- Medical Devices

- Acrylic Teeth Market

Acrylic Teeth Market Size, Share, and Growth Forecast, 2026 - 2033

Acrylic Teeth Market by Product Type (Complete Dentures, Partial Dentures, Overdentures), Manufacturing Technology (Traditional Fabrication, CAD/CAM Dentures, 3D Printed Dentures), End-User (Dental Clinics, Dental Laboratories, Hospitals), and Regional Analysis for 2026 - 2033

Acrylic Teeth Market Share and Trends Analysis

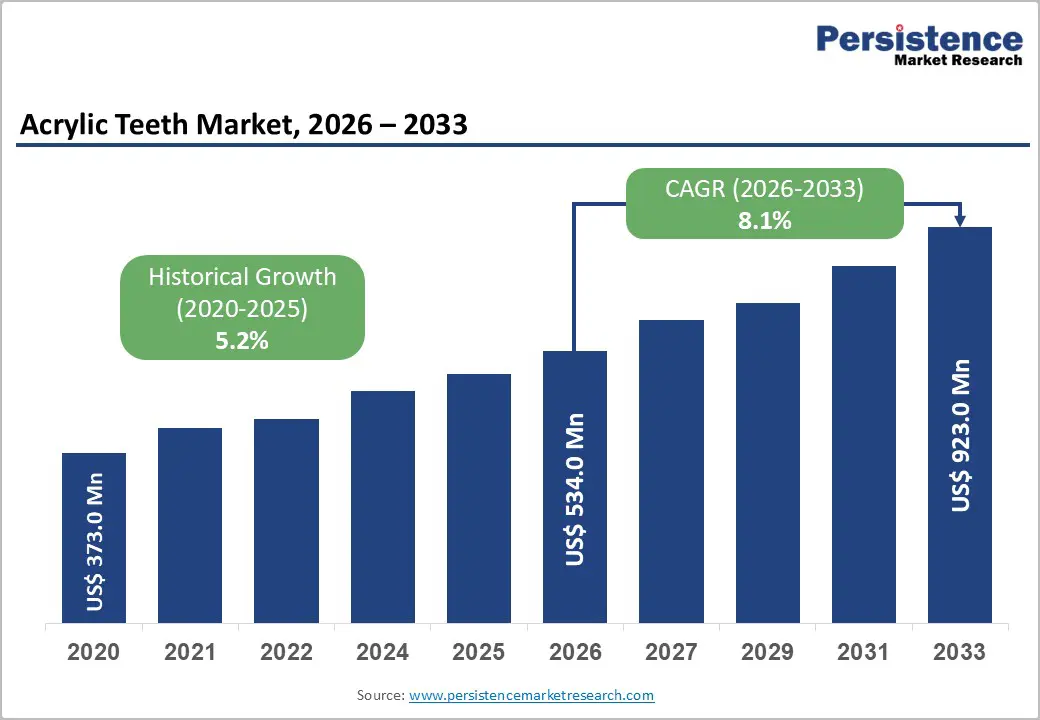

The global acrylic teeth market size is likely to be valued at US$ 534.0 million in 2026, and is projected to reach US$ 923.0 million by 2033, growing at a CAGR of 8.1% during the forecast period 2026–2033. The market is expanding due to rising global edentulism rates, aging populations, and the increasing adoption of digital dentistry technologies such as CAD/CAM and 3D printing.

According to the World Health Organization (WHO), severe tooth loss affects a significant proportion of adults worldwide, particularly those aged above 60, which increases the demand for dentures and prosthetic treatments. As the elderly population grows across developed and developing regions, the need for affordable restorative dental solutions is set to soar. Acrylic teeth remain widely preferred due to their cost-effectiveness, ease of adjustment, and satisfactory aesthetics. In emerging markets especially, affordability and accessibility strongly influence treatment decisions, further supporting the adoption of acrylic denture materials.

