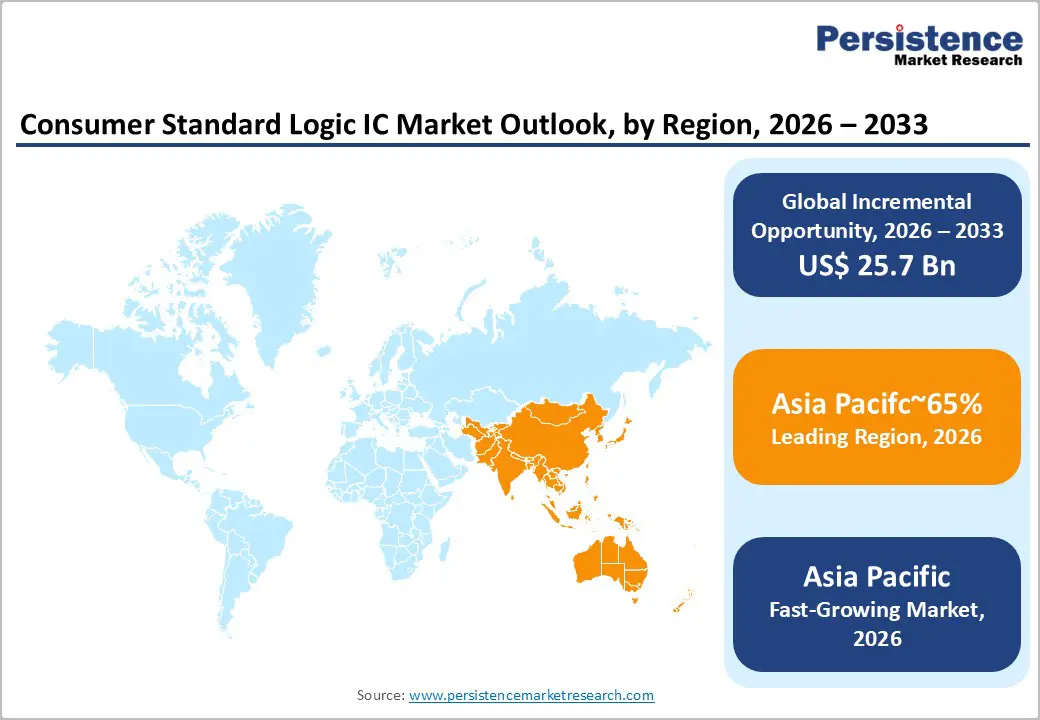

- Leading Region: Asia Pacific is projected to lead due to its concentration of semiconductor foundries, advanced packaging clusters, and dense electronics OEM ecosystems, accounting for approximately 65% share in 2026, supported by sub-7nm logic fabrication, vertical integration, and policy-backed expansion.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to industrial scaling, government incentives, and adoption across consumer electronics, IoT, and wearable sectors.

