- Pharmaceuticals

- Attention Deficit Hyperactivity Disorder Therapeutics Market

Attention Deficit Hyperactivity Disorder Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Attention Deficit Hyperactivity Disorder (ADHD) Therapeutics Market by Drug (Stimulants, Non-stimulants: Atomoxetine, Bupropion, Guanfacine, Clonidine), Age Group (Pediatric and Adolescent, Adults), Distribution Channel (Specialty Clinics, Hospital Pharmacies, Retail Pharmacies, E-Commerce), and Regional Analysis, 2026 - 2033

Attention Deficit Hyperactivity Disorder Therapeutics Market Size and Trend Analysis

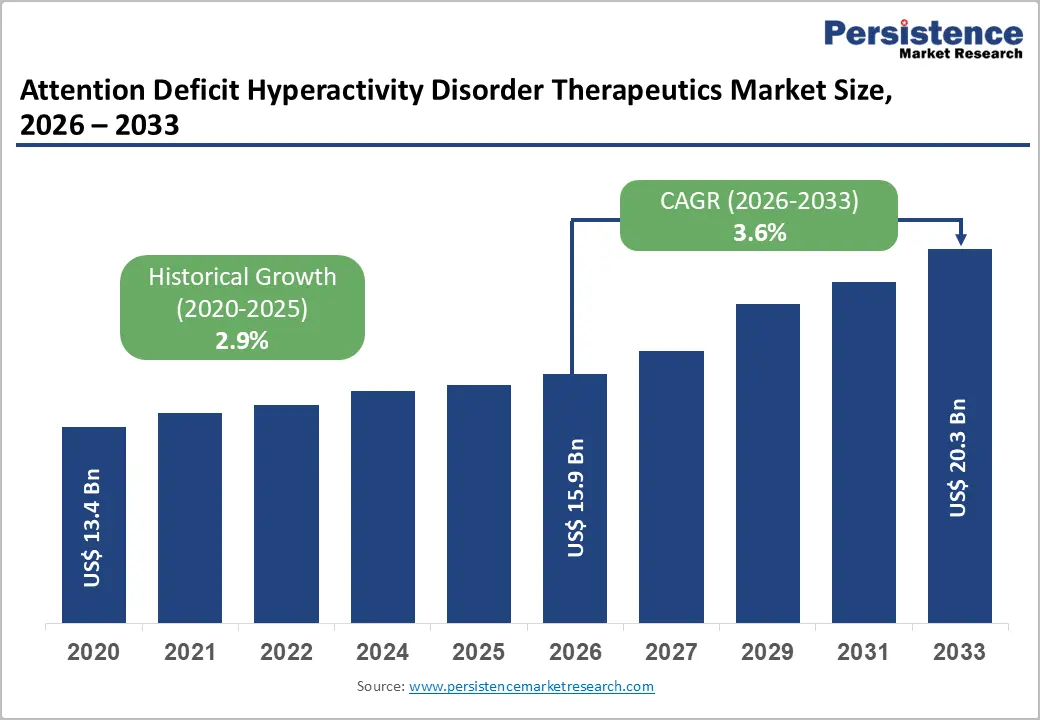

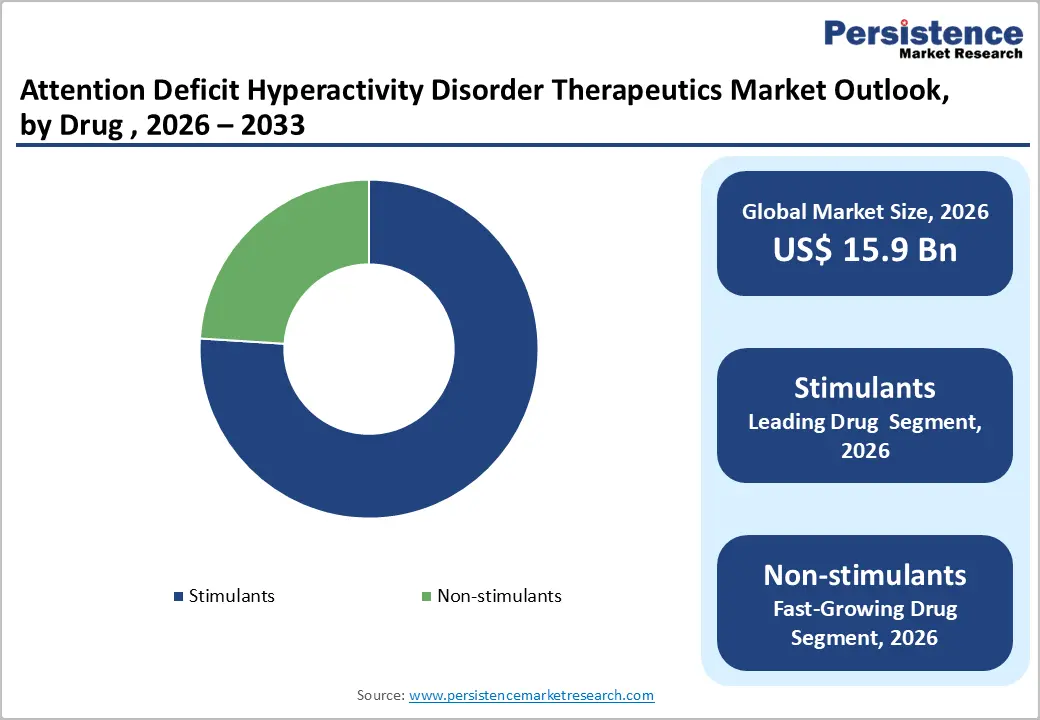

The global attention deficit hyperactivity disorder (ADHD) therapeutics market size is expected to be valued at US$ 15.9 billion in 2026 and projected to reach US$ 20.3 billion by 2033, growing at a CAGR of 3.6% between 2026 and 2033.

This consistent growth is underpinned by rising global ADHD diagnosis rates across both pediatric and adult populations, expanding insurance coverage for mental health treatment, and a robust pharmaceutical pipeline of long-acting stimulant reformulations and non-stimulant alternatives. The American Psychiatric Association (APA) estimates ADHD prevalence at 5% in children and approximately 2.5% in adults globally, with diagnosis rates historically underestimated, particularly in adult and female populations.

Heightened awareness driven by telehealth-enabled psychiatric consultations, growing destigmatization of mental health conditions, and the broadening recognition of adult ADHD as a chronic, manageable condition are collectively expanding the treated patient pool, creating sustained demand for both branded and generic ADHD therapeutics through the 2033 forecast horizon.

Key Industry Highlights:

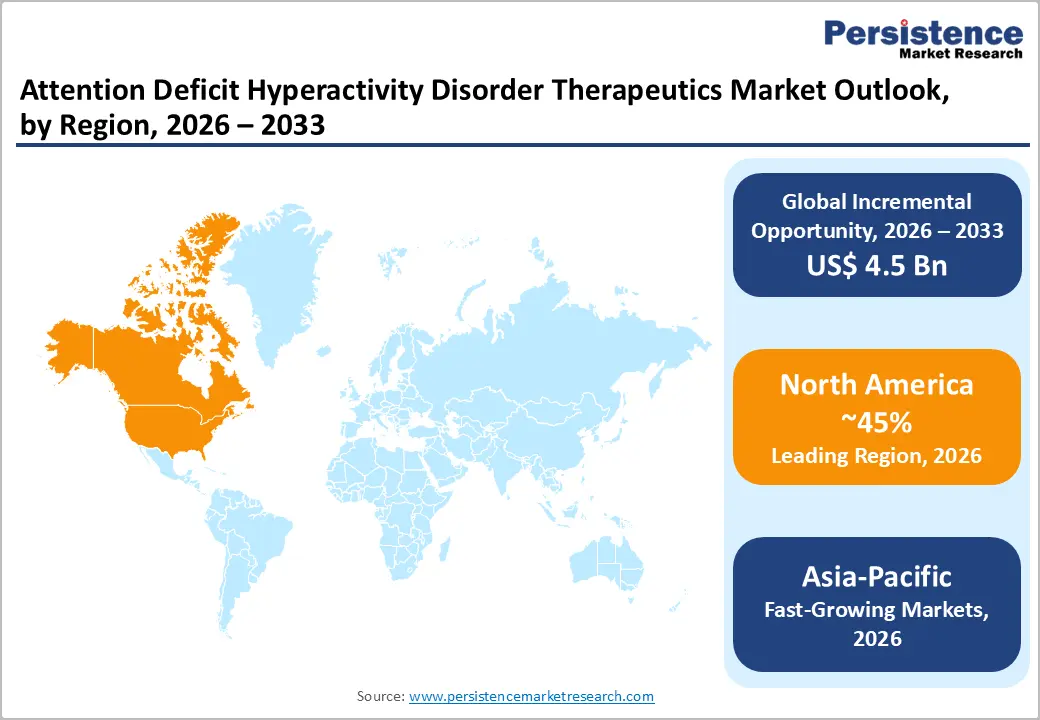

- Regional Leadership: North America leads the global ADHD Therapeutics market with approximately 45% revenue share in 2025, driven by the world's highest ADHD diagnosis rates (CDC: 9.8% of U.S. children), comprehensive insurance coverage, and telehealth-accelerated prescription growth.

- Fast-Growing Market: Asia Pacific is the fast-growing ADHD therapeutics market, driven by improving mental health literacy, DSM-5/ICD-11 adoption, Japan's established stimulant market, China's underpenetrated patient population, and expanding generic manufacturing across ASEAN nations.

- Dominant Drug Class: Stimulants command approximately 76% of drug class revenue in 2025, underpinned by over six decades of clinical evidence, AAP and NICE first-line guideline endorsement, and the continued dominance of branded products such as Vyvanse and Concerta.

- Fast-Growing Drug Class: Non-stimulants are the fast-growing drug class during the forecast period fueled by Supernus' Qelbree (viloxazine ER) adoption, generic atomoxetine availability, and growing demand from stimulant-intolerant patients with comorbid anxiety or cardiovascular conditions.

- Key Opportunity: Telehealth-enabled ADHD diagnosis combined with e-commerce pharmacy distribution represents the most significant growth opportunity, expanding adult ADHD treatment access and medication adherence, particularly as DEA and Congress move toward permanent telemedicine prescribing frameworks for Schedule II drugs.

Market Dynamics

Drivers - Rising ADHD Diagnosis Rates and Growing Adult ADHD Recognition

One of the most significant drivers of the ADHD therapeutics market is the sustained increase in diagnosis rates particularly among adults and previously underdiagnosed populations including women and girls. A landmark study published in JAMA Network Open (2023) found that ADHD diagnosis rates among adults in the U.S. increased by over 15% between 2020 and 2022 alone, partly accelerated by the expansion of telehealth psychiatric services during and after the COVID-19 pandemic.

The Centers for Disease Control and Prevention (CDC) reports that approximately 6 million children aged 3-17 in the U.S. have received an ADHD diagnosis. As adult ADHD awareness grows through clinical education campaigns by bodies such as CHADD (Children and Adults with ADHD) and ADHD Europe, the treatable patient population expands materially, directly increasing prescription volumes and long-term medication adherence.

Restraints - Controlled Substance Regulations and Prescription Access Barriers

ADHD stimulant medications are classified as Schedule II controlled substances under the U.S. Drug Enforcement Administration (DEA) framework, imposing stringent restrictions on prescribing, refilling, and dispensing. These regulations requiring written prescriptions for each refill and limiting supply quantities create access barriers, particularly in rural and underserved communities. In several European and Asian markets, equivalent national narcotic control frameworks further constrain prescribing flexibility.

The administrative burden on prescribers discourages initiation and continuation of ADHD pharmacotherapy, contributing to the significant treatment gap where fewer than 20% of diagnosed ADHD adults globally receive consistent pharmacological treatment, according to the World Journal of Psychiatry.

