- Pharmaceuticals

- Lichen Sclerosus Treatment Market

Lichen Sclerosus Treatment Market Size, Share and Growth Forecast, 2026-2033

Lichen Sclerosus Treatment Market by Product Form (Creams, Solutions, Tablets), Mode of Administration (Topical, Oral, Injection, Others), Distribution Channel (Hospital Pharmacies, Clinics, Retail Pharmacies, Others), and Regional Analysis for 2026-2033

Lichen Sclerosus Treatment Market Size and Trends Analysis

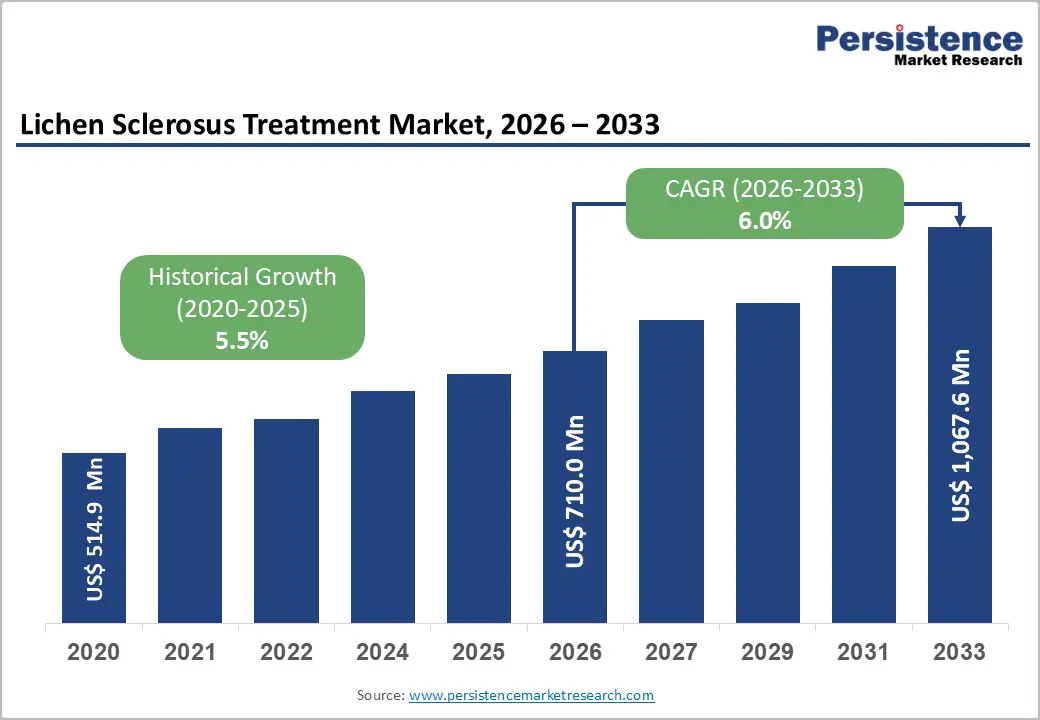

The global lichen sclerosus treatment market size is likely to be valued at US$710.0 million in 2026 and is projected to reach US$1,067.6 million by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by increasing diagnosis of chronic inflammatory skin disorders and growing awareness of vulvar health conditions.

Clinical guidelines from major dermatology associations continue to recommend high-potency topical corticosteroids as the first-line treatment for lichen sclerosus, supporting consistent treatment demand. Improved access to specialist dermatology and gynecology services, rising healthcare expenditure, and the growing adoption of telehealth platforms are further enhancing diagnosis rates and long-term disease management, contributing to sustained market growth globally.

