- Home Appliances

- Deep Fryer Market

Deep Fryer Market Size, Share, and Growth Forecast 2026 - 2033

Deep Fryer Market by Product Type (Electric Deep Fryers, Gas Deep Fryers, Air Fryers with Deep Fry Function, Commercial Deep Fryers), by Capacity (Less than 2 Liters, 2-5 Liters, Above 5 Liters), Application (Residential, Commercial), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Electronics Stores), and Regional Analysis, 2026 - 2033

Deep Fryer Market Size and Trend Analysis

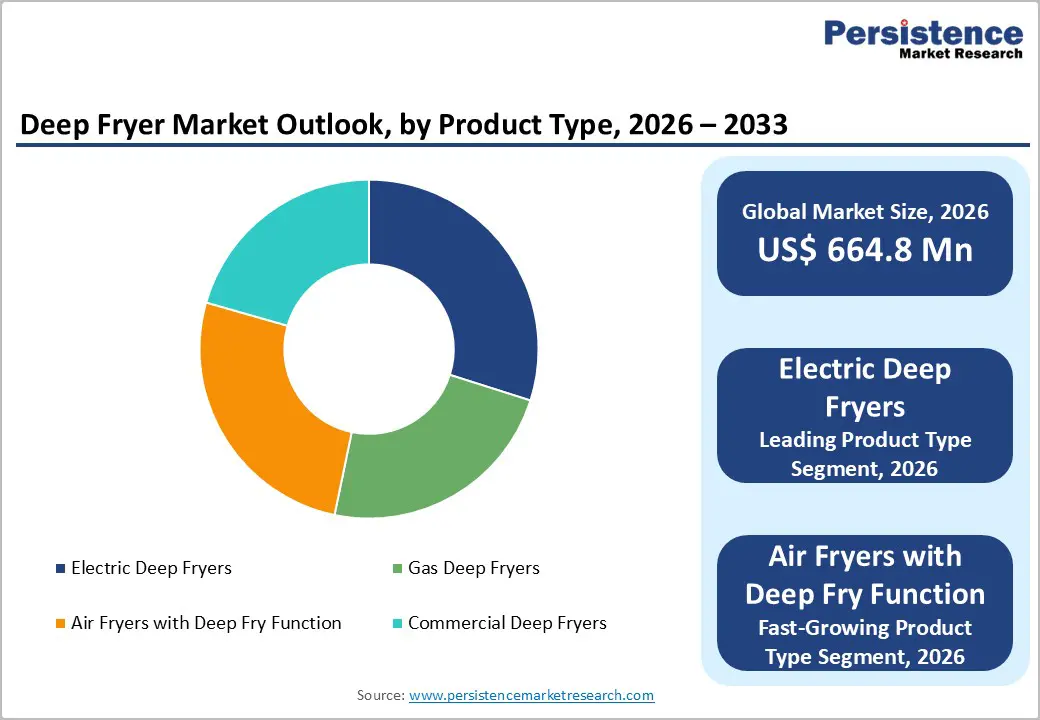

The global deep fryer market size is expected to be valued at US$ 664.8 million in 2026 and projected to reach US$ 986.5 million by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

Rising consumer appetite for fried foods such as French fries, chicken nuggets, and tempura is lifting market demand. According to the United States Department of Agriculture (USDA), per-capita potato consumption in the U.S. stands near 49 pounds annually, largely as frozen fries. Expanding quick-service restaurants, cloud kitchens, and adoption of energy-efficient electric and oil-less fryers further reinforce growth.

Key Industry Highlights:

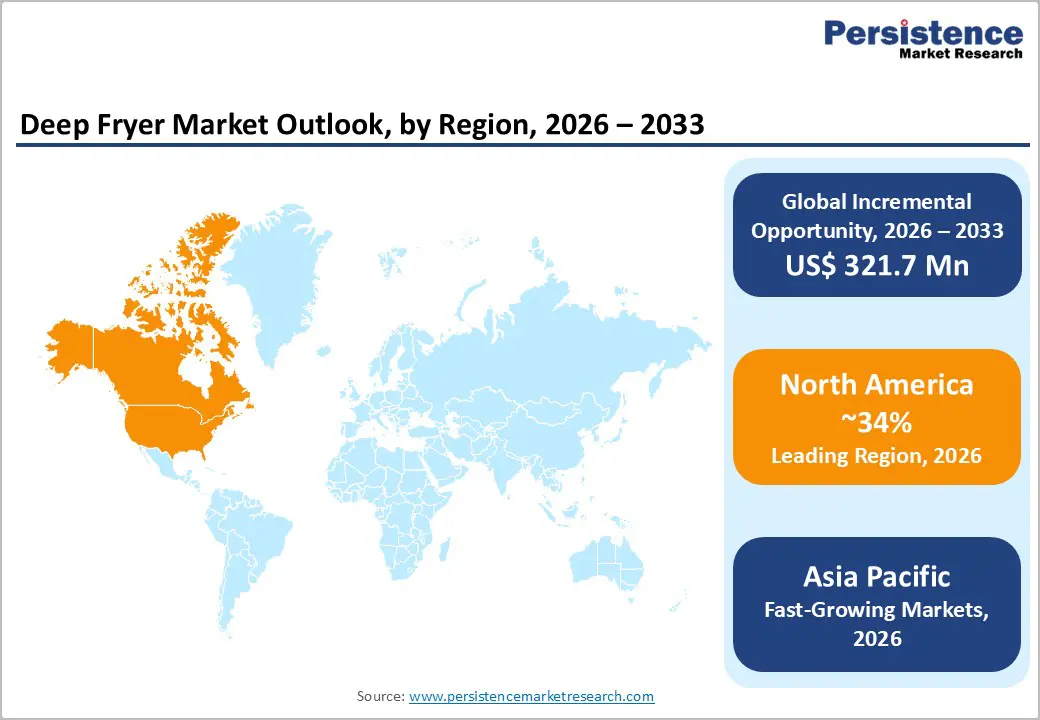

- Leading Region: North America dominates the global deep fryer market with a 34% share in 2025, anchored by a dense QSR network and high household appliance penetration.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2032, fuelled by urbanization, rising incomes, and rapid air fryer adoption across China, India, and Southeast Asia.

- Dominant Segment: Electric deep fryers lead the product-type category with a 52% share in 2025, supported by affordability, ease of use, and broad residential availability.

- Fast-Growing Product Segment: Air fryers with deep-fry function are the fastest-growing product type over 2025 - 2032, driven by health-conscious consumers and low-oil cooking trends.

- Key Opportunity: Smart, IoT-enabled, ENERGY STAR-certified deep fryers present a major opportunity, helping QSR chains cut oil and energy use by 30-50%.

Market Dynamics

Drivers - Aggressive Quick-Service Restaurant and Cloud Kitchen Network Expansion Worldwide

The rapid global expansion of quick-service restaurant (QSR) chains and online food delivery platforms is among the most powerful demand engines for commercial deep fryers. The National Restaurant Association reported that U.S. restaurant industry sales reached an all-time high of US$ 1.1 trillion in 2024, with QSRs accounting for a substantial share of new operator additions and remodels through the year.

Globally, McDonald's operated more than 43,000 outlets by year-end 2024, while Yum! Brands (KFC, Pizza Hut, Taco Bell) crossed 61,000 restaurants. Each new outlet typically requires two to four high-capacity gas or electric fryers, anchoring sustained replacement and new-installation demand and creating a multi-year procurement runway for established commercial fryer manufacturers across North America, Europe, and Asia Pacific.

Rising Health-Conscious Shift Toward Low-Oil Air Fryer Hybrids

Consumer preference for low-oil cooking is reshaping kitchen appliance purchases worldwide, especially in North America and Europe. Data from the U.S. Centers for Disease Control and Prevention (CDC) shows that adult obesity prevalence has crossed 40%, pushing households toward modern appliances that cut oil usage by up to 70-80% versus conventional deep frying methods at home.

This has driven manufacturers such as Philips, Ninja, and Tefal to launch hybrid deep fryers featuring rapid air technology, dual-zone baskets, and digital presets, accelerating adoption in residential kitchens. The cookware and small appliances category tracked by Eurostat continues to log positive household equipment expenditure growth across the European Union, reinforcing the shift toward premium, health-oriented fryer models in mature markets.

Restraints - Mounting Health Concerns Around Trans-Fat and Fried Food Consumption

Mounting clinical evidence on the risks of high-trans-fat and deep-fried diets is restraining adoption among health-conscious consumers in developed economies. The World Health Organization (WHO) estimates that industrially produced trans-fats contribute to more than 278,000 deaths globally each year from coronary heart disease, prompting national bans and regulatory limits across more than 60 countries worldwide.

