- Medical Devices

- Fusion Biopsy Market

Fusion Biopsy Market Size, Share and Growth Forecast, 2026 - 2033

Fusion Biopsy Market by Biopsy Route (Transperineal, Transrectal), End-user (Hospitals, Diagnostic Centers), and Regional Analysis for 2026 - 2033

Fusion Biopsy Market Share and Trends Analysis

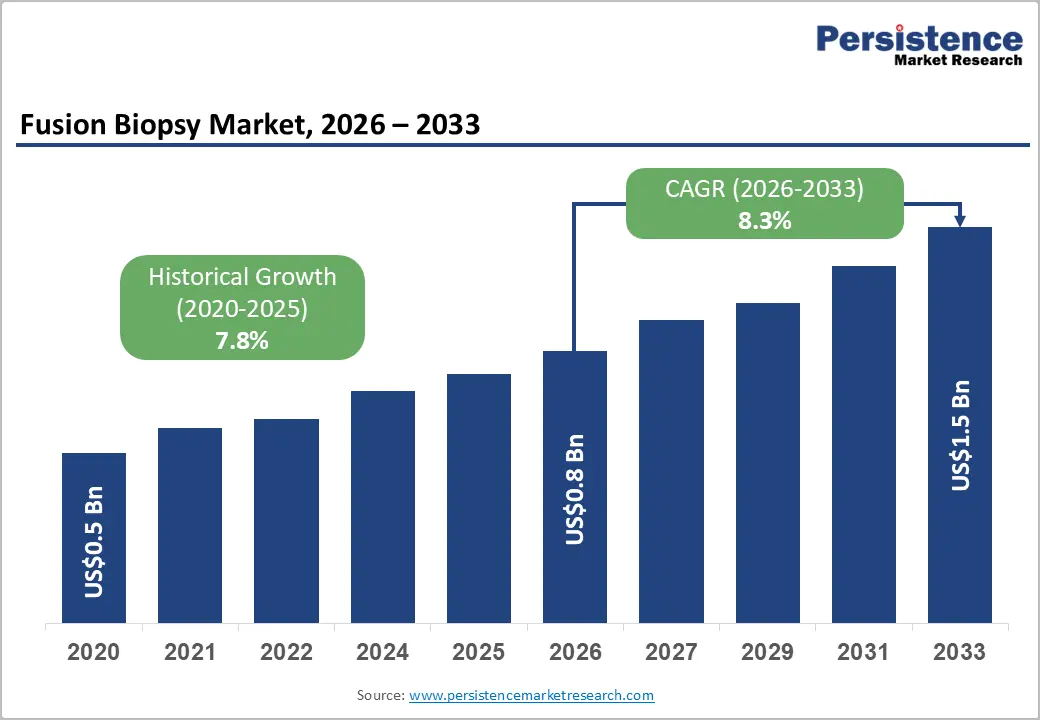

The global fusion biopsy market size is likely to be valued at US$ 0.8 billion in 2026 and is projected to reach US$ 1.5 billion by 2033, growing at a CAGR of 8.3% during the forecast period from 2026 to 2033, driven by the rising incidence of prostate cancer, increasing adoption of MRI fusion biopsy systems, and growing demand for highly accurate minimally invasive diagnostic procedures.

The growing adoption of multiparametric MRI (mpMRI) and targeted biopsy techniques is improving lesion detection accuracy and driving wider use across urology practices. Supportive early cancer detection initiatives in North America and Europe, along with rising investments in image-guided biopsy technologies, are further boosting market growth. Healthcare providers are increasingly using fusion-guided procedures to improve diagnostic precision, reduce false negatives, and enable personalized cancer treatment planning.

Key Industry Highlights:

- Key Market Driver: Rising prostate cancer prevalence and growing adoption of MRI-guided biopsy technologies are expected to continue strengthening global market demand, supported by increasing preference for precision-based cancer diagnostics and minimally invasive procedures.

- Dominant Biopsy Route: Transrectal biopsy is projected to lead with approximately 58% of the market share in 2026, while transperineal biopsy procedures are anticipated to witness the fastest growth through 2033 due to lower infection risks and increasing clinical acceptance.

