- Sporting Goods & Equipment

- Tennis Equipment Market

Tennis Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Tennis Equipment Market by Product Type (Tennis Racquets, Tennis Balls, Apparel, Footwear, Ball Machines, Tennis Bags, Other Accessories), by Material (Composites, Metallic, Other Materials), by End Use (Tennis Equipment for Individuals, Tennis Equipment for Institutional Use), and Regional Analysis, 2026 - 2033

Tennis Equipment Market Size and Trend Analysis

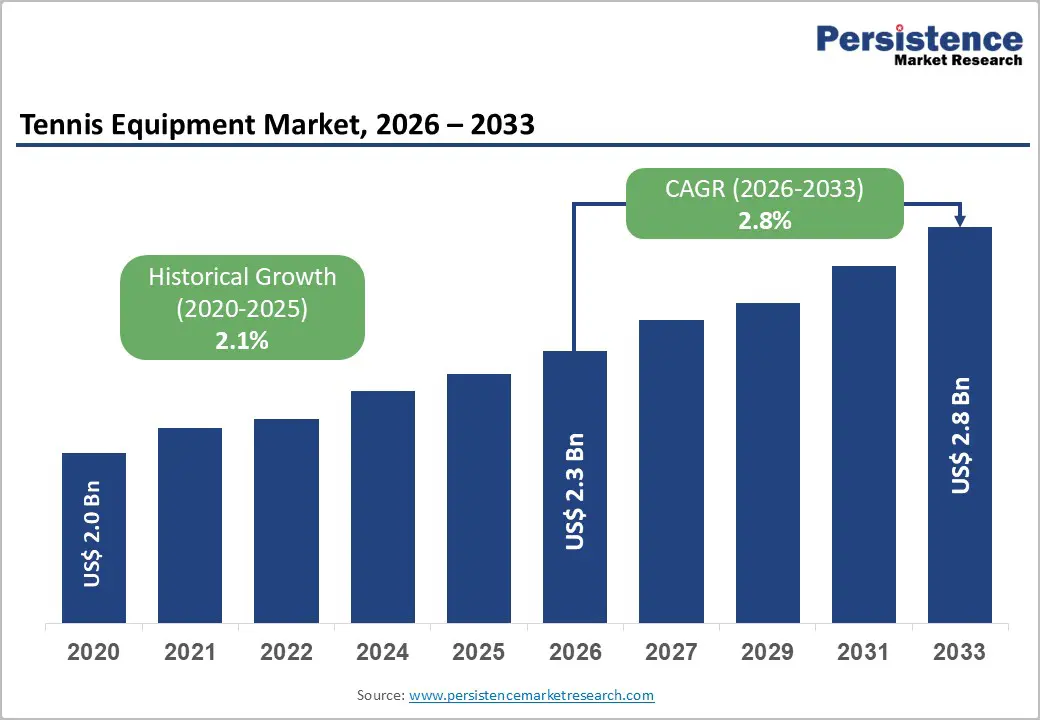

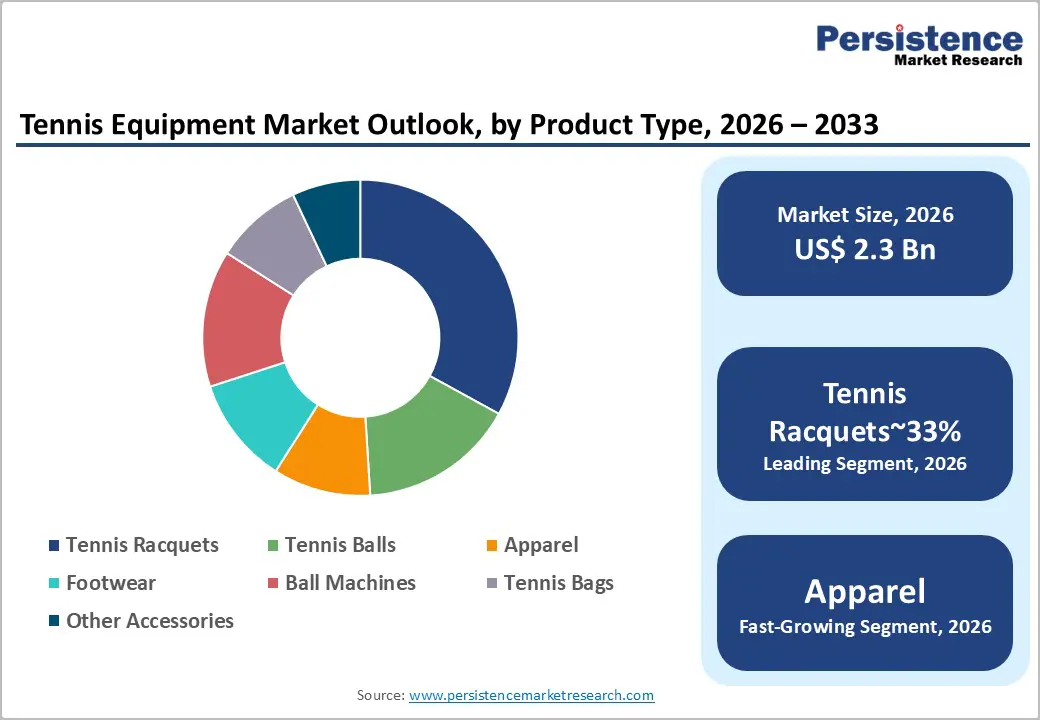

The global tennis equipment market is likely to be valued at US$ 2.3 billion in 2026 and is expected to reach US$ 2.8 billion by 2033, growing at a CAGR of 2.8% during the forecast period from 2026 to 2033.

This steady growth trajectory is anchored by rising global tennis participation rates, growing health and fitness awareness among urban populations, and the sustained influence of professional tournaments and celebrity athlete endorsements on consumer purchasing behavior.

Key Industry Highlights:

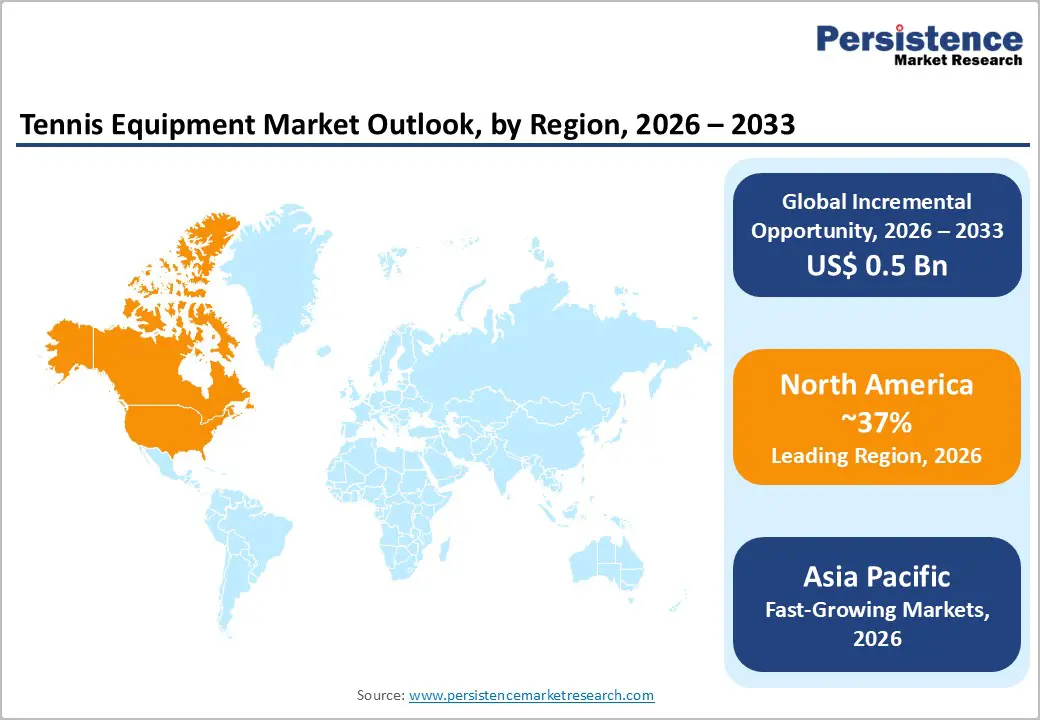

- Leading Region: North America leads the global Tennis Equipment market holding 37% share in the market, with the United States home to an estimated 21.6 million active tennis players supported by the USTA's extensive development infrastructure, strong brand loyalty toward premium products, and a thriving professional tournament ecosystem.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 4.2%, with China, India, and ASEAN economies registering rising tennis participation driven by urbanization and middle-class lifestyle shifts. Japan and China also provide significant manufacturing advantages that support regional cost competitiveness and export capabilities.

- Leading Segment: Tennis Racquets dominate the Product Type category with approximately 33% market share, fueled by consistent replacement cycle demand, continuous composite technology innovation, and strong athlete endorsement-driven consumer aspirations across recreational and competitive player segments worldwide.

- Fastest-Growing Segment: The Composites material segment is the most dominant and fastest-growing, commanding approximately 62% material share. Advanced carbon fiber and graphite composite technologies continue to deliver superior performance benefits over metallic alternatives, driving sustained adoption across all racquet and equipment categories.

- Key Market Opportunity lies in institutional procurement from expanding tennis academies, schools, and sports clubs globally. Programs supported by the ITF and national associations such as AITA in India create high-volume, repeat-purchase institutional demand for racquets, ball machines, and accessories.

| Key Insights | Details |

|---|---|

| Tennis Equipment Market Size (2026E) | US$ 2.3 Billion |

| Market Value Forecast (2033F) | US$ 2.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 2.8% |

| Historical Market Growth (2020 - 2025) | 2.1% |

Market Dynamics

Drivers - Rising Global Participation and Fitness Awareness Driving Sustained Long-Term Growth in Tennis Equipment Demand

Growing awareness of tennis as a lifelong fitness activity remains the primary structural driver of sustained demand in the global tennis equipment market. The International Tennis Federation (ITF) estimates that more than 87 million people play tennis worldwide, with participation steadily increasing across Asia, Latin America, and Africa. This growth is supported by junior development initiatives and expanding recreational court infrastructure.

