- Renewable Energy

- Micro Inverter Market

Micro Inverter Market Size, Share, and Growth Forecast, 2026 - 2033

Micro Inverter Market by Phase (Single-Phase, Three-Phase, Others), Application (Residential, Commercial, Others), Power Rating, and Regional Analysis for 2026 - 2033

Micro Inverter Market Size and Trends Analysis

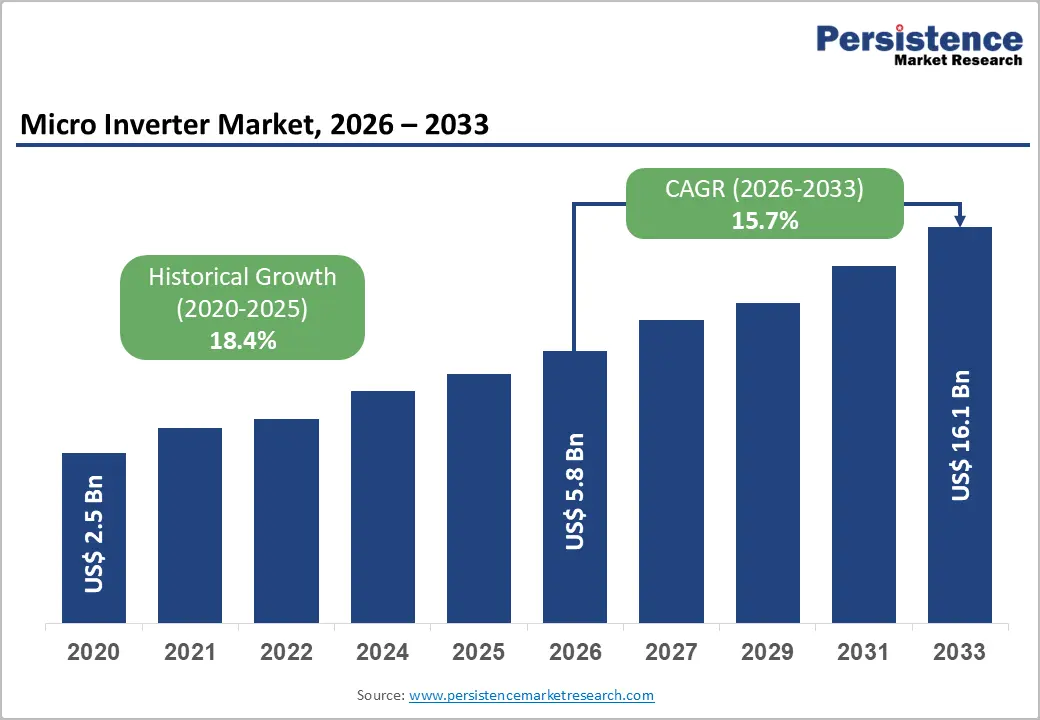

The global micro inverter market size is likely to be valued at US$5.8 billion in 2026 and is expected to reach US$16.1 billion by 2033, growing at a CAGR of 15.7% between 2026 and 2033, driven by the rising adoption of rooftop solar systems, increasing demand for panel-level power optimization, and the implementation of stricter electrical safety standards.

Microinverters are gaining significant traction in residential and small-scale commercial solar installations due to their ability to maximize energy generation in partially shaded conditions, enable flexible system expansion, and provide advanced module-level monitoring. Demand is further accelerating across regions focused on distributed renewable energy integration, building electrification, and strengthening energy resilience infrastructure.

Key Industry Highlights:

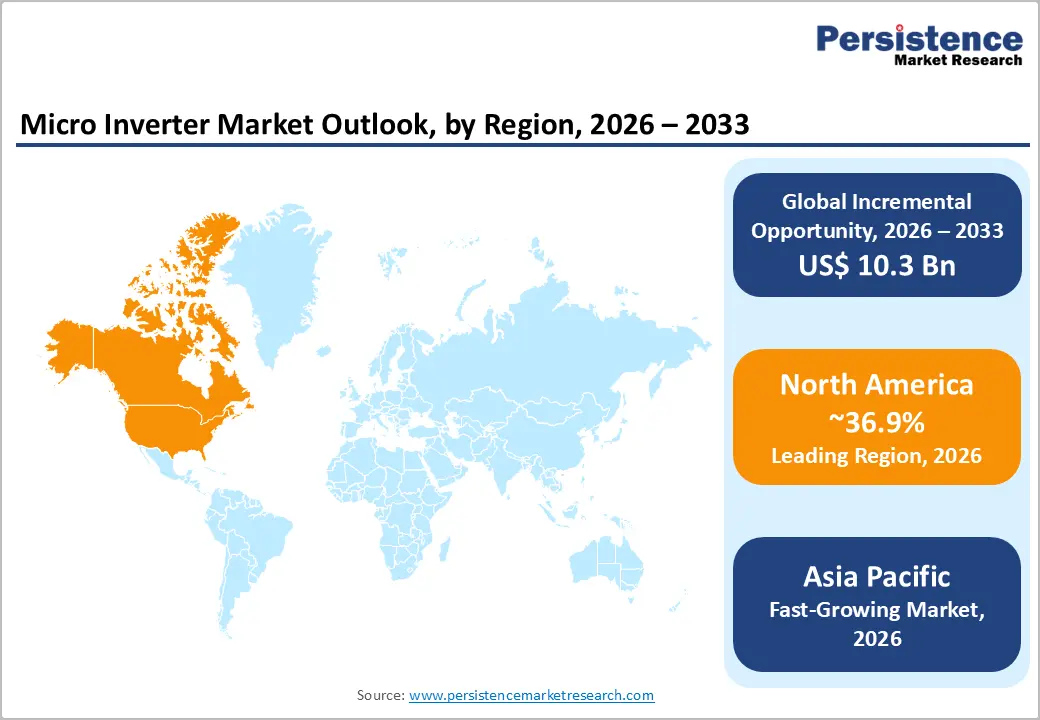

- Leading Region: North America is projected to lead with an anticipated 36.9% market share in 2026, supported by strong residential rooftop solar adoption, rapid shutdown safety regulations, and advanced installer networks across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market, due to rapid rooftop solar deployment, strong manufacturing capabilities, and increasing renewable energy investments across China, India, Japan, and ASEAN countries.

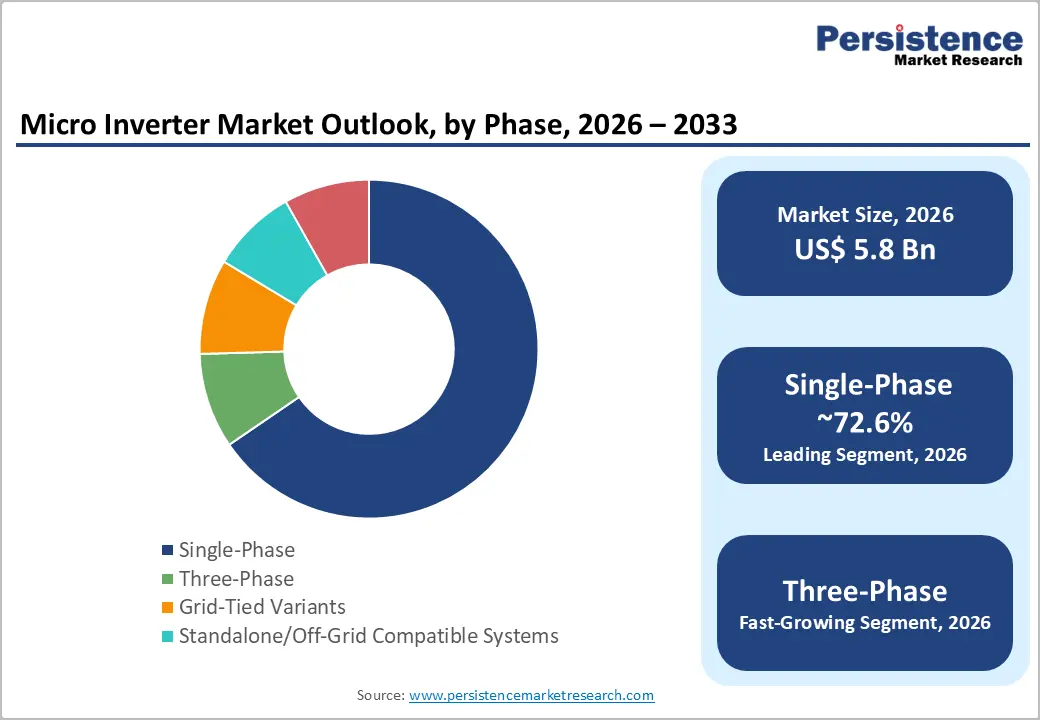

- Dominant Phase: Single-phase systems are anticipated to dominate with 72.6% of market share in 2026, driven by widespread residential rooftop solar adoption and growing demand for panel-level monitoring and modular system scalability.

