- Medical Devices

- 3D Medical Imaging Devices Market

3D Medical Imaging Devices Market Size, Share, and Growth Forecast, 2026 - 2033

3D Medical Imaging Devices Market by Product Type (MRI Systems, CT Scanners, Ultrasound Imaging Systems, Others), Application (Cardiology, Oncology, Others), End-user (Hospitals, Diagnostic Imaging Centers, Others), and Regional Analysis for 2026 - 2033

3D Medical Imaging Devices Market Share and Trends Analysis

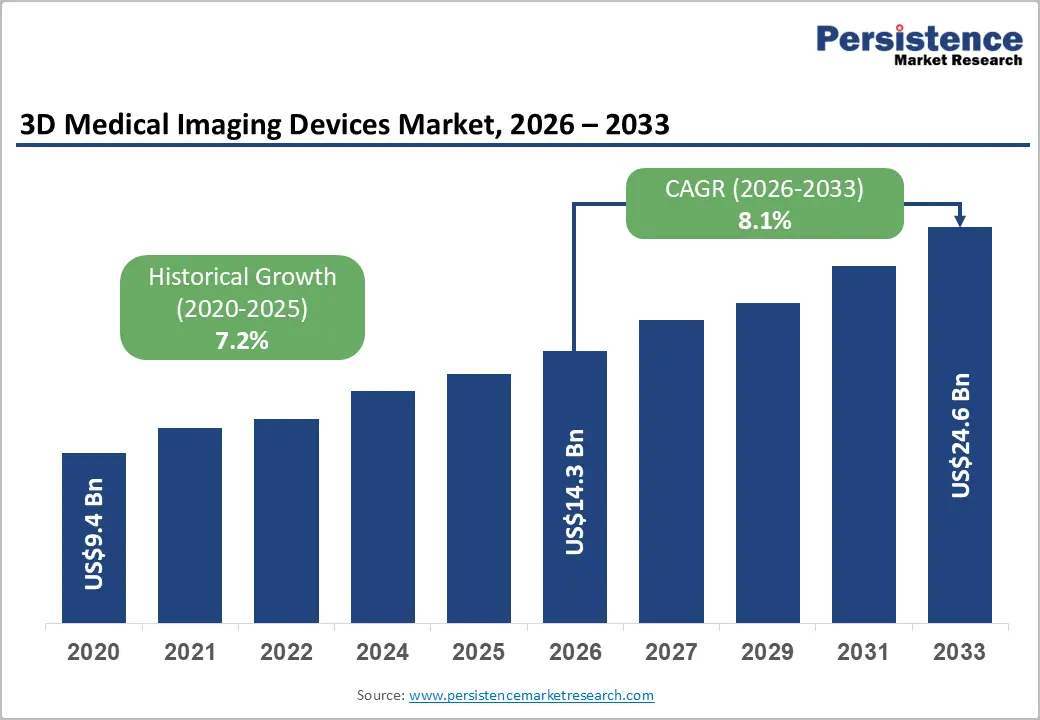

The global 3D medical imaging devices market size is likely to be valued at US$14.3 billion in 2026 and is estimated to reach US$24.6 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by rising chronic disease burden, expansion of diagnostic infrastructure, and rapid integration of artificial intelligence-enabled imaging technologies.

Increasing elderly population levels and higher incidence of cardiovascular, neurological, and oncological disorders are strengthening demand for precision imaging platforms across clinical environments. Regulatory approvals for advanced imaging software and radiation-optimized systems are accelerating product commercialization and hospital procurement activities.