In the post-pandemic period, consumers have shown a stronger preference for outdoor and individual sports, positioning tennis as an attractive option for active lifestyles. Municipal investments in public tennis courts, particularly in France, the United Kingdom, and Australia, have reduced entry barriers for new players. As the global player base expands, demand continues to rise for entry-level and mid-range racquets, apparel, footwear, and balls, supporting healthy and consistent market growth across major product categories through 2033.

Grand Slam Tournaments and Elite Athlete Endorsements Strengthening Brand Influence and Consumer Purchase Decisions

The global professional tennis circuit plays a powerful role in shaping consumer demand for tennis equipment. Prestigious tournaments such as the Wimbledon, French Open, US Open, and Australian Open attract hundreds of millions of viewers worldwide, generating strong aspirational appeal. Recreational players often seek to replicate the equipment choices of top professionals, directly influencing purchasing decisions.

Leading brands such as Wilson Sporting Goods and Babolat strategically leverage partnerships with Grand Slam champions to strengthen brand loyalty and sustain premium pricing. According to the Association of Tennis Professionals (ATP) and the Women's Tennis Association (WTA), prize money and sponsorship revenues reached record highs in 2023-2024, further increasing global visibility of equipment brands and driving retail sales growth worldwide.

Restraint - Price Sensitivity in Emerging Markets Limiting Premium Equipment Penetration Despite Rising Tennis Participation

Despite strong long-term growth prospects, the tennis equipment market faces challenges related to price sensitivity among mass-market and entry-level consumers. Premium racquets from established brands such as Wilson, Babolat, and Head N.V. are typically priced between US$150 and US$400, making them aspirational but often unaffordable for many players in developing regions. In fast-growing markets across Asia, Latin America, and Africa, purchasing power constraints remain a structural limitation despite rising participation.

