- Renewable Energy

- Solar Hybrid Inverter Market

Solar Hybrid Inverter Market Size, Share, and Growth Forecast, 2026 - 2033

Solar Hybrid Inverter Market by Product Type (Three-Phase Hybrid, Single-Phase Hybrid, Others), Application (Commercial, Residential, Others), Power Rating, and Regional Analysis for 2026 - 2033

Solar Hybrid Inverter Market Size and Trends Analysis

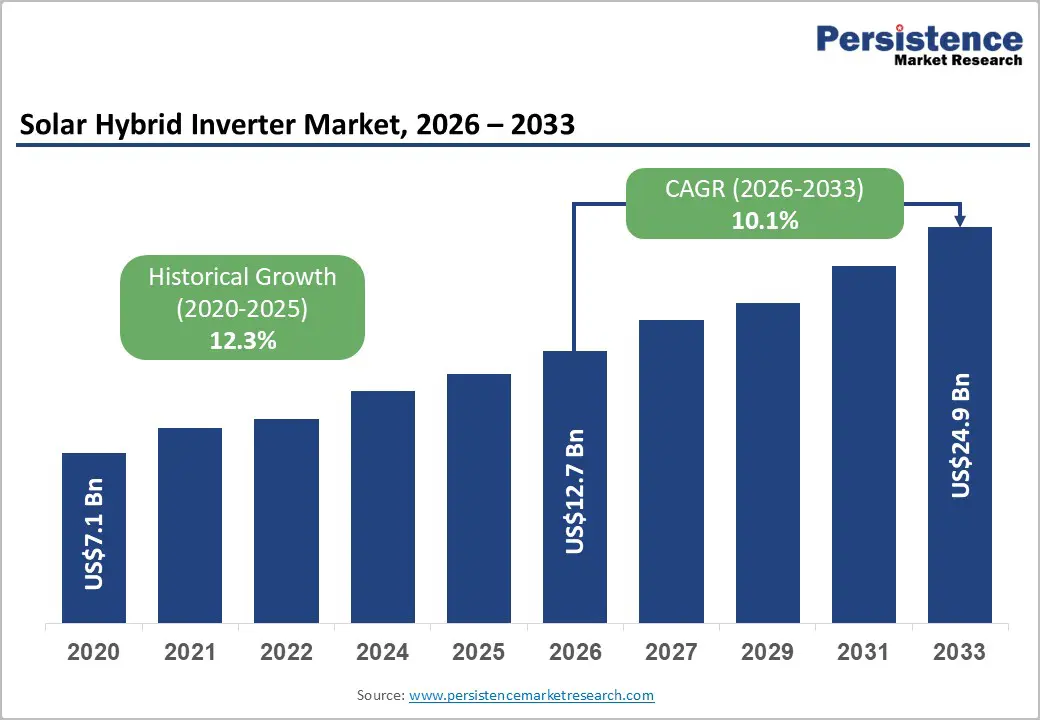

The global solar hybrid inverter market size is likely to be valued at US$12.7 billion in 2026 and is expected to reach US$24.9 billion by 2033, growing at a CAGR of 10.1% between 2026 and 2033, driven by the continuous rise in solar photovoltaic (PV) installations worldwide, increasing integration of battery storage systems into renewable energy networks, and stronger government initiatives promoting decentralized energy generation.

Rising deployment of rooftop solar installations, commercial energy storage systems, and backup power solutions is further driving demand for hybrid inverters. In addition, these systems are evolving into advanced energy management platforms that integrate solar panels, battery storage, electrical loads, and utility grid connections within a unified framework.

