- Renewable Energy

- Solar Fasteners Market

Solar Fasteners Market Size, Share, and Growth Forecast, 2026 - 2033

Solar Fasteners Market by Product Type (Fastening Sets for Metal Roofs, Metric Fasteners, Others), Material (Stainless Steel Fasteners, Aluminum Alloy Fasteners, Others), Application, End-use Industry, and Regional Analysis for 2026 - 2033

Solar Fasteners Market Size and Trends Analysis

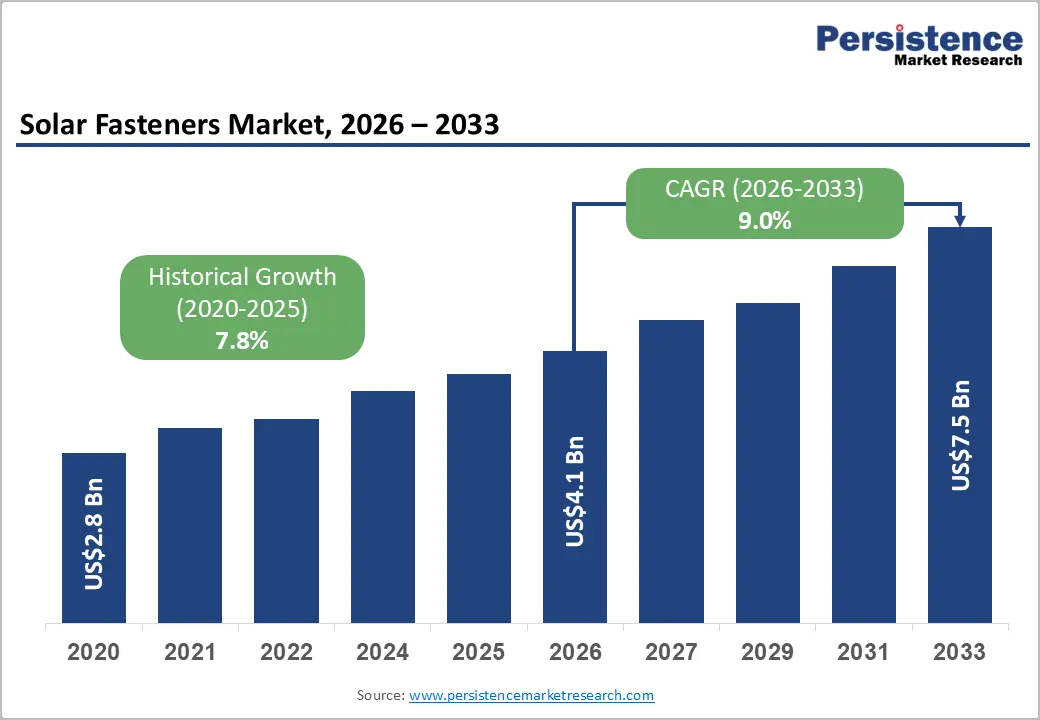

The global solar fasteners market size is likely to be valued at US$4.1 billion in 2026 and is expected to reach US$7.5 billion by 2033, growing at a CAGR of 9.0% between 2026 and 2033, driven by the rapid deployment of solar photovoltaic (PV) infrastructure across utility-scale, commercial, industrial, and residential sectors.

Increasing rooftop solar adoption, growth in utility-scale renewable projects, and rising demand for corrosion-resistant mounting hardware continue to support market expansion. Fasteners are becoming strategically important components in solar installations because project developers increasingly prioritize long-term structural reliability, installation efficiency, and compliance with international safety standards.

Key Industry Highlights:

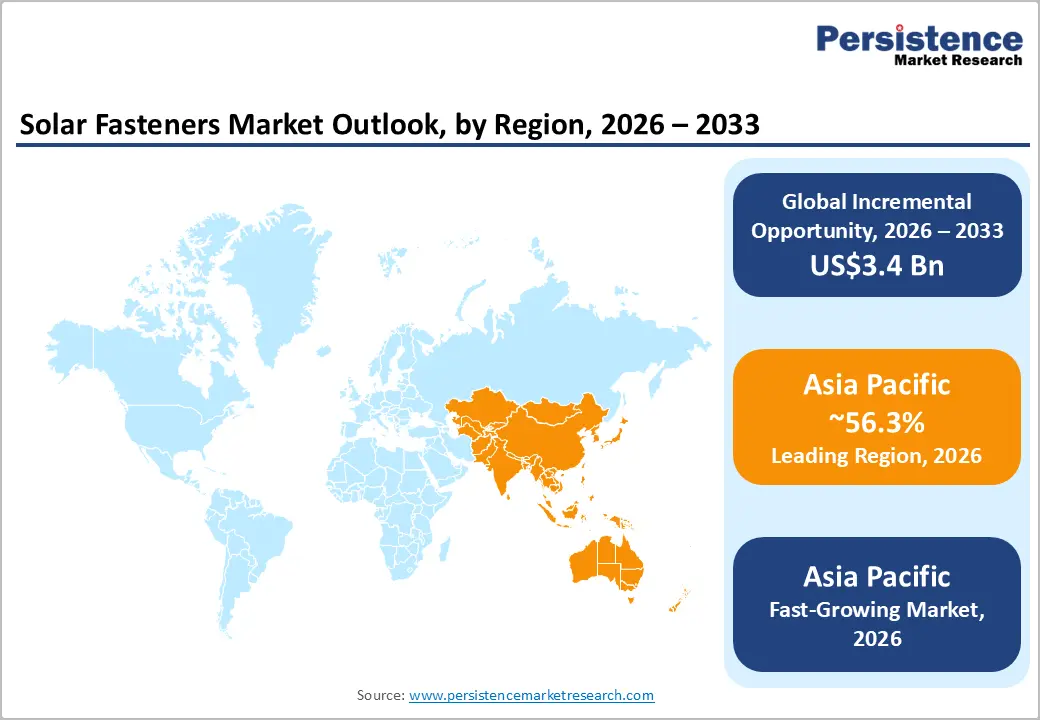

- Leading Region: Asia Pacific is anticipated to account for 56.3% of the market share in 2026, supported by large-scale solar deployment across China, India, Japan, and ASEAN countries, along with strong regional manufacturing capabilities.

- Fastest-growing Region: Asia Pacific is projected to remain the fastest-growing regional market during the forecast period, driven by rapid utility-scale and rooftop solar expansion, government renewable energy targets, and increasing localization of solar component manufacturing.

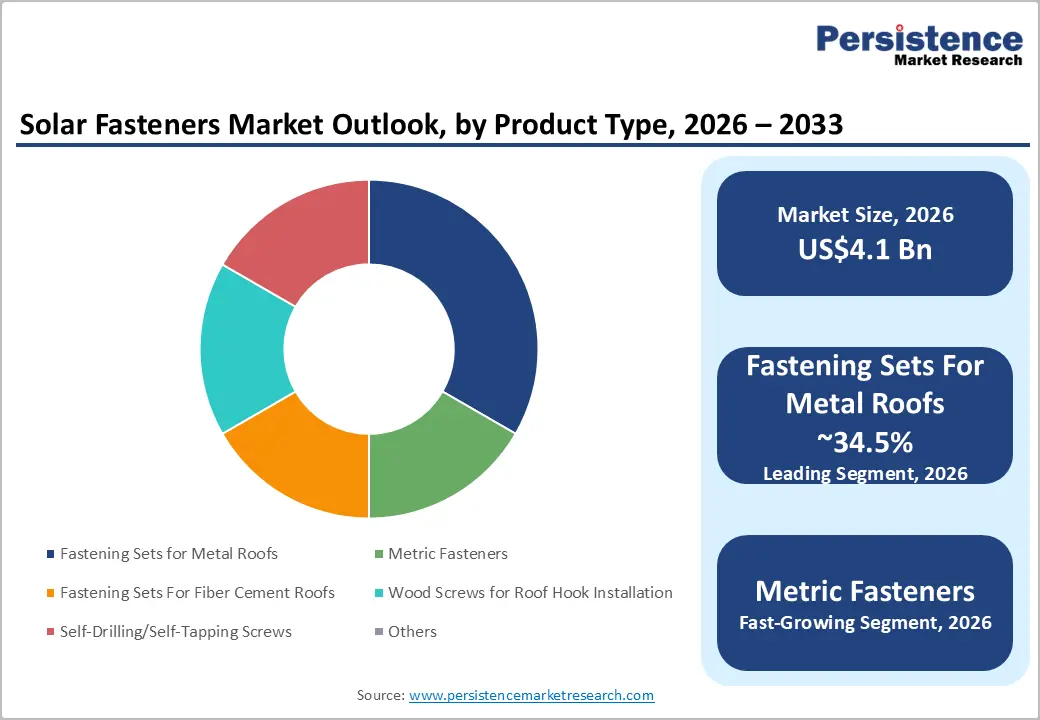

- Dominant Product Type: Fastening sets for metal roofs are anticipated to hold approximately 34.5% of the market share in 2026, due to strong demand from commercial, industrial, and retrofit rooftop solar installations.

