- Medical Devices

- Ventricular Assist Devices Market

Ventricular Assist Devices Market Size, Share, and Growth Forecast 2026 - 2033

Ventricular Assist Devices Market by Product (Left Ventricular Assist Device, Right Ventricular Assist Device, Bi-Ventricular Assist Device, Total Artificial Heart), Flow Type (Pulsatile Flow, Continuous Flow), Application (Bridge to Transplant, Destination Therapy, Others), End-user (Hospitals, Cardiac Centers, Ambulatory Surgical Centers, Specialty Clinics), and Regional Analysis, 2026 - 2033

Ventricular Assist Devices Market Share and Trends Analysis

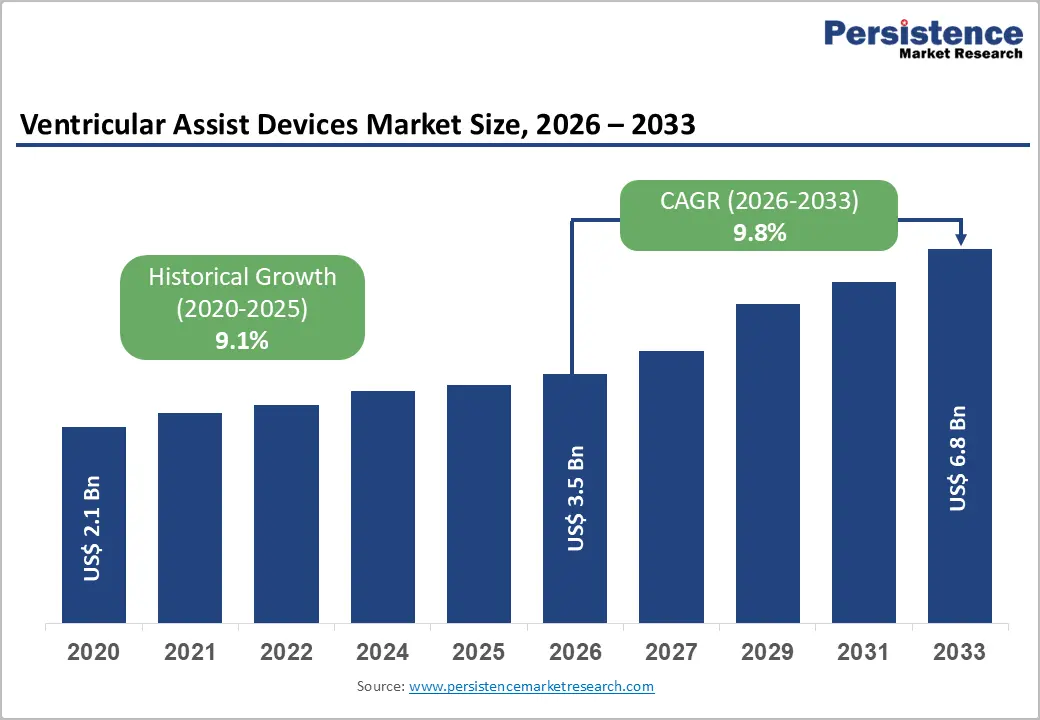

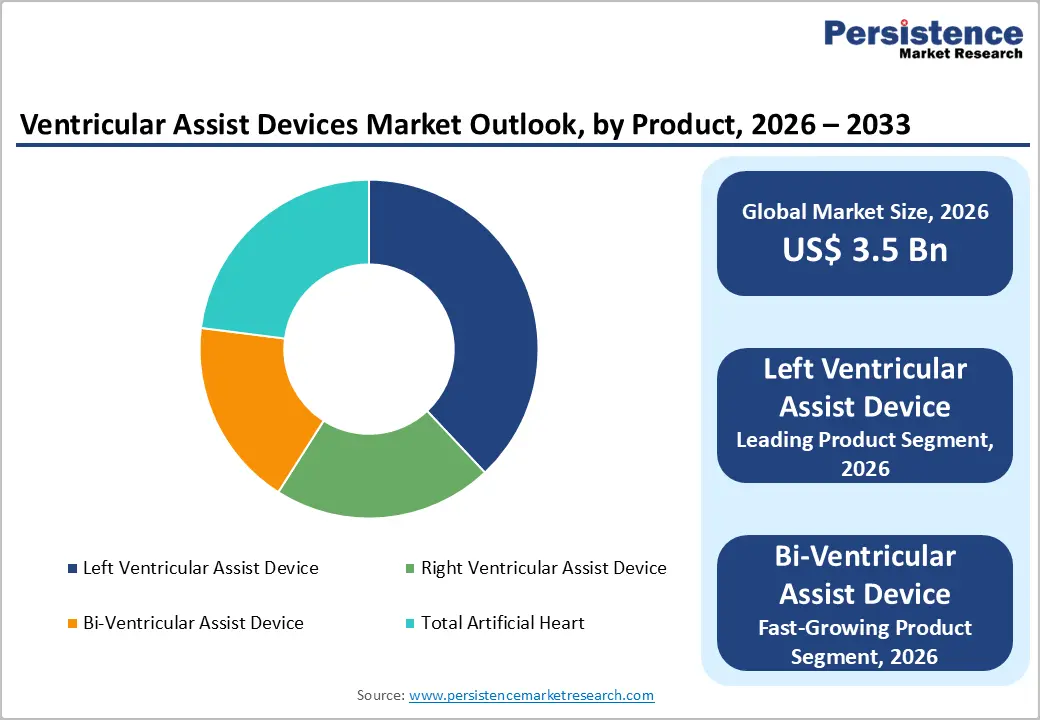

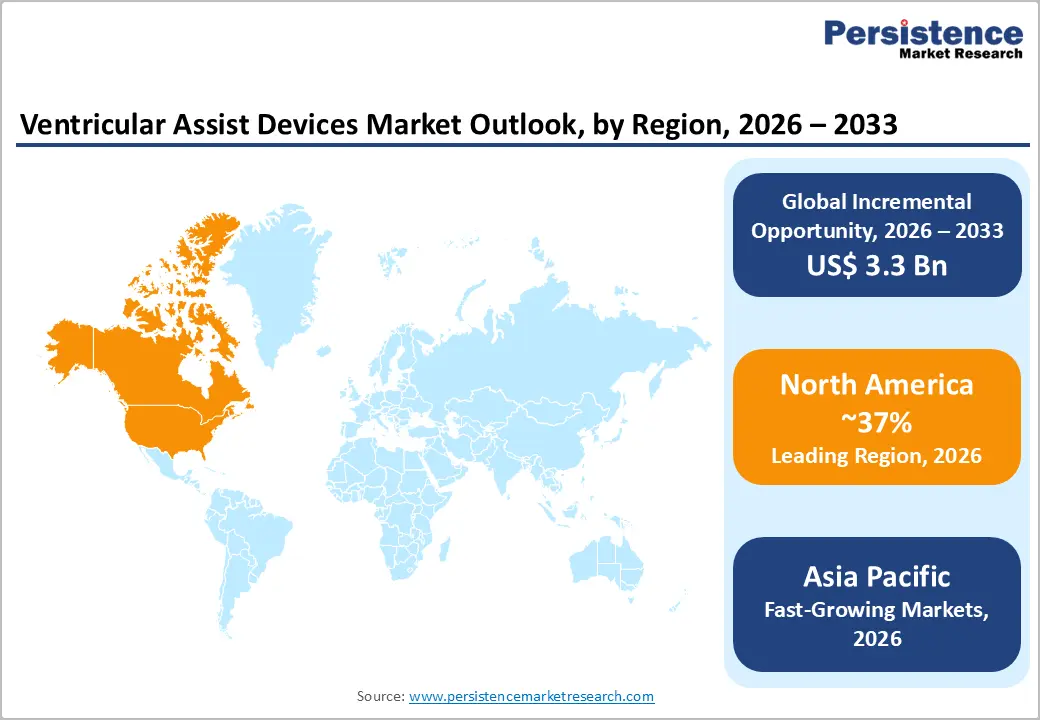

The global Ventricular Assist Devices (VAD) market size is expected to be valued at US$ 3.5 billion in 2026 and projected to reach US$ 6.8 billion by 2033, growing at a robust CAGR of 9.8% between 2026 and 2033.

It is growing steadily due to the rising prevalence of advanced heart failure, increasing shortage of donor hearts for transplantation, and continuous advancements in mechanical circulatory support technologies. These devices help improve cardiac output by supporting weakened ventricles and are widely used as bridge-to-transplant, destination therapy, and bridge-to-recovery solutions. Left ventricular assist devices remain the most adopted due to high cases of left-sided heart failure. Improved survival rates, compact implantable designs, and better patient outcomes are driving adoption globally.