Key Industry Highlights:

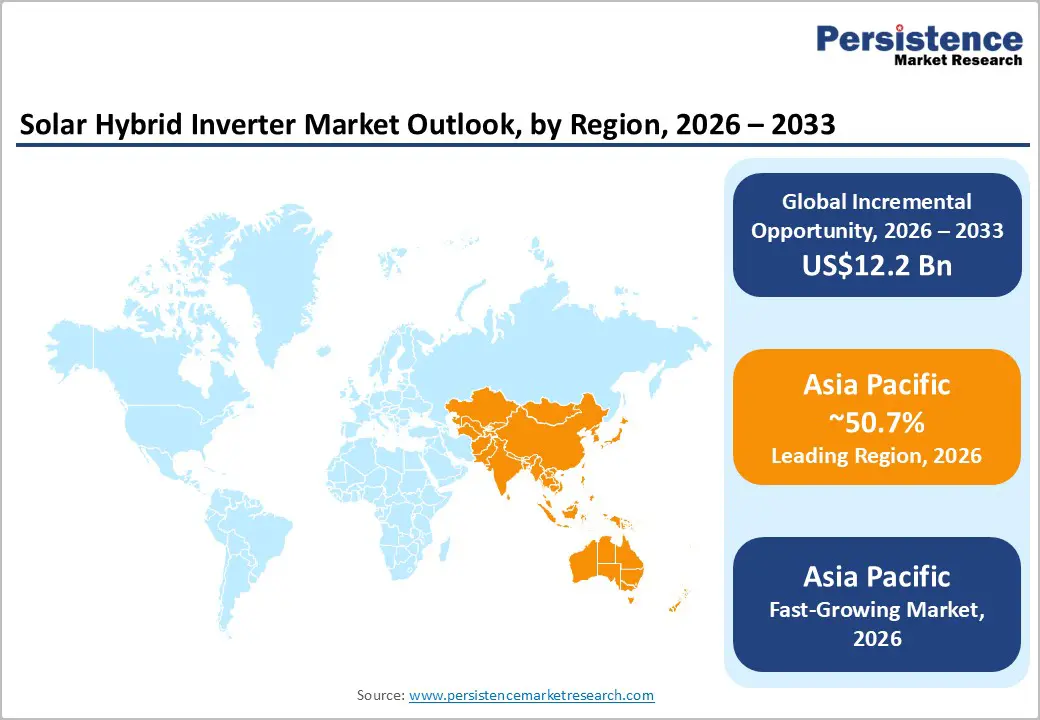

- Leading Region: Asia Pacific is anticipated to dominate the market, with approximately 50.7% market share in 2026, supported by large-scale solar deployment, robust manufacturing infrastructure, and rapid rooftop solar adoption in China and India.

- Fastest-growing Region: Asia Pacific is projected to remain the fastest-growing regional market, due to expanding distributed energy systems and rising investments in residential and commercial solar-plus-storage infrastructure.