- Leading End-use Industry: Utility-scale solar projects are anticipated to account for nearly 28.6% of the market share in 2026, supported by large solar farm developments requiring high volumes of mounting hardware and structural fastening systems.

DRO Analysis

Driver - Rising Solar Deployment across Utility-Scale and Distributed Projects

The expansion of solar PV capacity remains the primary growth driver for the solar fasteners market. Every new solar installation requires mounting systems, anchors, clamps, roof hooks, screws, and structural fastening components, directly increasing demand for specialized fastening solutions. Global renewable energy expansion has accelerated significantly, with solar accounting for the majority of new renewable power additions in recent years. Utility-scale solar farms, commercial rooftop systems, and residential solar installations are all contributing to a broader installed base requiring durable fastening hardware.

The United States continues to add substantial solar generation capacity annually, while Europe maintains strong deployment despite periodic fluctuations in subsidy structures and energy pricing. Emerging economies across Asia Pacific, particularly China and India, are scaling solar capacity aggressively through large public and private investments. This sustained expansion creates long-term recurring demand for fastening systems designed specifically for solar mounting applications, especially in projects requiring high wind-load resistance and long operational lifecycles.

Growing Preference for Compliance-Driven and Durable Fastening Systems

Solar systems are designed to operate for 28.6 years, increasing the importance of fastening durability and structural integrity. Fasteners used in PV installations must withstand wind uplift, vibration, corrosion, thermal expansion, moisture exposure, and fluctuating environmental conditions. As a result, project developers and EPC contractors increasingly prefer certified fastening systems that comply with international installation and safety standards.

The market is witnessing growing demand for stainless steel fasteners, coated steel systems, and engineered fastening assemblies that reduce maintenance risks and improve system longevity. Regulatory frameworks governing mounting systems, grounding mechanisms, and fire resistance are also influencing procurement decisions. Installers are shifting away from low-cost generic construction fasteners toward application-specific solar fastening products that offer improved reliability, warranty compatibility, and lower lifecycle costs. This trend supports premiumization within the market and improves opportunities for technologically differentiated suppliers.

Restraint - Pricing Pressure and Supply-Chain Complexity

One of the primary challenges facing the solar fasteners market is pricing pressure caused by commoditization and competition from conventional construction hardware suppliers. In cost-sensitive projects, procurement teams often prioritize upfront cost reductions, creating downward pressure on profit margins. Standardized products such as screws, anchors, and clamps face intense competition, particularly in large rooftop installations where buyers compare solar-specific products with cheaper alternatives.

The market also faces supply-chain risks associated with raw material volatility. Stainless steel, aluminum, and zinc-coated steel prices fluctuate depending on global industrial demand, trade conditions, and energy costs. These fluctuations can affect manufacturing costs and inventory planning for fastening suppliers. In addition, solar projects frequently encounter permitting delays, regulatory approvals, and logistical disruptions, which can postpone hardware procurement schedules and create working-capital challenges for manufacturers and distributors.

Opportunity - Expansion of Modular and Prefabricated Mounting Systems

The increasing adoption of modular and prefabricated solar mounting systems presents a major growth opportunity for fastening manufacturers. Solar installers are seeking mounting solutions that reduce labor requirements, simplify installation workflows, and minimize on-site assembly complexity. This trend is driving demand for standardized metric fasteners, rail-less mounting systems, integrated clamps, and pre-engineered fastening kits.

Manufacturers are increasingly integrating fastening products with digital planning software, installation support tools, and compliance documentation services. The market is transitioning from standalone fastening hardware toward integrated mounting ecosystems that improve installation speed and reduce operational errors. Suppliers capable of delivering installation-friendly, application-specific fastening systems are expected to gain stronger positioning in both mature and emerging solar markets.

Strong Growth Potential across Asia Pacific and India

Asia Pacific remains the most attractive growth region for solar fasteners due to its dominant position in global solar deployment and manufacturing. The region accounts for 56.3% of the global solar fasteners market share and continues to benefit from aggressive renewable energy investments, supportive government policies, and expanding domestic manufacturing ecosystems.

China remains the largest contributor to global solar capacity additions, while India is rapidly increasing rooftop, utility-scale, and agricultural solar deployment through national renewable energy programs. Large-scale infrastructure development across ASEAN countries is also creating significant demand for solar mounting and fastening systems. Regional manufacturing advantages, lower production costs, and localized supply chains further strengthen Asia Pacific’s leadership position within the global market.