The American Heart Association recommends limiting fried food intake to not more than once a week, prompting a steady migration toward grilling, baking, and air-frying methods at home. This dietary shift, reinforced by public-health campaigns from the U.S. Food and Drug Administration (FDA), slows volume growth of traditional oil-bath fryers, particularly across mature North American and Western European markets.

Volatile Edible Oil Prices and Rising Commercial Energy Costs

Sharp swings in palm, soybean, and sunflower oil prices, alongside elevated electricity tariffs, are squeezing operating economics for commercial deep fryer users worldwide. According to the Food and Agriculture Organization (FAO) Vegetable Oil Price Index, vegetable oil prices spiked over 30% between 2023 and 2024 amid weather disruptions, export curbs from Indonesia, and rising biofuel-driven demand from blending mandates.

Rising input costs are forcing smaller restaurants and street-food operators to delay fryer upgrades or trade down to lower-tier models. Higher European energy tariffs reported by Eurostat, with non-household electricity prices remaining well above pre-2022 levels, continue to weigh on commercial-kitchen capex decisions and slow replacement cycles among independent food-service operators across the region.

Opportunities - Smart, IoT-Connected, ENERGY STAR-Certified Commercial Fryer Adoption Pipeline

The shift toward connected kitchens presents a sizeable runway for manufacturers offering Wi-Fi-enabled deep fryers with auto-temperature control, oil-quality sensors, and smartphone app integration. The International Energy Agency (IEA) highlights that mandatory energy-efficient appliance standards are now active in over 100 countries, accelerating procurement of certified equipment by global hospitality and quick-service chains.

ENERGY STAR certifications administered by the U.S. Environmental Protection Agency (EPA) for commercial fryers can cut energy use by 30-50% versus standard models. Established players, including Henny Penny, Frymaster (a Welbilt brand), and Pitco, are commercializing low-oil-volume vat designs and high-efficiency burners that align with corporate carbon-reduction targets, opening multi-year procurement pipelines with global QSR chains.

Asia Pacific Air Fryer Hybrid Boom in Urban Households

Asia Pacific kitchens are upgrading from basic frying pans to multi-functional air fryer-deep fryer hybrids at an accelerating pace, supported by rising disposable incomes and rapid urbanization. Data from the World Bank indicates that the urban share of Asia's population has crossed 51%, with India alone projected to add 270 million urban residents by 2040, expanding the addressable consumer base.

E-commerce platforms such as Amazon and Flipkart consistently rank air fryers among their top-selling small appliances during festive periods like Diwali and Singles' Day. Brands such as Havells, Bajaj Electricals, and Panasonic are localizing product lines with smaller capacities and regional cuisine presets to capture this fast-rising middle-class consumer cohort across India and Southeast Asia.

Category-wise Analysis

Product Type Insights

Electric deep fryers lead the global product-type segment with an estimated 52% market share in 2025, owing to lower upfront costs, ease of installation, and broad availability across both residential and small-commercial settings. According to the U.S. Energy Information Administration (EIA), electricity remains a more accessible cooking-energy source than piped natural gas across most non-metropolitan U.S. counties, supporting electric fryer penetration among first-time household buyers.

Air fryers with deep-fry function are emerging as the fastest-growing sub-segment, propelled by health-conscious cooking trends and rising demand for low-oil hybrid appliances. Manufacturers, including Philips, Ninja, Tefal, Hamilton Beach, and Cuisinart, continue to launch dual-zone baskets, rapid-air technology, and digital presets, accelerating residential adoption across North America, Europe, and increasingly across Asia Pacific kitchens.

Capacity Insights

The 2-5 liters capacity segment is the leading category, accounting for roughly 47% of global deep fryer revenue in 2025. This range hits the sweet spot for nuclear-family households and small food outlets serving 4-8 portions per cycle. Per the United Nations Department of Economic and Social Affairs (UN DESA), average global household size has fallen to about 3.5 persons, which aligns with mid-capacity fryer purchases.

The Above 5 Liters segment is the fastest-growing capacity category, fueled by aggressive cloud-kitchen rollouts, ghost-kitchen platforms, and the expansion of high-throughput QSR outlets worldwide. Larger oil-bath capacities support faster batch cycles for fries, chicken, and seafood, with operators such as McDonald's, KFC, and Burger King standardizing high-volume commercial fryer specifications across new store openings in Asia Pacific and Latin America.