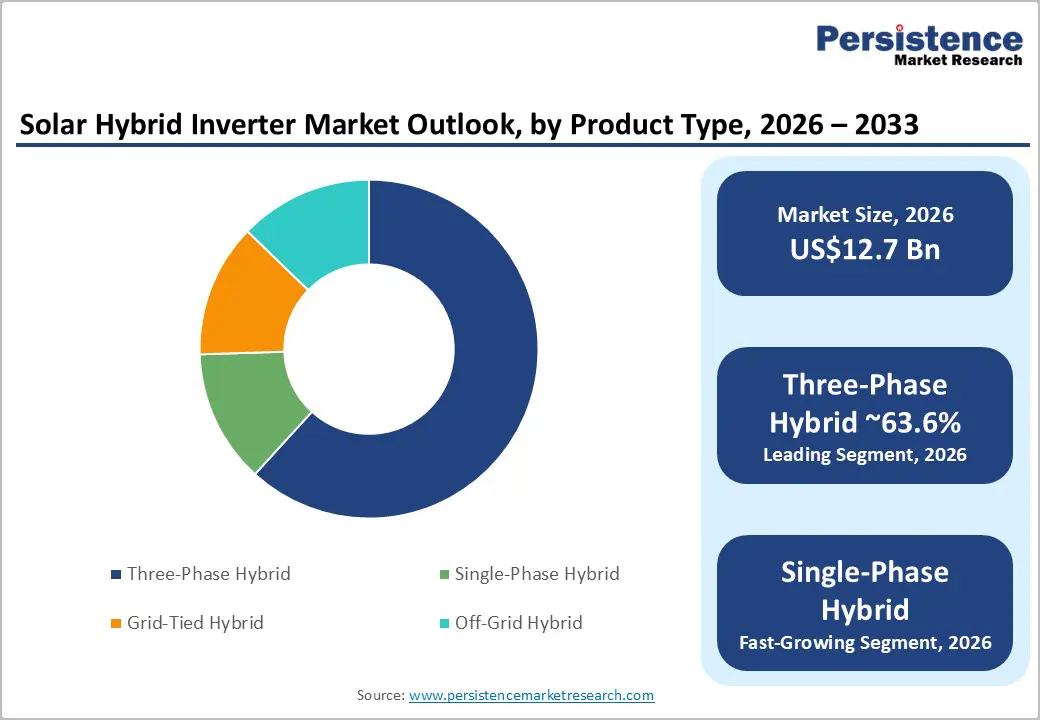

- Dominant Product Type: The three-phase hybrid segment is anticipated to lead with approximately 63.6% of market share in 2026, driven by strong adoption across commercial buildings, industrial facilities, and high-capacity energy storage applications.

- Leading Application: The commercial application segment is estimated to account for approximately 56.3% market share in 2026, supported by increasing demand for energy optimization, backup power management, and commercial solar-plus-storage deployments.

DRO Analysis

Drivers - Rooftop Solar Expansion and Solar-Plus-Storage Adoption are Accelerating Hybrid Inverter Demand

The rapid deployment of rooftop solar installations worldwide is significantly expanding the addressable market for solar hybrid inverters. Global solar PV capacity additions have continued to grow due to supportive government policies, falling photovoltaic costs, and rising demand for distributed renewable energy systems. Hybrid inverters are becoming a core component in these systems because they enable efficient coordination between solar generation, battery storage, and grid connectivity.

Residential and commercial users increasingly prefer integrated solar-plus-storage systems to improve energy reliability and reduce electricity expenses. Government-backed rooftop solar programs in India, Europe, Southeast Asia, and the U.S. are supporting the widespread installation of smaller hybrid systems for residential applications and higher-capacity systems for commercial facilities. Net-metering frameworks, feed-in tariff policies, and tax incentives are further strengthening market penetration. The transition toward decentralized power infrastructure is expected to sustain long-term demand for hybrid inverter technologies across both developed and emerging economies.

Grid Resilience Requirements are Driving Advanced Energy Management Capabilities

Power utilities and energy regulators are increasingly prioritizing grid stability and resilience as renewable energy penetration rises globally. Hybrid inverters are evolving from conventional power conversion devices into advanced energy management systems capable of handling battery charging, load balancing, grid synchronization, and backup power operations. The increasing integration of battery energy storage systems with renewable energy infrastructure is a major growth catalyst for the market.

Commercial facilities, industrial sites, and residential consumers are investing in hybrid systems to manage peak demand, improve power quality, and maintain operational continuity during outages. Smart grid modernization initiatives in North America and Europe are also encouraging the deployment of inverter-based energy systems with intelligent monitoring and automation features.

Technological advancements including AI-enabled monitoring, remote diagnostics, bidirectional energy flow management, and enhanced battery compatibility are improving product performance and expanding application scope. These innovations are expected to strengthen adoption of high-capacity three-phase hybrid systems in commercial and industrial environments.

Restraint - Supply Chain Concentration and Pricing Pressure are Affecting Profit Margins

The solar hybrid inverter market faces structural challenges, including supply chain concentration, intense pricing competition, and dependence on imported components. A substantial share of global solar equipment manufacturing remains concentrated in China, creating sourcing vulnerabilities for international suppliers and project developers. Declining prices across the solar value chain have improved affordability for end-users but have also increased pressure on inverter manufacturers to maintain profitability. Companies operating primarily as hardware suppliers face margin compression due to commoditization risks and aggressive pricing strategies from large-scale manufacturers.