Key Industry Highlights

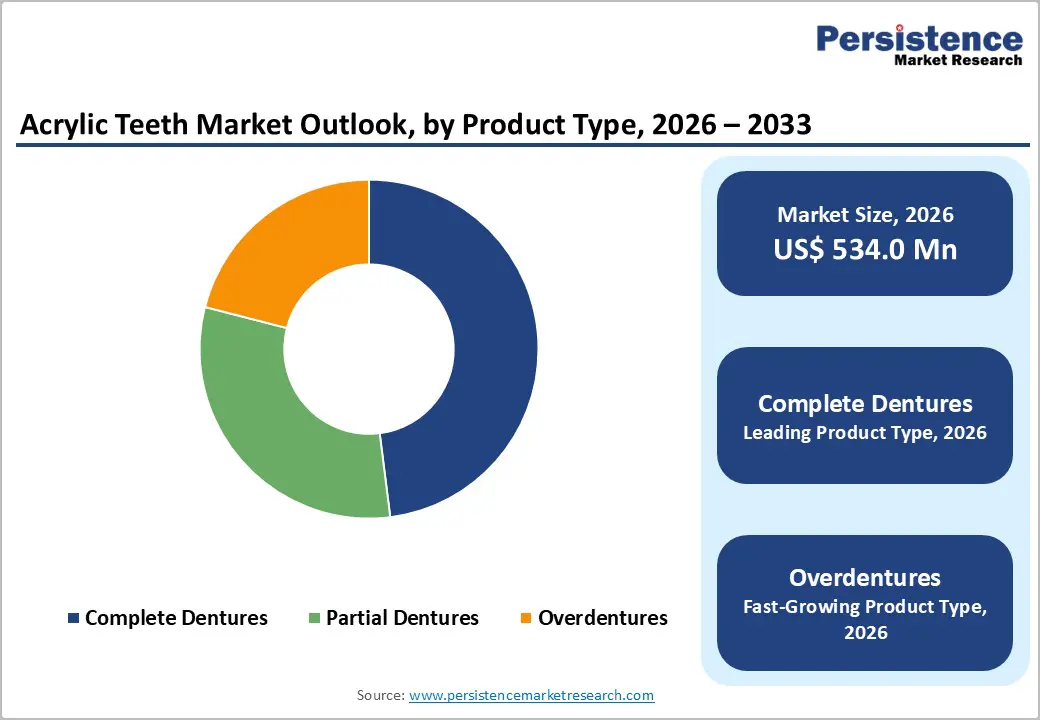

- Dominant Product Type: Complete dentures are projected to command around 48% revenue share in 2026, while overdentures are likely to grow the fastest at about 9.4% CAGR through 2033, supported by increasing adoption of implant-supported prosthetic treatments.

- Leading Technology: Traditional fabrication is anticipated to lead with approximately 54% revenue share in 2026, and 3D printed dentures are expected to grow the fastest during 2026–2033, driven by rapid digital dentistry adoption.