The availability of lower-cost, unbranded alternatives, particularly from manufacturers in China and other cost-efficient production hubs, adds competitive pressure and fragments retail spending. As a result, average selling prices in these regions may experience downward pressure. This dynamic creates a balancing challenge for premium brands seeking growth in emerging markets while maintaining pricing integrity and protecting long-term brand positioning.

Seasonal Weather Dependence Creating Revenue Volatility and Inventory Challenges Across Key Tennis Markets

Tennis remains predominantly an outdoor sport, making equipment demand highly sensitive to seasonal weather patterns and climate conditions. In markets such as Germany, Northern Europe, and Canada, sales of balls, apparel, and footwear typically decline during winter months, leading to noticeable seasonal revenue fluctuations for manufacturers and retailers. Limited availability and high costs associated with indoor tennis courts restrict year-round participation in many regions.

The Lawn Tennis Association (LTA) in the United Kingdom has consistently identified adverse weather as a key barrier to sustained adult participation. Reduced playing frequency during colder months directly impacts annual equipment replacement cycles and moderates total purchasing volumes. For retailers and distributors, this seasonality creates inventory management challenges and reliance on peak-season sales performance to achieve annual revenue targets, adding operational complexity across the value chain.

Opportunity - Rapid Expansion of E-Commerce and Direct-to-Consumer Channels Broadening Global Market Accessibility

The rapid growth of e-commerce and direct-to-consumer (DTC) channels presents a transformative opportunity for tennis equipment manufacturers to expand market reach and improve margins. Online penetration in sporting goods has increased significantly, with the National Sporting Goods Association (NSGA) reporting consistent year-over-year online sales growth since 2019. Leading brands such as Wilson, Babolat, and Head N.V. are investing in proprietary digital storefronts, subscription-based accessory services, and data-driven personalized product recommendations.

By reducing dependence on traditional brick-and-mortar retailers, brands can strengthen direct customer relationships and capture higher profit margins. Importantly, digital channels allow companies to access consumers in tier-2 and tier-3 cities across India, Southeast Asia, and Brazil, where specialty sports retail infrastructure remains limited. This shift toward digital commerce is expected to create substantial incremental demand opportunities through 2033.

Institutional Procurement Growth from Academies, Schools, and Clubs Supporting Stable Bulk Equipment Demand

The expansion of tennis academies, school programs, and organized sports clubs is creating a rapidly growing institutional procurement channel for equipment manufacturers. The International Tennis Federation supports structured junior development programs in more than 100 countries, generating consistent demand for racquets, balls, coaching machines, and court accessories. In India, the All India Tennis Association (AITA) has collaborated with state governments to integrate tennis into school sports curricula, driving new institutional purchases across educational institutions.

Elite academies in Spain, the United States, and Australia continue to produce professional-level talent, sustaining premium equipment procurement annually. High-value products such as advanced ball machines, including those manufactured by Nanjing Spark Shot Technology Co., Ltd., represent an important revenue category, as academies often purchase multiple units for structured training programs and player development initiatives.

Category-wise Analysis

Product Type Insights

The tennis racquets segment holds the largest share of the global tennis equipment market, accounting for approximately 33% of total revenue. Racquets are the most essential piece of equipment required for play at all skill levels, ensuring consistent demand across beginners, recreational players, and professionals. According to the International Tennis Federation, racquet performance and technology are central to the sport’s value proposition.

Players typically replace racquets every 12 to 24 months due to performance evolution and ongoing innovation cycles. Premium product lines from Wilson Sporting Goods, Babolat, and Head N.V. command high average selling prices and strong brand loyalty. Continuous innovation, such as advanced composite frame construction, optimized string patterns, and customizable grip options, maintains high consumer engagement. This steady product refresh cycle encourages repeat purchases and reinforces the racquet segment’s dominant market position globally.