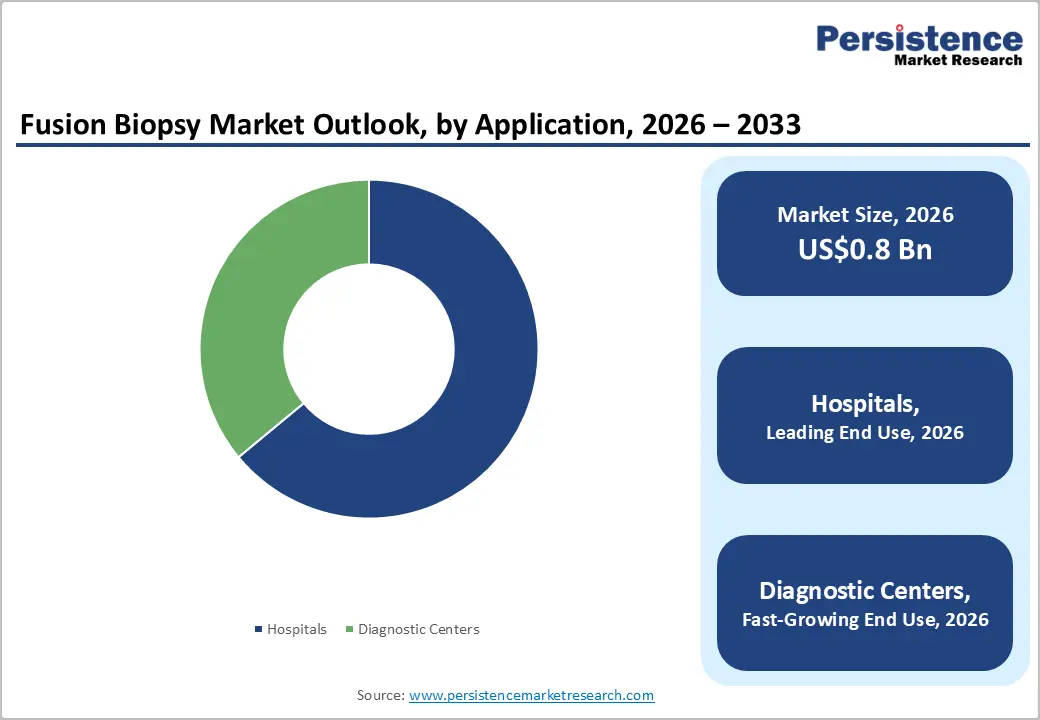

- Leading End-user: Hospitals are expected to account for nearly 64% of global revenue in 2026, supported by advanced imaging infrastructure, higher procedural volumes, and expanding investments in fusion biopsy systems and precision oncology workflows.

