- Beverages

- Shea Butter Market

Shea Butter Market Size, Share, and Growth Forecast 2026 - 2033

Shea Butter Market by Product Type (Raw Shea Butter, Refined Shea Butter), by Application (Cosmetics & Personal Care, Food Industry, Pharmaceuticals), Form (Solid, Liquid), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Shea Butter Market Size and Trend Analysis

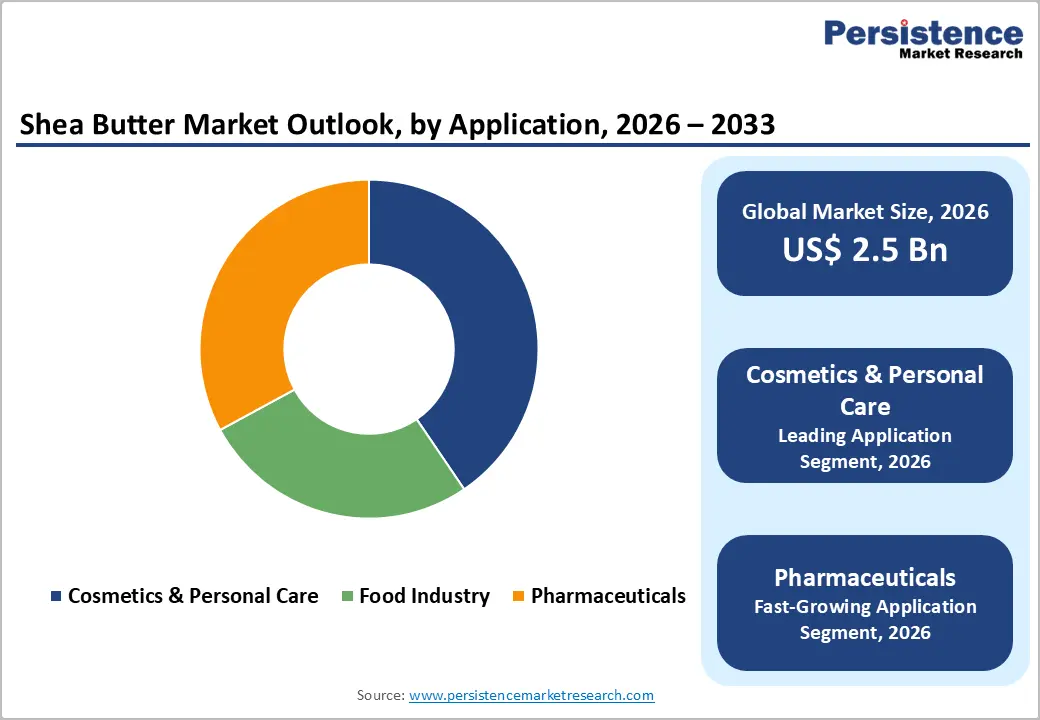

The global shea butter market size is expected to be valued at US$ 2.5 billion in 2026 and projected to reach US$ 4.4 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033. This reflects a shift toward naturally derived, multifunctional ingredients in skincare formulations. Parallel demand from the food industry, where shea stearin serves as a cocoa butter equivalent, and from pharmaceutical-grade emollient applications reinforces the market's multi-vertical momentum.

Key Industry Highlights:

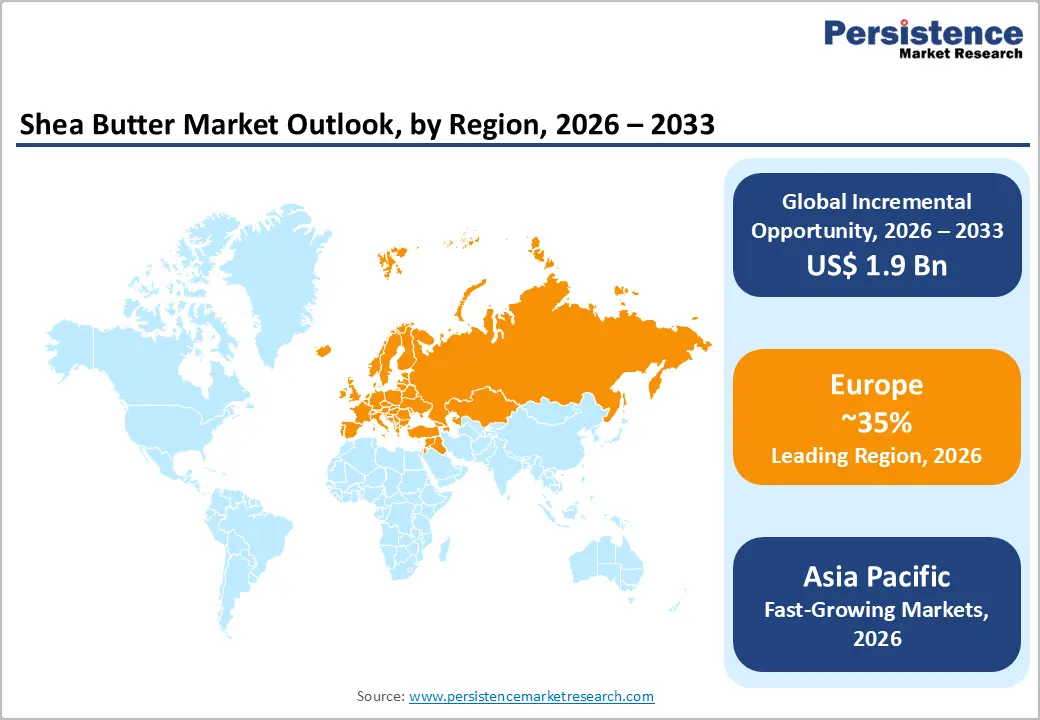

- Leading Region: Europe leads the global Shea Butter market with approximately 35% of total revenue, supported by strict EU cosmetics legislation favouring natural-origin ingredients and deep confectionery sector demand for shea-based cocoa butter equivalents.

- Leading Category: Refined Shea Butter dominates the product type segmentation with a 72.0% market share, driven by its fit with industrial-scale cosmetic and food formulation requirements and cost-efficient integration into high-volume automated manufacturing processes.

- Fastest Growing Region: Asia Pacific is the fast-growing market, projected to compound above the global average, driven by premiumising skincare markets in China, Japan, South Korea, and India where K-beauty adoption is accelerating.

- Fastest Growing Application Category: Pharmaceuticals is the fastest-growing application segment, expanding on the catalyst of clinical evidence for shea butter's anti-inflammatory and emollient efficacy and active pipeline development by dermatology-focused pharmaceutical manufacturers.

- Key Opportunity: Clean-label premiumisation creates a high-value opportunity for certified, unrefined shea butter in direct-to-consumer personal care, with fair-trade and organic credentials capturing 20-40% price premiums under tightening EU CSRD disclosure obligations.

Market Dynamics

Drivers - Rising Consumer Demand for Natural and Organic Personal Care Ingredients

The single most decisive growth catalyst in the Shea Butter market is the accelerating consumer pivot toward clean-label, plant-derived cosmetic ingredients. Formulators across skincare, haircare, and lip care are actively replacing synthetic emollients with shea butter due to its superior fatty acid profile, particularly its high oleic and stearic acid content, which delivers clinically demonstrable moisturisation benefits across diverse skin types and climatic conditions.

According to the Organic Trade Association, the global organic personal care segment has been expanding at rates exceeding 9% annually, pulling certified organic shea butter procurement volumes with it. Brand-level commitments by majors such as L'Oréal, Unilever, and Beiersdorf to raise natural ingredient thresholds above 95% in flagship moisturiser lines have translated directly into long-term offtake agreements with shea butter processors.

Expanding Application Base in the Food and Confectionery Sector

Shea butter's role as a cocoa butter equivalent in chocolate and confectionery manufacturing is generating a structurally durable second demand pillar for the shea butter industry. Processors fractionate shea butter into its stearin and olein components, producing ingredients that satisfy EU Directive 2000/36/EC, which permits up to 5% vegetable fat substitution in chocolate products sold across European markets, reinforcing shea stearin's commercial relevance.

This regulatory allowance has made shea stearin the preferred cocoa butter alternative among mid-market confectionery producers managing cocoa price volatility, which reached historic highs above US$ 10,000 per metric tonne in 2024 according to the International Cocoa Organization (ICCO). Food-grade shea butter is expanding particularly fast in Europe and East Asia, where confectionery consumption is high and cocoa supply constraints remain acute.

Restraints - Supply Chain Concentration and Seasonal Production Volatility

The shea butter market faces a structurally embedded supply risk because commercial production remains geographically concentrated in a narrow West African belt spanning Ghana, Burkina Faso, Mali, Nigeria, and Côte d'Ivoire, which collectively account for over 80% of global raw shea nut supply according to the Food and Agriculture Organization (FAO). Shea trees require 20 to 50 years to reach full nut-bearing maturity, making rapid supply expansion structurally impossible.

Field data from agricultural development organisations operating in the Sahel region, including the United Nations Development Programme (UNDP), indicates that seasonal rainfall variability and increasingly erratic weather patterns linked to climate change introduce year-on-year yield fluctuations of up to 30%. This volatility creates procurement uncertainty for downstream formulators and triggers pricing spikes that compress margins across the entire value chain.