Key Industry Highlights

- Regional Leadership: North America holds 37% of the global VAD market share in 2025, driven by the highest LVAD implantation rates, robust Medicare destination therapy reimbursement, INTERMACS registry leadership, and over 150 certified VAD implantation centers.

- Fast-Growing Region: Asia Pacific is forecast to register the highest regional CAGR through 2033, fueled by China's growing MCS infrastructure, India's expanding super-specialty cardiac capacity, Japan's organ shortage crisis, and increasing government cardiovascular investment.

- Dominant Product Segment: Left Ventricular Assist Devices hold 38% product market share in 2025, underpinned by Abbott's HeartMate 3 MOMENTUM 3 landmark trial outcomes, broad FDA and CE Mark approval, and established Medicare destination therapy reimbursement.

- Fast-Growing Product Segment: BiVADs are forecast to grow at the highest product segment CAGR, driven by BiVACOR's first-in-human milestone, growing clinical recognition of biventricular failure, and LVAD-associated right ventricular failure in 20–40% of patients.

- Key Opportunity: With DT now accounting for over 50% of U.S. LVAD implantations per INTERMACS, and global donor heart shortages persisting, destination therapy adoption growth represents the largest long-term commercial opportunity for VAD manufacturers worldwide.

Market Dynamics

Drivers – Rise in Cases of Heart Failure Burden and Chronic Donor Organ Shortage

The global heart failure pandemic is the most powerful structural demand driver for the ventricular assist devices market. The American Heart Association (AHA) estimates that approximately 6.7 million adults in the United States have heart failure, with projections indicating that prevalence will increase by 46% by 2030. Globally, the European Society of Cardiology (ESC) estimates heart failure affects over 15 million people across Europe alone.

Critically, fewer than 5,000 donor hearts become available annually worldwide, leaving the vast majority of end-stage heart failure patients without access to transplantation. This structural imbalance between need and organ supply is institutionalizing the role of LVADs and BiVADs as both life-sustaining bridge and long-term permanent support solutions, driving consistent high-value device implantation volumes.

Technological Advancements in Miniaturized Continuous-Flow and Fully Implantable VAD Platforms

Rapid innovation in VAD technology is a major market accelerator. The transition from bulky pulsatile-flow devices to compact continuous-flow centrifugal and axial pumps, exemplified by Abbott Laboratories' HeartMate 3 and Medtronic's HVAD, has dramatically improved patient quality of life, reduced adverse event rates, and extended device durability.

The landmark MOMENTUM 3 trial, published in the New England Journal of Medicine, demonstrated that HeartMate 3 achieved a 79% two-year survival rate in destination therapy patients, a benchmark that significantly broadened FDA-approved indications. Emerging fully implantable, transcutaneous energy transfer (TET)-powered systems under development by companies including BiVACOR Inc. and CorWave SA are poised to further expand clinical adoption by eliminating percutaneous drive line infection, the most common VAD complication.

Restraints - High Device Cost and Limited Reimbursement Coverage in Emerging Markets

The high cost of VAD implantation, including device procurement, implantation surgery, and post-operative management, represents a significant market access constraint, particularly in emerging economies. In the United States, total VAD implantation costs, including device and hospitalization, can exceed US$ 150,000–200,000 per patient. While Medicare and major private insurers in the U.S. and statutory systems in Europe provide VAD reimbursement, coverage in Asia, Latin America, and the Middle East remains inconsistent, restricting patient access in regions where cardiovascular disease burden is rapidly growing.

Adverse Events Including Stroke, Bleeding, and Driveline Infection

Despite substantial device improvements, VAD therapy carries clinically significant adverse event risks that dampen adoption rates and complicate patient selection. Published data from the Interagency Registry for Mechanically Assisted Circulatory Support (INTERMACS) indicate that stroke occurs in approximately 10–17% of patients over two years of LVAD support, while driveline infections affect 10–20% of patients annually.

These factors necessitate intensive post-implant monitoring, drive significant healthcare resource utilization, and contribute to patient and physician hesitancy toward early VAD adoption in less severe heart failure stages, limiting market volume expansion.

Opportunities - Bi-Ventricular Assist Devices Emerging as High-Growth Segment for Biventricular Failure

Bi-Ventricular Assist Devices (BiVADs) are the fastest-growing product segment in the VAD market, driven by growing clinical recognition that a significant proportion of advanced heart failure patients experience concurrent right and left ventricular dysfunction requiring biventricular mechanical support. Traditional LVAD implantation alone results in right ventricular failure requiring additional support in approximately 20–40% of cases, according to data published in the Journal of Cardiac Failure.