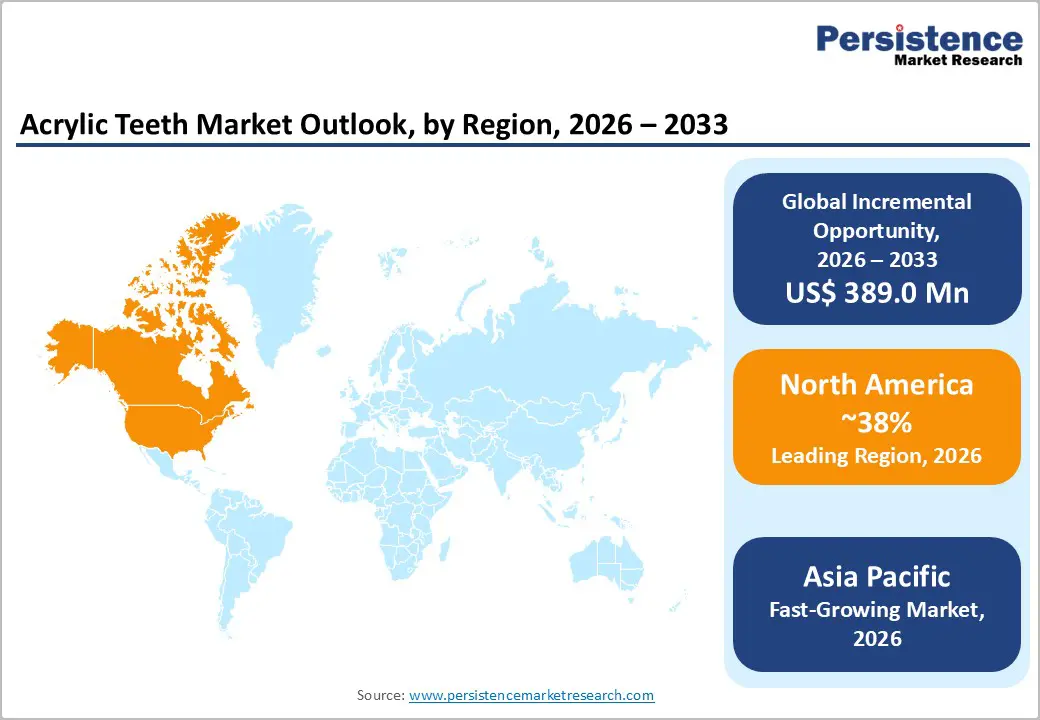

- Regional Leadership: North America is projected to lead with an estimated 38% share in 2026, while Asia Pacific is expected to grow the fastest at around 8.9% CAGR through 2033, aided by expanding dental care infrastructure.

- Competitive Environment: Market competition is characterized by digital denture technology launches, manufacturing expansions, and strategic partnerships, enabling companies to strengthen distribution networks.

| Key Insights | Details |

|---|---|

|

Substation Automation Market Size (2026E) |

US$ 534.0 Mn |

|

Market Value Forecast (2033F) |

US$ 923.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Burden of Tooth Loss and Aging Population

One of the strongest drivers of the acrylic teeth market is the growing prevalence of edentulism and tooth decay among the aging population. The WHO estimates that approximately 3.5 billion people globally suffer from oral diseases, including tooth loss and periodontal conditions. Furthermore, the United Nations Department of Economic and Social Affairs (UN DESA) projects that the global population aged 65 years and above will reach 1.6 billion by 2050, significantly increasing demand for dentures and restorative dental treatments. As life expectancy continues to rise across both developed and developing economies, the incidence of age-related dental conditions is also increasing. This demographic trend is creating sustained demand for removable prosthetic solutions such as dentures, encouraging wider adoption of acrylic denture teeth in restorative dentistry.

Government-led oral health programs are also strengthening the demand for dentures and prosthetic materials. For example, in 2025 the United Kingdom’s National Health Service (NHS) expanded dental care funding to improve access to prosthodontic treatments, including dentures, particularly for elderly and low-income patients. The initiative focuses on reducing waiting times for restorative dental procedures and improving oral health outcomes among vulnerable populations. Such public healthcare efforts highlight the growing policy emphasis on oral rehabilitation and denture accessibility. As more governments integrate dental care into national healthcare frameworks, demand for affordable denture materials like acrylic teeth is expected to increase steadily across both developed and emerging economies.

Growth in Dental Prosthetics Demand and Advancements in Digital Denture Manufacturing

Increasing awareness regarding oral aesthetics and prosthetic rehabilitation is contributing significantly to the growth of acrylic teeth demand. The American Dental Association (ADA) reports that over 120 million Americans are missing at least one tooth, while approximately 36 million individuals have no natural teeth remaining, highlighting the strong need for denture and prosthetic solutions. Tooth loss affects chewing function, speech clarity, and facial appearance, prompting more patients to seek restorative dental treatments. As a result, dental professionals increasingly rely on acrylic denture teeth for complete and partial denture treatments due to their balance of affordability, functionality, and aesthetic acceptability.