Adulteration and Quality Inconsistency Undermining Brand Trust

A persistent quality-assurance challenge restrains volume growth in the premium shea butter sector, particularly in refined and certified-grade supply chains. Adulteration with lower-cost vegetable fats including palm olein and soybean oil is documented in spot-market procurement, eroding buyer confidence and forcing brands to invest in third-party verification programmes to safeguard formulation integrity and consumer trust.

Regulatory bodies including the European Food Safety Authority (EFSA) and the US Food and Drug Administration (FDA) enforce strict composition standards, meaning non-compliant shipments face rejection and costly reformulation delays. Smaller formulators lacking the procurement infrastructure to maintain verified supply chains face competitive disadvantages relative to large multinationals with dedicated shea sourcing teams, constraining mid-market entry and growth.

Opportunities - Premiumisation of Unrefined and Ethically Sourced Shea Butter for Direct-to-Consumer Brands

The fast-moving commercial opportunity in the shea butter market lies at the intersection of premiumisation and ethical sourcing, specifically the positioning of unrefined, women-cooperative-sourced shea butter as a hero ingredient in direct-to-consumer personal care brands. According to the International Trade Centre (ITC), consumers in North America and Europe are willing to pay a 20-40% price premium for shea butter products carrying fair-trade, organic, or Rainforest Alliance certification.

Industry participants should prioritise direct partnerships with certified cooperatives in Ghana and Burkina Faso, including organisations such as the Katakyie Women's Cooperative and peer networks under the Global Shea Alliance umbrella, to lock in differentiated supply. Brands investing in transparent supply-chain storytelling now will build defensible positioning as disclosure requirements tighten under the EU Corporate Sustainability Reporting Directive (CSRD).

Growth of Pharmaceutical-Grade Shea Butter in Topical Drug Delivery and Dermatology

The pharmaceutical application segment represents the highest-growth, underserved opportunity in the broader shea butter industry, and participants with purification and fractionation capabilities are best positioned to capture it. Pharmaceutical-grade shea butter functions as an effective excipient in topical formulations for conditions including eczema, psoriasis, and wound healing, with its triterpene alcohol content demonstrating measurable anti-inflammatory efficacy in peer-reviewed dermatology research indexed by PubMed.

Regulatory harmonisation across International Council for Harmonisation (ICH) member markets is streamlining the approval pathway for plant-derived excipients, reducing time-to-market for pharmaceutical manufacturers. Companies investing in GMP-certified processing capacity and excipient-grade documentation will gain structural advantages as dermatology-focused pharmaceutical pipelines turn to botanical actives, with pharmaceutical applications emerging as the fast-growing segment.

Category-wise Analysis

Product Type Insights

Refined Shea Butter accounts for 72.0% of the global market in 2026, equivalent to US$ 1.73 billion, making it the structurally dominant product type. Refined shea butter leads because large-scale industrial buyers in cosmetics and food manufacturing require standardised, odour-neutral, consistent-quality ingredients that integrate seamlessly into automated formulation lines, with over 65% of global procurement by multinational personal care manufacturers specifying refined or ultra-refined grades.

Raw Shea Butter represents the fast-growing segment, accelerating on the back of the clean-beauty movement and rising consumer demand for minimally processed, nutrient-intact ingredients in artisanal and premium personal care products. As certified-unrefined supply chains mature and direct-to-consumer brands scale their volumes, the raw segment signals a potential structural rebalancing within the shea butter market share landscape toward the end of the forecast period.

Application Insights

Cosmetics & personal care accounts for 53.0% of the global Shea Butter market in 2026, equivalent to US$ 1.27 Billion, establishing it as the dominant application segment by a decisive margin. The segment leads because shea butter's unique composition combining high levels of stearic and oleic fatty acids with vitamins A, E, and F makes it one of the most functionally versatile ingredients available to cosmetic formulators at commercially viable price points.

Pharmaceuticals is the fastest-growing application segment, driven by escalating clinical validation of shea butter's anti-inflammatory and wound-healing properties, alongside increasing regulatory acceptance of botanical excipients in topical drug delivery systems. Formulators and ingredient distributors should consider building dual-channel capability serving both personal care and pharmaceutical customers to capture incremental revenue from the fastest-expanding application pockets within the broader shea butter market opportunity space.

Form Insights

Solid Shea Butter accounts for 88.0% of the global market in 2026, equivalent to US$ 2.11 Billion, representing an overwhelming structural majority within the shea butter market by form. Solid form dominates because shea butter's natural melting point of approximately 37°C means it exists as a stable, easily handled solid at ambient temperatures across most global markets, making it the default commercial format for bulk B2B trade and retail packaging.