- Leading Application: Residential applications are estimated to account for nearly 43.4% market share in 2026, supported by rising rooftop solar penetration, government incentives, energy independence goals, and increasing adoption of smart-home integrated solar systems.

DRO Analysis

Driver - Rooftop Solar Expansion and Rising Adoption of Module-Level Power Electronics

Global solar photovoltaic deployment continues to accelerate as countries pursue decarbonization and energy security goals. Distributed solar installations are becoming a major contributor to renewable electricity generation, particularly in residential and small commercial segments, where rooftop optimization is critical. Microinverters provide independent maximum power point tracking at the module level, improving the overall system efficiency when panels experience shading, orientation mismatch, or partial obstruction.

The increasing complexity of residential rooftops and the growing use of high-efficiency solar modules are strengthening demand for module-level power electronics. Homeowners and installers increasingly prioritize monitoring visibility, design flexibility, and long-term reliability, all of which favor microinverter adoption. The market impact is substantial as each additional rooftop solar installation expands the addressable opportunity for panel-level electronics instead of centralized string inverter systems. This trend is especially evident in North America, Europe, and Asia Pacific, where residential solar deployment remains a core renewable energy strategy.

Supportive Safety Regulations and Building Electrification Policies

Regulatory frameworks promoting rapid shutdown compliance, rooftop safety, and solar-ready building infrastructure are accelerating the adoption of microinverters globally. Building authorities increasingly emphasize safer rooftop electrical systems that reduce high-voltage DC exposure and improve maintenance accessibility. Microinverters support these requirements by converting DC to AC directly at the panel level, reducing the need for high-voltage DC cabling across rooftops.

Government rooftop solar initiatives are also expanding market demand. Public policy frameworks in the U.S., Europe, India, and Japan continue to encourage distributed solar deployment through tax incentives, rooftop installation mandates, and renewable energy transition programs. In India, rooftop solar targets are significantly increasing residential and commercial solar adoption, while Europe’s solar-ready building initiatives are creating long-term installation opportunities. These regulatory developments not only stimulate demand but also strengthen customer preference for safer and easier-to-expand solar architectures supported by microinverter systems.

Restraint - Higher Initial Costs and Financing Sensitivity Compared to String Inverters

Despite strong operational advantages, microinverters remain more expensive than traditional string inverter systems in many installations. The technology improves shade tolerance, module-level monitoring, and system flexibility, but upfront hardware costs can create adoption barriers in price-sensitive markets. Residential customers and installers often evaluate systems based on payback periods, making financing conditions and interest rates critical purchasing factors.

Demand volatility can increase when rooftop solar incentives decline or financing conditions tighten. In several developed markets, changes in net-metering frameworks and softer residential demand have affected solar equipment purchasing patterns. Microinverters may also face efficiency trade-offs relative to some centralized inverter configurations, particularly in large-scale installations where cost optimization is prioritized over module-level control. These structural challenges may slow adoption in emerging markets where rooftop solar economics remain highly subsidy-dependent.

Opportunity - Commercial Rooftop Expansion and Higher-Wattage Solar Modules

Commercial and industrial rooftop installations are creating significant growth opportunities for advanced microinverter systems. The market is shifting toward larger solar modules with higher wattage output, increasing demand for high-capacity microinverters capable of supporting commercial energy requirements. Manufacturers are responding with three-phase architectures, higher-power configurations, and multi-module microinverter platforms designed specifically for commercial rooftop applications.

Commercial customers increasingly seek integrated energy management capabilities that combine solar generation, monitoring, storage compatibility, and grid optimization. This transition expands the value proposition of microinverters beyond power conversion alone. Higher-capacity installations also improve revenue opportunities for manufacturers ascommercial systems typically require more advanced monitoring, connectivity, and service capabilities. As businesses prioritize energy cost reduction and sustainability targets, the commercial rooftop segment is expected to become one of the most profitable growth areas within the market.

Energy Resilience Demand and Smart Energy Ecosystem Integration

Rising consumer interest in backup power, energy resilience, and smart-home integration is expanding the role of microinverters within distributed energy systems. Residential customers increasingly prefer solar solutions that integrate with battery storage, load management systems, and digital monitoring platforms. Microinverters are well-positioned within this ecosystem as they enable modular scalability and simplify system expansion over time.