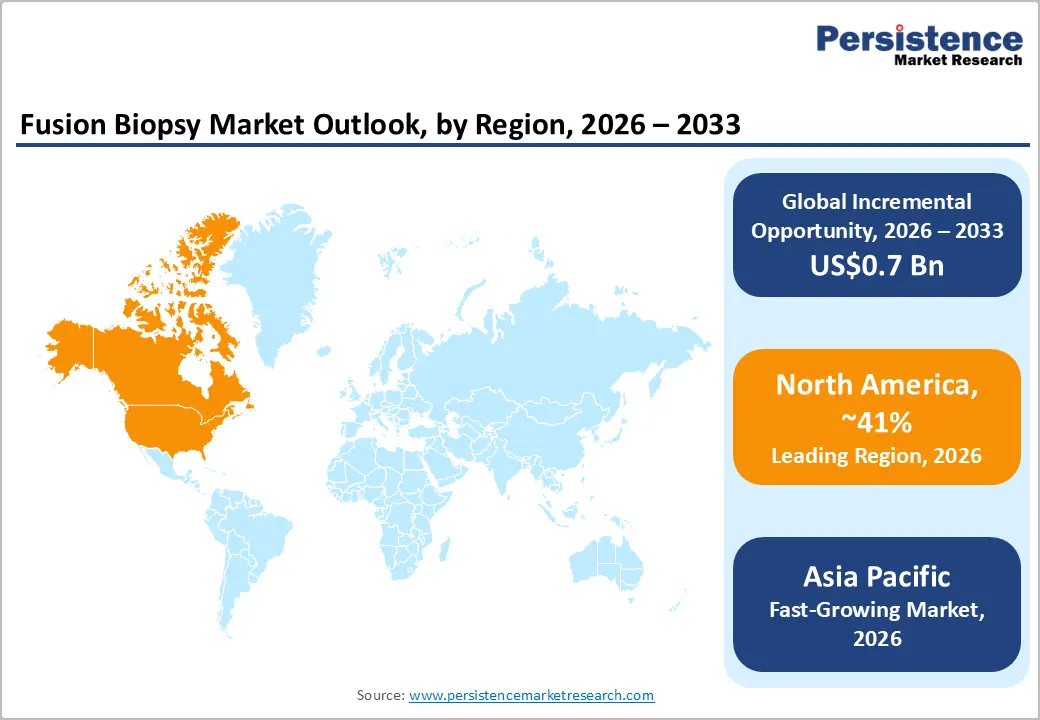

- Regional Leadership: North America is poised to dominate with an estimated 41% market share in 2026, driven by strong reimbursement frameworks, advanced healthcare infrastructure, and rapid adoption of AI-enabled diagnostic technologies.

- Competitive Environment: Competitive dynamics are increasingly shaped by AI-enabled imaging platforms, robotic-assisted biopsy systems, precision oncology integration, and strategic collaborations focused on improving diagnostic accuracy and workflow efficiency.

DRO Analysis

Driver - Rising Global Burden of Prostate Cancer and Demand for Precision Diagnostics

The rising prevalence of prostate cancer remains a major growth driver for the fusion biopsy market. According to the International Agency for Research on Cancer (IARC) and the World Health Organization (WHO), prostate cancer accounts for more than 1.4 million new cases annually worldwide. Growing recommendations from organizations such as the U.S. Centers for Disease Control and Prevention (CDC) and the American Cancer Society for early cancer detection are increasing demand for MRI-guided biopsy and fusion-guided diagnostic procedures.

Traditional biopsy methods often miss clinically significant tumors, particularly in difficult-to-access prostate regions. Fusion biopsy systems combine MRI and real-time ultrasound imaging to improve lesion targeting accuracy and reduce unnecessary repeat biopsies. Clinical studies published by the National Institutes of Health (NIH) show that fusion-guided procedures significantly improve clinically significant cancer detection rates compared with conventional biopsy techniques. This is encouraging hospitals and diagnostic centers to invest in precision biopsy platforms, robotic-assisted systems, and AI-enabled imaging technologies.

Restraint - High Equipment Costs and Limited Accessibility in Mid-Tier Healthcare Facilities

High capital investment remains a key barrier for the fusion biopsy market, especially in emerging economies and mid-tier healthcare facilities. A full system requires multiparametric MRI infrastructure, advanced ultrasound devices, and imaging software, with installation costs often reaching several hundred thousand dollars per facility, as noted by OECD and hospital procurement data.

Adoption is further limited by inconsistent reimbursement policies and continued reliance on conventional transrectal biopsy methods due to lower costs. Additional challenges include physician training requirements, workflow integration issues, and limited radiology capacity. These factors collectively slow the penetration of fusion-guided biopsy systems despite rising clinical demand for precision diagnostics.

Opportunity - Expansion of AI-Integrated Imaging and Transperineal Fusion Biopsy Adoption

The integration of artificial intelligence into fusion biopsy systems presents a strong growth opportunity, improving lesion detection accuracy and enabling automated image registration with reduced operator dependency. Regulatory support from the FDA and EMA for software-driven oncology imaging is further accelerating the commercialization of AI-enabled diagnostic technologies.