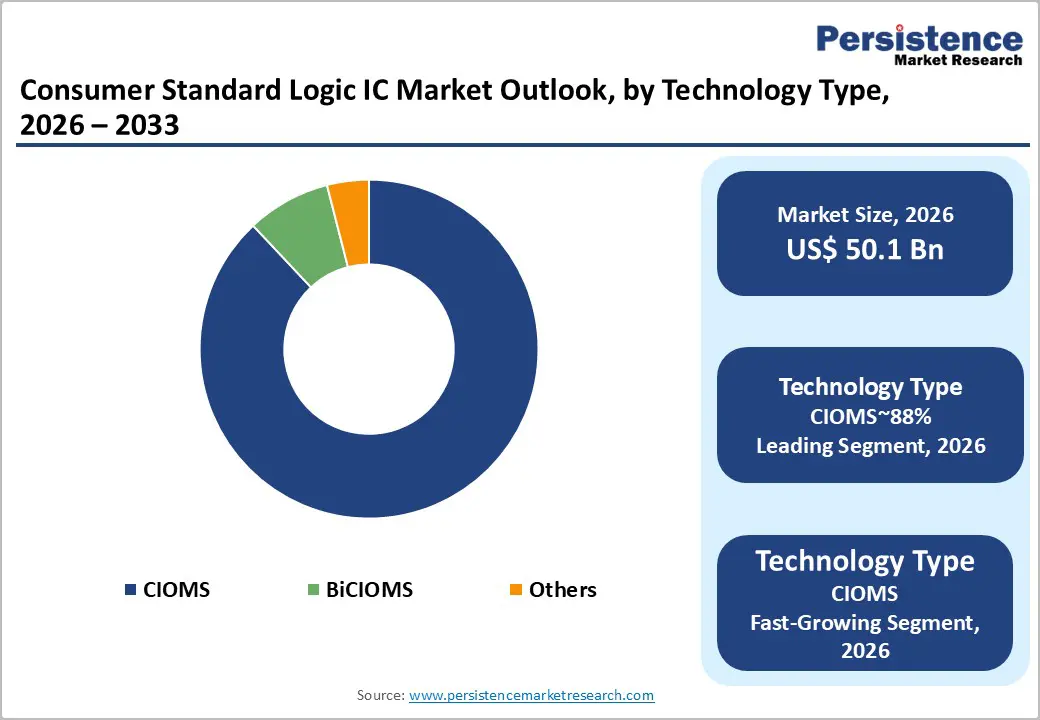

- Leading Technology Type: CMOS is projected to dominate due to energy efficiency, high integration density, and functional versatility across smartphones, wearables, and IoT modules, holding approximately 88% share in 2026.

- Leading Consumer Application: Smartphones are projected to dominate due to broad adoption, recurring device upgrades, and high logic integration requirements, with approximately 47% share in 2026.

| Key Insights | Details |

|---|---|

|

Consumer Standard Logic IC Market Size (2026E) |

US$50.1 Bn |

|

Market Value Forecast (2033F) |

US$75.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Proliferation of 5G-Enabled Smartphones and Escalating Hardware Architecture Complexity

The migration toward fifth-generation mobile connectivity structurally intensifies semiconductor content per device. 5G smartphone architectures require expanded signal routing, voltage translation, and control interfaces. Standard logic integrated circuits enable deterministic data exchange between application processors and distributed subsystems. Multi-band radio-frequency modules require precise level shifting across heterogeneous voltage domains. Advanced camera arrays and biometric authentication stacks increase the density of peripheral integration. This integration complexity amplifies the demand for logic gates, buffers, and signal-conditioning components. The resulting hardware densification embeds standard logic devices deeper within consumer handset designs.

Rising component counts elevate wafer demand across mature process nodes. Fabricators prioritize CMOS-based logic production due to power efficiency constraints. Increased I/O density reinforces the need for robust signal integrity management frameworks. Packaging innovations must accommodate tighter board layouts and thermal limitations. Regulatory spectrum allocations further complicate radio architectures, reinforcing interface requirements. Margin structures benefit from volume-driven scale across high-velocity smartphone cycles. The handset evolution sustains structural demand expansion within the consumer standard logic ecosystem.

Expansion of IoT Devices and Power-Constrained Wearable and Hearable Platforms

The proliferation of connected IoT endpoints is reshaping semiconductor demand composition. Wearable and hearable devices impose stringent constraints on footprint, thermal dissipation, and standby power. Standard logic integrated circuits enable discrete control functions without the overhead of a microcontroller. Advanced node CMOS architectures reduce leakage currents and optimize switching efficiency. Signal buffering and state management are increasingly offloaded to compact logic devices. This architectural distribution minimizes active power draw across sensor-driven consumer platforms. The logic miniaturization aligns with the ecosystem’s emphasis on battery longevity.

