- Home Appliances

- Ventilation Fan Market

Ventilation Fan Market Size, Share, and Growth Forecast 2026 - 2033

Ventilation Fan Market by Product Type (Axial Fans, Centrifugal Fans, Mixed Flow Fans, Cross Flow Fans, Inline Fans, Range Hood Fans, Domestic Exhaust Fans, Power Roof Fans), by Mounting Type (Wall-Mounted, Ceiling-Mounted, Window-Mounted, Inline/Duct-Mounted, Roof-Mounted Fans), Material Type, Distribution Channel, End-user, and Regional Analysis, 2026 - 2033

Ventilation Fan Market Size and Trend Analysis

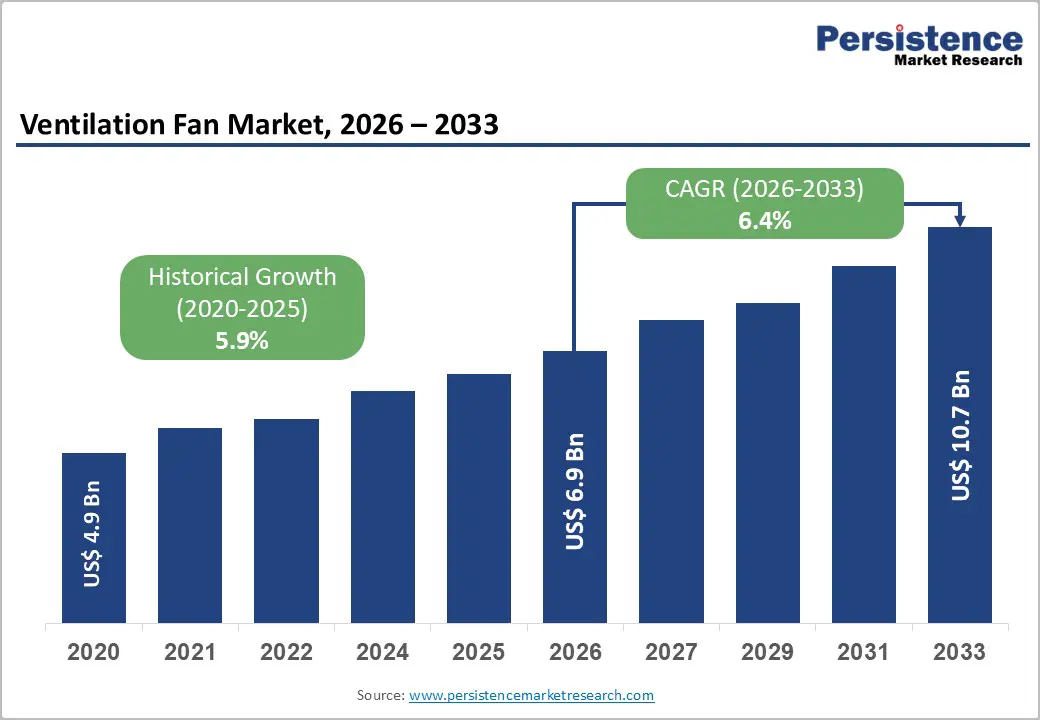

The global ventilation fan market size is likely to be valued at US$ 6.9 million in 2026 and is expected to reach US$ 10.7 million by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033. The market is being driven primarily by heightened global awareness around indoor air quality (IAQ) and the rapid pace of construction activity across emerging economies.

Key Industry Highlights:

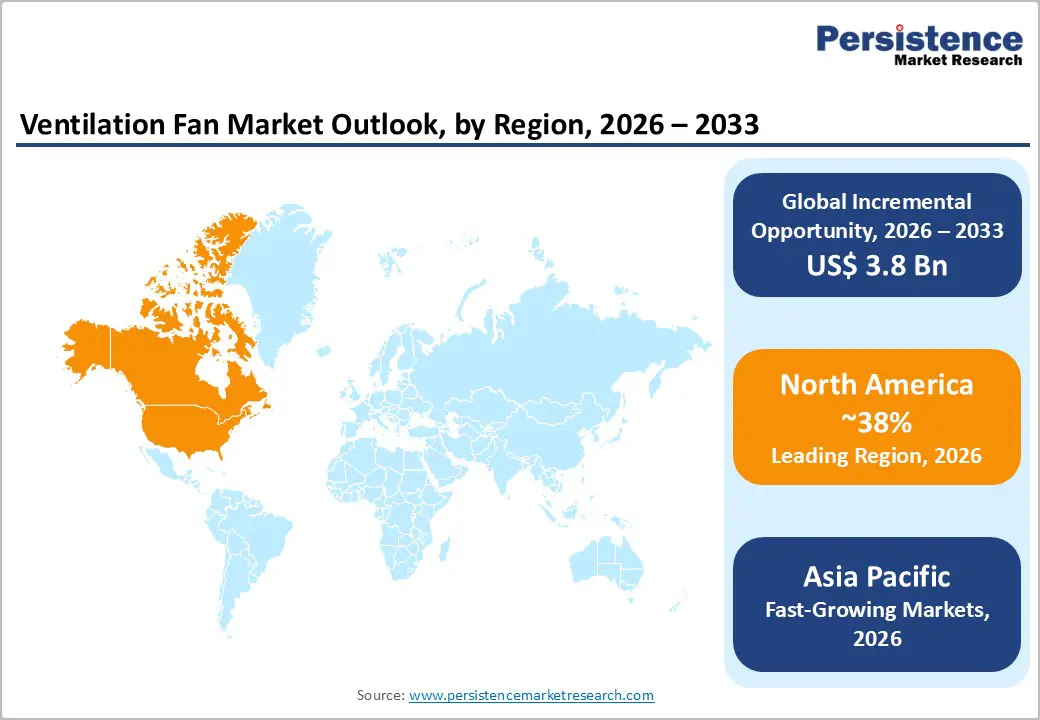

- Leading Region: North America leads the global ventilation fan market, underpinned by stringent building codes such as ASHRAE 62.1, a large replacement market, and strong consumer awareness of indoor air quality standards.

- Fastest Growing Region: Asia Pacific is the fast-growing regional market, driven by rapid urbanisation in China and India, government green building mandates, and accelerating industrial park development across Southeast Asia.

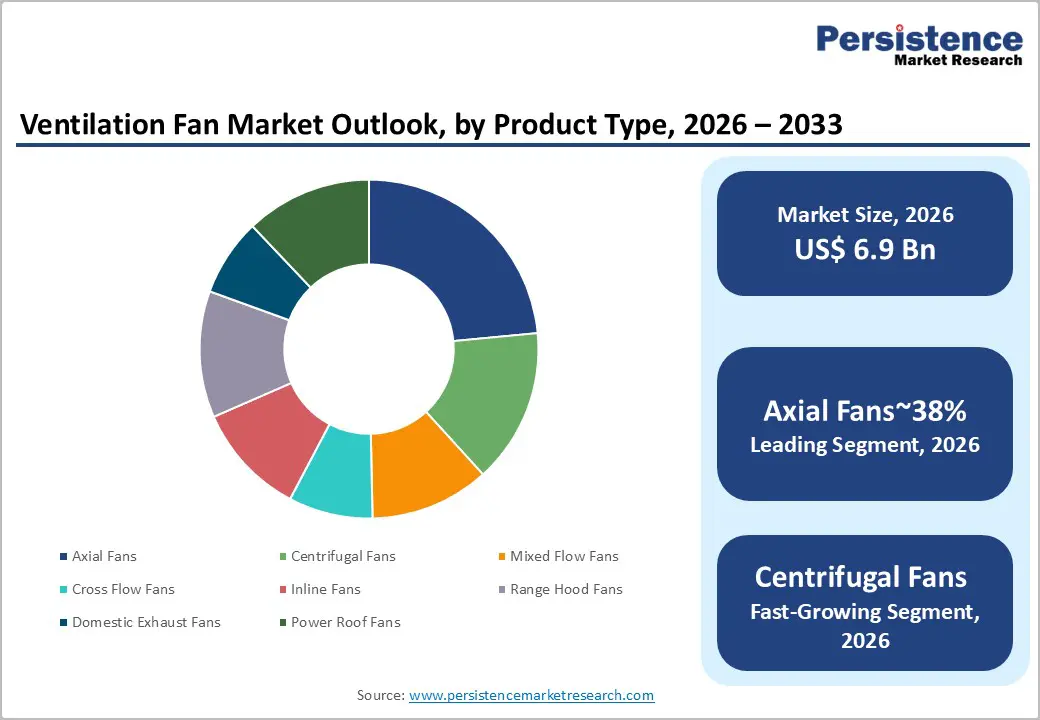

- Dominant Product: Axial fans dominate the product type category with approximately 38% market share, owing to their cost-efficiency, high-volume airflow capability, and broad applicability across residential, commercial, and industrial ventilation applications.