Application Analysis

The commercial application segment dominates the deep fryer market with around 61% revenue share in 2025, propelled by the global proliferation of restaurants, hotels, institutional canteens, and fast-food chains. The U.S. Bureau of Labor Statistics counted more than 1 million food service and drinking establishments in the United States alone, each typically operating one or more fryer units across daily service shifts.

The residential segment is the fastest-growing application category, driven by air fryer hybrids, rising at-home cooking, and growing consumer interest in restaurant-style fried recipes. Post-pandemic shifts in home dining behavior, supported by data from the U.S. Bureau of Economic Analysis (BEA) showing sustained at-home food expenditure, are pushing households across North America, Europe, and the Asia Pacific toward modern countertop fryers with smart connectivity.

Distribution Channel Analysis

Supermarkets and hypermarkets remain the leading distribution channel, capturing approximately 39% of global deep fryer sales in 2025. Big-box retailers such as Walmart, Costco, Carrefour, and Tesco offer wide product visibility, demonstration zones, and seasonal promotions. The U.S. Census Bureau reports that warehouse clubs and supercenters generated annual retail sales exceeding US$ 850 billion, reflecting their scale advantage in small-appliance distribution.

Online retail is the fastest-growing distribution channel, supported by aggressive festive sales on Amazon, Flipkart, and JD.com, along with manufacturer-direct e-commerce stores. Detailed product listings, verified consumer reviews, doorstep delivery, and easy-return policies are converting first-time buyers, while social-commerce features on platforms such as TikTok Shop and Instagram are amplifying air fryer demand among younger urban consumers globally.

Regional Insights

North America Deep Fryer Market Trends and Insights

North America leads the global deep fryer market with a 34% share in 2025, driven by a dense quick-service restaurant network, high household appliance penetration, and continuous menu innovation around fried offerings. Trends include rising adoption of ENERGY STAR-certified commercial fryers, oil-management automation, and a strong replacement cycle linked to ageing kitchen equipment in established chains.

- U.S. Deep Fryer Market Size

The United States accounts for roughly 82% of North American deep fryer revenue, with country-level sales estimated near US$ 185 million in 2026. Growth is supported by more than 200,000 QSR locations tracked by the National Restaurant Association, widespread air fryer adoption in households, and steady refresh cycles by leading chains.

Europe Deep Fryer Market Trends and Insights

Europe represents a mature yet steadily expanding market shaped by stringent energy-efficiency regulations, EU ecodesign rules, and a strong tradition of fried foods such as French fries, fish & chips, and churros. Demand is migrating toward low-oil air fryer hybrids, programmable digital fryers, and induction-compatible commercial units across HORECA buyers in Western and Northern Europe.

- Germany Deep Fryer Market Size

Germany commands close to 23% of European deep fryer revenue, with country-level sales estimated at around US$ 42 million in 2026. Demand is anchored by a strong gastronomy culture, more than 222,000 food-service enterprises reported by the Federal Statistical Office (Destatis), and brisk household uptake of premium small appliances.

- U.K. Deep Fryer Market Size

The United Kingdom holds nearly 18% of European deep fryer revenue, with sales projected close to US$ 33 million in 2026. Demand is sustained by an iconic fish & chip sector with over 10,000 outlets tracked by industry associations, alongside rapid air fryer adoption among UK households reported by the Office for National Statistics (ONS).

- France Deep Fryer Market Size

France contributes around 15% of European deep fryer revenue, with country sales estimated at US$28 million in 2026. The market benefits from deep cultural ties to pommes frites, an extensive bistro and brasserie network captured by INSEE, and the global presence of homegrown brand Tefal (Groupe SEB) in air fryer innovation.

Asia Pacific Deep Fryer Market Trends and Insights

Asia Pacific is the fastest-growing region through 2032, fuelled by urbanization, rising disposable incomes, and rapid expansion of QSR and cloud-kitchen formats across China, India, and Southeast Asia. China alone hosts more than 9 million food-service outlets per the National Bureau of Statistics of China, anchoring demand for compact electric fryers and high-throughput commercial units.

- India Deep Fryer Market Size

India contributes nearly 12% of the Asia Pacific deep fryer revenue, with country sales close to US$ 24 million in 2026. Demand is driven by a booming organized food-service sector tracked by the Ministry of Food Processing Industries, festive-season air fryer purchases, and aggressive online retail discounts that broaden first-time buyer access.

