- Beverages

- Probiotic Drink Market

Probiotic Drink Market Size, Share, and Growth Forecast 2026 - 2033

Probiotic Drink Market by Product Type (Dairy-Based, Non-Dairy-Based), Nature (Organic, Conventional), by Packaging Type (Bottles, Pouches, Cartons, Cans), Sales Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Health Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Probiotic Drink Market Size and Trend Analysis

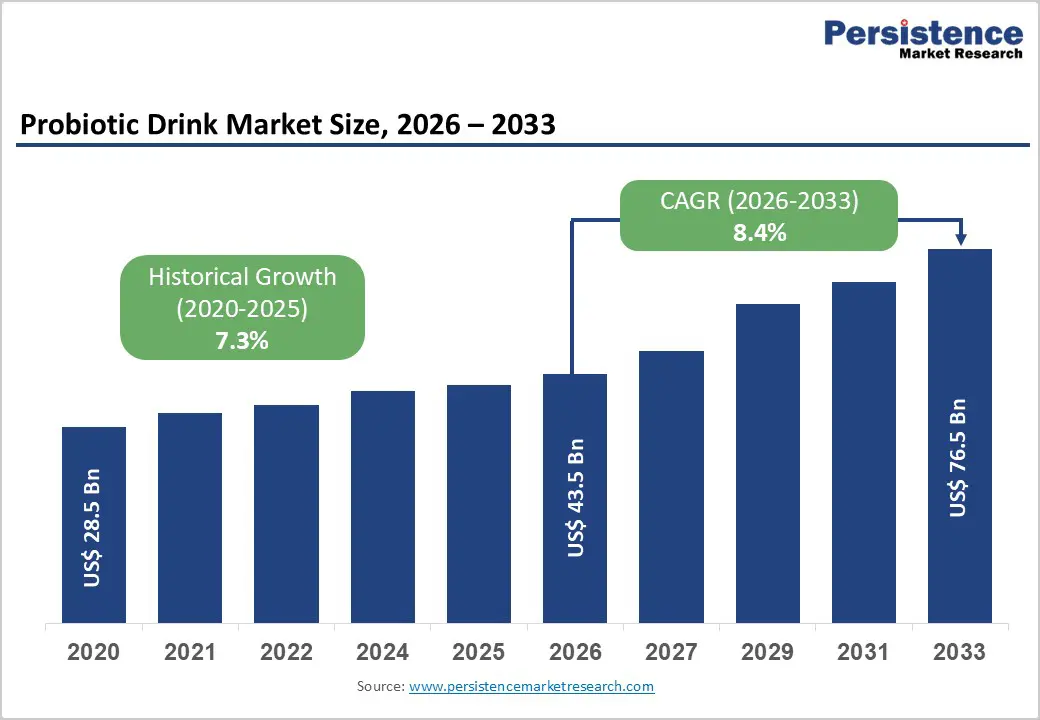

The global probiotic drink market size is expected to be valued at US$ 43.5 billion in 2026 and projected to reach US$ 76.5 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033. It is experiencing robust growth, primarily driven by heightened global consumer awareness of gut health and its far-reaching implications for immunity, mental wellness, and metabolic health. The World Health Organization (WHO) defines probiotics as live microorganisms that confer health benefits when administered in adequate amounts.