Liquid Shea Butter, also known as shea oil or olein, is the fastest-growing form, gaining traction in premium hair care, carrier oil blending, and spray-format personal care products where its lightweight, easily absorbed texture creates a superior consumer experience versus solid grades. Ingredient processors developing liquid shea butter capability alongside their core solid operations will capture value from two distinct demand streams without cannibalising existing customer relationships across mainstream cosmetic manufacturing channels.

Distribution Channel Insights

B2B distribution accounts for 89.0% of the global Shea Butter market in 2026, equivalent to US$ 2.14 Billion, reflecting the market's fundamental character as an ingredient-driven, industrial-supply sector. B2B channel dominance is structural, with the top 10 global personal care manufacturers collectively purchasing in excess of 200,000 metric tonnes of shea butter annually, representing volumes that can only be served through dedicated B2B procurement infrastructure and direct supply agreements.

B2C is the fastest-growing distribution channel, driven by the proliferation of direct-to-consumer natural beauty brands, e-commerce platforms, and rising consumer awareness of shea butter's benefits, which has created a thriving retail market for both raw and finished shea butter products. Industry participants across the value chain should develop B2C-compatible packaging, certification, and storytelling capabilities to participate in the channel with the most dynamic structural growth trajectory.

Regional Insights

North America Shea Butter Market Trends and Insights

North America represents a substantial consumer market driven by strong demand for organic and clean-label personal care products. According to the Organic Trade Association, U.S. consumer spending on natural beauty products has grown steadily, with shea butter featuring prominently in moisturizers, body butters, and hair care lines. Vegan and cruelty-free product launches further accelerate regional adoption.

- U.S. Shea Butter Market Size

The United States accounts for nearly 80% of North America's shea butter consumption, making it the dominant national market in the region. According to the U.S. Department of Commerce, imports of shea-based products have risen consistently as multicultural beauty brands and mainstream FMCG players expand natural product portfolios. Strong DTC e-commerce penetration and rising demand for textured hair care formulations underpin steady market growth.

Europe Shea Butter Market Trends and Insights

Europe leads the global shea butter market with approximately 35% market share in 2025, anchored by mature cosmetics manufacturing hubs and stringent natural ingredient regulations. The European Commission's Cosmetic Products Regulation favors plant-derived emollients, while the EU Organic Regulation drives certified shea butter consumption. Strong consumer preference for sustainable and ethically sourced ingredients reinforces regional dominance.

- Germany Shea Butter Market Size

Germany commands roughly 22% of the European shea butter market, driven by its position as the continent's largest cosmetics manufacturing base. According to Destatis (Federal Statistical Office of Germany), the country's natural cosmetics segment continues to expand robustly, with brands like Beiersdorf AG and Weleda AG integrating shea butter into flagship product lines. Strong organic certification standards reinforce demand.

- U.K. Shea Butter Market Size

The United Kingdom holds approximately 18% of Europe's shea butter market, supported by strong demand for ethical beauty and Afro-Caribbean haircare products. According to the UK Office for National Statistics, natural personal care consumption has grown steadily, with retailers including The Body Shop and Lush prominently featuring shea butter formulations. ESG-driven sourcing commitments continue to drive premium-grade demand.

- France Shea Butter Market Size

France accounts for nearly 20% of Europe's shea butter market, leveraging its global cosmetics leadership through brands like L'Oréal, Clarins, and L'Occitane en Provence, the latter being a flagship shea butter ambassador. According to INSEE, French organic cosmetics sales continue rising, while strong pharmacy-channel skincare distribution drives consistent growth across mass and premium tiers.

Asia Pacific Shea Butter Market Trends and Insights

Asia Pacific is the fast-growing region in the shea butter market between 2025 and 2032, driven by rising disposable incomes, expanding middle-class consumption, and rapid premiumization of personal care categories. China's natural cosmetics market is expanding strongly, supported by NMPA (National Medical Products Administration) approvals for plant-based ingredients. Increasing K-beauty and J-beauty influence further accelerates shea adoption.

- India Shea Butter Market Size

India represents one of the fastest-growing national markets within Asia Pacific, holding approximately 14% regional share. According to the India Brand Equity Foundation (IBEF), the Indian beauty and personal care sector is expanding rapidly, with shea butter increasingly featured in domestic ayurvedic-natural hybrid formulations. Rising e-commerce penetration through platforms like Nykaa further accelerates premium shea-based product adoption.