The demand shifts toward advanced packaging and wafer-level integration strategies. Foundries prioritize low-power CMOS process variants tailored for ultra-compact electronics. Component suppliers recalibrate portfolios toward small-outline and chip-scale configurations. Regulatory emphasis on energy efficiency reinforces low-consumption design imperatives. Margin structures depend on high-volume production across fragmented IoT categories. Supply-chain coordination intensifies as device lifecycles shorten within consumer ecosystems. These dynamics structurally elevate the integration of standard logic across distributed, connected devices.

Barrier Analysis - Escalating Design Complexity and Diminishing Economic Returns from Node Scaling

Migration toward sub-seven-nanometer CMOS nodes intensifies design and verification complexity. Advanced lithography demands sophisticated layout rules and multi-patterning integration strategies. Research and development expenditures expand disproportionately relative to incremental performance gains. Standard logic devices traditionally operate within high-volume, low-margin commercial frameworks. The capital required to port these components to leading-edge processes challenges profitability assumptions. Return-on-investment visibility weakens, particularly for manufacturers without diversified product portfolios. This economic imbalance discourages widespread participation in the development of advanced node-standard logic.

Shrinking geometries also introduce additional burdens for variability management and reliability validation. Process control precision becomes critical to mitigate leakage and electromigration risks. Smaller suppliers face structural barriers to accessing the extreme ultraviolet tooling ecosystem. Market participation increasingly favors vertically integrated device manufacturers with capital resilience. Reduced supplier diversity concentrates pricing power and compresses downstream negotiation flexibility. Entry thresholds for emerging designers consequently rise across consumer electronics ecosystems. These dynamics collectively moderate the diffusion of innovation within standardized logic component categories.

Escalating Research Intensity and Advanced Node Manufacturing Cost Structures

The transition toward advanced process nodes substantially increases semiconductor capital intensity. Fabrication facilities require investments of up to $20 billion per installation. Initial production cycles frequently operate below optimal yield thresholds. Suboptimal yields elevate per-unit costs and compress operational efficiency metrics. These economics directly transmit into integrated circuit pricing structures. Higher component prices constrain procurement flexibility among mid-tier consumer electronics manufacturers. Cost pass-through pressures become particularly acute within price-sensitive wearable categories.

Elevated development expenditures also expand amortization burdens across shortened product lifecycles. Engineering complexity increases the costs of mask design, validation, and qualification. Advanced node integration demands tighter process control and defect mitigation protocols. Equipment depreciation and energy consumption further inflate fabrication cost baselines. Pricing adjustments in logic components influence bill-of-material structures across compact devices.

Opportunity Analysis - Integration of Edge Artificial Intelligence within Consumer Home Automation Platforms

The decentralization of artificial intelligence processing toward edge-enabled consumer appliances expands interface complexity. Smart refrigerators, surveillance systems, and connected controllers increasingly execute inference locally. Localized processing architectures require precise voltage translation across heterogeneous component ecosystems. Legacy sensor modules often operate in higher-voltage domains than embedded AI processors. This voltage disparity necessitates advanced-level shifters and signal conditioning logic. Standard logic integrated circuits, therefore, become essential bridging components within distributed appliance architectures. The incremental revenue potential associated with home automation expansion reinforces this structural opportunity.

Embedded AI integration also elevates demand for deterministic latency and signal integrity. Power management frameworks must accommodate mixed-voltage subsystems without compromising thermal envelopes. Semiconductor suppliers capable of optimizing low-leakage CMOS logic benefit from design standardization trends. Regulatory scrutiny of data privacy further accelerates the adoption of local processing. This shift redistributes semiconductor value toward interface and control circuitry segments. Device manufacturers increasingly prioritize modular architectures supporting scalable intelligence layers. Collectively, these dynamics position standard logic components as foundational enablers of edge-enabled consumer ecosystems.

