- Renewable Energy

- E-Diesel Market

E-Diesel Market Size, Share, and Growth Forecast 2026 - 2033

E-Diesel Market by Renewable Source (On-site Solar, Wind), Technology (Fischer-Tropsch, eRWGS), Application (Automotive, Marine, Aviation, Industrial), and Regional Analysis, 2026 - 2033

E-Diesel Market Size and Trends Analysis

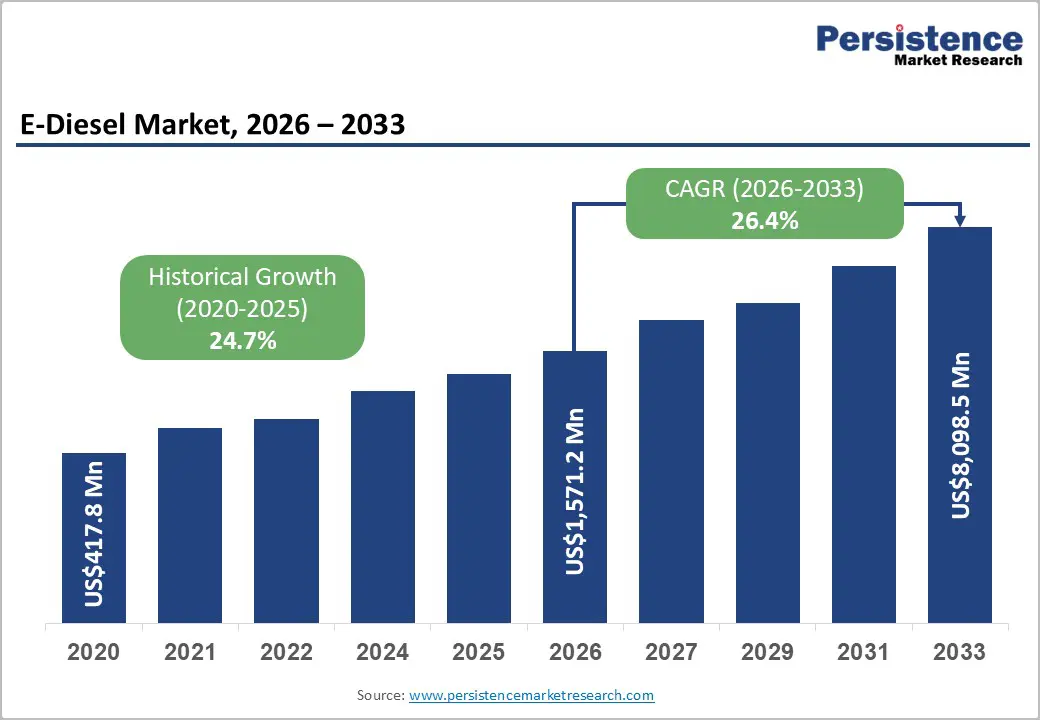

The global e-diesel market size is likely to be valued at US$1,571.2 million in 2026 and is expected to reach US$8,098.5 million by 2033, growing at a CAGR of 26.4% from 2026 to 2033, driven by strict emissions mandates across transport sectors, including the EU's Euro 7 standard effective from late 2026 and the FuelEU Maritime regulation active since January 2025.

Key Industry Highlights:

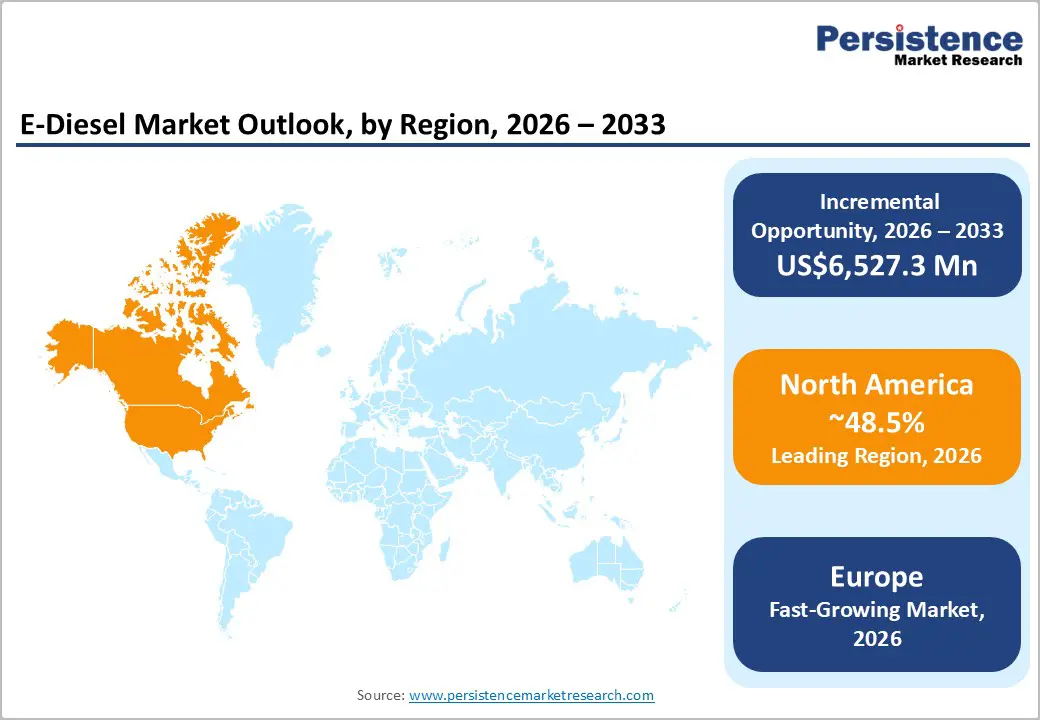

- Leading Region: North America, with about 48.5% share in 2026, as the U.S. combines the world's most commercially mature carbon credit framework.

- Fast-growing Region: Europe, as binding regulatory mandates across transport are converting policy intent into firm commercial demand.

- New Project: In January 2026, Norsk e-Fuel announced Project Tornio in Finland, co-located with Outokumpu's stainless steel operations in Koivuluoto. The project plans to produce 80,000 to 100,000 tons of sustainable fuel annually by using carbon monoxide side streams from Outokumpu's ferrochrome plant as a low-cost, continuously available feedstock.

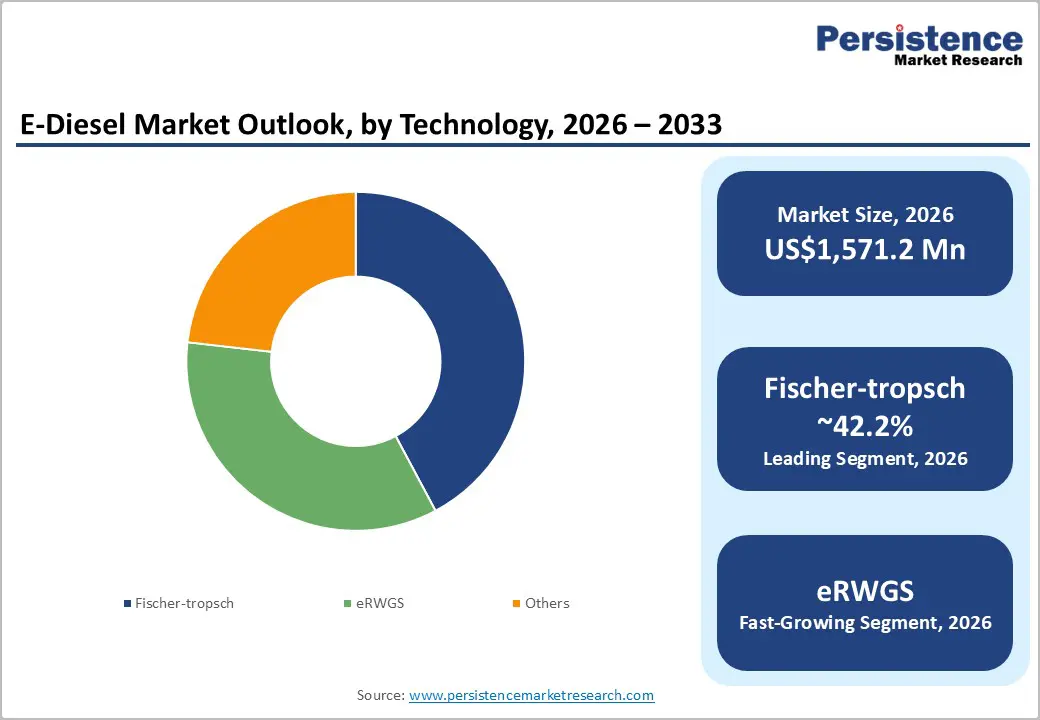

- Leading Technology: Fischer-Tropsch, approximately 42.2% share in 2026, as it is the only e-diesel production pathway with a 100-year industrial track record.

- Dominant Application: Automotive, nearly 35.7% in 2026, as it represents the largest existing pool of diesel-powered assets globally.

