- Pharmaceuticals

- Tapentadol Market

Tapentadol Market Size, Share, and Growth Forecast 2026 - 2033

Tapentadol Market by Product Type (Branded, Generic), Dosage Form (Injectable, Oral Solution, Tablets), End-user (Clinics, Hospitals, Home Care), and Regional Analysis, 2026 - 2033

Tapentadol Market Size and Trends Analysis

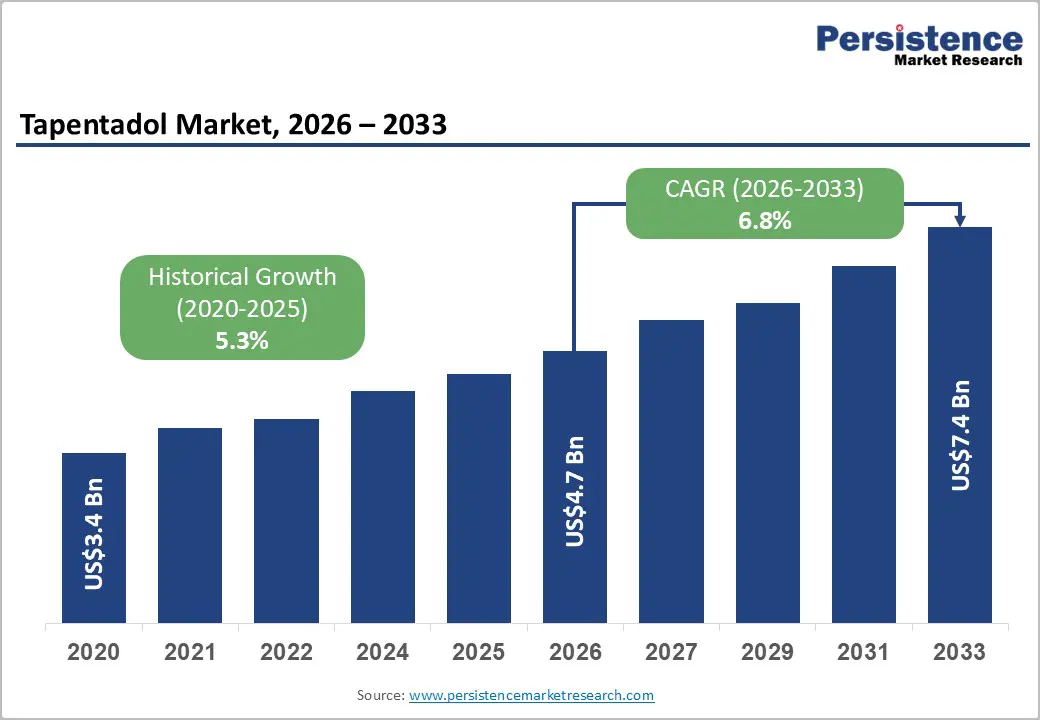

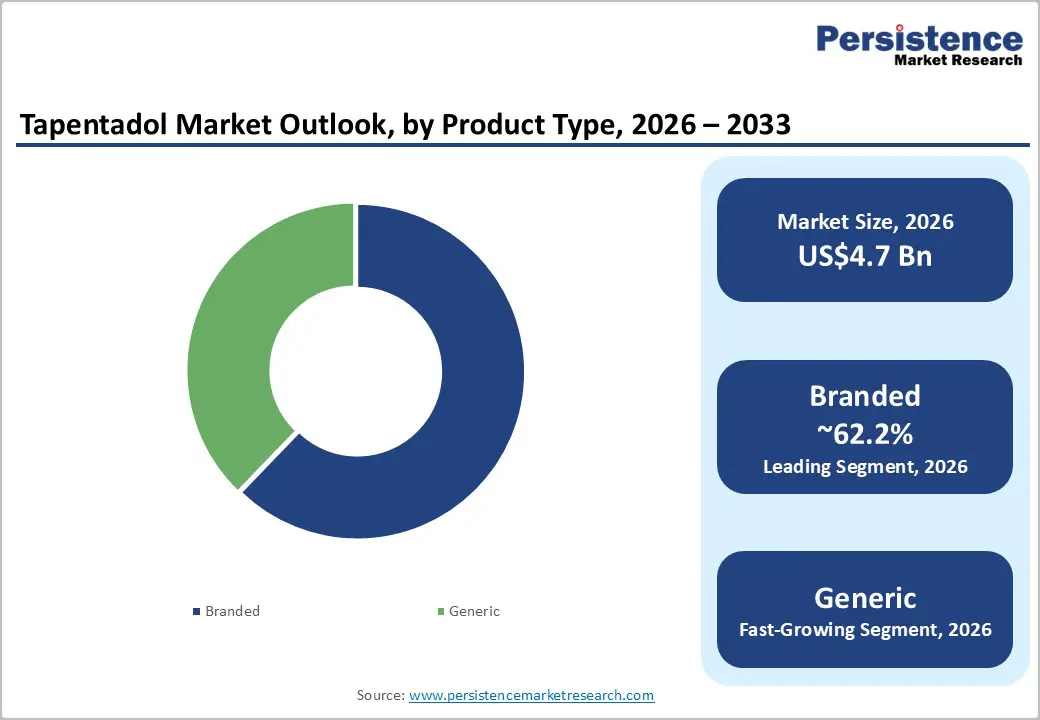

The global tapentadol market size is likely to be valued at US$4.7 billion in 2026 and is expected to reach US$7.4 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by rising prevalence of chronic pain conditions such as diabetic neuropathy, cancer-related pain, and musculoskeletal disorders.

Growth is further supported by increasing preference for dual-action analgesics such as tapentadol, which provide effective pain relief with a comparatively improved tolerability profile versus traditional opioids.