Key Industry Highlights:

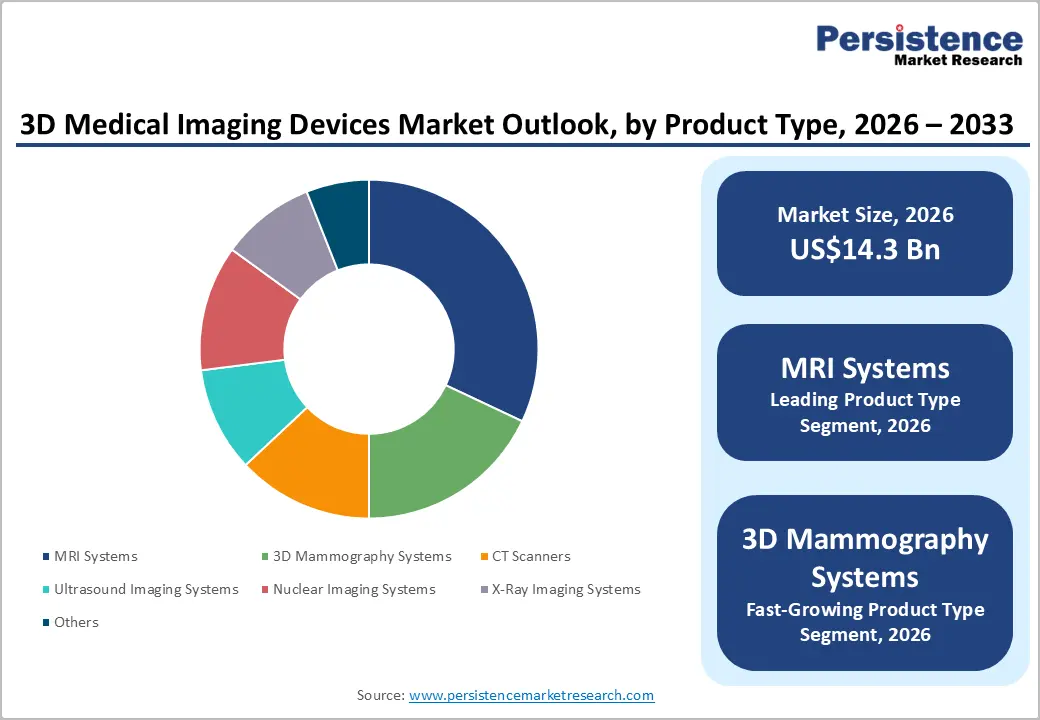

- Leading Product Type: MRI systems are set to hold around 32% of the market share in 2026, driven by broad clinical adoption across neurology and oncology departments.

- Fastest-growing Product Type: 3D mammography systems are projected as the fastest-growing segment, supported by national breast cancer screening mandates and tomosynthesis-based clinical preference.

- Leading Application: Oncology is estimated to hold roughly 34% of the market share in 2026, due to rising global cancer incidence and the clinical requirement for precise tumor localization in treatment planning.

- Fastest-growing Application: Dental imaging is forecast to record the fastest growth, driven by the rapid adoption of cone beam CT in private dental practices for implantology and orthodontic planning.