Category-wise Analysis

Product Type Insights

Fastening sets for metal roofs are anticipated to account for 34.5% of the market share in 2026, due to their widespread use in commercial, industrial, and retrofit rooftop solar projects. Metal roofs are commonly installed on warehouses, logistics centers, and manufacturing facilities, where solar adoption continues to expand rapidly. These systems require specialized clamps, sealing components, and corrosion-resistant screws that protect roof integrity while supporting long-term PV performance. Companies such as Schletter, K2 Systems, and S-5! have strengthened demand for metal-roof fastening solutions through rail-compatible and low-penetration mounting technologies.

Metric fasteners are anticipated to witness the fastest growth during the forecast period, supported by increasing standardization across global solar mounting systems. Large utility-scale and modular solar projects increasingly rely on metric-compatible rails, clamps, and structural assemblies to simplify installation and reduce procurement complexity. The segment is benefiting from rising adoption of prefabricated mounting systems and automated installation workflows. Manufacturers such as EJOT and fischer are expanding metric-compatible fastening portfolios to support faster installation and improved interchangeability across international solar projects.

End-use Industry Insights

Utility-scale solar projects are anticipated to account for 28.6% of the market share in 2026, owing to the large hardware requirements of solar farms and ground-mounted installations. These projects require high volumes of anchors, clamps, structural fasteners, and mounting hardware to support thousands of solar modules across extensive project sites. Demand remains strong across the U.S., China, India, and the Middle East, where governments and private developers continue investing heavily in renewable energy infrastructure. Large EPC contractors increasingly prioritize fastening systems with high wind-load resistance, corrosion protection, and long operational lifecycles.

Construction and real estate are anticipated to be the fastest-growing end-use segments, due to the rising integration of rooftop solar systems into residential, commercial, and industrial buildings. Green building regulations, energy-efficiency standards, and increasing electricity costs are encouraging developers to integrate solar infrastructure during initial construction and retrofit projects. Demand is particularly strong for low-penetration clamps, lightweight mounting hardware, and aesthetically integrated fastening systems used in office buildings, retail centers, and residential housing developments. This trend is creating strong growth opportunities for manufacturers offering modular and building-compatible fastening solutions.

Regional Insights

North America Solar Fasteners Market Trends

North America represents a high-value market for solar fasteners, due to rapid solar deployment, strong regulatory frameworks, and increasing domestic manufacturing activity. The region benefits from rising investments in utility-scale solar farms, commercial rooftop systems, and energy-transition infrastructure projects. Demand for certified fastening systems continues to increase as EPC contractors prioritize structural durability, fire safety compliance, and long-term system reliability.

U.S. Solar Fasteners Market Trends

The U.S. is the dominant market in North America, supported by large utility-scale solar projects, expanding rooftop solar adoption, and federal clean energy incentives. Solar energy continues to account for a significant share of new electricity generation capacity additions across the country. Demand for solar fasteners is particularly strong in utility-scale projects across Texas, California, Arizona, and Nevada, where large solar farms require substantial volumes of mounting hardware, anchors, clamps, and structural fasteners.

Strict compliance standards related to mounting systems, grounding, fire safety, and structural integrity are shaping procurement strategies. Developers increasingly prioritize UL-certified fastening systems capable of reducing inspection timelines and improving long-term performance. Commercial warehouse rooftop installations and industrial retrofit projects are also driving demand for low-penetration fastening solutions and corrosion-resistant roof attachments.

Canada Solar Fasteners Market Trends

Canada is witnessing gradual growth in solar infrastructure development, particularly across Ontario and Alberta. Commercial rooftop solar installations and community solar projects are increasing demand for durable fastening systems capable of withstanding harsh winter conditions and thermal fluctuations. The market also benefits from rising investments in sustainable buildings and renewable energy integration within industrial and public infrastructure projects.

Europe Solar Fasteners Market Trends

Europe remains a strategically important market driven by renewable energy targets, sustainability regulations, and widespread rooftop solar adoption. Demand for advanced solar fastening systems is increasing across both rooftop and utility-scale projects, particularly in applications requiring long-term corrosion resistance and roof-preserving installation methods. European suppliers compete aggressively on engineering quality, structural reliability, installation efficiency, and compliance with regional standards.

Germany Solar Fasteners Market Trends

Germany remains the leading solar fasteners market in Europe due to its mature rooftop solar ecosystem and strong renewable energy policies. Commercial and residential rooftop installations continue generating substantial demand for roof hooks, clamps, and low-penetration fastening systems. Industrial retrofit projects are also contributing to market growth as companies seek to reduce energy costs and improve sustainability performance.

The market emphasizes high-quality fastening products capable of supporting long-term rooftop reliability under varying weather conditions. German manufacturers remain highly competitive in engineered mounting and fastening technologies designed for modular and prefabricated solar systems.