Technological innovation in dental manufacturing is further accelerating market growth. The emergence of CAD/CAM denture fabrication and 3D printing technologies has transformed traditional dental laboratory workflows by enabling highly precise and efficient denture production. Industry events such as the International Dental Show (IDS) 2025, which featured over 2,500 exhibitors from 64 countries, highlighted the rapid expansion of digital dentistry technologies including intraoral scanners, cloud-connected dental platforms, and 3D printed dentures. Additionally, in July 2025 the U.S. Food and Drug Administration (FDA) cleared a new fully digital denture solution for commercial release, demonstrating increasing regulatory acceptance of digitally manufactured dentures. These developments reinforce the accelerating shift toward digital denture production using acrylic-based prosthetic materials.

Competition from Alternative Materials such as Ceramic and Composite Teeth

One of the primary restraints affecting the acrylic teeth market growth is the growing availability of alternative prosthetic materials such as ceramic and composite denture teeth. Ceramic teeth offer higher wear resistance and superior aesthetics, which makes them attractive for premium dental restorations. Many patients seeking long-term prosthetic solutions increasingly prefer materials that provide enhanced durability and a more natural appearance. Advances in dental materials science have expanded the range of prosthetic options available to clinicians. As a result, dentists can now recommend highly aesthetic restorations tailored to patient expectations. This broader material selection has intensified competition for traditional acrylic denture teeth in several prosthodontic procedures.

However, these alternatives come with higher costs and more complex manufacturing processes, which limits their adoption in cost-sensitive markets. In 2025, dental laboratories in developed markets increasingly adopted hybrid denture materials to meet patient demand for long-lasting prosthetics and improved aesthetics. Modern restorative materials such as ceramic-reinforced composites and zirconia-based prosthetics are gaining attention due to their strength and natural appearance. These developments reflect a gradual shift toward high-performance dental materials in advanced prosthodontic treatments. As dental laboratories continue experimenting with newer restorative materials, acrylic denture teeth face growing competition in premium dental applications. This evolving material landscape could moderately limit acrylic teeth adoption in high-end restorative procedures.

Limited Access to Dental Care in Developing Regions

Despite growing demand, limited access to dental care services remains a challenge for the acrylic teeth market in many low-income regions. According to the WHO and other global health agencies, shortages of trained dental professionals and inadequate healthcare infrastructure continue to affect oral healthcare accessibility. Many rural and underserved communities lack sufficient dental clinics and prosthodontic specialists. These structural limitations reduce the availability of restorative procedures such as dentures and implant-supported prosthetics. As a result, large populations with untreated tooth loss remain outside the formal dental treatment system. This gap between oral health needs and service availability continues to slow the adoption of prosthetic dental solutions.

Recent industry developments further highlight this challenge. In 2026, reports from Healthwatch England indicated that nearly 32% of patients in England had shifted to private dental care due to limited availability of public dental services, reflecting increasing access barriers within national healthcare systems. Furthermore, workforce shortages have forced many regions to implement policy changes to expand the dental workforce and improve patient access to care. These developments demonstrate the growing pressure on dental healthcare systems worldwide. When dental services remain inaccessible or expensive, patients often delay or avoid prosthodontic treatment. Consequently, restricted access to dental care continues to act as a structural restraint on the overall acrylic teeth market.