The development of purpose-designed, compact total artificial heart and biventricular platforms, including BiVACOR Inc.'s titanium centrifugal BiVAD, which entered clinical trials, and SynCardia Systems' Total Artificial Heart, is creating a rapidly expanding clinical and commercial opportunity for manufacturers with biventricular solution portfolios beyond conventional LVAD-focused offerings.

Category-wise Analysis

Product Insights

Left Ventricular Assist Devices (LVADs) dominate the VAD product market with approximately 38% market share in 2025. LVADs address the most prevalent form of advanced heart failure, left ventricular dysfunction, which constitutes the majority of end-stage heart failure cases. Clinical evidence supporting LVAD use spans both bridge-to-transplant and destination therapy indications, with landmark trials including MOMENTUM 3 and REMATCH establishing robust survival and quality-of-life outcomes data. The market's dominant LVAD platforms, Abbott's HeartMate 3 and previously Medtronic's HVAD (withdrawn in 2021) have been adopted across hundreds of certified VAD centers globally. LVAD miniaturization advances and expanded reimbursement coverage sustain this segment's commanding market position.

Flow Type Insights

Continuous Flow devices dominate the flow type segment, commanding approximately 82% of the VAD market in 2025. Continuous-flow pumps utilizing either axial or centrifugal pump mechanisms have almost entirely replaced earlier pulsatile-flow devices due to their superior durability, smaller size, lower complication rates, and longer device lifespan. The INTERMACS registry data consistently demonstrate that continuous-flow LVADs achieve superior two-year survival outcomes compared to legacy pulsatile devices.

The engineering simplicity of continuous-flow designs with fewer moving parts and no mechanical valves reduces device failure rates significantly. Third-generation centrifugal continuous-flow pumps such as the HeartMate 3 have further advanced the field through magnetically levitated impeller technology, further reducing thrombosis and hemolysis events.

End-user Insights

Hospitals are the dominant end-user segment, representing approximately 62% of VAD market revenue in 2025. The complex implantation procedure, intensive post-operative care requirements, and mandatory cardiac surgery and perfusionist expertise confine VAD implantation exclusively to hospitals with advanced cardiac surgery programs and certified mechanical circulatory support (MCS) teams.

The Joint Commission and The Society of Thoracic Surgeons (STS) in the U.S. oversee quality benchmarks for VAD programs, further concentrating implantations within credentialed hospital centers. Dedicated cardiac centers at major academic medical institutions, including those with UNOS-certified heart transplant programs, are the primary purchasers of VAD systems and associated consumables.

Regional Insights

North America Ventricular Assist Devices Market Trends and Insights

North America leads the global VAD market with approximately 37% market share in 2025, anchored by the world's most advanced mechanical circulatory support ecosystem, robust Medicare and private insurance reimbursement for both BTT and DT indications, and the highest density of certified VAD implantation centers. The INTERMACS registry the world's most comprehensive MCS database, is U.S.-based, driving global evidence generation and clinical protocol standards from North America.

U.S. Ventricular Assist Devices Market Size

The United States accounts for approximately 90% of the North American VAD market in 2025. Over 3,000 LVAD implantations are performed annually per INTERMACS data, with more than 150 certified VAD centers operating nationally. Medicare's established DRG reimbursement for LVAD destination therapy sustains consistent high-volume implantation demand.

Europe Ventricular Assist Devices Market Trends and Insights

Europe is the second-largest VAD market, supported by universal healthcare coverage, high end-stage heart failure prevalence, and a growing number of certified MCS centers. The European Association for Cardio-Thoracic Surgery (EACTS) and ESC Heart Failure Association guidelines are progressively incorporating LVAD destination therapy recommendations, driving uptake across Germany, France, and the U.K.

Germany Ventricular Assist Devices Market Size

Germany holds approximately 26% of the European VAD market in 2025. Germany has one of Europe's highest VAD implantation rates, supported by GKV statutory health insurance reimbursement, a dense cardiac surgery center network, and the headquarters of Berlin Heart GmbH, a leading pediatric and adult VAD manufacturer sustaining strong domestic clinical and commercial activity.