Emerging rooftop solar markets in Asia Pacific and Europe are also creating long-term opportunities for integrated residential energy platforms. Governments promoting electrification, low-carbon buildings, and renewable self-consumption are encouraging the adoption of storage-ready solar infrastructure. Manufacturers are therefore positioning microinverters as part of broader home energy management ecosystems rather than standalone hardware products. This transition enables suppliers to generate recurring revenue through software, monitoring services, and storage integration solutions while improving customer retention across the installation lifecycle.

Category-wise Analysis

Phase Analysis

Single-phase microinverter systems are anticipated to account for 72.6% of market share in 2026, due to their strong alignment with residential rooftop solar installations. Most households operate on single-phase electrical infrastructure, making these systems highly suitable for compact rooftop arrays and suburban housing developments. Homeowners increasingly prefer single-phase microinverters for panel-level monitoring, simplified installation, and easy system expansion.

The segment continues gaining traction across the U.S., Germany, Japan, and India, where rooftop solar adoption remains strong. For example, Enphase Energy’s IQ series is widely deployed in residential solar projects due to its compatibility with home energy management systems and battery storage integration. Rising adoption of rooftop solar in urban residential communities and smart-home ecosystems continues to reinforce segment leadership.

Three-phase microinverter systems are projected to witness the fastest growth as commercial rooftops and larger residential buildings require higher-capacity solar infrastructure. These systems provide better compatibility with commercial electrical networks and support advanced energy management applications.

Manufacturers are increasingly introducing high-capacity three-phase platforms for commercial and industrial installations. For instance, APsystems and Hoymiles have launched multi-module commercial microinverters supporting higher-wattage solar panels and enhanced monitoring capabilities. Growth is particularly strong across Europe, North America, and Asia Pacific, where businesses are investing in distributed renewable energy systems to support decarbonization and energy cost optimization.

Application Analysis

The residential segment is anticipated to hold nearly 43.4% of market share in 2026, as rooftop solar remains the primary application for module-level power electronics. Homeowners increasingly prioritize energy independence, lower electricity bills, and sustainable energy generation, driving strong demand for residential solar systems with panel-level optimization.

Government subsidies, tax credits, and rooftop solar incentive programs continue supporting adoption across North America, Europe, Japan, and India. For example, residential solar installations in California and Germany frequently utilize microinverter-based systems for improved shading performance and real-time monitoring. The segment also benefits from strong installer familiarity and growing adoption of integrated solar-plus-storage solutions.

Commercial applications are projected to grow at the fastest pace, due to rising corporate sustainability initiatives and increasing investments in rooftop solar infrastructure across warehouses, office buildings, and industrial facilities. Businesses are adopting microinverter-based systems to reduce electricity costs, improve ESG performance, and strengthen energy resilience.

The segment is benefiting from increasing deployment of smart-building technologies and high-capacity solar modules. For example, Enphase Energy and APsystems have introduced commercial-grade microinverter platforms specifically designed for three-phase commercial rooftop installations. Demand is particularly strong in the U.S., China, Germany, and Australia, where commercial decarbonization targets continue accelerating distributed solar adoption.

Regional Insights

North America Micro Inverter Market Trends

North America is projected to account for approximately 36.9% of market share in 2026, supported by strong residential solar adoption, advanced installer networks, and favorable rooftop solar regulations.

U.S. Micro Inverter Market Trends

The U.S. dominates the North America market, due to high rooftop solar penetration, federal renewable energy incentives, and rapid shutdown safety requirements. California, Texas, Florida, and Arizona remain major solar installation hubs due to strong solar irradiation and supportive clean-energy policies. Residential consumers increasingly prefer microinverters with integrated monitoring, battery storage compatibility, and smart-home energy management features. Commercial rooftop installations are also expanding as businesses focus on decarbonization and electricity cost reduction.

Canada Micro Inverter Market Trends

Canada is steadily expanding its distributed renewable energy infrastructure, particularly in provinces supporting sustainable construction and energy-transition initiatives. Residential rooftop solar adoption is increasing in Ontario, British Columbia, and Alberta, where consumers are prioritizing energy efficiency and grid resilience solutions.