The increasing adoption of transperineal biopsy techniques is expanding market potential due to lower infection risks compared with transrectal methods and growing clinical acceptance in Europe and North America. Supported by recommendations from the European Association of Urology (EAU), combined with rising investments in minimally invasive outpatient procedures, these trends are driving demand for robotic fusion biopsy systems, navigation software, and advanced biopsy consumables.

Category-wise Analysis

Biopsy Route Insights

The transrectal route is expected to lead the fusion biopsy market with 58% share in 2026, supported by strong clinical familiarity and seamless integration with existing ultrasound-guided workflows. Its dominance is driven by lower adoption costs and established hospital protocols, especially in high-volume screening systems across North America and Asia Pacific. Recent upgrades in MRI fusion biopsy systems are improving targeting accuracy. However, infection risk concerns are gradually limiting long-term dependence.

The transperineal route is projected to grow fastest through 2033 due to rising preference for safer, infection-reducing biopsy techniques. EAU guidelines and NHS-led adoption in the UK are accelerating clinical uptake in hospitals. Robotic needle guidance and outpatient procedures are improving accuracy and patient comfort. Expansion across Europe and North America reflects a shift toward precision-driven prostate cancer diagnostics.

End-user Insights

Hospitals are expected to dominate with 64% share in 2026, driven by advanced imaging infrastructure and high prostate cancer screening volumes. Adoption of MRI fusion biopsy systems and AI-enabled workflows is strengthening diagnostic precision. Government investments in oncology care across the U.S. and Europe further support growth. Strong reimbursement frameworks continue to reinforce hospital leadership.

Diagnostic centers are the fastest-growing segment due to rising demand for outpatient and cost-efficient fusion biopsy procedures. Increasing preference for quicker diagnostics outside hospitals is boosting standalone imaging center expansion. Partnerships with urology networks are improving service integration. Compact imaging systems and ambulatory care models are accelerating adoption.

Regional Analysis

North America Fusion Biopsy Market Trends

North America is expected to account for approximately 41% share of the global fusion biopsy market in 2026, driven by strong penetration of MRI-guided prostate biopsy systems, advanced hospital infrastructure, and early adoption of AI-enabled diagnostic workflows. The region is expected to remain a technology-first market, where growth is largely supported by the replacement of conventional systems with precision-driven fusion and robotic-assisted platforms rather than new procedural introductions.

U.S. Fusion Biopsy Market Trends

U.S. is expected to represent nearly 75% of the North American market in 2026, supported by high prostate cancer screening intensity and widespread use of fusion biopsy systems across hospital and specialty oncology settings. The market is increasingly shifting toward AI-integrated imaging and navigation-assisted biopsy systems, with FDA-cleared solutions expected to accelerate clinical upgrades. Adoption of robotic-assisted biopsy platforms is also projected to expand, improving lesion targeting accuracy and reducing repeat biopsy dependency.

Canada Fusion Biopsy Market Trends

Canada is expected to account for around 25% of the North American market in 2026, supported by the gradual modernization of imaging infrastructure and expanding access to multiparametric MRI. Adoption of MRI-ultrasound fusion biopsy technologies is expected to increase across tertiary care hospitals, particularly in urban regions. The market is also expected to benefit from centralized diagnostic pathways and expanding use of AI-assisted radiology tools aimed at improving workflow efficiency and diagnostic consistency.

Europe Fusion Biopsy Market Trends

Europe is expected to hold approximately 26% share of the global market in 2026, supported by strong regulatory standardization and increasing clinical shift toward transperineal biopsy procedures. The region is expected to witness steady adoption driven by structured prostate cancer screening programs, rising MRI utilization, and increasing emphasis on reducing infection-related complications in biopsy procedures.

Germany Fusion Biopsy Market Trends

Germany is expected to account for nearly 36% of the regional market in 2026, supported by advanced radiology infrastructure and high utilization of multiparametric MRI in prostate cancer diagnostics. Adoption of fusion biopsy platforms is expected to remain strong across university hospitals and cancer centers. The market is also expected to benefit from increasing integration of AI-enabled lesion detection tools and navigation-assisted biopsy systems aimed at improving procedural precision.