DRO Analysis

Driver - Compatibility with Engines, Fuel Chains, and Distribution Networks

One of the advantages of e-diesel is that it does not require any changes to existing engines, storage tanks, or delivery systems. E-diesel meets the standard petroleum specifications, i.e., ASTM D975 in the U.S. and EN 590 in Europe. This allows it to work as a direct drop-in replacement in diesel engines without modification. It is a key commercial edge over alternatives such as hydrogen or battery-electric, which require entirely new infrastructure.

Engine manufacturers, including Caterpillar, confirm that no specific engine conversion process is required when switching to paraffinic renewable and synthetic diesel alternatives. The same holds for distribution. Pipelines, storage terminals, tanker trucks, and fuel dispensers all remain compatible. This matters most for hard-to-electrify sectors such as long-haul trucking, marine shipping, and agriculture, where replacing physical infrastructure is neither practical nor cost-effective.

Strict Emissions Rules and Net-Zero Pledges to Boost Demand

Tightening regulations worldwide are pushing fleet operators and shipping companies toward low-carbon alternatives such as e-diesel. The EU's Euro 7 standard, set to come into effect in July 2025, introduces the strictest tailpipe emission limits yet for diesel engines, covering both exhaust and, for the first time, non-exhaust sources, including tire and brake particles. At sea, the pressure is equally strong.

In April 2025, the IMO approved a Net-Zero Framework, the first binding global regulation combining mandatory emissions limits and a GHG pricing mechanism across an entire industry sector. It targets net-zero shipping emissions by or around 2050. As e-diesel is chemically identical to fossil diesel but produced from green hydrogen and captured CO2, it delivers a ready-made compliance path without fleet overhauls. For sectors where full electrification remains decades away, it is increasingly becoming the practical answer to meeting these mandates.

Restraint - High Cost of Production to Limit Widespread Uptake

One of e-diesel's commercial barriers is its price. The core problem is in the production chain. It requires green hydrogen, which is made through electrolysis powered by renewable electricity, and that process is still costly. Green hydrogen currently costs between US$3.50 and US$6.00 per kg to produce, making it the most expensive hydrogen pathway available today. As green hydrogen is the primary feedstock for e-diesel, this cost flows directly into the final fuel price.

According to the International Council on Clean Transportation (ICCT), e-diesel produced in any country will likely remain substantially more expensive than fossil diesel until at least 2030. A Frontier Economics study commissioned by the eFuel Alliance further found that e-diesel production costs are projected to range between €1.58 (US$1.77) and €2 (US$2.24) per liter in 2025. This is well above the pump price of conventional diesel in most markets. Until green hydrogen costs fall and electrolyzer capacity expands significantly, e-diesel is expected to remain a premium product accessible mainly to sectors with regulatory or reputational pressure to decarbonize.

Opportunity - Long-Term Purchase Deals to Unlock Project Finance for Producers

Firm buyer commitments are becoming a key enabler for e-diesel and e-fuel producers to secure project financing. Without a guaranteed offtake, lenders won't fund capital-heavy production plants. This scenario, however, is changing. In January 2024, Norwegian Air Shuttle and Cargolux Airlines committed to purchasing fossil-free fuel from Norsk e-Fuel.

The combined offtake agreement covered more than 140,000 tons of fuel supply, along with supporting the development of two additional production facilities by 2030. Boeing followed this up by joining as a strategic partner and investor in January 2025. These agreements indicate that large transport buyers are moving beyond preliminary interest and making binding commercial commitments. As aviation and shipping regulations become more stringent, similar agreements are expected to increase, thereby strengthening the financial viability and bankability of e-diesel projects.

Expanding Carbon Management Infrastructure to Secure Low-Cost CO2 Feedstock

E-diesel production requires a steady, affordable supply of CO2. Until recently, this was a practical bottleneck. That is now beginning to shift. In August 2025, TotalEnergies, Equinor, and Shell successfully injected the first CO2 volumes into the Northern Lights project in Norway. It is the world's first merchant CO2 transport and storage facility. Its initial capacity of 1.5 Mt CO2 per year is fully booked by industrial customers across Europe.

In March 2025, the owners committed NOK 7.5 billion to broaden capacity from 1.5 to a minimum of 5 million tons of CO2 per year by 2028. As CO2 capture infrastructure expands, e-diesel producers gain access to a more reliable and cost-competitive feedstock. It is predicted to lower production costs and strengthen the commercial case for new plants.

Category-wise Analysis

Technology Insights

Fischer-Tropsch synthesis (FTS) is predicted to dominate with approximately 42.2% of the market share in 2026. FTS has a 100-year track record in industrial fuel production. The process, first patented in 1925, has evolved into a key driver of large-scale commercial plants, enabling the production of diesel, jet fuel, and gasoline from syngas. This long history means the process is well understood, bankable, and already supported by leading engineering firms. FT e-diesel has the highest energy density per kilometer among all alternative fuels and shares similar characteristics to fossil diesel. This makes it highly attractive as a drop-in substitute.