Key Industry Highlights:

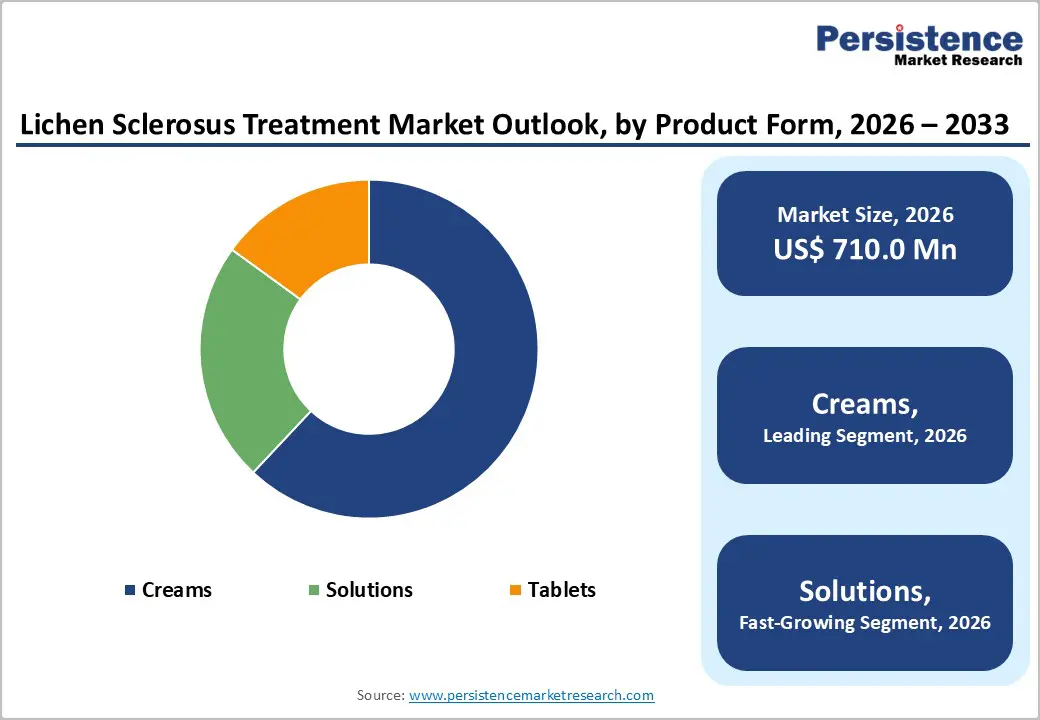

- Dominant Product Form: Creams are expected to lead with approximately 62% of the market share in 2026, while solutions are projected to be the fastest-growing product form at around 6.7% CAGR through 2033.

- Leading Mode of Administration: Topical administration is anticipated to dominate with nearly a 71% share in 2026, while injection therapies are expected to register the fastest growth during 2026–2033, supported by advances in biologic and regenerative treatments.

- Key Distribution Channel: Hospital pharmacies are likely to account for the largest share in 2026, while online pharmacies are projected to be the fastest-growing channel through 2033, driven by telehealth expansion and e-pharmacy adoption.