Europe Micro Inverter Market Trends

Europe remains a strategically important market driven by renewable energy mandates, building electrification policies, and rooftop solar expansion initiatives.

Germany Micro Inverter Market Trends

Germany is the largest market in Europe due to its mature solar infrastructure and widespread residential rooftop adoption. The country’s strong focus on energy independence and decentralized renewable generation continues driving demand for module-level power electronics. Balcony solar systems and compact rooftop installations are also supporting microinverter adoption across urban areas.

U.K Micro Inverter Market Trends

The U.K. is witnessing growing rooftop solar deployment supported by clean-energy transition goals and rising electricity prices. Residential and commercial users increasingly prefer distributed solar systems integrated with battery storage and energy management solutions.

France Micro Inverter Market Trends

France is strengthening rooftop solar deployment through renewable energy targets and sustainable building initiatives. Commercial rooftop installations are increasing steadily as businesses focus on lowering operational energy costs and improving ESG performance.

Spain Micro Inverter Market Trends

Spain remains one of Europe’s fastest-growing solar markets due to favorable solar irradiation and supportive renewable energy policies. Commercial and industrial rooftop installations are expanding rapidly across logistics, manufacturing, and retail facilities.

Asia Pacific Micro Inverter Market Trends

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 17.9% during the forecast period. The region benefits from strong manufacturing capabilities, expanding rooftop solar deployment, and rising renewable energy investments.

China Micro Inverter Market Trends

China serves as both the world’s largest solar manufacturing hub and a rapidly growing domestic rooftop solar market. Chinese manufacturers continue investing in higher-capacity and intelligent microinverter platforms to strengthen global competitiveness. The country’s large-scale photovoltaic ecosystem supports lower production costs and rapid technological advancement.

India Micro Inverter Market Trends

India is emerging as a high-growth market due to aggressive rooftop solar deployment targets and increasing government support for residential renewable energy adoption. Rising electricity demand, urbanization, and energy affordability concerns are accelerating rooftop solar installations across residential and small commercial sectors.

Japan Micro Inverter Market Trends

Japan remains a key market due to its emphasis on energy-efficient buildings, distributed generation, and long-term decarbonization goals. Residential consumers prioritize compact, reliable, and space-efficient rooftop systems, supporting strong adoption of microinverter technologies.

Competitive Landscape

The global micro inverter market demonstrates a moderately consolidated competitive structure, with a limited number of established players controlling a substantial share of global revenue. The market is led by Enphase Energy, which maintains a dominant position due to its strong installer ecosystem, integrated software platform, extensive patent portfolio, and early-mover advantage in module-level power electronics. Industry assessments indicate that the top five companies collectively account for more than 70%-80% of global market revenue.

The market also includes regional and niche competitors such as SMA Solar Technology, Darfon Electronics, Growatt, SolaX Power, Generac, and Northern Electric Power, which focus on emerging markets, commercial rooftop projects, storage integration, and off-grid applications. Mid-tier players compete primarily through pricing flexibility, regional distribution strength, and installer-friendly system architectures.

Key Industry Developments:

- In April 2025, Enphase Energy expanded its European presence by introducing the IQ Battery 5P with FlexPhase in Luxembourg, targeting growing demand for resilient rooftop solar and backup power systems in three-phase residential applications.

Companies Covered in Micro Inverter Market

- Enphase Energy

- APsystems

- Hoymiles

- SolarEdge Technologies

- SMA Solar Technology AG

- Northern Electric Power

- Darfon Electronics

- Envertech

- Chilicon Power

- Altenergy Power System Inc.

- Sparq Systems

- AEconversion GmbH & Co. KG

- Growatt New Energy

- SolaX Power

- Fronius International GmbH

- Ginlong Technologies (Solis)

Frequently Asked Questions

The global micro inverter market is projected to reach US$5.8 billion in 2026.

The micro inverter market is anticipated to reach US$16.1 billion by 2033.

Major trends include rising rooftop solar adoption, increasing deployment of solar-plus-storage systems, growth in smart-home integrated energy solutions, expansion of commercial rooftop solar projects, and rising adoption of higher-capacity three-phase microinverters.

Single-phase systems lead the market with an anticipated 72.6% share, primarily driven by strong residential rooftop solar adoption.

The micro inverter market is projected to grow at a CAGR of 15.7% between 2026 and 2033.

Key companies with strong market portfolios include Enphase Energy, APsystems, Hoymiles, and SolarEdge Technologies.