Opportunities - Non-Stimulant Drug Class as the Fast-Growing Segment: Addressing Unmet Needs

The Non-stimulants segment represents the fastest growing drug class in the ADHD therapeutics market, driven by clinical demand for effective therapies in populations where stimulants are contraindicated or insufficiently tolerated, including patients with comorbid anxiety, substance use history, cardiovascular conditions, and a preference to avoid controlled substances.

Atomoxetine (Strattera, Eli Lilly) remains the most widely prescribed non-stimulant globally, with generic availability now expanding access significantly. Supernus Pharmaceuticals' Qelbree (viloxazine ER), approved by the FDA in 2021 for children and 2022 for adults, has demonstrated strong clinical uptake as a novel selective norepinephrine reuptake inhibitor. Guanfacine and clonidine extended-release products further broaden non-stimulant options, positioning this segment for above-market growth throughout the forecast period.

Category-wise Analysis

Drug Insights

The stimulants segment dominates the ADHD therapeutics market, accounting for approximately 76% of total drug class revenue in 2026. This commanding market position reflects over six decades of clinical evidence supporting stimulant efficacy, with amphetamines and methylphenidate consistently demonstrating >70% response rates across randomized controlled trials cited by the American Academy of Pediatrics (AAP) and NICE (UK) clinical guidelines.

Products including Adderall XR (Teva), Vyvanse (Takeda), Concerta (Johnson & Johnson), and Ritalin LA (Novartis) collectively generate the majority of stimulant segment revenue. The availability of generics for key molecules particularly amphetamine salts and methylphenidate has sustained high prescription volumes while shifting revenue mix. Stimulants' established first-line status in both AAP and EFNS guidelines ensures durable dominance through the forecast period.

Age Group Insights

The pediatric and adolescent age group leads the ADHD therapeutics market, accounting for approximately 58% of age-group revenue in 2026. This segment's dominance is supported by the fact that ADHD is most commonly diagnosed in childhood, with the CDC reporting that the average age of ADHD diagnosis in the U.S. is 7 years old. First-line pharmacotherapy is initiated predominantly in the pediatric and adolescent cohort under American Academy of Pediatrics (AAP) guidelines that recommend stimulant medication for children aged 6 and above as a standard of care.

School-based identification programs across North America and Europe continue to increase diagnosis rates in this age cohort. Importantly, many pediatric patients transition to adult ADHD treatment continuity, making this segment the primary acquisition channel for long-term prescription revenue.

Regional Insights

North America ADHD Therapeutics Market Trends and Insights

North America dominated the ADHD therapeutics market due to high diagnosis rates, strong healthcare infrastructure, rising adult ADHD awareness, and broad access to stimulant and non-stimulant medications. The regional market benefited from increasing prescriptions, expanding telehealth services, and favorable reimbursement systems. The U.S. is the largest contributor, while Canada emerged as a steadily growing market supported by mental health investments and awareness campaigns.

U.S. ADHD Therapeutics Market Trends and Insights

The U.S. led the North American ADHD therapeutics market and was expected to reach nearly US$ 6.4 Bn by 2026 due to increasing ADHD prevalence and prescription drug utilization. According to the CDC, nearly 7 million U.S. children aged 3-17 years had been diagnosed with ADHD in 2022, representing 11.4% of children nationwide. CDC data also showed that around 15.5 million adults had current ADHD diagnoses in 2023.

Rising adult diagnosis rates, widespread stimulant medication usage, and strong insurance coverage significantly supported market expansion. The country also experienced increasing telehealth adoption for ADHD consultations, improving access to psychiatrists and behavioral therapy services.

Canada ADHD Therapeutics Market Trends and Insights

Canada is likely to achieve a CAGR of 4.2% during the forecast period due to increasing mental health awareness and rising pediatric neurodevelopmental disorder diagnoses. Government-backed mental health initiatives and expanded healthcare access encouraged earlier ADHD diagnosis and treatment among children and adolescents. The country also witnessed higher demand for non-stimulant therapies and behavioral treatment programs.