The market also faces technical and regulatory challenges associated with product certification, grid compliance standards, and battery integration requirements. Variations in utility regulations and interconnection procedures across countries can increase deployment complexity and extend project timelines. Smaller manufacturers may struggle to maintain competitiveness without strong software ecosystems, robust after-sales service networks, or integrated energy management capabilities.

Opportunities - Residential Electrification Programs are Creating Large-Scale Growth Opportunities

Government-supported residential electrification initiatives and rooftop solar subsidy programs are creating significant growth opportunities for solar hybrid inverter manufacturers. Countries including India, China, Australia, and several European nations are promoting distributed solar generation to reduce pressure on centralized utility infrastructure and accelerate renewable energy adoption.

Residential consumers are increasingly investing in solar-plus-storage systems to reduce electricity costs, improve backup power availability, and enhance energy independence. Hybrid inverters are becoming a preferred solution because they allow households to optimize solar utilization while maintaining an uninterrupted power supply during outages.

The growing popularity of electric vehicles, smart homes, and battery storage systems is expected to further increase demand for integrated residential energy management solutions. Manufacturers are responding by developing compact, high-efficiency, and user-friendly hybrid inverter platforms with advanced monitoring capabilities and seamless battery compatibility.

Commercial Energy Storage Integration is Expanding Revenue Potential

Commercial and industrial organizations are increasingly deploying hybrid inverter systems to manage energy consumption, reduce peak electricity demand, and improve operational resilience. Rising electricity tariffs and growing emphasis on sustainability targets are encouraging businesses to adopt solar-plus-storage infrastructure.

Hybrid inverters are gaining importance in commercial buildings, warehouses, manufacturing facilities, educational institutions, and healthcare infrastructure, where an uninterrupted power supply is critical. These systems provide opportunities for demand response participation, energy arbitrage, and improved load management.

The integration of battery energy storage systems with commercial solar installations is expected to create substantial opportunities for higher-capacity hybrid inverter solutions. Market participants are also focusing on intelligent software platforms, predictive maintenance systems, and integrated monitoring tools to strengthen recurring revenue streams and improve customer retention.

Category-wise Analysis

Product Type Analysis

The three-phase hybrid segment accounts for the largest market share, estimated at approximately 63.6% of the market share in 2026. The dominance of this segment is primarily linked to strong adoption across commercial, industrial, and large residential applications requiring higher power output and balanced electricity distribution. Three-phase hybrid systems are widely used in commercial rooftops, industrial facilities, educational campuses, and large residential complexes where higher energy loads and larger battery systems are necessary.

These inverters provide superior efficiency, better grid interaction capabilities, and improved operational stability compared to single-phase alternatives. Manufacturers are increasingly focusing on advanced three-phase systems with smart energy management features, remote monitoring capabilities, and enhanced battery compatibility to strengthen competitiveness in commercial markets.

The single-phase hybrid segment is projected to witness the fastest growth during the forecast period due to increasing residential rooftop solar adoption. Single-phase systems are particularly suitable for households, small retail outlets, and small-scale commercial establishments with moderate power requirements. Government incentives for residential solar systems, rising electricity prices, and growing awareness regarding energy independence are supporting demand for compact single-phase hybrid systems.

Consumers increasingly prefer these systems because they offer backup power functionality, efficient battery integration, and lower installation complexity. Grid-tied hybrid systems continue to gain popularity among urban consumers seeking grid-connected energy optimization, while off-grid hybrid systems remain important in remote and under-electrified regions where reliable grid infrastructure is limited.

Application Insights

The commercial segment is anticipated to lead accounting for approximately 56.3% of the market share. Commercial buildings increasingly require hybrid inverter systems to improve energy efficiency, reduce operational expenses, and support sustainability initiatives. Retail centers, office complexes, hospitals, educational institutions, and hospitality facilities are adopting hybrid systems to optimize electricity consumption and ensure power continuity during outages.

Commercial deployments generally involve higher-capacity inverter systems and advanced battery integration, resulting in greater revenue contribution compared to residential installations. Increasing corporate commitments toward carbon reduction and energy optimization are expected to support continued expansion of commercial hybrid inverter adoption across developed and emerging economies.