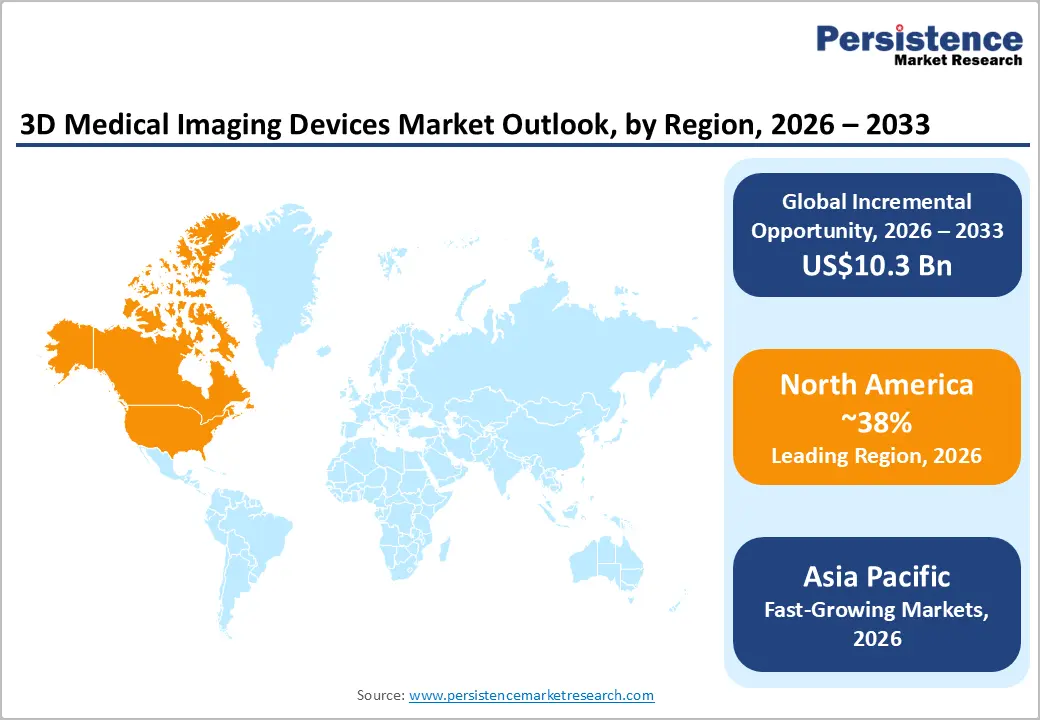

- Regional Leadership: North America is projected to capture approximately 38% of the global market share in 2026, while Asia Pacific is forecast to record the fastest regional growth due to government-led hospital infrastructure expansion programs.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as GE HealthCare and Siemens Healthineers leveraging AI integration, global service networks, and long-term hospital procurement relationships to maintain competitive positioning.

DRO Analysis

Driver - Rising Chronic Disease Burden and Aging Population

The increasing prevalence of cancer, cardiovascular disorders, musculoskeletal conditions, and neurological diseases is accelerating dependence on high-resolution diagnostic imaging systems. Aging demographics are increasing demand for early-stage disease detection and image-guided treatment planning across hospitals and specialty clinics. According to the United States Centers for Disease Control and Prevention (CDC), nearly 129 million individuals in the U.S. were living with at least one major chronic disease in 2025, creating sustained diagnostic imaging requirements.

Growing patient volumes are encouraging healthcare providers to expand advanced imaging infrastructure capable of delivering accurate anatomical visualization and improved diagnostic precision. Three-dimensional reconstruction technologies are reducing diagnostic uncertainty in complex procedures involving oncology and cardiovascular care. Integration of artificial intelligence-assisted interpretation tools is strengthening workflow productivity, reducing reporting delays, and improving patient throughput across radiology departments.

Restraint - Workforce Shortages and Imaging Interpretation Bottlenecks

Shortage of trained radiologists, imaging technicians, and biomedical engineers is restricting optimal utilization of advanced imaging platforms. Healthcare institutions in developing healthcare systems face challenges in maintaining standardized imaging quality and interpretation accuracy. Limited workforce availability delays diagnostic turnaround times and reduces equipment productivity.

Complex software integration and imaging data management requirements are increasing training burdens across healthcare facilities. Artificial intelligence integration requires continuous technical support and workflow adaptation, creating operational inefficiencies during implementation phases. Workforce limitations also reduce scalability of advanced imaging deployment within rural healthcare institutions and community-based diagnostic environments.

Opportunity - Integration of Artificial Intelligence in Imaging Diagnostics

Artificial intelligence-enabled reconstruction, automated segmentation, and predictive analytics capabilities are creating opportunities for imaging providers to improve diagnostic efficiency and clinical accuracy. AI-supported imaging reduces interpretation variability and enhances detection of abnormalities within oncology, cardiology, and neurology applications. Regulatory approvals for AI-based imaging software are accelerating commercialization opportunities for technology developers and healthcare providers.

Healthcare systems are expanding investments in intelligent imaging ecosystems capable of supporting personalized medicine strategies and workflow automation. Companies are introducing cloud-based diagnostic platforms that enable remote collaboration and real-time imaging interpretation. Strategic partnerships between imaging manufacturers and software developers are creating scalable opportunities for integrated diagnostic ecosystems across hospitals and outpatient imaging facilities.