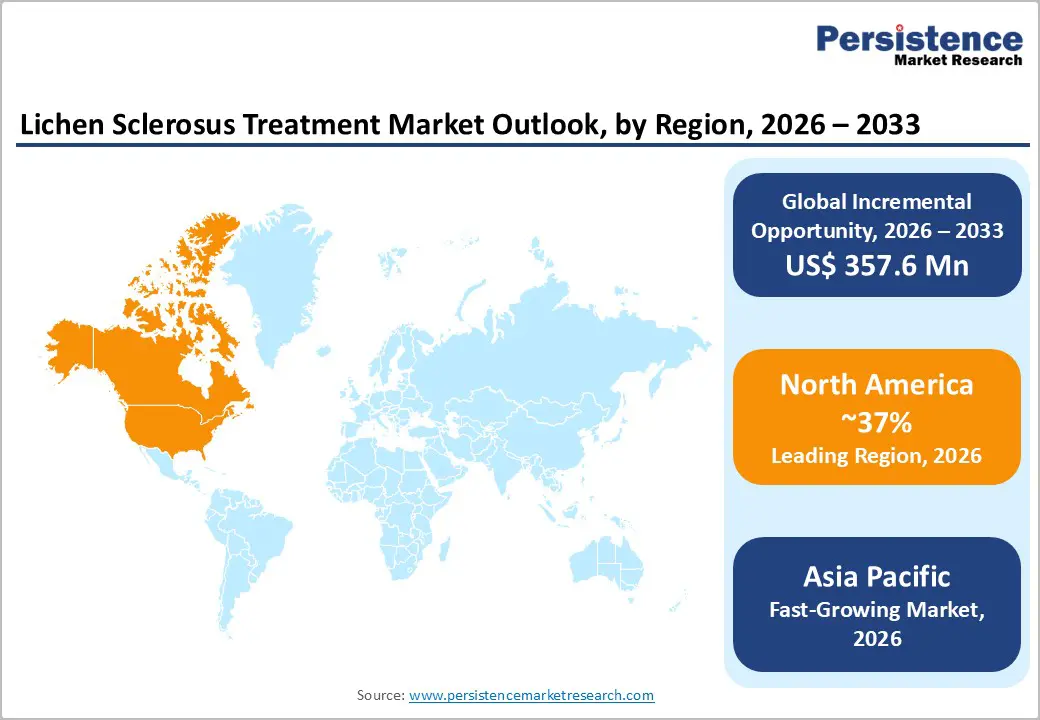

- Regional Leadership: North America is poised to lead with an estimated 37% share in 2026, while Asia Pacific is expected to record the fastest growth through 2033, supported by healthcare infrastructure development and increasing disease awareness.

- Competitive Environment: Competitive activity is centered on women's health initiatives, specialty dermatology innovation, inflammatory disease research, and expanded treatment accessibility through strategic partnerships and digital healthcare platforms.

DRO Analysis

Driver - Growing Prevalence of Chronic Dermatological and Autoimmune Disorders Driving Treatment Demand

The increasing burden of autoimmune and inflammatory skin diseases is a primary growth driver for the lichen sclerosus treatment market. According to the National Organization for Rare Disorders (NORD) and the National Institutes of Health (NIH), lichen sclerosus primarily affects women, particularly postmenopausal women, although it can occur across all age groups. Studies published by the British Association of Dermatologists indicate that prevalence rates are higher than previously recognized due to improved diagnosis and awareness.

The World Health Organization (WHO) reports that skin diseases affect nearly 1.8 billion people globally at any given time, increasing demand for specialized dermatological therapies. As healthcare systems emphasize earlier diagnosis and chronic disease management, prescription volumes for topical corticosteroids, immunomodulators, and supportive therapies continue to rise, supporting long-term market expansion and improving treatment accessibility.

Restraint - Underdiagnosis and Delayed Clinical Intervention Limiting Market Penetration

Despite increasing awareness, underdiagnosis remains a significant barrier to market growth. Clinical studies published through the National Center for Biotechnology Information (NCBI) indicate that many patients experience symptoms for years before receiving a confirmed diagnosis. Misdiagnosis with other dermatological or gynecological conditions often delays treatment initiation and disease management.

Healthcare access disparities in developing economies also restrict consultation with specialists such as dermatologists and gynecologists. The WHO continues to highlight shortages of specialized healthcare professionals across several emerging markets. Delayed diagnosis can result in disease progression, scarring, and higher treatment complexity, increasing healthcare costs while limiting early pharmaceutical intervention opportunities. These structural challenges reduce treatment uptake rates and create barriers to consistent market penetration, particularly in low-resource healthcare systems.

Opportunity - Expansion of Specialized Women's Health and Dermatology Services Creating New Growth Opportunities

Significant opportunities are emerging from expanding women's health programs and specialized dermatology services worldwide. Healthcare authorities across North America, Europe, and Asia Pacific are investing in preventive gynecological care and chronic disease management programs. According to the International Federation of Gynecology and Obstetrics (FIGO), increased screening and patient education initiatives are improving recognition of vulvar disorders. Growing teledermatology adoption is also expanding specialist access in underserved regions.

The opportunity is particularly strong in Asia Pacific, where healthcare infrastructure investments and rising awareness are accelerating diagnosis rates. Pharmaceutical manufacturers are increasingly focusing on improved formulations, combination therapies, and patient-friendly delivery systems. As healthcare providers prioritize quality-of-life outcomes and long-term disease management, demand for advanced lichen sclerosus treatment products is expected to create substantial commercial opportunities through 2033.