Electrochemical reverse water-gas shift (e-RWGS) is projected to be the fastest-growing segment in the forecast period. The e-RWGS reaction converts CO2 and hydrogen into carbon monoxide and water, producing syngas that feeds directly into FTS for diesel production. What makes it attractive is the ability to run it using renewable electricity, removing the need for high-temperature fossil fuel heating. A fully electrified RWGS process has been demonstrated at industrially relevant conditions using integrated ohmic heating and a nickel-type catalyst. It has achieved an H2/CO ratio of 2.0 with no detectable methane.

Application Insights

The automotive segment is estimated to lead in 2026, with nearly 35.7% of the share. Road transport, mainly heavy commercial vehicles, remains one of the most prominent consumers of diesel worldwide. Electrification is advancing in light-duty vehicles, but long-haul trucking faces range, payload, and charging time constraints that make a full battery-electric transition impractical for years. E-diesel, which functions identically to fossil diesel, plugs directly into this demand. Engine manufacturers, including Caterpillar, Cummins, and Volvo, have confirmed compatibility without modification, removing any adoption barrier for fleet operators.

The marine segment is estimated to remain in the second position in 2026, as shipping is under intense regulatory pressure and has very few decarbonization options that work at scale today. From 1 January 2025, the FuelEU Maritime regulation began monitoring and incentivizing the uptake of RFNBOs for ships over 5,000 gross tons calling at EU ports. It explicitly includes e-diesel. E-diesel's appeal here is a drop-in fuel that works in existing ship engines with no retrofitting.

Regional Insights

North America E-Diesel Market Trends

North America is expected to dominate with approximately 48.5% of the share in 2026, owing to regulatory incentives, early commercial-scale projects, and deep infrastructure for fuel distribution. California's Low Carbon Fuel Standard (LCFS) is a primary driver. It creates a direct revenue mechanism for e-fuel producers through tradeable carbon credits. The U.S. also has the Renewable Fuel Standard (RFS) at the federal level, layering additional policy support.

U.S. E-Diesel Market Trends

The U.S. blends two structural advantages: a mature carbon credit market and large available renewable energy capacity, specifically in wind-rich states such as Texas. HIF Global's Matagorda facility targets 1.4 million tons per year of e-fuels, one of the largest planned projects globally. The Inflation Reduction Act (IRA) layered on top of LCFS credits creates a double incentive structure.

The IRA provides green hydrogen tax credits of up to US$3.00 per kg, which directly reduces the cost of the primary input for e-diesel production. California's displacement of fossil diesel by renewable alternatives is also spurring. As e-diesel enters the LCFS credit program, it will likely compete for the same demand pools.

Europe E-Diesel Market Trends

Europe's growth is policy-driven and structured. The ReFuelEU Aviation mandate, FuelEU Maritime regulation, and RED III framework together create binding demand signals across transport sectors. The European Commission's Sustainable Transport Investment Plan, adopted in November 2025, estimates that 6.8 million tons of e-fuels will be required by 2035 to meet regulatory targets, requiring an estimated €100 billion in investment to propel production.

Europe also hosts the densest concentration of technology developers, including Sunfire, INERATEC, Norsk e-Fuel, and Liquid Wind. The EU's InvestEU program, European Investment Bank funding, and Innovation Fund grants are actively de-risking early-stage commercial projects. The region is also unique in having operating CO2 infrastructure, including the Northern Lights CCS facility in Norway.

Germany E-Diesel Market Trends

Germany leads Europe in e-fuel infrastructure, industrial policy implementation, and renewable energy capacity. In June 2025, INERATEC officially inaugurated ERA ONE in Frankfurt-Höchst, Europe's largest commercial-scale Power-to-Liquid plant. It is capable of producing up to 2,500 tons of carbon-neutral e-fuels annually, including e-diesel, from green hydrogen and biogenic CO2. The plant received a €70 million financing package comprising a €40 million venture debt loan from the European Investment Bank and a €30 million grant from Breakthrough Energy Catalyst. Germany also has an unusually superior automotive legacy that keeps it invested in liquid fuels.

U.K. E-Diesel Market Trends

The U.K. is advancing through a mandate-led model rather than subsidy-heavy spending. The Renewable Transport Fuel Obligations (Sustainable Aviation Fuel) Order 2024 came into force on January 1, 2025. It made the U.K. one of the first countries in the world to introduce mandatory SAF requirements, starting at 2% of aviation fuel in 2025 and rising to 10% by 2030. For synthetic e-fuels specifically, the mandate includes a Power-to-Liquid sub-obligation beginning at 0.2% in 2028 and rising to 3.5% by 2040, with non-compliance penalties set at £5.00 per liter.