The residential segment, is emerging as one of the fastest-growing application areas due to rapid rooftop solar deployment and rising demand for home energy storage solutions. Consumers are increasingly investing in hybrid systems to lower electricity bills, improve resilience against grid outages, and maximize solar self-consumption.

Government incentives, favorable financing options, and declining battery costs are making residential solar-plus-storage systems more financially viable. Industrial and utility-scale applications are also expanding steadily, particularly in regions with unreliable grid infrastructure or high industrial electricity consumption. Hybrid systems in these sectors are increasingly used for peak shaving, backup power management, and operational continuity.

Regional Insights

North America Solar Hybrid Inverter Market Trends

North America accounts for a significant share of the market, supported by rising solar-plus-storage adoption, grid modernization investments, and strong renewable energy policies. The region is projected to maintain stable growth throughout the forecast period, with a CAGR closely aligned with the global average of 9.9%. Demand is primarily concentrated in the United States and Canada, where residential backup power systems, commercial energy optimization, and distributed renewable energy infrastructure continue to expand.

U.S. Solar Hybrid Inverter Market Trends

The U.S. dominates the North America market, accounting for the majority of regional revenue generation. Strong federal incentives, expanding battery energy storage deployment, and rising electricity price volatility are supporting large-scale adoption of hybrid inverter systems. Commercial facilities, residential households, and industrial operators increasingly prefer solar-plus-storage systems to improve energy resilience and reduce dependence on centralized utility networks.

States, including California, Texas, Florida, Arizona, and New York, represent major deployment hubs due to high solar penetration and favorable policy frameworks. The growing frequency of grid disruptions and weather-related outages is also encouraging homeowners and businesses to invest in hybrid inverters with backup power capabilities. Increasing integration of smart-grid technologies and AI-enabled energy management systems is further strengthening market growth.

Canada Solar Hybrid Inverter Market Trends

Canada represents an emerging growth market for solar hybrid inverters, supported by distributed renewable energy investments and rural electrification projects. Provinces including Ontario, Alberta, and British Columbia are witnessing increasing solar deployment across residential and commercial sectors. Remote communities and off-grid infrastructure projects are also driving demand for hybrid inverter systems integrated with battery storage solutions.

Government sustainability initiatives and carbon reduction targets are supporting investments in decentralized renewable energy systems. However, permitting complexity, higher installation costs, and seasonal climate variations remain operational challenges affecting broader adoption rates.

Europe Solar Hybrid Inverter Market Trends

Europe remains one of the most technologically advanced and policy-driven markets for solar hybrid inverters. The region benefits from ambitious decarbonization goals, strong rooftop solar penetration, and increasing deployment of residential battery storage systems.

Germany Solar Hybrid Inverter Market Trends

Germany remains the leading market for solar hybrid inverters in Europe due to its advanced renewable energy infrastructure and strong residential solar adoption. Rising electricity costs and growing demand for energy independence are encouraging consumers to integrate battery storage systems with rooftop solar installations. Residential and commercial consumers increasingly prefer hybrid inverters capable of optimizing self-consumption and supporting backup power functionality.

The country also demonstrates strong demand for premium inverter technologies with advanced grid-support capabilities, cybersecurity integration, and smart monitoring systems. Commercial retrofit projects and battery storage upgrades continue to support market expansion.

U.K. Solar Hybrid Inverter Market Trends

The U.K. is experiencing steady growth in hybrid inverter adoption due to rising residential solar deployment and increasing interest in home energy storage systems. Government decarbonization initiatives and high electricity prices are encouraging households and businesses to invest in integrated solar-plus-storage infrastructure.

Demand is particularly strong in residential applications where consumers seek improved energy resilience and lower electricity costs. Commercial installations are also expanding as businesses pursue carbon reduction targets and energy efficiency improvements.

France Solar Hybrid Inverter Market Trends

France is strengthening its position in the European market through increased investments in renewable energy and supportive energy transition policies. Hybrid inverter demand is expanding across residential and commercial sectors as consumers adopt rooftop solar systems with battery storage.