U.K. Ventricular Assist Devices Market Size

The United Kingdom accounts for approximately 18% of the European VAD market in 2025. The NHS England Commissioning Policy for LVADs covers both BTT and DT indications at designated specialist heart failure centers. NICE technology appraisal support for LVAD destination therapy has formalized clinical pathways and driven consistent procedural volume growth across U.K. specialist cardiac centers.

Asia Pacific Ventricular Assist Devices Market Trends and Insights

Asia Pacific is the fastest-growing VAD market region, driven by rapidly expanding cardiovascular disease burden, improving cardiac surgery infrastructure, and increasing government healthcare investment across China, Japan, and India. China is building specialized MCS centers and the National Medical Products Administration (NMPA) has approved several LVAD devices, stimulating growing implantation volumes in major cardiac surgery hospitals.

India Ventricular Assist Devices Market Size

India holds approximately 13% of the Asia Pacific VAD market in 2025. Rising heart failure incidence linked to a growing hypertension and diabetes burden and expanding super-specialty cardiac hospital capacity in cities such as Mumbai, Chennai, and Delhi are creating a nascent but growing VAD implantation market, with Ayushman Bharat coverage beginning to extend to advanced cardiac interventions.

Competitive Landscape

The Ventricular Assist Devices market is highly competitive and innovation-driven, with manufacturers focusing on advanced pump technologies, miniaturized implantable systems, and improved long-term patient outcomes. Competition is centered on product reliability, reduced risk of thrombosis, lower infection rates, and enhanced portability for patient convenience. Companies are investing heavily in next-generation magnetically levitated pumps, fully implantable systems, and pediatric support devices to strengthen market presence. Regulatory approvals, clinical trial success, and hospital partnerships play a major role in market positioning.

Key Developments

- In April 2026, Sagar Haval launched the ECMO Simulation Academy, a global initiative aimed at improving training standards in extracorporeal life support therapies, including ECMO, Left Ventricular Assist Devices (LVADs), and bi-ventricular assist systems.

- In November 2025, The Medicity launched its Advanced Surgical Heart Failure Clinic to support patients with complex and end-stage heart failure. The specialized center was designed to provide diagnosis, surgical management, and rehabilitation through a multidisciplinary team of cardiac surgeons, heart failure specialists, interventional cardiologists, and rehabilitation experts.

Global Ventricular Assist Devices Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.1 Billion |

|

Current Market Value (2026) |

US$ 3.5 Billion |

|

Projected Market Value (2033) |

US$ 6.8 Billion |

|

CAGR (2026–2033) |

9.8% |

|

Leading Region |

North America, 37% market share in 2025 |

|

Dominant Product Segment |

Left Ventricular Assist Device (LVAD), ~38% market share in 2025 |

|

Top-Ranking Flow Type Segment |

Continuous Flow, ~82% market share in 2025 |

|

Incremental Opportunity (2026–2033) |

US$ 3.3 Billion |

Companies Covered in Ventricular Assist Devices Market

- Abbott Laboratories

- ABIOMED

- Medtronic plc

- Berlin Heart GmbH

- Jarvik Heart, Inc.

- SynCardia Systems, LLC

- Terumo Corporation

- ReliantHeart Inc.

- Calon Cardio-Technology Ltd.

- CARMAT

- CorWave SA

- BiVACOR Inc.

- Evaheart, Inc.

Frequently Asked Questions

The global Ventricular Assist Devices market is expected to be valued at US$ 3.5 billion in 2026.

Primary drivers include the WHO's estimate of over 64 million heart failure patients globally, fewer than 5,000 donor hearts available annually per ISHLT, and landmark clinical evidence from the MOMENTUM 3 trial validating HeartMate 3's superior outcomes, driving FDA-approved expansion of LVAD destination therapy indications and broadening clinical adoption globally.

North America leads the market with approximately 37% global market share in 2025, supported by the world's highest LVAD implantation volumes, Medicare destination therapy reimbursement, the INTERMACS registry evidence infrastructure, and the global headquarters of leading VAD innovators, including Abbott Laboratories and BiVACOR Inc.

Key opportunities include the continued expansion of Destination Therapy (DT) indications, where DT now accounts for over 50% of U.S. implantations per INTERMACS, and the emergence of next-generation Bi-Ventricular Assist Device platforms such as BiVACOR's titanium magnetically levitated BiVAD, targeting the large biventricular failure patient population currently underserved by conventional LVAD-only approaches.

Leading companies include Abbott Laboratories, ABIOMED, Medtronic plc, Berlin Heart GmbH,Jarvik Heart, Inc., etc.