- Fast-growing Distribution Channel: Online retail is the fastest-growing distribution channel, driven by rising contractor and DIY consumer adoption of digital procurement platforms and manufacturer-direct e-commerce strategies.

- Key Opportunity: The integration of IoT sensors, AI-driven demand-controlled ventilation, and smart home connectivity presents a compelling opportunity, particularly in healthcare, hospitality, and food & beverage facilities requiring precision air quality management.

Market Dynamics

Drivers - Rising Demand for Energy-Efficient Indoor Ventilation Solutions

Escalating concerns about indoor air quality and rising energy costs are fundamentally reshaping procurement decisions across residential, commercial, and industrial segments. According to the U.S. Environmental Protection Agency (EPA), indoor air can be two to five times more polluted than outdoor air, a finding that has translated into updated building codes mandating mechanical ventilation in new constructions.

The International Energy Agency (IEA) notes that buildings account for approximately 30% of global energy consumption, spurring demand for fans with EC (electronically commutated) motors that consume up to 50% less electricity than conventional AC-motor fans. Government incentive programmes, including ENERGY STAR certifications in North America and ErP (Ecodesign) Directive compliance in Europe, are further reinforcing demand for high-efficiency ventilation fan systems.

Rapid Urbanization and Sustained Growth in the Global Construction Sector

The global construction sector continues to expand at a robust pace, providing a sustained demand base for ventilation fan manufacturers. The United Nations projects that 68% of the world's population will live in urban areas by 2050, up from 55% today, necessitating millions of new residential and commercial buildings all equipped with ventilation infrastructure. The Global Construction Perspectives and Oxford Economics forecast estimated total global construction output to reach US$ 15.5 trillion by 2030.

In Asia Pacific alone, large-scale infrastructure programmes such as India's Smart Cities Mission and China's 14th Five-Year Plan for green building development are generating substantial volume demand for wall-mounted, ceiling-mounted, and inline ducted ventilation fans across diverse end-use applications.

Restraints - High Initial Capital Expenditure and Installation Complexity

Despite long-term energy savings, the relatively high upfront cost of advanced ventilation fan systems, particularly heat-recovery ventilators (HRVs) and energy-recovery ventilators (ERVs), remains a significant adoption barrier, especially in price-sensitive developing markets.

According to the U.S. Department of Energy, a whole-home HRV installation can cost between US$ 1,000 and US$ 4,500, inclusive of equipment and labour, pricing out a large share of low- and middle-income households. The technical complexity of integrating smart fans with Building Management Systems (BMS) further inflates installation and commissioning expenses, discouraging retrofit adoption in aging commercial buildings.

Vulnerability to Raw Material Price Volatility

Ventilation fan manufacturing depends heavily on steel, aluminium, copper windings, and engineered plastics, all commodities exposed to significant price volatility. The London Metal Exchange (LME) reported aluminium prices surging over 40% in 2021–2022 and remaining elevated through 2023, compressing manufacturer margins.

Global supply chain disruptions, amplified by geopolitical tensions and logistics bottlenecks, have further inflated input costs and extended lead times, making it difficult for mid-sized manufacturers to maintain competitive pricing without sacrificing product quality or profitability.

Opportunities - Emergence of Smart and IoT-Integrated Ventilation Fan Systems

The convergence of the Internet of Things (IoT), artificial intelligence, and advanced sensor technology is creating a transformative opportunity for ventilation fan manufacturers to develop intelligent, demand-controlled products. Smart fans equipped with CO2 sensors, temperature and humidity probes, and wireless connectivity protocols (Wi-Fi, Zigbee, Z-Wave) enable real-time air quality monitoring and automatic speed adjustment, reducing energy waste by up to 30–40% compared to fixed-speed counterparts.