Growing investments in child psychiatry and school-based mental healthcare improved therapeutic adoption. Canadian healthcare providers are increasingly focused on adult ADHD management as awareness of untreated adult ADHD continues to rise. Expanding telemedicine services further strengthened treatment accessibility in remote and underserved populations, supporting long-term therapeutic market growth across the country.

Europe ADHD Therapeutics Market Trends and Insights

Europe represented a significant region in the ADHD therapeutics market due to increasing ADHD diagnosis rates, supportive healthcare systems, and rising focus on child and adolescent mental health. The region benefited from improved clinical guidelines, greater awareness among parents and educators, and growing acceptance of adult ADHD treatment.

Countries such as Germany and the United Kingdom played major roles in market revenue generation, while France emerged as a rapidly growing market because of increasing mental healthcare spending. Expanding use of non-stimulant medications and behavioral therapies also supported regional growth. Europe maintained strong market demand through public healthcare reimbursement systems and continuous psychiatric research initiatives.

Germany ADHD Therapeutics Market Trends and Insights

Germany led the European ADHD therapeutics market and was expected to reach nearly US$ 1.8 Bn by 2026 due to strong psychiatric healthcare infrastructure and rising ADHD diagnosis rates among children and adults. The country benefited from broad reimbursement coverage for ADHD medications and increasing prescriptions of methylphenidate-based therapies. Germany also recorded growing awareness regarding adult ADHD management and behavioral therapy integration.

Rising school-based mental health programs and strong physician accessibility contributed to higher treatment adoption. The country’s healthcare system supported early diagnosis and multidisciplinary ADHD care, including psychotherapy and cognitive behavioral treatment. Increasing research activities in neurodevelopmental disorders further strengthened Germany’s position in the European market.

France ADHD Therapeutics Market Trends and Insights

France was expected to grow with a CAGR of 4.1% during the forecast period due to improving ADHD awareness and expanding psychiatric care services. Historically, ADHD was considered underdiagnosed in France, but increasing educational campaigns and physician training improved recognition of the disorder. Growing pediatric mental health consultations and wider use of ADHD screening tools supported treatment demand.

The French healthcare system also expanded access to behavioral therapy and specialist consultations. Rising attention toward adult ADHD diagnosis further accelerated therapeutic adoption. Additionally, increasing government focus on mental health policies and neurodevelopmental disorder management encouraged pharmaceutical companies to expand ADHD treatment availability across the country.

Asia Pacific ADHD Therapeutics Market Trends and Insights

Asia Pacific is projected to register the fast-growth in the ADHD therapeutics market due to improving mental health awareness, expanding healthcare expenditure, and rising diagnosis rates in developing economies. Increasing urbanization, academic pressure, and greater recognition of neurodevelopmental disorders accelerated treatment demand across the region. Countries such as Japan and China contribute significantly to regional market growth, while India has emerged as a rapidly expanding market because of improving psychiatric healthcare access.

Growing investments in mental healthcare infrastructure and increasing acceptance of behavioral therapy further supported market expansion. Rising healthcare digitization and telepsychiatry adoption also improved access to ADHD diagnosis and treatment services across Asia Pacific countries.

Japan ADHD Therapeutics Market Trends and Insights

Japan led the Asia Pacific ADHD therapeutics market and is expected to reach nearly US$ 1.2 Bn by 2026 due to increasing diagnosis rates and growing acceptance of psychiatric treatment. The country benefited from advanced healthcare infrastructure and rising awareness regarding childhood neurodevelopmental disorders. Japanese studies estimated ADHD prevalence around 3%, supporting long-term treatment demand.

The country also experienced increasing use of non-stimulant medications because of strict regulations surrounding stimulant therapies. Expanding mental healthcare access and strong physician support for behavioral therapy contributed to therapeutic growth. In addition, growing adult ADHD recognition and increasing workplace mental health awareness support the continuous expansion of the ADHD therapeutics market in Japan.