- Japan Deep Fryer Market Size

Japan holds about 14% of Asia Pacific deep fryer sales, valued near US$ 28 million in 2026. The market is supported by a long-standing tempura and tonkatsu food culture, premium-appliance preferences from Panasonic and Zojirushi, and steady commercial demand from convenience-store chains documented by the Japan Franchise Association.

- Southeast Asia Deep Fryer Market Size

Southeast Asia accounts for roughly 20% of regional deep fryer revenue, with combined sales near US$ 39 million in 2026. Indonesia, Thailand, Vietnam, and the Philippines lead growth, supported by vibrant street-food economies, the ASEAN bloc's expanding middle class, and rapid QSR rollouts highlighted by national investment boards across the region.

Competitive Landscape

The global deep fryer market is moderately fragmented, with a mix of multinational appliance manufacturers, regional brands, and private-label suppliers competing across residential and commercial segments. Leading players differentiate through energy-efficient burner technology, advanced oil-filtration systems, IoT-enabled connectivity, and dual-zone air fryer designs that align with evolving consumer and regulatory expectations.

Strategic priorities include capacity expansion across Asia, long-term supply partnerships with QSR chains, and targeted acquisitions to broaden countertop appliance portfolios. Subscription-based oil-management services, ENERGY STAR certification, and direct-to-consumer e-commerce are emerging business models, supported by sustained R&D investments in low-oil and connected-kitchen cooking platforms.

Key Developments:

- In March 2025, Ninja (SharkNinja) expanded its Double Stack XL air fryer line-up across European retail channels, introducing higher-capacity dual-zone hybrids with rapid-air technology, targeting family-size households seeking versatile low-oil cooking appliances for everyday kitchen use.

- In October 2024, Welbilt launched a next-generation Frymaster commercial deep fryer equipped with built-in oil-quality sensors, IoT diagnostics, and predictive maintenance features, aimed at large global QSR operators seeking to cut oil consumption, energy costs, and equipment downtime.

- In July 2024, Groupe SEB unveiled new Tefal Easy Fry models featuring smart guided cooking, connected app integration, and personalized recipe presets, reinforcing its leadership in the European low-oil fryer segment and strengthening its premium connected-kitchen appliance portfolio worldwide.

Deep Fryer Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 516.4 million |

| Current Market Value (2026) | US$ 664.8 million |

| Projected Market Value (2033) | US$ 986.5 million |

| CAGR (2026 - 2033) | 5.8% |

| Leading Region | North America, 34% |

| Dominant Category-1 (Product Type) | Electric Deep Fryers, US$ 345.7 million |

| Top-ranking Category-2 (Capacity) | 2-5 Liters, US$ 312.5 million |

| Incremental Opportunity | US$ 321.7 million (2026 - 2033) |

Companies Covered in Deep Fryer Market

- Groupe SEB

- Koninklijke Philips N.V.

- SharkNinja Operating LLC

- De'Longhi S.p.A.

- Hamilton Beach Brands Holding Company

- Conair LLC

- National Presto Industries, Inc.

- Welbilt, Inc.

- Henny Penny Corporation

- Pitco Frialator, Inc.

- Electrolux Professional AB

- Panasonic Corporation

- Havells India Ltd.

- Bajaj Electricals Ltd.

- Whirlpool Corporation

- Breville Group Limited

- Zojirushi Corporation

- Midea Group

Frequently Asked Questions

The global deep fryer market is expected to be valued at US$ 664.8 million in 2026 and is projected to reach US$ 986.5 million by 2033, growing at a CAGR of 5.8% during the forecast period.

The primary demand driver is the rapid global expansion of quick-service restaurants and cloud kitchens, with the National Restaurant Association noting U.S. restaurant industry sales of US$ 1.1 trillion in 2024, alongside surging adoption of low-oil air fryer hybrids in households.

North America leads the global deep fryer market with around 34% share in 2025, driven by a dense QSR network, high household appliance penetration, and steady replacement cycle among major U.S. restaurant chains.

Smart, IoT-enabled, and ENERGY STAR-certified deep fryers represent a major opportunity, with the U.S. Environmental Protection Agency (EPA) noting energy savings of 30-50% for certified commercial fryers, supporting cost and sustainability goals.

Key players include Groupe SEB, Koninklijke Philips N.V., SharkNinja, De'Longhi, Hamilton Beach, and Welbilt.