Expansion of Dental Care Infrastructure in Emerging Markets

The burgeoning economies of India, China, Brazil, and Southeast Asian countries present significant growth opportunities for acrylic teeth manufacturers. Governments across these regions are investing in public dental health programs and expanding oral healthcare infrastructure to improve treatment accessibility. Rising healthcare spending and increasing awareness of oral health are encouraging more people to seek professional dental care. In several countries, public health authorities are prioritizing preventive dentistry and restorative treatments as part of broader healthcare strategies. As a result, dental services such as dentures and prosthodontic rehabilitation are becoming more widely available. This expansion of healthcare infrastructure is expected to significantly support demand for denture materials.

For instance, several countries implemented national oral health initiatives in 2025 aimed at improving dental screening and prosthetic rehabilitation services. The Government of Canada expanded the Canadian Dental Care Plan (CDCP) in 2025, enabling nearly six million Canadians to receive dental care, including restorative treatments such as dentures. The program also supports training and infrastructure projects designed to improve access to oral healthcare services nationwide. Such initiatives demonstrate increasing government commitment to improving oral health accessibility and affordability. As healthcare systems expand dental coverage and treatment capacity, demand for prosthetic solutions including acrylic denture teeth is expected to rise steadily.

Rapid Growth of Digital Dentistry and Demand for Affordable Prosthetic Solutions

The adoption of digital dentistry platforms, including intraoral scanners, CAD/CAM software, and additive manufacturing systems, is opening new growth avenues for the acrylic teeth market. These technologies allow dental laboratories to design and fabricate dentures more efficiently while improving clinical precision. Digital workflows enable faster denture production, reducing treatment time for patients and improving workflow efficiency for dentists and technicians. Acrylic denture teeth remain widely used in digitally fabricated dentures due to their flexibility and compatibility with modern manufacturing techniques. As digital dentistry continues to advance, prosthetic materials that integrate easily with digital workflows are gaining strong market traction.

Recent industry developments further highlight this opportunity. In July 2025, 3D Systems announced the commercial release of its U.S. FDA-cleared NextDent digital denture solution, which enables laboratories to produce single-piece multi-material dentures through advanced 3D printing technology. The system significantly improves manufacturing efficiency and denture durability, demonstrating the growing integration of additive manufacturing in dental prosthetics. Such innovations illustrate how digital technologies are reshaping denture fabrication and enabling scalable production of prosthetic solutions. As dental clinics and laboratories continue adopting digital workflows, manufacturers of acrylic denture materials are expected to benefit from increasing demand for digitally compatible prosthetic products.

Category-wise Analysis

Product Type Insights

Complete dentures are projected to account for around 48% of the acrylic teeth market revenue share in 2026, serving patients who have lost all teeth in one or both jaws. Acrylic teeth remain preferred for their balance of aesthetics, comfort, and ease of customization, enabling natural tooth replication. High edentulism rates, particularly among elderly populations, and affordability drive widespread adoption in clinics and prosthodontic centers. Digital workflows are increasingly used; for example, the Government Dental College and Research Institute in Bengaluru introduced digital intra-oral scanning and 3D printing in early 2026, enhancing precision, reducing production time, and reinforcing the segment’s leading market position.

Overdentures are expected to be the fastest-growing product segment at a CAGR of approximately 9.4% from 2026 to 2033, driven by the rising adoption of implant-supported denture systems. They offer improved stability, comfort, and chewing efficiency compared with conventional dentures, while acrylic teeth provide a cost-effective prosthetic option. Growth is supported by expanding implant procedures and digital workflows that enhance treatment accuracy. For instance, in 2025, multiple clinics in Europe and North America implemented CAD/CAM-assisted overdenture fabrication, improving patient outcomes and treatment efficiency. The combination of functional benefits, affordability, and technological integration positions overdentures as a high-growth opportunity in the market.

Manufacturing Technology Insights

Traditional denture fabrication is projected to hold approximately 54% of the acrylic teeth market share in 2026, remaining dominant due to established workflows, low equipment costs, and technician familiarity. Manual techniques such as wax modeling, flasking, and heat-polymerized acrylic processing ensure reliable and customizable outcomes. In regions with limited digital infrastructure, conventional fabrication is practical and accessible. Many dental laboratories continue using these methods for complete and partial dentures, prioritizing cost efficiency and hands-on quality control. Its widespread adoption in both developed and developing markets cements traditional fabrication as the backbone of the acrylic teeth industry.