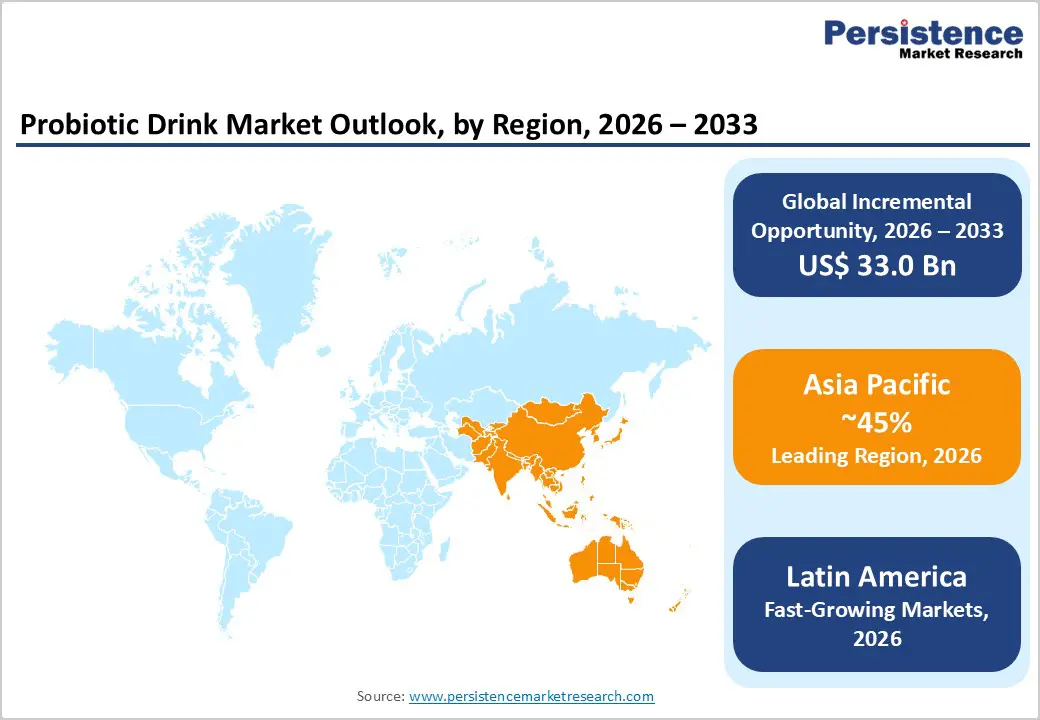

The rising incidences of gastrointestinal disorders, compounded by post-pandemic consumer prioritization of preventive healthcare, are accelerating product adoption across demographic segments. Asia Pacific continues to lead global consumption, accounting for approximately 45% of market revenue in 2025, while premiumization and plant-based innovation are reshaping product portfolios in North America and Europe.

Key Industry Highlights

- Regional Leadership: Asia Pacific leads the global probiotic drink market with approximately 45% revenue share in 2025, anchored by Japan's Yakult brand dominance, China's expanding middle class, and deeply rooted fermented beverage consumption traditions across the region.

- Fast-growing Market: Latin America is the fastest-growing regional market through 2033, fueled by rising health awareness, expanding urban retail infrastructure, and growing middle-class demand for functional beverages across Brazil, Mexico, and Colombia.

