- Home Appliances

- Kitchen Chimney Market

Kitchen Chimney Market Size, Share, and Growth Forecast 2026 - 2033

Kitchen Chimney Market by Product Type (Wall-Mounted Chimney, Built-In Chimney, Island Chimney, Corner Chimney, Others), Distribution Channel (Online, Offline), End-user (Residential, Commercial), and Regional Analysis, 2026 - 2033

Kitchen Chimney Market Size and Trend Analysis

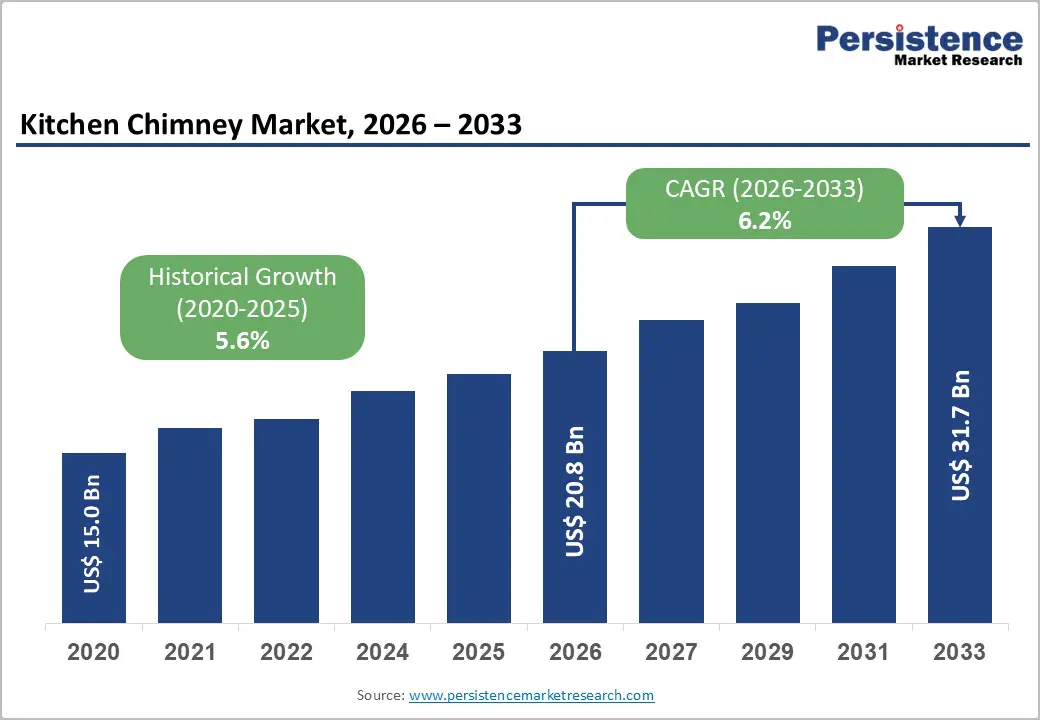

The global kitchen chimney market is expected to be valued at US$ 20.8 billion in 2026 and is projected to reach US$ 31.7 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rapid urbanization across emerging economies, combined with accelerating modular kitchen adoption in middle-income households, is structurally reshaping demand for residential kitchen ventilation solutions in ways that conventional range hood categories cannot fully address.

Key Industry Highlights:

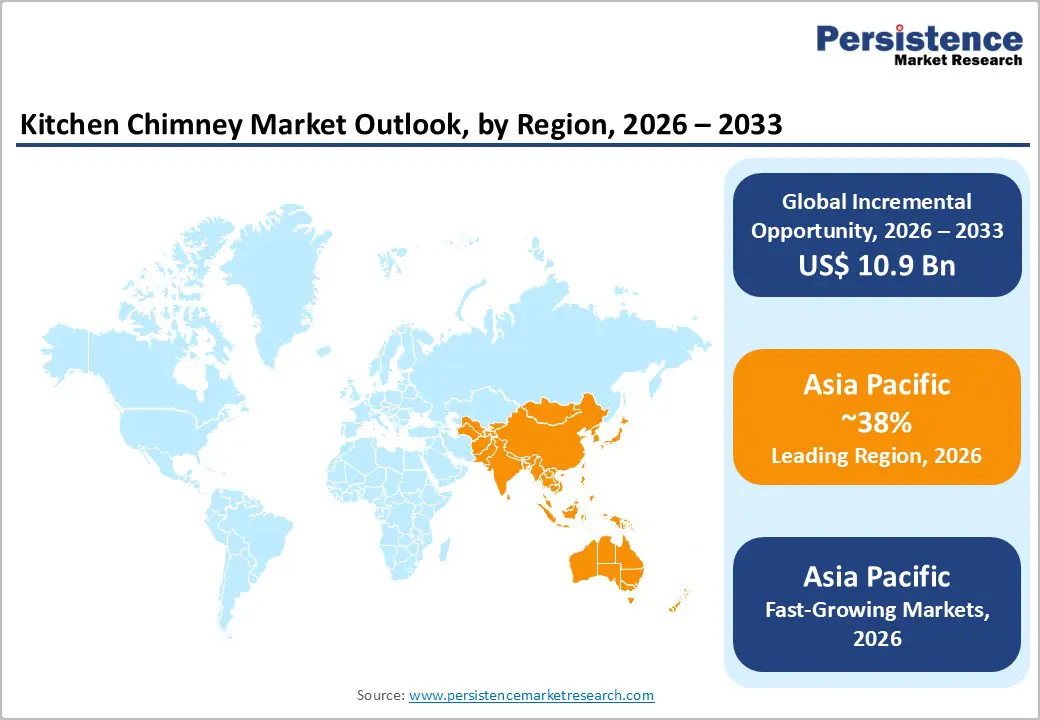

- Leading Region: Asia Pacific's structural dominance at 38% of global kitchen chimney market revenue in 2026 rests on three simultaneous forces: China's prefabricated housing pipeline, India's urban household formation surge, and Southeast Asia's rising mid-income consumer class, a combination that no other region can replicate at an equivalent scale.

- Leading Segment: Wall-mounted chimneys command 38% product type share in 2026, generating US$ 7.90 billion, reinforced by contractor and interior designer specification habits in high-rise residential construction across South and East Asia, where the form factor's compatibility with compact kitchen layouts makes substitution by alternative product types unlikely in the near term.

- Fastest Growing Segment: Built-in chimneys are the fastest growing product type, accelerated by the global premiumisation of residential interiors and the mainstreaming of open-plan kitchen-living configurations in new premium construction; brands offering seamless integration with cabinetry systems will capture disproportionate revenue share.

- Key Opportunity: Commercial kitchen ventilation presents the market's highest-margin strategic opportunity for brands with NSF- or CE-certified high-suction island chimney and built-in chimney products, as cloud kitchen operator expansion and tightening municipal ventilation code enforcement across North America and Europe create a compliance-driven replacement cycle that will sustain commercial end-use growth above residential rates through the forecast period.

Market Dynamics

Drivers - Rise in Modular Kitchen Penetration Driven by Urban Housing Policy

The synchronised expansion of prefabricated modular kitchens across South and Southeast Asia, where wall-mounted and built-in chimney units are standard specifications rather than optional upgrades.

China's Ministry of Housing and Urban-Rural Development issued its Prefabricated Building Action Plan, mandating that prefabricated construction account for at least 30% of new urban floor area in major cities by 2025, a policy that directly embeds kitchen ventilation units into project bills of materials at scale. As prefabricated housing pipelines mature through 2027, original equipment manufacturers supplying stainless steel chimney units with integrated baffle filter technology will see project-driven volume orders displace fragmented retail demand, rewarding players with certified supply chains and installer partnerships.