The rapid global rollout of smart home ecosystems, such as Amazon Alexa, Google Home, and Apple HomeKit, is expanding consumer acceptance of connected home appliances. Governments in the European Union are also mandating smart-ready buildings under the Smart Readiness Indicator (SRI) framework, opening significant procurement channels for IoT-enabled ventilation solutions.

Growing Adoption in the Healthcare and Food & Beverage Sectors

Stringent infection control protocols in healthcare facilities and rigorous hygiene standards in food processing plants are emerging as high-value growth channels for specialised ventilation fan manufacturers. The World Health Organization (WHO) and ASHRAE Standard 170 mandate minimum air change rates of 6–15 air changes per hour (ACH) in hospital wards and operating theatres, requiring high-performance, low-noise centrifugal and mixed-flow fans.

The U.S. Food & Drug Administration (FDA) and the European Food Safety Authority (EFSA) enforce strict temperature and humidity control in food production environments. As the global healthcare infrastructure investment rises, especially in post-pandemic rebuilding and hospital expansion programmes across the Asia Pacific and the Middle East, demand for specialised, hygienic ventilation fans are expected to grow substantially over the forecast horizon.

Category-wise Analysis

Product Type Insights

Axial fans dominate the ventilation fan market by product type, commanding an estimated market share of approximately 38% in 2026. Their dominance stems from a highly favourable combination of cost-efficiency, simplicity of design, and versatility across a wide spectrum of applications, from domestic bathroom exhausts to large-scale industrial process cooling.

Axial fans move air parallel to the fan shaft and are particularly well-suited for low-resistance, high-airflow applications, making them the default choice in construction and commercial HVAC installations. According to ASHRAE, axial fans are specified in over 60% of low-to-medium pressure ventilation designs globally. Their lower energy consumption profile, especially EC motor-driven axial fans, aligns directly with global Ecodesign Directive requirements, further entrenching their market leadership.

Mounting Type Insights

Wall-mounted fans represent the leading segment within the mounting type category, accounting for approximately 32% of overall market revenue. Their widespread adoption is underpinned by ease of installation, cost-effectiveness, and suitability for a broad range of environments, from residential kitchens and bathrooms to commercial kitchens, warehouses, and light industrial units.

Wall-mounted units do not require duct penetration through ceilings or roof structures, significantly reducing installation time and associated labour costs. The U.S. Census Bureau reported record residential construction permits in 2022 and sustained high levels through 2024, directly translating into elevated demand for wall-mounted ventilation fans. Advances in brushless DC motor technology have further enhanced the performance and energy-efficiency profile of this segment.

Material Type Insights

Metal ventilation fans lead the material type segment with an estimated share of approximately 52%, reflecting their superior durability, heat resistance, and suitability for demanding industrial and commercial environments. Galvanised steel and die-cast aluminium housings are the predominant materials, offering structural robustness under continuous high-speed operation and resistance to elevated temperatures encountered in kitchen exhaust, manufacturing, and HVAC ducting applications.

Industry data from the Air Movement and Control Association International (AMCA) indicates that metal-cased fans are preferred in applications requiring UL or CE fire-rated certifications, which are mandatory in many public and commercial buildings. While plastic fans are gaining traction in the residential segment due to lower weight and cost, metal variants retain a dominant share in B2B and institutional procurement.

Distribution Channel Insights

Distributors & Dealers constitute the leading distribution channel, holding approximately 42% of total market revenue. This channel remains dominant because ventilation fans, especially commercial and industrial-grade units, require technical specification, site survey, and after-sales support that online-only or direct-sale models struggle to replicate.

Established distributor networks provide access to engineering consultants, HVAC contractors, and building developers who collectively influence the majority of large-volume procurement decisions. Trade associations such as the Heating, Air-conditioning and Refrigeration Distributors International (HARDI) report that distributor-led channels account for over 70% of commercial HVAC equipment sales in North America. Nonetheless, the online retail channel is the fastest-growing distribution segment, fuelled by rising contractor and DIY consumer comfort with digital procurement platforms.

End-user Insights

The construction is the dominant end-use segment for ventilation fans, representing approximately 35% of total market demand. New residential, commercial, and institutional construction projects are the primary volume driver, as building codes across major economies mandate minimum ventilation rates per occupant. The International Building Code (IBC) and ASHRAE Standard 62.1 specify mechanical ventilation requirements for all newly constructed buildings, creating inelastic demand for fans in every new build.