Acceleration of Green Electronics and Ultra-Low Power Logic Architectures

Global decarbonization mandates are reshaping performance benchmarks for consumer semiconductor components. Policy frameworks such as the European Green Deal emphasize energy efficiency across electronic ecosystems. Consumer devices increasingly require near-zero standby leakage under always-on operating conditions. Advanced CMOS and BiCMOS platforms enable substantial reductions in quiescent current profiles. Ultra-low leakage logic gates directly support extended battery endurance targets. Environmental compliance expectations, therefore, translate into measurable shifts in design specifications.

Battery-operated devices intensify scrutiny on static power dissipation across interface circuitry. Leakage minimization improves lifecycle efficiency and reduces cumulative energy footprints. Semiconductor process refinement enhances threshold control and subthreshold leakage management. Procurement strategies increasingly integrate sustainability metrics alongside cost-performance benchmarks. Ultra-low-power logic segments are projected to expand at rates exceeding baseline averages. This growth differential signals structural reallocation of demand toward efficiency-centric architectures.

Category–wise Analysis

Technology Type Insights

CMOS is expected to lead, accounting for approximately 88% share in 2026, underpinned by its intrinsic low static power consumption and superior noise immunity across battery-operated consumer platforms. Its dominance reflects deep integration across smartphones, wearables, and IoT modules, where density and leakage control directly influence device thermals and battery endurance. Industry leaders such as Texas Instruments, with its SN74 logic portfolio; Nexperia’s 74HC and 74LVC series; and STMicroelectronics’ advanced low-voltage logic families anchor high-volume deployments across OEM ecosystems. Fab capacity allocation heavily favors CMOS architectures, reinforcing economies of scale and predictable supply continuity. Continuous node migration, packaging miniaturization, and compatibility with advanced SoC platforms sustain its structural advantage within high-throughput consumer electronics manufacturing environments.

CMOS nodes are expected to be the fastest-growing segment, driven by escalating performance-per-watt requirements in premium smartphones, AR devices, and edge-enabled consumer appliances. Sub-7nm process migration enhances switching efficiency and leakage suppression, enabling tighter integration with leading processors from Samsung and Sony Semiconductor Solutions. Renesas Electronics’ low-power microcontroller platforms and NXP’s advanced node-integration strategies align with high-density logic requirements. AI-assisted electronic design automation tools increasingly optimize layout complexity and yield performance at advanced geometries.

Consumer Application Insights

Smartphones are expected to lead, accounting for approximately 47% share in 2026, underpinned by sustained global shipment volumes and dense subsystem integration across flagship and mid-tier devices. Each handset embeds multiple standard logic components for display control, RF switching, camera interfacing, and battery management, reinforcing recurring semiconductor content per unit. Platforms built around Qualcomm Snapdragon, Samsung Exynos, and MediaTek Dimensity processors rely on companion logic from Texas Instruments SN74 series and Nexperia 74LVC families to manage voltage translation and signal integrity. Foldable architectures and on-device AI acceleration further intensify the deployment of logic gates across flexible PCBs and sensor hubs. High replacement cycles and premium feature stacking sustain smartphones as the structural revenue anchor within consumer logic integration.

Wearables and hearables are expected to be the fastest-growing segment, driven by the accelerating adoption of health-centric devices and true wireless audio ecosystems. Products such as Apple AirPods Pro, Samsung Galaxy Buds, and Galaxy Ring integrate ultra-miniaturized logic for noise cancellation, touch control, and biometric sensing. Ambiq Micro’s subthreshold Apollo platforms and Nordic Semiconductor's Bluetooth Low Energy solutions exemplify ultra-low-power architectures that support always-on monitoring. Expanding sensor arrays for ECG, SpO2, and temperature tracking elevate demand for precision level shifters and low-noise buffers. Migration toward WLCSP and DSBGA packaging enables extreme miniaturization, increasing logic intensity per device and positioning wearables as the highest-velocity growth frontier within consumer electronics.