IoT Integration and Auto-Clean Technology Elevating Average Selling Prices

Consumer willingness to pay a premium for smart kitchen appliances, specifically IoT-enabled chimneys with touch control panels, motion-sensor activation, and auto-clean technology, is compressing the entry-level segment while inflating revenue per unit at the mid-to-premium tier.

Elica S.p.A. launched its connected NikolaTesla Switch range in 2023, embedding gesture-based controls and app connectivity into its induction-chimney combination units, achieving a retail price point approximately 35% above equivalent non-connected models in the European market. Over the next two to three years, as the cost of embedded Wi-Fi and sensor modules is expected to experience a continuous decline as per IEC 62368-1 safety standard harmonisation across the EU and India, IoT-enabled chimneys will migrate from the premium segment into mainstream mid-market price bands, broadening addressable revenue pools for incumbent brands.

Restraints - High Installation Complexity and Ducting Infrastructure Costs

Ducted chimney systems require permanent structural modifications, ceiling penetrations, rigid duct runs, and external exhaust terminations, which add an estimated US$ 300 per installation in labour and materials beyond the appliance purchase price, suppressing demand in retrofit residential segments where structural intervention is cost-prohibitive.

India's Bureau of Indian Standards (BIS) mandates compliance with IS 12845 for kitchen ventilation ducts, and non-compliant installations in older urban housing stock frequently require full duct replacement, extending payback periods and deterring lower-income buyers from upgrading to ducted systems. New entrants without established installer networks bear a disproportionate share of this friction, as trusted after-sales service relationships remain the primary differentiator in converting aspirational demand into completed transactions.

Raw Material Price Volatility in Stainless Steel and Aluminium

Stainless steel chimney body fabrication and aluminium baffle filter components expose manufacturers to commodity price cycles that are structurally difficult to hedge at the product level, particularly for mid-tier brands lacking long-term supply contracts.

Per London Metal Exchange data, aluminium spot prices oscillated between US$ 2,100 and US$ 2,700 per metric tonne across 2022-2023, creating margin compression of an estimated 7 percentage points for manufacturers without vertically integrated stamping operations. Incumbent players with backward-integrated manufacturing, such as BSH Home Appliances Group, operating its own pressed-steel fabrication facilities, absorb these swings more effectively than contract-assembled brands, widening the competitive moat between tier-one OEMs and regional assemblers.

Opportunities - Premium Commercial Kitchen Ventilation in the Hospitality Sector

Hotel chains, cloud kitchen operators, and quick-service restaurant franchises represent a systematically under-penetrated buyer segment for high-suction-capacity island chimney and built-in chimney systems, and appliance brands with UL or CE-certified commercial-grade products are best positioned to capture this channel.

The National Restaurant Association (U.S.) reported in its 2024 State of the Restaurant Industry report that cloud kitchen operations expanded by approximately 11% year-on-year in North America, each new unit requiring dedicated ventilation infrastructure compliant with local fire and building codes. For this opportunity to materialise fully, manufacturers must invest in commercial certification pathways and direct specification relationships with foodservice design consultants, who act as the primary influence point in commercial kitchen fit-out decisions.

Tier-2 and Tier-3 City Expansion Enabled by E-Commerce Logistics Maturation

Online retail platforms reaching second- and third-tier cities across India, Vietnam, and Indonesia are opening previously inaccessible consumer segments to branded kitchen chimney products at accessible price points, with suction capacity education delivered through video content replacing the traditional in-store demonstration.

Amazon India activated same-day and next-day delivery in over 100 Tier-2 and Tier-3 cities by the end of 2024, effectively converting previously catalogue-only markets into live purchase environments for large appliances, including kitchen chimneys. Regional brands with competitive noise reduction specifications and localised warranty servicing networks, rather than global incumbents reliant on metro-centric service infrastructure, are best positioned to convert this logistics unlock into durable market share gains.