U.K. Fusion Biopsy Market Trends

The U.K. is expected to represent around 20% of the regional market in 2026, supported by the NHS-led transition toward transperineal fusion biopsy procedures aimed at reducing infection risks. The market is expected to shift toward streamlined diagnostic pathways, including one-stop prostate cancer diagnostic clinics combining MRI and biopsy services. Increasing use of AI-supported radiology systems is also expected to improve diagnostic turnaround times and workflow efficiency.

Asia Pacific Fusion Biopsy Market Trends

Asia Pacific is expected to account for approximately 20% share of the global fusion biopsy market in 2026, and is expected to remain the fastest-growing region due to rising prostate cancer awareness, expanding diagnostic infrastructure, and increasing adoption of fusion-guided biopsy technologies. Growth is expected to be driven by rapid healthcare modernization and increasing penetration of MRI-based diagnostic systems in both public and private healthcare sectors.

China Fusion Biopsy Market Trends

China is expected to hold around 35% of the regional market in 2026, supported by large-scale hospital expansion and growing integration of advanced imaging technologies in oncology care. Adoption of MRI fusion biopsy systems is expected to increase across tier-1 and tier-2 hospitals. The market is also expected to benefit from the expansion of AI-enabled imaging platforms and national cancer screening initiatives aimed at improving early detection rates.

India Fusion Biopsy Market Trends

India is expected to account for nearly 18% of the regional market in 2026, driven by rising prostate cancer awareness and increasing investment in private healthcare infrastructure. Adoption of fusion biopsy technologies is expected to expand across metropolitan tertiary hospitals and diagnostic chains. The market is also expected to benefit from increasing installation of multiparametric MRI systems and the emergence of integrated oncology diagnostic centers aimed at reducing diagnostic delays.

Competitive Landscape

The global fusion biopsy market is moderately consolidated, with leading imaging OEMs such as Siemens Healthineers, GE HealthCare, Philips, and Canon Medical Systems collectively holding a significant share of revenue. Their dominance is driven by integrated MRI-ultrasound fusion platforms, strong hospital partnerships, and continuous investment in AI-enabled imaging and navigation technologies. High regulatory barriers and the need for clinical validation further reinforce their market position.

Specialized players such as Koelis, BK Medical, Eigen Health, and Exact Imaging are strengthening their presence through dedicated prostate biopsy navigation systems and precision imaging solutions. The market is expected to see gradual consolidation, supported by acquisitions and partnerships focused on AI-guided biopsy systems, robotic assistance, and cloud-based imaging analytics, enhancing procedural accuracy and workflow integration.

Key Industry Developments:

- In November 2025, GE HealthCare announced a US$2.3 billion acquisition of Intelerad Medical Systems, a cloud-based imaging software provider focused on outpatient diagnostics. This deal strengthens GE HealthCare’s shift toward cloud imaging, AI-enabled workflows, and outpatient diagnostic ecosystems, directly supporting fusion biopsy imaging integration.

- In 2025, Koelis is expanding its Trinity fusion biopsy platform adoption through new regional distribution and hospital partnerships across Europe and North America.

Companies Covered in Fusion Biopsy Market

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- GE HealthCare Technologies Inc.

- Canon Medical Systems Corporation

- Samsung Medison Co., Ltd.

- Koelis

- Eigen Health

- BK Medical

- ESAOTE S.p.A.

- Hitachi Ltd.

- FUJIFILM Holdings Corporation

- MedCom GmbH

- Micrima Limited

- Exact Imaging

- Biobot Surgical Pte Ltd

Frequently Asked Questions

The global fusion biopsy market is expected to reach approximately US$0.8 billion in 2026.

The fusion biopsy market is driven by rising prostate cancer cases and increasing adoption of MRI-guided fusion biopsy systems for precise diagnosis.

The fusion biopsy market is projected to grow at a CAGR of 8.3% from 2026 to 2033.

Key opportunities include the expansion of AI-enabled imaging systems and the growing adoption of transperineal biopsy techniques.

Key players include Siemens Healthineers, GE HealthCare, Philips, Canon Medical Systems, Koelis, and BK Medical.