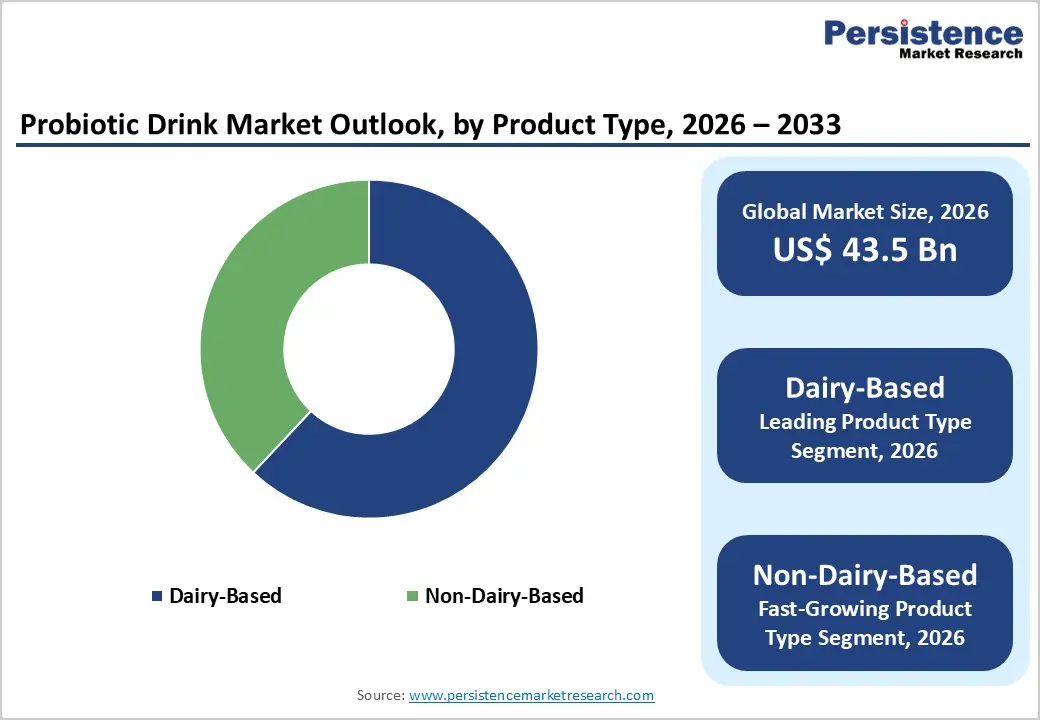

- Fast-growing Product: Dairy-based probiotic drinks dominate the market with approximately 62% product type share in 2025, sustained by consumer familiarity, clinical credibility of fermented dairy cultures, and the established distribution infrastructure of leading brands, including Yakult and Danone Actimel.

- Non-dairy probiotic drinks represent the fastest-growing product type segment, driven by plant-based dietary adoption, lactose intolerance prevalence, and innovation in kombucha, water kefir, and oat-based fermented beverage formulations targeting vegan and flexitarian consumers.

- Online retail represents the highest-potential channel opportunity, enabling premium-priced subscription models, personalized nutrition positioning, and direct consumer relationships that deliver 20–30% pricing premiums versus conventional trade for health-focused probiotic brands.

Market Dynamics

Drivers - Surging Gut Health Awareness and Preventive Healthcare Adoption

The global consumer pivot toward preventive nutrition, a behavioral shift that has converted gut health from a niche wellness concern, fuels the need for probiotic drinks. Scientific evidence linking the gut microbiome to immunity, mental health via the gut-brain axis, and chronic disease prevention has reached popular media, dramatically expanding consumer motivation beyond traditional digestive health applications.

A 2022 International Food Information Council (IFIC) Food and Health Survey found that 39% of U.S. consumers actively seek out probiotics in food and beverages, up significantly from prior years. Post-COVID-19, immunity-linked food products have seen sustained demand elevation, with major retailers globally reporting double-digit volume growth in functional beverages.

The proliferation of clinical publications validating probiotic strains such as Lactobacillus acidophilus and Bifidobacterium lactis for specific health outcomes is providing marketers with credible, evidence-based positioning, further accelerating mainstream adoption and premiumization across both dairy and non-dairy product formats.

Restraints - Regulatory Complexity and Inconsistent Health Claim Standards Across Markets

The lack of regulatory harmonization across key geographies creates significant market access complexity and constrains the ability of brands to standardize global messaging. In the European Union, the European Food Safety Authority (EFSA) has rejected the vast majority of submitted probiotic health claims. The U.S. Food and Drug Administration (FDA) similarly requires rigorous substantiation for structure/function claims. This regulatory asymmetry forces companies to maintain distinct labeling and marketing strategies across regions, adding product development cost and limiting the speed of international market rollout for innovative formulations.

Opportunities - Expansion of Online Retail and Direct-to-Consumer Probiotic Beverage Channels

The accelerating shift to e-commerce in food and beverage represents a structurally transformative distribution opportunity for probiotic drink brands, particularly those targeting health-conscious premium consumers who over-index on digital purchasing behavior. Statista reported that global online food and beverage sales surpassed US$ 300 billion in 2023, with functional and health-focused products among the highest-growth sub-categories.