Category-wise Analysis

Product Type Insights

The wall-mounted chimney segment accounts for 38.0% of the global kitchen chimney market in 2026, equivalent to US$ 7.90 billion, establishing it as the clear structural leader across all product type categories. Residential buyers in mid-segment apartment developments consistently select wall-mounted models because they integrate cleanly against tile backsplashes above hob positions without consuming overhead cabinet space, a critical constraint in compact urban kitchens averaging 8 to 12 square metres across South Asian and East Asian new-build formats.

Built-in chimneys are accelerating as the fastest growing product type, driven by architect and interior designer preference for flush, seamless kitchen aesthetics in premium open-plan residential developments. As open-plan living layouts continue to displace traditional closed kitchen configurations in new premium construction, built-in chimney demand will structurally outpace the broader market through the forecast period.

Distribution Channel Insights

The offline distribution channel accounts for 66% of the global kitchen chimney market in 2026, equivalent to US$ 13.73 billion, sustained by the appliance category's inherent need for physical demonstration and post-purchase installation services. Buyers purchasing kitchen chimneys through authorised brand showrooms, large-format electronics retailers such as Croma (India) and Euronics (Europe), and specialty kitchen studio showrooms rely on in-person demonstration of suction capacity, noise reduction performance, and touch control panel functionality before committing to a high-consideration purchase typically priced above US$ 200.

Online channels are the fast-growing distribution segment for kitchen chimneys, propelled by the expansion of EMI-based purchase financing on platforms such as Flipkart and Lazada, which reduces effective entry price barriers for first-time buyers in Southeast Asian and South Asian markets.

End-user Insights

The residential segment accounts for 59.0% of the global kitchen chimney market in 2026, equivalent to US$ 12.27 billion, driven by persistent household formation rates and housing-driven appliance replacement cycles across the Asia Pacific. New homeowners undertaking kitchen renovation or first-fit installation represent the primary residential buyer cohort, selecting wall-mounted or built-in chimneys with auto-clean technology to minimise maintenance frequency, a decisive preference factor among dual-income urban households with limited time for appliance upkeep.

The commercial end-user segment is growing at a faster pace than the residential segment, driven by the proliferation of ghost kitchens, cloud kitchens, and fast-casual dining formats that require purpose-built ventilation infrastructure meeting local health and fire safety codes.

Regional Insights

North America Kitchen Chimney Market Trends and Insights

North America accounts for 28.0% of the global kitchen chimney market in 2026, representing US$ 5.82 billion, with market structure anchored by kitchen renovation activity and the premium appliance replacement cycle across the United States and Canada. The National Kitchen and Bath Association (NKBA) reported that U.S. kitchen renovation spend exceeded US$ 170 billion in 2023, with ventilation upgrades, including high-performance ducted chimney and island chimney installations, among the top five specified improvements.

- United States Kitchen Chimney Market Size

The United States represents an estimated 80% of the North America kitchen chimney market, underpinned by high per-capita renovation expenditure and a mature contractor network that integrates premium chimney systems into both new construction and kitchen remodelling projects. Vent-A-Hood's continued market presence in the premium custom-insert segment, combined with growing builder-grade demand for stainless steel chimney wall-mounted models, positions the U.S. as the region's structural demand anchor through 2033.

Europe Kitchen Chimney Market Trends and Insights

Europe accounts for 24.0% of the global kitchen chimney market in 2026, representing US$ 4.99 billion, shaped by the dual forces of stringent indoor air quality regulation and the region's deep-rooted modular kitchen culture. The European Union's Ecodesign Regulation (EU) 2019/2019, which set minimum energy efficiency requirements for local space heaters and related ventilation appliances, has accelerated the replacement of older under-cabinet hoods with certified ducted chimney systems meeting ErP Tier 2 performance thresholds.

Italy, Germany, and the United Kingdom collectively constitute the dominant demand base, reflecting their combination of high kitchen renovation frequency and consumer acceptance of premium chimney pricing.