- Japan Shea Butter Market Size

Japan accounts for nearly 18% of Asia Pacific's shea butter market, driven by sophisticated J-beauty formulations emphasizing skin barrier nourishment. According to the Japan Cosmetic Industry Association, demand for natural emollients has been consistently rising. Premium positioning by domestic brands such as Shiseido and Kao Corporation reinforces Japan's strategic relevance, while aging demographics drive continued moisturizer category expansion.

- Southeast Asia Shea Butter Market Size

Southeast Asia represents approximately 16% of Asia Pacific's shea butter market, with Thailand, Indonesia, and Vietnam leading consumption. According to the ASEAN Cosmetics Association, the regional natural cosmetics market is expanding rapidly, supported by tropical climate-driven moisturizer demand. Rising halal-certified beauty product launches in Indonesia and Malaysia markets validated by JAKIM and MUI accelerate shea butter adoption across emerging consumer segments.

Competitive Landscape

The Shea Butter market operates as a moderately fragmented competitive landscape, stratified across three distinct tiers. Large-scale, vertically integrated multinationals compete on processing scale, supply-chain security, and the ability to deliver certified, specification-consistent product at global volumes, while mid-tier regional processors and specialty ingredient distributors differentiate through certification credentials, origin transparency, and flexible minimum order quantities.

A fragmented base of artisanal and cooperative-linked suppliers serves the premium direct-to-consumer and natural beauty segments, competing on authenticity and ethical sourcing narratives. The dominant strategic themes shaping the competitive landscape include vertical integration into West African sourcing, sustainability certification acquisition, and application-specific product development targeting pharmaceutical and food-grade demand pools.

Key Developments:

- In March 2025, AAK AB announced an expanded long-term sourcing agreement with women's shea cooperatives across Ghana and Burkina Faso, committing to purchase 50,000 additional metric tonnes annually by 2027 under its certified sustainable shea programme, reinforcing its supply-chain differentiation strategy.

- In November 2024, Croda International launched a new pharmaceutical-grade shea butter excipient line under its Crodamol platform, targeting topical drug delivery formulators in the EU and US markets and signalling the company's strategic entry into the fast-growing pharmaceutical application segment.

- In January 2025, Cargill completed capacity expansion at its shea processing facility in Tema, Ghana, increasing annual refined shea butter output by 35%, positioning the company to meet rising demand from European confectionery and personal care manufacturers amid ongoing cocoa price volatility.

Shea Butter Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.54 Billion |

| Current Market Value (2026) | US$ 2.5 Billion |

| Projected Market Value (2033) | US$ 4.4 Billion |

| CAGR (2026 - 2033) | 8.4% |

| Leading Region | Europe (35%) |

| Dominant Product Type | Refined Shea Butter (72.0%) |

| Top-ranking Application | Cosmetics & Personal Care (53.0%) |

| Top-ranking Form | Solid (88.0%) |

| Top-ranking Distribution Channel | B2B (89.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 1.82 Billion |

Companies Covered in Shea Butter Market

- BASF

- AAK AB

- Croda International

- Bunge Loders Croklaan

- Clariant

- Cargill

- Ghana Nuts Company

- Shea Radiance

- The Savannah Fruits Company

- IOI Loders Croklaan

- Akoma Cooperative

- Star Shea Ltd

- Jedwards International

- Sophim

- Fuji Oil

- Olvea Group

- Agrobotanicals LLC

- Global Shea Alliance (member processors)

- Timiniya Tuma Company

- Yacoubou Issoufou et Frères (YIF)

- Agri Resources Group

- Natural Sourcing LLC

Frequently Asked Questions

The global Shea Butter market is valued at US$ 2.5 Billion in 2026 and projected to reach US$ 4.4 Billion by 2033, expanding at 8.4% CAGR.

Growth is driven by accelerating consumer demand for clean-label, plant-derived cosmetic ingredients and expanding use of shea stearin as a cocoa butter equivalent in European confectionery manufacturing.

Refined Shea Butter holds 72.0% share in 2026, driven by industrial buyers' need for odour-neutral, specification-consistent ingredients that integrate reliably into automated cosmetic and food production lines.

Europe dominates with approximately 35% revenue share, supported by a well-capitalised personal care manufacturing base and deep confectionery sector demand for shea stearin under EU cosmetic regulations.

Pharmaceutical-grade shea butter excipients for topical drug delivery present the most actionable opportunity, supported by advancing clinical validation and ICH-aligned regulatory harmonisation shortening approval timelines.

The leading companies in the Shea Butter market include AAK AB, Cargill, Croda International, Bunge Loders Croklaan, BASF, Clariant, Ghana Nuts Company, and The Savannah Fruits Company.