The direct-to-consumer model enables brands to sidestep cold chain retail cost pressures through subscription-model temperature-controlled delivery while building proprietary first-party consumer data. Companies like Lifeway Foods and emerging DTC kombucha brands have demonstrated that subscription-based probiotic beverage delivery commands 20–30% price premiums versus mass retail channels. Brands investing in digital marketing capabilities, personalized nutrition positioning, and seamless last-mile delivery infrastructure are well-positioned to capture this high-margin, fast-growing channel that remains underpenetrated relative to its long-term structural potential.

Category-wise Analysis

Product Type Insights

Dairy-based probiotic drinks command approximately 62% of the global probiotic drink market by product type in 2025, a position grounded in deep cultural consumption habits, established retail infrastructure, and the superior bioavailability of live cultures in dairy fermentation matrices. Products such as kefir, fermented milk drinks, and dairy-based yogurt beverages led by Yakult Honsha's globally recognized Yakult and Danone's Actimel range have decades of consumer trust and clinical validation behind them.

The International Dairy Federation (IDF) notes that fermented dairy products remain the most widely consumed probiotic food format globally. However, the segment faces competitive pressure from non-dairy alternatives, and its share is expected to gradually compress as plant-based formulations improve in strain viability, taste profile, and distribution reach through the forecast period.

Nature Insights

Conventional probiotic drinks retain approximately 72% of market share by nature in 2025, driven by mass-market pricing accessibility and established manufacturing ecosystems that support high-volume production at scale. The conventional segment benefits from the broad retail footprint of major FMCG players including Danone, Nestlé, and Yakult Honsha, which leverage cost-optimized fermentation and distribution networks to sustain high-volume turnover across hypermarkets and convenience stores globally. That said, organic probiotic drinks represent the fastest-growing nature segment, with accelerating demand from premium retail channels and online platforms particularly in North America and Western Europe. The Organic Trade Association confirms the organic functional beverage category is outpacing conventional growth rates, signaling a gradual but structural share shift over the forecast horizon.

Regional Insights

Asia Pacific Probiotic Drink Market Trends and Insights

Asia Pacific dominates the probiotic drink market, accounting for ~35–40% share globally, supported by strong cultural consumption of fermented beverages and large population base. Countries such as Japan, China, and India drive demand due to rising health awareness and urbanization. The region is projected to remain dominant with expanding functional beverage adoption and increasing disposable incomes.

- Japan Probiotic Drink Market Trends and Insights

Japan leads the regional market due to its long-standing probiotic culture and strong brand presence like Yakult. It is expected to reach ~US$ 9–10 Bn by 2027, driven by high per capita consumption of functional drinks and aging population demand for digestive health. Government-supported nutrition awareness and widespread retail penetration further strengthen growth. Japan also exhibits innovative steadiness for probiotic formulations and delivery formats.

- China Probiotic Drink Market Trends and Insights

China is the fast-growing market, expected to reach ~10% CAGR, supported by rapid urbanization and rising middle-class spending. Increasing awareness of gut health, expansion of e-commerce, and strong domestic production are key drivers. The country has witnessed rise in probiotic consumption, supported by government health initiatives and rising demand for functional foods among younger consumers.

North America Probiotic Drink Market Trends and Insights

North America holds a significant share of ~30% globally, driven by strong consumer awareness of gut health and a mature functional beverage industry. High disposable income and innovation in plant-based probiotic drinks further support market growth. The region is also a trendsetter in premium and clean-label probiotic beverages.

- U.S. Probiotic Drink Market Trends and Insights

The U.S. is a dominant region and is expected to reach ~US$ 14 billion by 2026, supported by high consumption of functional beverages and widespread retail availability. Over 9.1 billion units of probiotic drinks were consumed in 2023, reflecting strong demand. Increasing focus on immunity, digestive health, and personalized nutrition continues to drive growth across multiple demographic segments.