3D printed dentures are poised to be the fastest-growing manufacturing segment, with a CAGR of 11.3% during 2026–2033, driven by additive manufacturing and digital design adoption. Digital workflows allow precise, faster, and reproducible denture fabrication with acrylic-based printable resins, reducing material waste and turnaround time. In 2025, U.S. FDA-cleared multi-material 3D denture printing systems were introduced in the U.S., enabling high-quality, durable prosthetics and expanding clinic adoption. As digital dentistry becomes standard practice, 3D printed acrylic dentures are expected to gain significant market share, combining efficiency, precision, and cost-effective production to meet growing patient demand.

Regional Insights

North America Acrylic Teeth Market Trends

North America is expected to account for around 38% of the acrylic teeth market value in 2026, due to its advanced dental healthcare infrastructure, high prosthodontic demand, and strong regulatory oversight. The United States leads regional performance with millions of adults requiring dentures due to aging-related tooth loss. The U.S. FDA continues to enforce strict device quality standards, ensuring reliability of denture materials and prosthetic systems. Dental clinics and labs in the region widely adopt digital denture workflows, including CAD/CAM and intraoral scanning, to increase accuracy and speed of production. These capabilities improve clinical outcomes and patient satisfaction. High levels of dental insurance coverage further support treatment accessibility for prosthodontic care.

In 2026, the U.S. Department of Veterans Affairs expanded its dental care eligibility criteria for older veterans, specifically including coverage for prosthodontic treatments such as complete and partial dentures. This policy change was widely reported in national media and underscores growing institutional support for restorative dental care among priority patient groups. Such government-backed dental program expansions are expected to drive incremental demand for acrylic teeth in complete and partial denture applications. Combined with ongoing investment in dental research and digital technologies, these developments reinforce North America’s leading market position and continued growth through the forecast period.

Europe Acrylic Teeth Market Trends

Europe represents a mature market for acrylic teeth, with steady expansion supported by well-established dental healthcare systems and regulatory harmonization under the European Union (EU) Medical Device Regulation (MDR). Key markets such as Germany, the United Kingdom, France, and Spain contribute significant market share due to advanced dental clinic networks and high levels of patient awareness around oral health. Acrylic teeth maintain strong usage in both conventional and digitally assisted denture workflows across the region. European clinics increasingly integrate chairside CAD/CAM systems to boost prosthetic accuracy and reduce patient visits, reflecting broader digital adoption trends within clinical practice.

Several European dental institutes participated in a cross-country digital dentistry collaboration program aimed at standardizing CAD/CAM denture fabrication practices, which was covered by regional health news outlets. This initiative allows clinics across member countries to share best practices and improve access to digital prosthetic workflows. Additionally, the French Ministry of Health launched a subsidized oral rehabilitation program in mid-2026, expanding coverage for denture treatments for low-income seniors, a development widely reported by national media. These policy measures, combined with Europe’s strong regulatory framework and commitment to dental innovation, support continued demand for acrylic teeth and reinforce steady regional market growth.

Asia Pacific Acrylic Teeth Market Trends

Asia Pacific is poised to be the fastest-growing regional market for acrylic teeth, with an estimated CAGR of around 8.9% from 2026 to 2033, driven by a large population base, expanding dental healthcare infrastructure, and cost-sensitive patient segments. China, Japan, India, and Southeast Asian nations are key growth engines. China has rapidly scaled dental clinics and prosthodontic training programs, while Japan’s aging population fuels ongoing demand for dentures and restorative care. India and ASEAN countries have invested heavily in community oral health initiatives, increasing public awareness and uptake of prosthetic treatments. Acrylic teeth are frequently preferred due to their cost effectiveness and compatibility with both traditional and digital denture workflows.