Spain Solar Fasteners Market Trends

Spain is experiencing strong growth in utility-scale solar projects due to favorable solar irradiation conditions and continued renewable energy investments. Large ground-mounted solar farms are increasing demand for structural fastening systems, anchors, and corrosion-resistant mounting hardware. The country is also expanding commercial rooftop solar adoption across logistics centers and industrial facilities.

U.K. Solar Fasteners Market Trends

The U.K. continues to witness rising rooftop solar adoption across residential, commercial, and public infrastructure projects. Demand for roof-preserving fastening systems is increasing due to retrofit activity and growing emphasis on building-integrated renewable energy solutions. Regulatory focus on sustainable construction practices is further supporting demand for certified mounting hardware.

Asia Pacific Solar Fasteners Market Trends

Asia Pacific is both the largest and fastest-growing regional market, accounting for approximately 56.3% of the market share. The region benefits from large-scale solar deployment, strong manufacturing capabilities, supportive government policies, and rapidly expanding renewable energy infrastructure.

China Solar Fasteners Market Trends

China remains the largest solar market globally and continues to dominate utility-scale solar deployment and solar component manufacturing. Massive solar farm developments and expanding distributed solar installations are creating substantial demand for mounting structures, standardized fasteners, anchors, and roof attachment systems. Domestic manufacturing advantages and large-scale production capabilities also support competitive pricing across the regional supply chain.

The market increasingly favors modular mounting systems and standardized metric fasteners that improve installation speed and compatibility with utility-scale projects.

India Solar Fasteners Market Trends

India is emerging as one of the fastest-growing markets due to rapid expansion across rooftop, agricultural, commercial, and utility-scale solar sectors. Government initiatives supporting domestic renewable energy deployment and localization policies are strengthening demand for locally manufactured fastening systems and mounting hardware.

Commercial rooftop installations, warehouse solar systems, and agricultural solar projects are significantly increasing demand for corrosion-resistant fasteners, roof hooks, and low-penetration mounting systems. The country’s expanding industrial infrastructure and rising energy consumption continue to support long-term market growth.

Japan Solar Fasteners Market Trends

Japan continues to invest in high-performance rooftop solar systems designed for urban environments with limited installation space. Demand for lightweight, earthquake-resistant, and corrosion-resistant fastening systems is particularly strong due to stringent structural safety standards and coastal environmental conditions.

Competitive Landscape

The global solar fasteners market is moderately fragmented, with competition distributed across global fastening manufacturers, solar mounting specialists, and regional construction hardware suppliers. Competitive intensity is particularly strong in standardized fastening products, while higher-margin opportunities exist in certified, application-specific, and integrated mounting solutions.

Leading companies are prioritizing innovation, certification, localization, and installation efficiency. Market leaders continue investing in modular mounting technologies, corrosion-resistant materials, digital design tools, and application-specific fastening systems. Geographic expansion, strategic partnerships, and integration with broader solar mounting ecosystems remain key competitive strategies.

Key Industry Developments:

- In March 2026, Schletter Group announced the completion of a 96 MWp ground-mounted solar project in Italy in partnership with EnValue Solar, strengthening its position in Europe’s large-scale solar infrastructure segment through advanced structural mounting and fastening systems.

- In April 2026, Fischer Group launched the FSIS Solar Inverter Shelter, a new outdoor installation solution for photovoltaic inverters designed for flat roofs, PV façades, industrial carports, and ground-mounted systems, addressing increasing demand for fire-safe and space-efficient solar infrastructure installations.

Companies Covered in Solar Fasteners Market

- Würth Group

- EJOT

- fischer Group

- Schletter Group

- K2 Systems

- Unirac

- Esdec

- Renusol

- Clenergy

- SFS Group

- S-5!

- novotegra

- Roof Tech Inc.

- SunModo

- Van der Valk Solar Systems

- Mounting Systems GmbH

Frequently Asked Questions

The global solar fasteners market is anticipated to be valued at US$4.1 billion in 2026.

The solar fasteners market is projected to reach approximately US$7.5 billion by 2033.

The solar fasteners market is projected to grow at a CAGR of 9.0% between 2026 and 2033.

Key trends include increasing adoption of modular mounting systems, growing demand for corrosion-resistant stainless steel fasteners, rising rooftop solar installations, and greater use of standardized metric fastening systems in utility-scale projects.

Fastening sets for metal roofs are the leading product segment, holding an anticipated 34.5% market share in 2026 due to strong demand from commercial and industrial rooftop solar projects.

Major companies include Würth Group, EJOT, fischer Group, Schletter Group, and K2 Systems.