India ADHD Therapeutics Market Trends and Insights

India is likely to expect a CAGR of 5.1% during the forecast period due to rising ADHD awareness, expanding psychiatric services, and improving healthcare accessibility. Increasing academic stress and higher recognition of childhood behavioral disorders encouraged more ADHD screenings in urban hospitals and schools. Government mental health programs and growing telepsychiatry services improved treatment access across semi-urban and rural areas. India also witnessed increasing demand for affordable generic ADHD medications and behavioral therapies.

The growing number of child psychiatrists, rising healthcare expenditure, and stronger parental awareness regarding developmental disorders supported market expansion. Additionally, increasing diagnoses among adolescents and adults created new growth opportunities for ADHD therapeutics in India.

Competitive Landscape

The global ADHD therapeutics market exhibits a moderately consolidated structure, with Takeda Pharmaceutical, Eli Lilly, Johnson & Johnson, Novartis, and Teva Pharmaceutical Industries commanding significant branded and generic revenue positions. Leaders differentiate through extended-release technology platforms, robust controlled-substance compliance infrastructure, and specialty sales forces targeting child psychiatrists and primary care prescribers.

Supernus Pharmaceuticals and Neos Therapeutics compete with differentiated novel delivery system formulations. Generic manufacturers, including Amneal Pharmaceuticals and Mallinckrodt Pharmaceuticals, sustain volume competition in post-patent molecules. An emerging competitive dynamic is the entry of digital therapeutics companies and telehealth-integrated prescription platforms, challenging traditional pharma-only commercial models.

Key Developments:

- January 2026: Treatment approaches for ADHD had increasingly shifted beyond traditional stimulant medications such as Ritalin and Adderall, as researchers and pharmaceutical companies focused on developing non-stimulant therapies and alternative interventions. The move was driven by concerns over stimulant side effects, misuse potential, drug shortages, and limited effectiveness in some patients.

- November 2025: Pfizer Inc. agreed to a $41.5 million settlement with the state of Texas over allegations related to the marketing of an ADHD drug for children. The lawsuit claimed that the company had misleadingly promoted the medication and provided inaccurate information regarding its safety and effectiveness for pediatric use.

- November 2025: Otsuka Pharmaceutical Co., Ltd. submitted a New Drug Application (NDA) to the U.S. Food and Drug Administration for centanafadine, an investigational once-daily therapy for attention-deficit/hyperactivity disorder (ADHD) in children, adolescents, and adults. The company stated that centanafadine is a first-in-class norepinephrine, dopamine, and serotonin reuptake inhibitor (NDSRI).

Companies Covered in Attention Deficit Hyperactivity Disorder Therapeutics Market

- Pfizer Inc.

- Eli Lilly and Company

- Novartis AG

- GlaxoSmithKline PLC

- Mallinckrodt Pharmaceuticals

- Hisamitsu Pharmaceutical Co., Inc.

- Johnson & Johnson

- UCB S.A.

- Purdue Pharma L.P.

- Takeda Pharmaceutical Company

- Supernus Pharmaceuticals

- Teva Pharmaceutical Industries Ltd.

- Neos Therapeutics

- Tris Pharma

- Others

Frequently Asked Questions

The global ADHD therapeutics market is estimated to be valued at US$ 15.9 billion in 2026.

Rising ADHD prevalence, increasing diagnosis rates, growing awareness, improved treatment access, and expanding pediatric patient population.

North America leads with approximately 45% of global revenue in 2025, driven by the world's highest ADHD diagnosis and treatment rates, robust FDA-regulated pharmaceutical infrastructure and comprehensive insurance reimbursement.

Development of non-stimulant therapies, digital therapeutics, adult ADHD treatments, and expanding healthcare access globally.

Pfizer Inc., Eli Lilly and Company, Novartis AG, GlaxoSmithKline PLC, Mallinckrodt Pharmaceuticals, Hisamitsu Pharmaceutical Co., Inc.