Regional Insights

Asia Pacific Consumer Standard Logic IC Market Trends

Asia Pacific is expected to remain the leading regional market, with an approximately 65% share of the global market, and to be the fastest-growing region, supported by structural semiconductor concentration across China, Taiwan, South Korea, and Japan. The region is positioned to anchor global supply through vertically integrated foundries, advanced packaging clusters, and dense electronics OEM ecosystems. Platform leadership from TSMC and Samsung Electronics is expected to reinforce their dominance in sub-7nm logic fabrication, while SMIC is anticipated to deepen domestic capacity under localization strategies. Regional design champions such as MediaTek and system OEMs, including Xiaomi, are projected to sustain downstream demand integration. Policy-backed semiconductor expansion, 5G infrastructure densification, and on-device AI adoption are expected to consolidate Asia Pacific’s role as the structural epicenter of global standard logic deployment.

China is expected to serve as the regional anchor, shaping investment flows, supply chain configurations, and industrial policy alignment across the broader Asia-Pacific ecosystem. National self-reliance initiatives are projected to accelerate domestic fabrication, the migration of advanced packaging, and ecosystem financing, thereby reinforcing vendor localization strategies. Industrial demand from telecom operators and hyperscale device assemblers is anticipated to sustain high wafer throughput and multi-foundry procurement models. Regulatory tightening around export controls and cybersecurity compliance is expected to reorganize sourcing networks toward trusted supply corridors, influencing fab expansion sequencing and technology node prioritization.

North America Consumer Standard Logic IC Market Trends

North America is expected to remain a structurally stable and innovation-centric market within the global consumer standard logic IC landscape, anchored by high-value intellectual property creation and advanced architecture design. While large-scale wafer fabrication is concentrated in the Asia Pacific, the region is well-positioned to retain strategic relevance through its depth in semiconductor R&D and fabless leadership. The policy environment under the CHIPS and Science Act is expected to reinforce domestic fabrication incentives, supply chain security, and the localization of advanced-node capacity. Technology firms such as Intel and NVIDIA are projected to sustain high-end logic innovation across AI-accelerated consumer electronics and immersive computing platforms. Demand is anticipated to remain anchored in premium applications, including augmented and virtual reality devices, and advanced gaming systems.

The U.S. is expected to function as the regional anchor, shaping regulatory standards, capital allocation priorities, and next-generation logic design frameworks. Federal semiconductor funding mechanisms are projected to stimulate ecosystem reintegration across design, fabrication, and advanced packaging layers. Emphasis on cybersecurity resilience and hardware-level trust architectures is expected to influence logic IC validation protocols and secure-by-design engineering standards. Vendor strategies are expected to evolve toward closer integration between chip designers and cloud platform operators, reinforcing co-optimization of AI workloads and edge-processing efficiency. As geopolitical supply chain sensitivities persist, multi-sourcing strategies and domestic capacity expansion are positioned to preserve strategic autonomy.

Europe Consumer Standard Logic IC Market Trends

Europe is expected to remain a mature and structurally stable market within the global consumer-standard logic IC landscape, supported by regulatory harmonization, high industrial quality standards, and cross-sector technology convergence. The regional ecosystem is positioned around advanced engineering depth rather than volume-led fabrication scale, with policy coordination under the European Chips Act expected to reinforce strategic semiconductor autonomy. Demand is expected to be driven by the integration of consumer-grade logic architectures into automotive and industrial platforms, as cockpit digitization and connected mobility systems adopt higher-performance processing standards. Design leadership from ARM Holdings is expected to continue shaping global logic instruction sets and energy-efficient chip architectures.

Germany is expected to serve as the regional anchor, shaping the adoption of industrial logic through its automotive manufacturing base and precision electronics ecosystem. High-reliability logic deployment in advanced driver assistance systems and digital instrument clusters is anticipated to sustain demand for automotive-grade standard IC integration. Regulatory emphasis on sustainability compliance and supply chain transparency is expected to influence vendor sourcing models and production traceability standards. European semiconductor firms are projected to prioritize energy-efficient node optimization, advanced packaging collaboration, and long-lifecycle product qualification cycles.