The country’s focus on grid modernization and distributed renewable generation is supporting the deployment of advanced hybrid systems capable of intelligent energy management and peak-load optimization.

Asia Pacific Solar Hybrid Inverter Market Trends

Asia Pacific leads the market with approximately 50.7% market share and remains the fastest-growing region globally. The regional market is projected to grow at a CAGR 8.8%, supported by rapid solar deployment, strong manufacturing capabilities, and increasing investments in distributed renewable energy systems.

Manufacturers are expanding local distribution partnerships, technical training programs, and after-sales service capabilities to strengthen regional market penetration. Rapid urbanization and industrialization are expected to continue supporting demand for hybrid inverter systems across both residential and commercial sectors.

China Solar Hybrid Inverter Market Trends

China dominates the Asia Pacific market due to its massive solar manufacturing ecosystem, extensive photovoltaic deployment, and strong government support for renewable energy infrastructure. The country is the largest global production base for solar equipment and continues to expand residential, commercial, and utility-scale solar installations.

Hybrid inverter demand is increasing across industrial facilities, commercial buildings, and residential projects as battery storage integration becomes more common. Strong domestic manufacturing capabilities also provide Chinese companies with significant cost advantages in international markets.

India Solar Hybrid Inverter Market Trends

India is emerging as one of the fastest-growing markets for solar hybrid inverters, driven by aggressive rooftop solar programs, rural electrification initiatives, and rising residential solar adoption. Government programs supporting distributed renewable energy deployment are significantly increasing demand for residential hybrid inverter systems.

Commercial and industrial facilities are also investing in solar-plus-storage systems to reduce electricity costs and improve power reliability. The market benefits from increasing awareness regarding energy independence and rising investments in localized manufacturing infrastructure.

Competitive Landscape

The global solar hybrid inverter market remains moderately fragmented with strong regional competition. Chinese manufacturers maintain significant influence due to cost competitiveness, manufacturing scale, and extensive export networks. European companies remain strong in premium technology segments, while North American firms focus heavily on residential energy management systems and smart-grid integration.

Leading companies are prioritizing technological innovation, localization strategies, battery ecosystem partnerships, and software-driven energy management platforms to strengthen market competitiveness. Manufacturers are increasingly offering integrated solar-plus-storage ecosystems supported by remote monitoring, predictive maintenance, and intelligent grid interaction capabilities.

Key Industry Developments

- In May 2025, GoodWe launched new solar-plus-storage solutions at Intersolar Europe 2025, including the ESA residential all-in-one system and the ESA 125kW/261kWh commercial & industrial storage platform, aiming to strengthen its integrated smart energy ecosystem for residential and C&I applications.

- In June 2025, Hoymiles introduced its HY3 Series three-phase hybrid inverters designed for commercial and residential energy storage applications, focusing on improved ROI, higher operational efficiency, and enhanced battery compatibility.

Companies Covered in Solar Hybrid Inverter Market

- Huawei Digital Power

- Sungrow Power Supply Co., Ltd.

- SMA Solar Technology AG

- Growatt

- GoodWe

- Ginlong Solis

- Deye

- SolarEdge Technologies

- Enphase Energy

- Schneider Electric

- Delta Electronics

- FIMER

- Fronius International GmbH

- Hoymiles

- Victron Energy

- Sungrow Renewable Energy Investment Pte. Ltd.

Frequently Asked Questions

The global solar hybrid inverter market is projected to be valued at US$12.7 billion in 2026.

The solar hybrid inverter market is expected to reach US$24.9 billion by 2033.

Key trends include rising adoption of solar-plus-storage systems, increasing rooftop solar installations, growth in residential energy storage demand, expansion of smart-grid infrastructure, and increasing deployment of three-phase hybrid inverter systems in commercial applications.

The three-phase hybrid segment is the leading product type category, accounting for approximately 63.6% market share.

The solar hybrid inverter market is projected to grow at a CAGR of 10.1% between 2026 and 2033.

Major players include Huawei Digital Power, Sungrow Power Supply Co., Ltd., SMA Solar Technology AG, GoodWe, and Growatt.