The global construction pipeline remains robust: the Dodge Construction Network reported over US$ 1 trillion worth of construction starts in the United States alone in 2023. In the Asia Pacific, India's government target of building 20 million affordable urban houses under the Pradhan Mantri Awas Yojana Urban scheme further amplifies construction-driven ventilation fan procurement.

Regional Insights

North America Ventilation Fan Market Trends and Insights

North America accounted for an estimated 38% share of the global ventilation fan market in 2026. The regional growth is strongly supported by residential renovation activities, stricter indoor air quality regulations, and growing penetration of ENERGY STAR-certified ventilation systems. Increasing adoption of smart HVAC systems and energy-efficient EC motor-based ventilation fans continues to strengthen replacement demand across residential and commercial applications.

- United States Ventilation Fan Market Size

The U.S. dominates the North American ventilation fan market, representing nearly 79% of the regional market in 2026, equivalent to around US$ 1.90 billion. Demand growth is driven by rising residential construction permits, tightening DOE energy-efficiency mandates, and increasing awareness regarding indoor air quality. Expansion of green building certifications such as LEED and WELL standards is accelerating the adoption of advanced ventilation technologies in commercial buildings and institutional infrastructure.

Europe Ventilation Fan Market Trends and Insights

Europe accounted for approximately 27.5% of the global ventilation fan market in 2026, reaching nearly US$ 1.90 billion. The region’s growth is primarily driven by stringent energy-efficiency regulations, accelerated retrofit activities, and implementation of the Energy Performance of Buildings Directive (EPBD). Increasing investments in low-carbon buildings, coupled with rising adoption of heat recovery ventilation systems across residential and commercial sectors, are sustaining long-term market expansion throughout Europe.

- Germany Ventilation Fan Market Size

Germany remains the largest ventilation fan market in Europe, estimated at around US$ 520 Million in 2026. Strong industrial manufacturing activity, strict Ecodesign regulations, and high adoption of energy-efficient HVAC systems continue to support market demand. Growth in smart factories, commercial retrofits, and sustainable residential construction projects is further driving installation of premium ventilation fan systems across the country.

- United Kingdom Ventilation Fan Market Size

The U.K. ventilation fan market is estimated at approximately US$ 340 Million in 2026. Updated Part F Building Regulations, increasing emphasis on indoor air quality, and rising residential renovation projects are major market growth contributors. Demand for low-noise, energy-efficient extractor and inline fans is expanding rapidly across urban residential developments and mixed-use commercial properties.

- France Ventilation Fan Market Size

France accounted for an estimated US$ 300 Million ventilation fan market in 2026. Government-backed renovation programmes, including MaPrimeRénov’, are accelerating deployment of energy-efficient ventilation systems in older residential buildings. Rising demand for balanced ventilation and heat recovery units in low-energy housing projects is expected to support stable long-term market growth across the country.

Asia Pacific Ventilation Fan Market Trends and Insights

Asia Pacific is the fastest-growing regional market and accounted for nearly 30.4% of the global ventilation fan market in 2026, valued at approximately US$ 2.10 Billion. Rapid urbanisation, industrial infrastructure expansion, and increasing disposable income levels are significantly boosting demand across residential, commercial, and industrial applications. Government-led green building initiatives and smart city development programmes are further accelerating adoption of energy-efficient ventilation technologies throughout the region.

- China Ventilation Fan Market Size

China represents the largest ventilation fan market globally, estimated at approximately US$ 980 Million in 2026. Strong domestic manufacturing capabilities, extensive construction activity, and implementation of green building standards under the 14th Five-Year Plan are driving substantial market demand. Expansion of industrial facilities and commercial real estate projects continues to strengthen consumption of centrifugal and axial ventilation fan systems.

- India Ventilation Fan Market Size

India is the fastest-growing major market in Asia Pacific, estimated at around US$ 320 Million in 2026. Rapid urban housing development, increasing investments in smart cities, and rising awareness regarding indoor air quality are key growth drivers. Government initiatives promoting energy-efficient infrastructure and the expansion of commercial real estate projects are accelerating adoption of advanced ventilation systems across metropolitan regions.