Material Analysis

The composites segment leads by material type, representing approximately 62% of total share. Composite materials, including carbon fiber, graphite, and fiberglass blends, are widely used in premium and mid-range racquets due to their superior strength-to-weight ratio and vibration control properties. Technical standards supported by the International Tennis Federation highlight the performance benefits of modern composite frames, which typically weigh below 300 grams while maintaining structural rigidity.

Major manufacturers such as Head N.V., Wilson Sporting Goods, and Yonex Co. Ltd. continue investing in proprietary composite technologies to differentiate performance. Yonex’s Isometric frame geometry, for example, enhances sweet spot optimization. Ongoing advancements in composite engineering further widen the performance gap compared to traditional metallic alternatives, ensuring the segment’s continued leadership throughout the forecast period.

End-user Insights

Individual segment dominates the tennis equipment market by end use, accounting for approximately 71% of total share. Recreational and competitive players represent the largest consumer base globally, ranging from casual participants to serious amateurs. The International Tennis Federation estimates over 87 million players worldwide, highlighting the scale of this segment. Individual consumers purchase racquets, balls, apparel, footwear, and accessories, with buying decisions strongly influenced by professional endorsements and digital content.

The growing popularity of personalized equipment, such as customized string tension, grip preferences, and racquet weight specifications, has deepened engagement with premium brands. This trend encourages higher transaction values and repeat purchases, particularly among frequent players. As tennis participation expands, the Individuals segment is expected to remain the primary revenue contributor to the global market.

Regional Insights

North America Tennis Equipment Market Trends

North America is the largest revenue-generating region in the global tennis equipment market, led by the United States. The Tennis Industry Association reported that approximately 21.6 million Americans played tennis in 2020, reflecting a 22% increase compared to previous years. Strong participation growth during and after the pandemic significantly boosted equipment sales.

The United States Tennis Association (USTA) invests more than US$300 million annually in grassroots and junior development programs, ensuring a steady pipeline of new players. North American consumers typically demonstrate strong brand loyalty and preference for premium products, supporting high average selling prices. Leading brands such as Wilson Sporting Goods and Babolat maintain strong retail penetration and endorsement visibility, reinforcing sustained regional demand and revenue stability.

Europe Tennis Equipment Market Trends

Europe represents the second-largest regional market, supported by deep tournament heritage and extensive club infrastructure. France, Spain, Germany, and the United Kingdom account for a significant portion of regional revenue. The French Open enhances France’s global visibility, while the Fédération Française de Tennis oversees over one million licensed players.

Germany’s Deutscher Tennis Bund and the United Kingdom’s Lawn Tennis Association manage strong development networks. Regulatory harmonization across the European Union simplifies product launches for brands such as Head N.V., Dunlop Sports Co. Ltd., and Tecnifibre. Increasing sustainability regulations are encouraging innovation in recyclable materials and environmentally friendly packaging across the region.

Asia Pacific Tennis Equipment Market Trends

Asia Pacific is the fastest-growing regional market, driven by China, Japan, India, and ASEAN economies. Government-backed sports promotion initiatives in China have significantly increased participation, with an estimated 15 million players nationwide. The resumption of major Women's Tennis Association events in China has strengthened consumer engagement and sponsorship activity. Japan remains a mature market, supported by strong domestic brand presence from Yonex Co. Ltd.

In India, development programs led by the All India Tennis Association are expanding grassroots participation. Manufacturing advantages in China and South Korea provide regional cost competitiveness. Emerging ASEAN markets such as Thailand, Indonesia, and Malaysia are witnessing rising urban participation, creating meaningful long-term growth opportunities through 2033.

Competitive Landscape

The global tennis equipment market demonstrates a moderately consolidated structure led by established multinational brands such as Wilson Sporting Goods, Head N.V., Babolat, and Yonex Co. Ltd. These companies command strong market share through brand equity, athlete endorsements, and extensive global distribution networks. Competitive differentiation is driven by continuous innovation in composite engineering, proprietary string technologies, and performance-focused product design validated by professional athletes.