Key Industry Highlights:

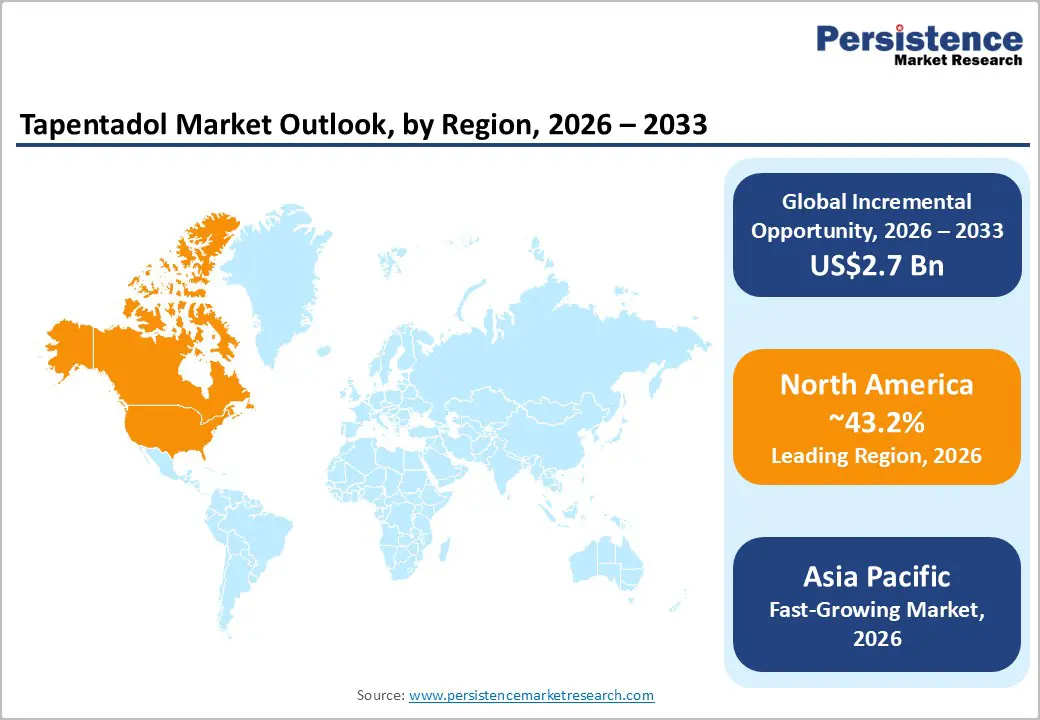

- Leading Region: North America, with about a 43.2% share in 2026, due to its high prevalence of chronic pain disorders.

- Fast-growing Region: Asia Pacific, backed by rising healthcare spending and increasing surgical procedures.

- Latest Drug: In March 2026, Hikma Pharmaceuticals PLC launched an authorized generic version of Nucynta ER (tapentadol) extended-release for U.S. patients, marking the first available generic of this product in the country. The launch followed Hikma's February 2026 introduction of the authorized generic of Nucynta immediate-release.

- Leading Product Type: Branded, approximately 62.2% share in 2026, owing to patent protections and delayed generic entry for key extended-release formulations.

- Dominant Dosage Form: Tablets, nearly 82.4% in 2026, as they are available in both immediate-release and extended-release forms.