In 2025, the Ministry of Health and Family Welfare in India announced the launch of a nationwide oral health initiative, which included subsidized denture services within public hospitals and community clinics, a program widely covered by national news outlets. The initiative aims to expand access to restorative dental services for rural and low-income populations and is expected to increase prosthodontic treatment volumes. Pakistan and Malaysia reported expansion of regional dental colleges and government-backed prosthetic labs in 2026, improving training capacity and patient access to dentures. These developments demonstrate how public healthcare investments are strengthening dental treatment ecosystems across Asia Pacific, reinforcing its role as the fastest-growing regional market for acrylic teeth.

Competitive Landscape

The global acrylic teeth market structure is moderately consolidated, with leading players such as Ivoclar Vivadent, Dentsply Sirona, GC Corporation, and Kuraray Noritake Dental collectively accounting for over 50% of market revenue in 2026. These established companies leverage extensive distribution networks, strong relationships with dental laboratories and clinics, and expertise in dental material science. They invest significantly in R&D for advanced acrylic formulations, color stability, and digitally compatible denture teeth, maintaining technological leadership and product differentiation in both conventional and digital denture workflows.

Regional and niche competitors, including Nissin Dental Products and Dental Arts Laboratories, focus on specialized prosthetic solutions and local market strongholds. Entry barriers such as strict regulatory approvals, material biocompatibility standards, and high-quality manufacturing requirements limit new entrants. However, trends in digital dentistry, CAD/CAM systems, and 3D printed dentures are enabling innovation from smaller and software-enabled dental technology firms. Market consolidation is expected to rise gradually as global leaders acquire regional producers, expand geographically, and form strategic partnerships for digital denture technologies, while specialized labs continue offering tailored prosthetic solutions for growing clinical demand.

Key Industry Developments

- In March 2026, Stratasys received CE Class IIa certification for its TrueDent resins, making it Europe’s first monolithic, high-aesthetic 3D-printed denture solution and enabling broader clinical use. The certification expands applications to long-term intraoral use such as dentures, crowns, and bridges, while supporting scalable digital workflows and strengthening adoption across European dental laboratories.

- In December 2025, SprintRay acquired the dental segment of EnvisionTEC, including patents and intellectual property for 3D printing and dental materials. This strategic move enhanced SprintRay’s position in additive manufacturing for dental prosthetics, enabling faster, precise, and digitally integrated acrylic denture production.

- In December 2025, Standard Dental Labs signed an agreement to acquire Dream Dentistry Labs in Florida, consolidating lab operations and expanding its geographic service offerings. This acquisition strengthens its manufacturing footprint, improves supply chain efficiency, and supports faster delivery of acrylic dentures and related prosthetic solutions.

Companies Covered in Acrylic Teeth Market

- Dentsply Sirona Inc.

- Ivoclar Group

- Kulzer GmbH

- SHOFU Inc.

- Yamahachi Dental Mfg. Co., Ltd.

- New Stetic S.A.

- Major Prodotti Dentari S.p.A.

- VITA Zahnfabrik H. Rauter GmbH & Co. KG

- Ruthinium Group

- GC Corporation

- Heraeus Kulzer

- Huge Dental

- Shanghai Pigeon Dental Manufacturing

- Toros Dental

Frequently Asked Questions

The global acrylic teeth market is projected to reach US$ 534.0 million in 2026.

Rising global edentulism, aging populations, and increasing adoption of digital dentistry technologies are driving the market.

The market is poised to witness a CAGR of 8.1% from 2026 to 2033.

Expansion of dental care infrastructure in emerging markets and rapid adoption of digital denture technologies are opening key market opportunities.

Ivoclar Vivadent, Dentsply Sirona, GC Corporation, and Kuraray Noritake Dental are some of the leading market players.