Category-wise Analysis

Product Type Insights

MRI systems are anticipated to secure around 32% of the 3D medical imaging devices market share in 2026, reflecting broad clinical adoption driven by superior soft-tissue contrast resolution in neurology and oncology. Siemens Healthineers' MAGNETOM Free. Max exemplifies how innovation is expanding deployment settings. Continuous demand from tertiary care hospitals and AI-based motion correction integration support sustained revenue leadership for this segment.

3D mammography systems are expected to be the fastest-growing segment, propelled by national breast cancer screening mandates and elevated public awareness programs. Hologic's Dimensions platform, widely deployed across U.S. screening networks, demonstrates clinical preference for tomosynthesis-based detection. Government-backed screening expansion programs in Europe and Asia Pacific are creating structured procurement demand that accelerates installed base growth.

Application Insights

Oncology is poised to dominate with a forecast market share of over 34% in 2026, powered by rising global cancer incidence and the clinical necessity of precise tumor localization for surgical and radiation planning. The deployment of PET-CT imaging protocols at major oncology centers such as MD Anderson Cancer Center reflects current clinical standards. Expanded reimbursement coverage for diagnostic imaging in cancer care pathways reinforces the commercial dominance of this segment.

Dental imaging is estimated to be the fastest-growing segment, fueled by the rapid adoption of cone beam computed tomography in private dental practices. Planmeca's ProMax 3D system, widely adopted in European dental clinics, exemplifies the transition from 2D panoramic imaging to volumetric 3D diagnostics. Declining equipment costs and expanding dental insurance coverage are structurally broadening adoption across outpatient dental settings.

End-user Insights

Hospitals are likely to be the leading segment with a projected 48% of the 3D medical imaging devices market share in 2026 due to centralized budget authority and multi-specialty imaging requirements. The Mayo Clinic's multi-site deployment of integrated imaging suites illustrates how large hospital systems drive volume purchasing decisions. Ongoing hospital capacity expansion programs in North America, Europe, and Asia Pacific maintain a robust equipment procurement pipeline.

Ambulatory surgical centers are anticipated to be the fastest-growing segment, fueled by the shift of diagnostic and surgical procedures from inpatient to cost-efficient outpatient environments. Regulatory changes by the U.S. Centers for Medicare and Medicaid Services, expanding approved outpatient procedures, are directly increasing imaging equipment requirements at these facilities. The lower cost structure of ambulatory centers makes them attractive targets for compact 3D imaging system deployments.

Regional Insights

North America 3D Medical Imaging Devices Market Trends

North America is expected to lead with an estimated 38% of the 3D medical imaging devices market share in 2026, supported by a concentration of academic medical centers, robust private insurance reimbursement, and an established regulatory infrastructure that accelerates device commercialization.

U.S. 3D Medical Imaging Devices Market Insights

The U.S. is projected to account for nearly 79% of the North America 3D medical imaging devices market share in 2026, driven by high diagnostic imaging volumes, widespread hospital digitization, and increasing chronic disease prevalence. Federal investments supporting healthcare interoperability are accelerating integration of AI-assisted imaging platforms.

Canada 3D Medical Imaging Devices Market Insights

Canada is forecast to hold approximately 13% of the North America 3D medical imaging devices market share in 2026, supported by government investments in MRI and CT modernization programs. Provincial healthcare authorities are increasing procurement of advanced imaging equipment to reduce patient waiting periods and improve diagnostic accessibility.

Europe 3D Medical Imaging Devices Market Trends

Europe is projected to capture nearly 27% share in 2026, supported by aging population growth, expanding cancer screening programs, and strong regulatory focus on low-radiation imaging systems. Philips and Canon Medical Systems Corporation are strengthening software interoperability and workflow automation capabilities.