DRO Analysis

Driver - Rising Geriatric Population and Persistent Pain Conditions

According to the Centers for Disease Control and Prevention’s (CDC) National Health Interview Survey (2023), chronic pain rates increase sharply with age, from just 12.3% among adults aged 18 to 29 to 36% among those aged 65 and older. This age-linked surge in pain burden creates high demand for targeted therapies. Tapentadol has emerged as a well-suited option for this demographic. A sub-group analysis published in Pain Research and Management studied 752 elderly patients (above 65 years) with chronic osteoarthritis on tapentadol prolonged release (PR).

Mean baseline pain scores dropped by 3.8 points, while sleep quality and independence also improved significantly. By the end of the 3-month observation, 68% of elderly patients achieved at least a 50% reduction in pain, and only 8.4% reported adverse drug reactions, mainly nausea (2.7%) and dizziness (1.5%). These outcomes make tapentadol a key treatment choice as the global elderly population continues to rise.

Cleaner Side Effect Profile Compared to Conventional Opioids

Tapentadol's dual mechanism, combining mu-opioid receptor (MOR) agonism with norepinephrine reuptake inhibition (NRI), reduces dependence on pure opioid activity, which lowers the burden of typical opioid-related side effects. In a key comparative study, patients on oxycodone CR had a treatment discontinuation rate of 55.4%, mainly due to gastrointestinal issues. In contrast, the tapentadol group's discontinuation rate (36.8%) was nearly on par with placebo (35.0%).

A head-to-head trial also found that nausea and vomiting incidences were significantly lower with tapentadol IR 50 mg and 75 mg versus oxycodone HCl IR 10 mg over 14 days (P<0.001). A 2024 systematic review published in JCA Advances further confirmed that tapentadol led to fewer treatment-emergent adverse events than oxycodone following orthopedic surgery, supporting its profile as a safer pain management alternative.

Restraint - Regulatory Hurdles as a Tightly Controlled Substance

Tapentadol's classification as a Schedule II controlled substance under the U.S. Controlled Substances Act (CSA) places it in the same regulatory tier as morphine and oxycodone, creating notable access barriers. The Drug Enforcement Administration (DEA) determined that tapentadol has a high potential for abuse and that its abuse may lead to severe psychological or physical dependence, citing its substantial pharmacological overlap with other Schedule II opioids.

The FDA's official labeling for NUCYNTA ER further warns that addiction can occur at recommended doses, even when the drug is prescribed appropriately, with extended-release formulations posing a high risk due to the large amount of tapentadol present. Owing this classification, tapentadol is governed by strict laws on who can prescribe it and how it may be dispensed, with the standard risks of opiate addiction, diversion, and misuse all applying. These restrictions limit prescription volumes, complicate pharmacy stocking, and deter adoption in markets with rigid opioid control policies.

Opportunity - Orally Disintegrating Tablet Formulations to Improve Accessibility

Reformulating tapentadol into fast-dissolving tablet (FDT) formats opens the drug to patient groups who struggle with conventional oral dosing. Dysphagia affects 15 to 22% of the general population globally, and this rises significantly to 35 to 40% among geriatric patients and up to 60% among institutionalized individuals, precisely the groups most likely to require tapentadol for chronic pain management.

Researchers at Bentham Science developed and optimized tapentadol FDTs using super disintegrants, specifically croscarmellose sodium and crospovidone. The TH5 formulation achieved rapid disintegration and optimal drug release, with stability confirmed under ICH conditions. These formulations dissolve within seconds in the oral cavity, eliminating the need for water or chewing. This development hence improves compliance in elderly and post-surgical patients, extending tapentadol's practical use.

Extended-Release (ER) Formulation as a Sustained-Action Alternative

The ER formulation of tapentadol provides a distinct advantage for patients requiring round-the-clock pain relief. Canada's Canadian Agency for Drugs and Technologies in Health (CADTH) recognizes tapentadol ER as indicated for pain severe enough to require daily, continuous, long-term opioid treatment where alternative options are inadequate, with a recommended dosage of 100 to 250 mg orally twice daily.

A Phase III open-label extension trial found that pain relief and quality-of-life improvements were sustained throughout up to 2 years of tapentadol ER treatment in patients with chronic osteoarthritis or low back pain. Evidence also shows tapentadol ER to be non-inferior to oxycodone for severe chronic low back pain and osteoarthritis pain, with potentially better gastrointestinal tolerability in clinical trials. This positions the ER formulation as a credible long-term alternative to traditional opioids across chronic pain conditions.