- Germany Kitchen Chimney Market Size

Germany represents an estimated 24% of the European kitchen chimney market, driven by a robust kitchen furniture manufacturing sector centred in the Ostwestfalen-Lippe region, where brands such as Nobilia and Häcker integrate certified chimney units as standard kitchen package components. Forward demand is reinforced by Germany's Gebäudeenergiegesetz (GEG) 2023 building energy legislation, which encourages ventilation system upgrades in residential retrofits.

- United Kingdom Kitchen Chimney Market Size

The United Kingdom represents an estimated 16% of the Europe kitchen chimney market, with demand factors driven by a high rate of semi-detached and terraced house kitchen renovation activity and consumer preference for statement-design island chimneys in open-plan extensions. Post-Building Regulations Part F amendments mandating improved kitchen ventilation provisions in both new builds and extensions are expanding the mandatory specification base for chimney-category products.

- France Kitchen Chimney Market Size

France represents an estimated 14% of the European kitchen chimney market, underpinned by a strong tradition of structured meal preparation culture and high consumer sensitivity to odour extraction efficiency. GIFAM data indicates French household appliance replacement cycles average 10 years, creating a predictable replacement demand wave for chimney units entering the end of their service life across the installed base.

Asia Pacific Kitchen Chimney Market Trends and Insights

Asia Pacific accounts for 38.0% of the global kitchen chimney market in 2026, representing US$ 7.90 billion, making it the market's leading region by share and its fast-growing at a CAGR of 7.8% by 2033, powered by simultaneous urbanisation, rising disposable incomes, and policy-driven housing construction across China, India, and Southeast Asia. China's 14th Five-Year Plan prioritised smart home technology adoption and urban housing quality upgrades, directly embedding demand for smart kitchen appliances, including IoT-enabled chimneys, into national policy objectives.

- China Kitchen Chimney Market Size

China represents an estimated 38% of the Asia Pacific kitchen chimney market, supported by a mature domestic manufacturing ecosystem and consumer demand for high-suction-capacity stainless steel chimney models tailored to wok-cooking's intense heat and smoke generation. Haier Group's 2024 launch of its Leader sub-brand chimney line at sub-¥2,000 price points has expanded volume penetration into lower-tier city households, signalling accelerating democratisation of the category beyond premium urban segments.

- India Kitchen Chimney Market Size

India represents an estimated 25% of the Asia Pacific kitchen chimney market, with Kaff Appliances and Glen Appliances competing aggressively in the INR 8,000 to INR 20,000 mid-segment through baffle filter and auto-clean technology differentiation pitched at first-time buyers in Tier-1 cities. India's PM Vishwakarma Scheme (2023), which provides subsidised skill training to kitchen installation artisans, is simultaneously expanding the trained installer base that underpins after-sales conversion in non-metro markets.

- Japan Kitchen Chimney Market Size

Japan represents an estimated 12% of the Asia Pacific kitchen chimney market, with demand characterised by preference for ultra-quiet noise reduction specifications, particularly below 45 dB, driven by compact high-density apartment living where ventilation noise directly affects residential liveability.

Panasonic's FY2024 domestic appliance division reported growing traction for its whisper-quiet ceiling-integrated chimney models among condominium developers in the Greater Tokyo Area, a deployment context that is gradually expanding to Osaka and Nagoya metropolitan markets.

Competitive Landscape

The global kitchen chimney market operates as a moderately consolidated competitive landscape, with Elica, Faber, and BSH Home Appliances Group (Bosch/Siemens brands) collectively holding an estimated 32% of global revenue, competing primarily on suction capacity ratings, auto-clean technology differentiation, and design aesthetics. The dominant strategic theme across tier-one players is platform premiumisation, bundling chimney units with matching hob and oven products to drive attachment rate and increase average basket size per kitchen project.