Competitive Landscape

The global consumer-standard logic IC market is moderately consolidated, with top players including Texas Instruments, Renesas Electronics, NXP Semiconductors, Toshiba Electronic Devices, and Analog Devices. Market structure exhibits higher concentration in high-volume CMOS gate production, whereas specialized segments such as level shifters and low-power logic devices remain fragmented, supporting niche players with tailored capabilities. Concentration is reinforced by scale, design IP portfolios, and reliability standards that influence procurement across industrial, automotive, and consumer electronics sectors.

Leaders matter for their ability to integrate horizontal breadth with vertical depth, offering extensive, discrete logic portfolios while advancing low-power and high-efficiency nodes. Competitive positioning is shaped by manufacturing scale, power-efficiency ratings, and ecosystem partnerships that align semiconductor IP with customer-specific design workflows. Industry behavior is characterized by incremental consolidation, selective M&A activity, and platform-level integration strategies, with innovation focused on reducing die size, optimizing thermal performance, and expanding reliability-compliant solutions. The market is expected to sustain structural stability while enabling smaller specialized players to address low-volume, high-precision logic requirements.

Key Industry Developments:

- In February 2026, STMicroelectronics introduced the first automotive MCU with AI acceleration for edge intelligence, enabling real-time processing and democratization of AI in next-gen consumer vehicles.

- In January 2026, Texas Instruments launched a new automotive chip lineup with performance up to 1200 TOPS, boosting autonomous driving features through higher-density logic and AI sensing.

- In December 2025, Toshiba introduced the TC75W71FU, a high-speed CMOS dual comparator featuring a full input/output voltage range. The device is specifically engineered for overcurrent detection applications in industrial and consumer hybrid equipment.

Companies Covered in Consumer Standard Logic IC Market

- Texas Instruments

- Nexperia

- ON Semiconductor

- Toshiba Electronic Devices & Storage Corporation

- Renesas Electronics Corporation

- STMicroelectronics

- Diodes Incorporated

- Microchip Technology

- Analog Devices

- NXP Semiconductors

- ROHM Semiconductor

- Broadcom

- Infineon

- MediaTek

- Skyworks

- Qorvo

Frequently Asked Questions

The global consumer standard logic IC market is projected to be valued at US$50.1 billion in 2026 and is expected to reach US$75.8 billion by 2033, driven by 5G integration, wearable device proliferation, and miniaturized, power-efficient logic components.

The rapid adoption of health-focused wearables and true wireless audio devices is driving demand for ultra-low-power, compact logic ICs. These components support high-density integration, signal conditioning, and voltage translation across sensor arrays while minimizing energy consumption for extended battery life.

The consumer standard logic IC market is forecast to grow at a CAGR of 6.1% from 2026 to 2033, reflecting sustained adoption in smartphones, home automation, and edge-AI-enabled consumer appliances.

Asia Pacific is both the leading and fastest-growing region, accounting for approximately 65% share. Growth is underpinned by manufacturing hubs in China, Taiwan, South Korea, and Japan, combined with strong OEM integration, sub-7nm CMOS node adoption, and policy-backed semiconductor expansion.

The consumer standard logic IC market is moderately consolidated, with leading players including Texas Instruments, Nexperia, ON Semiconductor, Toshiba Electronic Devices & Storage, Renesas Electronics, STMicroelectronics, Diodes Incorporated, Microchip Technology, Analog Devices, NXP Semiconductors, ROHM Semiconductor, Broadcom, Infineon, MediaTek, Skyworks, and Qorvo. These firms compete through scale, IP portfolios, low-power node capabilities, and ecosystem partnerships.