Category-wise Analysis

Product Form Insights

Creams are expected to hold approximately 62% of the market share in 2026, maintaining their position as the preferred treatment option. Their dominance is supported by recommendations from the British Association of Dermatologists and other clinical bodies, which identify high-potency topical corticosteroid creams as the standard first-line therapy. Patient preference also favors creams due to ease of self-application, rapid symptom relief, and the ability to manage itching and discomfort without requiring clinical intervention.

Solutions are projected to expand at a 6.7% CAGR during 2026–2033, making them the fastest-growing product form. Demand is increasing as patients seek formulations that offer improved absorption, less residue, and easier application in sensitive anatomical areas. Ongoing innovation in dermatology drug delivery systems and growing interest in personalized treatment approaches are further supporting adoption, particularly among patients requiring long-term disease management.

Mode of Administration Insights

Topical administration is anticipated to account for nearly 71% of the market in 2026, driven by strong physician and patient preference. Clinical studies consistently demonstrate that most patients achieve symptom control through topical corticosteroid therapy, reducing the need for systemic treatments. The convenience of home-based application, lower risk of systemic adverse effects, and established long-term safety profile continue to make topical therapies the cornerstone of lichen sclerosus management.

Injection therapies are expected to register the fastest growth at a 7.1% CAGR through 2033. Growth is being fueled by increasing exploration of regenerative treatments such as platelet-rich plasma (PRP) and biologic-based approaches for patients who experience recurrent or treatment-resistant disease. Rising patient demand for therapies that may improve tissue regeneration and quality-of-life outcomes is encouraging specialist clinics to expand injectable treatment offerings.

Distribution Channel Insights

Hospital pharmacies are projected to command approximately 38% of market revenue in 2026, reflecting the importance of specialist-led diagnosis and treatment. As lichen sclerosus is frequently underdiagnosed or misdiagnosed, many patients initially seek care through hospital-based dermatology and gynecology departments. Access to expert consultation and prescription management continues to make hospital pharmacies the preferred dispensing channel for newly diagnosed patients.

Online pharmacies are forecast to grow at an 8.0% CAGR from 2026 to 2033, supported by changing patient purchasing behavior. The widespread adoption of telemedicine and digital prescription services has increased consumer confidence in online medication procurement. Patients managing chronic conditions increasingly value home delivery, automatic refill options, and discreet access to treatments, making e-pharmacy platforms an attractive alternative to traditional retail channels.

Regional Analysis

North America Lichen Sclerosus Treatment Market Trends

North America is expected to account for approximately 37% of the global lichen sclerosus treatment market in 2026. The region benefits from higher diagnosis rates than most global markets, supported by active patient advocacy groups such as the National Vulvodynia Association (NVA) and growing awareness among gynecologists and dermatologists. Increasing recognition that lichen sclerosus is frequently underdiagnosed has encouraged earlier specialist referrals and long-term disease management programs.

U.S. Lichen Sclerosus Treatment Market Trends

The U.S. is expected to hold an estimated 84% share of the North America market in 2026. Patients predominantly prefer clobetasol propionate-based topical therapies, which remain the first-line treatment recommended by leading dermatology guidelines. Growing adoption of specialist vulvar clinics, including programs at institutions such as the Mayo Clinic and Cleveland Clinic, is improving diagnosis and treatment adherence, particularly among postmenopausal women who represent the largest patient population.

Canada Lichen Sclerosus Treatment Market Trends

Canada is expected to account for approximately 16% of the regional revenue share in 2026. The country is witnessing rising utilization of teledermatology and women's health services, helping reduce delays in diagnosis. Canadian patients continue to favor conservative long-term topical treatment approaches, while academic centers are increasingly participating in research focused on chronic vulvar disorders and quality-of-life outcomes.

Europe Lichen Sclerosus Treatment Market Trends

Europe is projected to capture approximately 31% of global market revenue share in 2026. Strong awareness among healthcare professionals is supported by guidance from the British Association of Dermatologists (BAD), which continues to recommend ultra-potent topical corticosteroids as the standard treatment pathway for lichen sclerosus. As a result, patient adherence to long-term maintenance therapy remains relatively high across major European markets.