Samsung Electronics represents the most credible disruptive entrant, leveraging its SmartThings IoT ecosystem to position connected kitchen chimneys as nodes within a broader smart home platform, a strategy that incumbents without equivalent software ecosystems cannot easily replicate. Laggards are distinguished by dependence on single-channel retail distribution and the absence of certified commercial-grade product lines.

Key Developments:

- January 2025: Elica announced a strategic manufacturing capacity expansion at its Fabriano, Italy facility, adding a dedicated production line for IoT-enabled chimney units targeting the European and Middle East premium residential markets.

- March 2024: Whirlpool Corporation introduced its Connected Kitchen Suite in North America, incorporating a ducted chimney with voice-activation via Amazon Alexa and auto-diagnostics, priced at a 22% premium over its previous flagship ventilation model.

- September 2024: Hindware Smart Appliances completed the rollout of its Auto-Clean Plus chimney series across 8,000 retail touchpoints in India, supported by a dedicated service network expansion covering 180 cities to address after-sales barriers in non-metro markets.

Companies Covered in Kitchen Chimney Market

- Elica S.p.A.

- Faber S.p.A.

- Whirlpool Corporation

- BSH Home Appliances Group

- Panasonic Corporation

- Samsung Electronics Co., Ltd.

- Miele & Cie. KG

- Falmec S.p.A.

- Hindware Smart Appliances

- Kaff Appliances (India) Pvt. Ltd.

- Glen Appliances Pvt. Ltd.

- Franke Group

- Siemens Home Appliances (BSH)

- Vent-A-Hood Ltd.

- Haier Group Corporation

- Smeg S.p.A.

- Bertazzoni S.p.A.

- ROBAM Appliances Co., Ltd.

- Fotile Group

- IFB Industries Ltd.

Frequently Asked Questions

The global kitchen chimney market is valued at US$ 20.8 Billion in 2026 and is projected to reach US$ 31.7 Billion by 2033, expanding at a CAGR of 6.2%. The primary growth catalyst is accelerating modular kitchen adoption across Asia Pacific's urbanising middle-income population, supported by government-backed housing construction programmes generating systematic first-fit appliance demand.

National housing policy mandates, such as China's 14th Five-Year Plan prefabricated construction targets, embedding ventilation systems into project specifications at scale, and second, consumer premiumisation toward auto-clean technology and touch control panel features that raise average transaction values and stimulate earlier replacement cycles.

Wall-mounted chimneys hold the largest product type share at 38.0% of the global kitchen chimney market in 2026, because their form factor aligns precisely with the space constraints and duct-routing economics of high-rise urban apartment kitchens across Asia and Europe.

Asia Pacific dominates the kitchen chimney market with 38.0% revenue share in 2026, driven by two structural factors: the region's unmatched pace of urban household formation, projected by the Asian Development Bank to add hundreds of millions of new urban residents by 2040, and deeply embedded high-temperature cooking cultures across China and India that generate intense ventilation demand relative to Western counterparts. As Southeast Asian markets, including Vietnam and Indonesia, formalise housing finance systems, Asia Pacific's demand advantage will continue widening through 2033.

The most actionable opportunity in the global kitchen chimney market is commercial kitchen ventilation for cloud kitchen and quick-service restaurant operators, where compliance with evolving ASHRAE Standard 154 ventilation codes in North America and equivalent EN 16282 standards in Europe creates mandatory procurement cycles that premium commercial appliance brands can systematically capture.

Regional appliance brands with strong Tier-2 and Tier-3 city service networks in South and Southeast Asia are best positioned to capture the second major opportunity, first-time residential buyers accessing the category via maturing e-commerce logistics infrastructure.

Elica, Faber, and BSH Home Appliances Group are the leading companies in the global kitchen chimney market, collectively commanding an estimated 28-32% of global revenue through product innovation in suction capacity, baffle filter technology, and smart connectivity. The competitive landscape is moderately consolidated at the premium tier but highly fragmented in the mid-to-value segment.