Category-wise Analysis

Product Type Insights

Branded tapentadol is predicted to lead with a share of approximately 62.2% in 2026, as physicians have relied on established brands such as Nucynta and Palexia for more than a decade. These products have extensive clinical evidence supporting their use in chronic pain, diabetic peripheral neuropathy, and severe acute pain. Several pain specialists are familiar with the efficacy, safety profile, and dosing flexibility of branded formulations, especially extended-release tablets. This long prescribing history has created strong physician confidence and patient loyalty.

Generic tapentadol is estimated to be the fastest-growing segment over the forecast period, as regulatory barriers are gradually disappearing. A key milestone occurred in January 2026 when the U.S. FDA approved the first generic tapentadol tablet from Humanwell Pharmaceutical and the first generic oral solution from Novitium Pharma. These approvals opened the door for broad competition and improved patient access.

Dosage Form Insights

Tablets are anticipated to dominate with a share of nearly 82.4% in 2026, as they are the primary formulation used for both acute and chronic pain treatment. Most patients receiving tapentadol are treated in outpatient settings rather than hospitals. Tablets are convenient, easy to transport, simple to store, and allow patients to self-administer medication without medical supervision.

The oral solution segment is expected to remain in the second position in 2026, as it addresses the needs of patients who cannot easily swallow tablets. This includes elderly patients, pediatric patients, individuals with neurological disorders, and patients recovering from surgery. For these groups, liquid formulations improve treatment compliance and dosing accuracy.

Regional Insights

North America Tapentadol Market Trends

North America is predicted to dominate in 2026 with a share of approximately 43.2% as it has one of the world's most developed pain-management hubs. Hospitals, pain clinics, orthopedic centers, and cancer care facilities routinely use advanced analgesics for post-surgical and chronic pain treatment. Tapentadol has gained acceptance as it combines opioid receptor activity with norepinephrine reuptake inhibition, delivering effective pain relief with a comparatively lower burden of some opioid-related side effects. Academic institutions such as the University of California, San Francisco continue to showcase its dual mechanism and use in neuropathic and chronic pain management.

U.S. Tapentadol Market Trends

A share of nearly 60.6% is expected to be held by the U.S. in 2026. The country has a well-established prescribing framework for severe acute pain, chronic pain, and diabetic peripheral neuropathy. However, the market is undergoing a transition from branded products toward generic competition. A key development occurred in January 2026 when the Food and Drug Administration (FDA) approved the first generic tapentadol hydrochloride tablets and oral solution. This is predicted to improve accessibility and intensify competition. The FDA specifically listed tapentadol among its first generic approvals of 2026.

Asia Pacific Tapentadol Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 29.7%, as healthcare systems are improving access to pain management therapies. Rising numbers of orthopedic surgeries, cancer treatments, trauma cases, and diabetes-related complications are raising the demand for effective analgesics. Several countries are also investing heavily in hospital infrastructure and specialist care. The region benefits from a large pharmaceutical manufacturing base.

India, China, and several Southeast Asian countries have well-established generic drug industries that can produce pain medications at low costs. As awareness of chronic pain management improves, physicians are gradually moving beyond traditional analgesics and exploring new options such as tapentadol.

China Tapentadol Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 8.5%, owing to its rapidly aging population and increasing incidence of chronic diseases. Conditions such as diabetic neuropathy, osteoarthritis, lower back pain, and cancer-related pain are becoming more common. These trends are creating long-term demand for advanced pain therapies. The government continues to extend healthcare coverage and improve access to hospital services. Large tertiary hospitals are now adopting modern pain-management protocols.

At the same time, local pharmaceutical companies are strengthening their capabilities in specialty and generic medicines, which could improve the availability of tapentadol-based products over the next ten years.

India Tapentadol Market Trends

In 2026, India is projected to account for a share of approximately 6.2%. The country plays a dual role as both a large consumer market and an important manufacturing hub. Rising road accidents, cancer prevalence, orthopedic procedures, and diabetes cases are supporting demand for strong pain-management therapies. The country also hosts several manufacturers involved in producing tapentadol formulations for domestic and export markets. This manufacturing strength gives India a strategic position in the global supply chain.

However, regulatory scrutiny is increasing. In 2025, the country’s authorities took action against illegal exports involving tapentadol-containing products after international concerns regarding misuse and diversion. Such measures are expected to improve oversight and strengthen the legitimacy of approved manufacturers.

Europe Tapentadol Market Trends

Europe will likely see decent growth over the forecast period with a share of nearly 18.3% in 2026, as the region has well-established healthcare network and pain-management guidelines. Unlike rapidly expanding emerging markets, growth in the continent is augmented by consistent clinical adoption rather than sudden market expansion. Several physicians view tapentadol as a useful option for neuropathic pain and chronic musculoskeletal conditions. The region also has a large elderly population, creating sustained demand for pain therapies. Reimbursement systems in several countries support access to advanced prescription analgesics.