At the same time, numerous regional manufacturers serve price-sensitive and niche segments, increasing competitive intensity. The expansion of digital DTC strategies, sustainability-focused product development, and athlete collaborations is reshaping competitive dynamics. Leading brands continue investing in innovation and consumer engagement initiatives to maintain premium positioning while capturing new growth opportunities across emerging and developed markets alike.

Key Developments:

- In January 2025, Wilson Sporting Goods introduced the Blade v9 racquet series featuring upgraded carbon fiber layup technology co-developed with professional tour athletes. The launch strengthens Wilson’s premium positioning, enhances frame stability and feel, and reinforces its innovation-led strategy across competitive global retail markets.

- In March 2024, Babolat expanded its direct-to-consumer e-commerce platform into 12 additional markets across Asia and Latin America. This strategic move improves digital accessibility, strengthens customer engagement, and targets fast-growing recreational tennis communities in emerging high-potential regions.

- In September 2023, Head N.V. refreshed its Radical and Prestige racquet lines with enhanced Auxetic material technology for improved responsiveness and stability. The upgrade targets premium players seeking tournament-validated performance enhancements within Head’s established high-performance product portfolio.

Companies Covered in Tennis Equipment Market

- Amer Sports Corporation

- Head N.V.

- Dunlop Sports Co. Ltd.

- Tecnifibre

- Oliver Sports & Squash GmbH

- Harrow Sports Inc.

- Babolat

- Yonex Co. Ltd.

- Prince Global Sports LLC

- Wilson Sporting Goods

- Nanjing Spark Shot Technology Co., Ltd.

- VINEX TECHNOLOGIES

- Volkl Tennis

- DONIC

Frequently Asked Questions

The global Tennis Equipment market is valued at US$ 2.3 Billion in 2026 and is projected to reach US$ 2.8 Billion by 2033, growing at a CAGR of 2.8% during the forecast period. Historical growth between 2020 and 2025 was recorded at a CAGR of 2.1%, reflecting steady expansion supported by rising global participation and increasing consumer health consciousness.

The primary growth drivers are rising global tennis participation-with the International Tennis Federation (ITF) reporting over 87 million players worldwide-combined with the powerful consumer influence of professional tournaments such as the Grand Slam events and elite athlete endorsement ecosystems. Post-pandemic outdoor sports participation growth and expanding grassroots programs by organizations like the USTA and AITA further support sustained market demand through 2033.

The Tennis Racquets segment is the leading product type, holding approximately 33% market share. Its dominance is driven by the racquet's status as the single indispensable piece of tennis equipment, consistent 12-to-24-month replacement cycles among active players, continuous innovation in composite frame technologies, and strong athlete endorsement programs from brands including Wilson Sporting Goods, Babolat, and Head N.V. sustaining high average selling prices.

North America, led by the United States, is the dominant regional market. With an estimated 21.6 million American tennis players and a robust infrastructure supported by the United States Tennis Association (USTA)'s annual investment of over US$ 300 million in grassroots development, the region generates the highest per-capita equipment spending globally, sustained by strong consumer brand loyalty and a vibrant professional tournament ecosystem.

The most significant growth opportunity lies in expanding institutional procurement channels-including tennis academies, school programs, and sports clubs-globally. The ITF's active development programs across more than 100 countries and government-backed school tennis initiatives by associations such as the All India Tennis Association (AITA) are generating fast-growing, high-volume institutional demand for racquets, ball machines, and bulk accessories through 2033.

The leading companies in the global Tennis Equipment market include Wilson Sporting Goods, Head N.V., Babolat, Yonex Co. Ltd., Dunlop Sports Co. Ltd., Tecnifibre, Amer Sports Corporation, Prince Global Sports LLC, Volkl Tennis, Nanjing Spark Shot Technology Co., Ltd., Nike, Inc., and Adidas AG, among other regional and specialized manufacturers competing across product, material, and end-use segments worldwide.