Germany 3D Medical Imaging Devices Market Insights

Germany is expected to account for nearly 24% of the European share in 2026, supported by advanced hospital infrastructure and strong investment in precision diagnostics technologies. Public healthcare modernization initiatives are encouraging the procurement of AI-enabled MRI and CT systems across tertiary healthcare facilities.

France 3D Medical Imaging Devices Market Insights

France is likely to hold around 16% of the European share in 2026, driven by rising diagnostic imaging utilization and healthcare digitization initiatives. National healthcare programs focused on breast cancer screening are increasing the deployment of advanced mammography systems and low-dose imaging technologies.

Asia Pacific 3D Medical Imaging Devices Market Trends

Asia Pacific is forecast to be the fastest-growing regional market, stimulated by rapid healthcare infrastructure expansion, rising patient population, and increasing government healthcare expenditure. Fujifilm Holdings Corporation and Samsung Medison are expanding regional commercialization strategies for advanced imaging systems. Rising medical tourism and smart hospital investments are strengthening imaging technology adoption.

China 3D Medical Imaging Devices Market Insights

China is projected to account for nearly 31% of the Asia Pacific share in 2026, supported by rapid hospital expansion and increasing healthcare digitization initiatives. Government reforms promoting domestic imaging equipment manufacturing are accelerating commercialization of advanced diagnostic technologies.

India 3D Medical Imaging Devices Market Insights

India is forecast to hold approximately 19% of the Asia Pacific share in 2026, driven by the expansion of private diagnostic chains, increasing healthcare insurance penetration, and rising demand for early-stage disease detection. Government healthcare modernization programs are improving accessibility to advanced imaging technologies across secondary and tertiary healthcare facilities.

Competitive Landscape

The global 3D medical imaging devices market is moderately consolidated, with a defined group of large-scale multinationals commanding the majority of the installed base. GE HealthCare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Hologic collectively account for an estimated 60–65% of global revenue. Their competitive positions are sustained by integrated product portfolios, global service networks, and long-standing hospital procurement relationships.

Mid-tier competitors, including Mindray, Esaote, and Shimadzu, are expanding through competitive pricing and distribution partnerships in Asia Pacific, Latin America, and the Middle East. AI capability is increasingly shifting procurement decisions, enabling imaging AI firms such as Aidoc and Intelerad to influence clinical purchasing through demonstrated diagnostic improvement evidence.

Key Industry Developments:

- In May 2026, GE HealthCare showcased AI-powered MRI technologies including next-generation SIGNA systems and intelligent workflow platforms, strengthening innovation in precision-focused 3D medical imaging devices and radiology automation.

- In November 2025, Hologic, Inc. unveiled new clinical evidence for its AI-powered mammography and 3D imaging solutions at RSNA, reinforcing advancements in breast cancer detection efficiency and radiology workflow optimization.

Companies Covered in 3D Medical Imaging Devices Market

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Koninklijke Philips N.V. (Philips Healthcare)

- Canon Medical Systems Corporation

- Hologic Inc.

- Shimadzu Corporation

- Mindray Medical International Limited

- Esaote S.p.A.

- Samsung Medison Co., Ltd.

- Fujifilm Holdings Corporation

- Carestream Health Inc.

- Agfa-Gevaert Group

- Hitachi Healthcare Americas

- United Imaging Healthcare Co., Ltd.

- Brainlab AG

Frequently Asked Questions

The global 3D medical imaging devices market is projected to reach US$14.3 billion in 2026.

Rising prevalence of chronic diseases, increasing demand for early and accurate diagnostics, and expanding adoption of AI-enabled imaging technologies drive the 3D medical imaging devices market.

The 3D medical imaging devices market is poised to witness a CAGR of 8.1% from 2026 to 2033.

Expansion of AI-integrated imaging platforms, growing demand for portable diagnostic systems, and increasing investment in digital healthcare infrastructure create key opportunities in the 3D medical imaging devices market.

Some of the key market players include GE HealthCare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Hologic.