- Japan Ventilation Fan Market Size

Japan’s ventilation fan market reached an estimated US$ 290 Million in 2026. Demand is supported by the country’s advanced building automation sector, stringent energy conservation standards, and strong replacement demand from ageing residential infrastructure. Growing emphasis on high-efficiency and low-noise ventilation products in healthcare facilities, commercial buildings, and smart homes continues to support stable market expansion.

Competitive Landscape

The global ventilation fan market exhibits a moderately consolidated structure, with a handful of multinational corporations, including Panasonic Corporation, Mitsubishi Electric, ebm-papst, Systemair AB, and Greenheck Fan Corporation, commanding significant revenue share through diversified product portfolios, global distribution networks, and robust R&D investment.

Key competitive differentiators include motor efficiency ratings, noise levels (dB(A)), smart connectivity features, and compliance with regional energy standards. Market leaders are increasingly pursuing inorganic growth through strategic acquisitions of regional niche players to expand geographic footprint. An emerging trend is the shift toward direct-to-contractor digital sales models and subscription-based maintenance services, which enhance customer lifetime value and create defensible recurring revenue streams.

Key Developments:

- January 2025: Systemair AB announced the commercial launch of its next-generation SAVE VSR series of residential heat-recovery ventilation units featuring integrated CO2 demand-controlled ventilation, targeting the Northern European near-zero energy building segment.

- October 2024: ebm-papst unveiled its AxiEco Protect series of axial fans with patented GreenTech EC motor technology, claiming up to 55% energy savings versus legacy AC-motor equivalents, compliant with the latest EU Ecodesign Regulation fan efficiency requirements.

- March 2023: Panasonic Corporation expanded its WhisperGreen Select product line in North America, introducing models with integrated air quality sensors and compatibility with Amazon Alexa and Google Assistant, reinforcing its position in the smart home ventilation segment.

Global Ventilation Fan Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 4.9 Billion |

|

Current Market Value (2026) |

US$ 6.9 Billion |

|

Projected Market Value (2033) |

US$ 10.7 Billion |

|

CAGR (2026–2033) |

6.4% |

|

Leading Region |

North America (38%) |

|

Dominant Product type |

Axial fans (68.0%) |

|

Top-ranking Mounting Type |

Wall-Mounted Fans (32.0%) |

|

Incremental Opportunity (2026–2033) |

US$ 3.8 Billion |

Companies Covered in Ventilation Fan Market

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Delta Electronics, Inc.

- Systemair AB

- Greenheck Fan Corporation

- Soler & Palau Ventilation Group

- Broan-NuTone

- Vent-Axia Group Limited

- Zehnder Group

- Twin City Fan Companies Ltd.

- Loren Cook Company

- ebm-papst

- FläktGroup

- Havells India Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Midea Group Co., Ltd.

- Nidec Corporation

- Ziehl-Abegg SE

Frequently Asked Questions

The global ventilation fan market is valued at approximately US$ 6.9 Million in 2026 and is forecast to reach US$ 10.7 Million by 2033, expanding at a CAGR of 6.4% during the 2026–2033 forecast period.

Key demand drivers include tightening indoor air quality regulations enforced by bodies such as ASHRAE and the European Commission, rapid urbanisation and construction sector growth in emerging economies, rising awareness of IAQ-related health impacts, and the growing adoption of energy-efficient EC motor fans aligned with ENERGY STAR and Ecodesign Directive compliance requirements.

Axial fans represent the leading product type segment with an estimated market share of approximately 38%. Their dominance is attributable to cost-effectiveness, design simplicity, high-volume airflow capability, and broad applicability across residential, commercial, and industrial ventilation applications, as well as alignment with global energy efficiency mandates.

North America holds the largest regional market share, led by the United States. The region benefits from stringent building energy codes (ASHRAE 62.1, NAECA), a large installed base generating replacement demand, strong consumer awareness of indoor air quality, and a well-established distribution infrastructure serving both the residential and commercial construction sectors.

The integration of IoT connectivity, AI-based demand-controlled ventilation, and smart home ecosystem compatibility presents the most significant near-to-medium-term growth opportunity. This is especially relevant in the healthcare and food & beverage sectors, where regulatory mandates for precise air quality control are driving adoption of intelligent, sensor-enabled ventilation fan systems.