Germany Tapentadol Market Trends

Germany will likely register a substantial share of approximately 10.6% in 2026. The country has a sophisticated pain-management framework and a high level of physician awareness regarding multimodal pain treatment. Germany also serves as the home market for Grünenthal GmbH, which continues to invest heavily in pain-management research and commercialization. The company's long-standing presence helps maintain strong clinical familiarity with tapentadol among healthcare professionals.

The country's aging population is another important factor. Rising cases of arthritis, spinal disorders, cancer-related pain, and neuropathic conditions are projected to support continued demand. Growth is likely to remain steady rather than explosive as Germany is already a mature market with high treatment penetration.

U.K. Tapentadol Market Trends

A share of around 5.2% is predicted to be held by the U.K. in 2026, as it maintains strict opioid prescribing practices due to concerns about dependence and misuse. Tapentadol is generally prescribed for carefully selected patients rather than broad use. However, demand continues to be supported by increasing numbers of elderly patients and rising awareness of chronic pain management. Hospitals and specialist pain clinics are focusing more on individualized treatment approaches, where tapentadol can be considered when conventional therapies are insufficient.

The National Health Service's (NHS) emphasis on evidence-based prescribing means that products demonstrating clear clinical value continue to find a place in treatment pathways. This is supporting stable demand, mainly in neuropathic pain and severe chronic pain settings.

Competitive Landscape

The global tapentadol market is moderately consolidated with a handful of branded and licensed manufacturers controlling a significant share. Regional generic companies are steadily increasing competition as patent barriers weaken. The market has historically been dominated by the original developer, Grünenthal GmbH, and its commercialization partners, mainly Janssen Pharmaceuticals, which marketed branded products such as Nucynta and Palexia across multiple regions. Their long-standing physician relationships and established pain-management portfolios have helped maintain a superior market presence.

A key competitive trend is the gradual shift from branded products toward generic tapentadol formulations. Following regulatory approvals for generic versions in several markets, companies such as Lupin Limited, Ipca Laboratories, Cadila Pharmaceuticals, and other regional manufacturers have strengthened their positions by delivering cost-competitive alternatives, especially in Asia Pacific, Latin America, and parts of Europe. This is increasing pricing pressure on branded suppliers while broadening patient access.

Key Industry Developments:

- In January 2026, the U.S. FDA approved the first generic tapentadol oral solution from Novitium Pharma LLC. The product serves as a generic alternative to Nucynta oral solution. The approval marked a significant expansion of generic tapentadol availability beyond tablet formulations and strengthened the transition toward a more competitive market environment.

- In January 2026, the U.S. FDA approved the first generic tapentadol hydrochloride tablet developed by Humanwell Pharmaceutical US, Inc. The approval covers the generic version of Nucynta and is intended for the management of severe acute pain in adults and eligible pediatric patients. The approval is predicted to increase competition in the U.S. opioid analgesics market and improve patient access to low-cost tapentadol products.

- In March 2025, Grünenthal continued strengthening its U.S. pain-management business following its acquisition of Valinor Pharma. The company stated that the transaction expanded its presence in the U.S. pain therapeutics market and improved its commercial capabilities.

Companies Covered in Tapentadol Market

- Alembic Pharmaceuticals Limited

- Alkem Laboratories Ltd.

- Amneal Pharmaceuticals, Inc.

- Arbor Pharmaceuticals, LLC.

- Aurobindo Pharma Ltd.

- Cadila Pharmaceuticals Ltd.

- Glenmark Pharmaceuticals Ltd.

- Hikma Pharmaceuticals PLC

- Janssen Pharmaceuticals, Inc.

- Lupin Limited

- Macleods Pharmaceuticals Ltd.

- Mylan N.V.

- Novartis AG

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Torrent Pharmaceuticals Ltd.

- Wockhardt Ltd.

- Zydus Lifesciences Ltd.

Frequently Asked Questions

The global tapentadol market is projected to be valued at US$4.7 billion in 2026.

The tapentadol market is expected to reach US$7.4 billion by 2033.

Key market trends include rising generic approvals and increasing use of extended-release formulations.

Branded tapentadol is expected to be the leading solution with a share of nearly 62.2% in 2026, as established brands such as Nucynta and Palexia have strong physician trust.

The tapentadol market is expected to grow at a CAGR of 6.8% from 2026 to 2033.

Alembic Pharmaceuticals Limited, Alkem Laboratories Ltd., and Amneal Pharmaceuticals, Inc. are a few key market players.