Asia Pacific E-Diesel Market Trends

Asia Pacific is moving from pilot projects toward early commercial activity. Policy frameworks are strengthening in Japan, South Korea, and Australia, while China is boosting through biofuel blending mandates rather than power-to-liquid pathways. The region's advantages, including abundant solar and wind resources, proximity to high industrial demand, and government hydrogen roadmaps, position it as a key future production base.

Japan E-Diesel Market Trends

Japan is unique in that it has pursued a multi-pathway transport decarbonization strategy for years. Japan's GX2040 Vision and Plan for Global Warming Countermeasures, approved by the Cabinet in February 2025, includes synthetic fuels alongside hydrogen as priority decarbonization pathways for the road transport sector. It emphasizes the decarbonization of internal combustion engine fuels. The government's Green Innovation Fund, managed by NEDO, is actively backing domestic e-fuel pilots. A synthetic fuels demonstration plant backed by the country’s government also began operations in September 2024.

China E-Diesel Market Trends

China holds enormous structural advantages, including low-cost renewable electricity, dominant electrolyzer manufacturing, and massive industrial expansion. But near-term demand for synthetic diesel specifically faces headwinds from China's constant EV and LNG adoption. The country’s position in the e-diesel supply chain is unmatched globally. By the end of 2024, it will lead the world in electrolysis capacity at 3.5 GW, accounting for 70% of global installed capacity, with projections to reach 50 GW by 2030. This matters enormously for e-diesel, which requires green hydrogen as its primary feedstock.

Competitive Landscape

The global e-diesel market is highly fragmented, with no single dominant player. The competitive field splits into two distinct groups. Synthesis technology specialists such as HIF Global and Sunfire combine hydrogen and CO2 to produce e-diesel through power-to-liquid processes. On the other hand, electrolyzer suppliers, including Siemens Energy and Nel, provide the underlying technology. Oil majors such as ExxonMobil and TotalEnergies use their existing infrastructure to enter the market with far less technological risk.

HIF Global and Porsche are pursuing vertical integration by controlling everything from renewable power generation to carbon capture and fuel synthesis. They aim to manage costs and secure supply. Firms such as Uniper, Air Liquide, and Siemens Energy are going the partnership route, forming alliances with hydrogen producers and governments to reduce capital burden.

Key Industry Developments:

- In August 2025, Rolls-Royce Power Systems and INERATEC formed a strategic partnership to replace fossil diesel in emergency backup generators for data centers with synthetic e-diesel produced from green hydrogen and CO2. The initial rollout targets Germany’s data centers, using INERATEC's ERA ONE production facility in Frankfurt for short delivery routes.

- In March 2025, HIF Global became the first company to receive U.S. approval for an e-fuels pathway, in the form of a Tier II Design Pathway Certification under the California Air Resources Board's Low Carbon Fuel Standard program. The certification covers e-SAF, e-Naphtha, and e-Diesel, allowing producers to generate carbon credits under the program.

- In January 2025, Norsk e-Fuel announced Prime Capital AG as a new shareholder and separately signed a partnership with Boeing covering both offtake and project support. This marked one of the first major aerospace-company commitments to a European power-to-liquid producer.

Companies Covered in E-Diesel Market

- Arcadia eFuels

- Ballard Power Systems, Inc.

- CAC Synfuel Plant

- Clean Fuels Alliance America

- Ceres Power Holding Plc

- Climeworks AG

- ExxonMobil

- eFuel Pacific Limited

- Electrochaea GmbH

- FuelCell Energy, Inc.

- HIF Global

- INERATEC GmbH

- Liquid Wind

- LanzaJet

- MAN Energy Solutions

- Norsk E-Fuel AS

- Nordic Electrofuel

- Porsche

- Sunfire GmbH

- Synhelion

Frequently Asked Questions

The global e-diesel market is projected to be valued at US$1,571.2 million in 2026.

The e-diesel market is expected to reach US$8,098.5 million by 2033.

Increasing integration with renewable energy and favorable government policies are a few key market trends.

Automotive is expected to lead in 2026 with nearly 35.7% of the share, as e-diesel enables fleet operators to meet stringent emissions regulations.

The e-diesel market is expected to grow at a CAGR of 26.4% from 2026 to 2033.

Arcadia eFuels, Ballard Power Systems, Inc., CAC Synfuel Plant, and Clean Fuels Alliance America are a few key market players.