Germany Lichen Sclerosus Treatment Market Trends

Germany is expected to account for nearly 28% of the Europe market share in 2026. The country benefits from extensive access to dermatologists and gynecologists, enabling earlier diagnosis compared with many regions globally. German patients increasingly seek treatment before irreversible scarring develops, reflecting broader awareness of the disease's long-term complications and quality-of-life impact.

U.K. Lichen Sclerosus Treatment Market Trends

The U.K. is estimated to represent approximately 18% of the regional revenue share in 2026. Adoption of BAD treatment guidelines through NHS clinical pathways has strengthened standardized disease management. Patient groups and educational campaigns have also improved recognition of symptoms such as chronic vulvar itching, helping reduce the historical problem of delayed diagnosis.

Asia Pacific Lichen Sclerosus Treatment Market Trends

Asia Pacific is anticipated to hold approximately 23% of the global market share in 2026 and remains the fastest-growing region. Unlike North America and Europe, market growth is driven largely by improving disease recognition. Historically, many patients remained undiagnosed due to limited awareness of vulvar health conditions and social stigma surrounding genital disorders, but this trend is gradually changing across major healthcare systems.

China Lichen Sclerosus Treatment Market Trends

China is projected to account for around 35% of the Asia Pacific market share in 2026. Growing investments in dermatology departments at major urban hospitals and increased women's health awareness are contributing to rising diagnosis rates. Patients continue to favor affordable topical therapies, although demand for advanced dermatological treatments is increasing among urban populations seeking improved long-term symptom control.

India Lichen Sclerosus Treatment Market Trends

India is expected to represent approximately 16% of regional revenue in 2026. Market growth is being driven by expanding gynecology services, digital health platforms, and awareness initiatives related to women's reproductive health. Many patients are diagnosed only after years of symptoms, creating substantial unmet treatment demand. The rapid expansion of teleconsultation platforms is helping connect patients with dermatology and gynecology specialists, particularly in underserved regions.

Competitive Landscape

The global lichen sclerosus treatment market is moderately fragmented, with leading companies such as Pfizer, AbbVie, Sanofi, Organon, and Viatris accounting for a substantial share of market revenue. These players leverage their established dermatology and immunology portfolios, strong physician networks, and extensive distribution capabilities. Continued investments in topical therapies, inflammatory disease research, and women's health initiatives help maintain their competitive positions.

Meanwhile, specialty dermatology companies such as LEO Pharma, Almirall, and Taro Pharmaceutical focus on niche treatment areas and regional market strengths. Regulatory requirements and limited disease-specific therapies create entry barriers, while growing interest in biologics and regenerative treatments is attracting new innovation. Market competition is expected to intensify through strategic partnerships, licensing agreements, and product portfolio expansion as companies seek to address unmet needs in chronic and recurrent lichen sclerosus management.

Key Industry Developments:

- In April 2026, Sun Pharmaceutical Industries announced the acquisition of Organon for approximately US$11.75 billion, significantly expanding its global women's health portfolio and strengthening its presence in chronic gynecological disease treatment markets.

Companies Covered in Lichen Sclerosus Treatment Market

- Pfizer Inc.

- AbbVie Inc.

- Sanofi S.A.

- Viatris Inc.

- Organon & Co.

- Bayer AG

- Novartis AG

- GlaxoSmithKline plc

- Eli Lilly and Company

- Bausch Health Companies Inc.

- Teva Pharmaceutical Industries Ltd.

- Perrigo Company plc

- Taro Pharmaceutical Industries Ltd.

- LEO Pharma A/S

- Almirall S.A.

Frequently Asked Questions

The global lichen sclerosus treatment market is projected to reach US$710.0 million in 2026.

Rising disease awareness, increasing diagnosis rates, and growing adoption of topical therapies drive market growth.

The lichen sclerosus treatment market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

Expanding women's health programs, telemedicine adoption, and the development of advanced dermatology therapies create significant growth opportunities.

Pfizer, AbbVie, Sanofi, Organon, Viatris, LEO Pharma, and Almirall are among the key market participants.