- Canada Probiotic Drink Market Trends and Insights

Canada is the fastest growing country in the region, expected to grow at ~8–9% CAGR, driven by rising demand for plant-based and lactose-free probiotic drinks. Increasing health-conscious consumers and government-backed nutrition awareness programs are key growth drivers. Expansion of organic and clean-label products is further accelerating adoption.

Latin America Probiotic Drink Market Trends and Insights

Latin America is the fastest growing region, with a projected ~8.5% CAGR, driven by increasing health awareness and rising disposable incomes. Although it currently holds a smaller share, rapid urbanization and expanding retail distribution are fueling strong growth across the region.

- Brazil Probiotic Drink Market Trends and Insights

Brazil leads the region and is expected to reach ~US$ 80 million by 2027, accounting for a major share of regional sales. It is also the fastest growing country, projected to grow at ~8.5% CAGR, supported by increasing middle-class population and growing demand for functional beverages. Rising awareness of digestive health, along with expanding supermarket and retail penetration, is driving strong adoption of probiotic drinks.

- Mexico Probiotic Drink Market Trends and Insights

Mexico is emerging as a key growth market, expected to grow at ~8% CAGR, driven by increasing urbanization and rising consumption of functional beverages. Government health initiatives addressing obesity and digestive health are encouraging probiotic adoption. Growing availability of affordable probiotic drinks and the expansion of distribution channels are further supporting market growth.

Competitive Landscape

The global probiotic drink market is moderately consolidated at the upper tier, with Yakult Honsha, Danone, and Nestlé collectively holding significant revenue concentration, while the mid and lower tiers remain highly fragmented with hundreds of regional and emerging brands.

Scale differentiators among market leaders include proprietary probiotic strain libraries, global cold chain distribution networks, and sustained investment in clinical substantiation. Strategic themes shaping the competitive environment include portfolio premiumization, plant-based product line extensions, and strategic acquisitions of high-growth kombucha and functional beverage startups. The DTC and subscription business model is emerging as a key competitive frontier, enabling challenger brands to build direct consumer relationships and achieve superior margins versus traditional trade channels.

Key Developments

- April, 2026: Bio-K+ announced the launch of its “Pain in the Gut” campaign, aimed at strengthening its positioning as a scientifically backed leader in the probiotic space. The campaign focused on raising awareness about gut health issues and educating consumers on the role of clinically validated probiotic strains in managing digestive discomfort.

- November, 2025: Danone announced that it had sold its probiotic juice brand ProViva to Lactalis as part of its portfolio optimization strategy. The divestment reflected Danone’s focus on strengthening its core segments, particularly dairy, plant-based products, and specialized nutrition.

Global Probiotic Drink Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 28.5 Billion |

|

Projected Market Value (2026) |

US$ 43.5 Billion |

|

Projected Market Value (2033) |

US$ 76.5 Billion |

|

CAGR (2026-2033) |

8.4% |

|

Leading Region |

Asia-Pacific, 45% share |

|

Dominant Product Type |

Dairy-Based, 62% share |

|

Top-ranking Nature |

Conventional, 81% share |

|

Incremental Opportunity |

US$ 33.0 billion |

Companies Covered in Probiotic Drink Market

- Yakult Honsha Co., Ltd.

- Danone

- Bio-K+

- PepsiCo

- Lifeway Foods, Inc.

- GoodBelly

- Mother Dairy Fruit & Vegetable Pvt. Ltd.

- Chobani, LLC.

- Nestlé

- Fonterra Co-operative Group

- Kirin Holdings Company, Limited

- General Mills, Inc.

- GCMMF (Amul)

- Others

Frequently Asked Questions

The global probiotic drink market is projected to reach US$ 43.5 billion in 2026.

Rising gut health awareness, functional beverages demand, lactose intolerance, immunity focus, urbanization, and premium health trends.

Asia Pacific leads the global probiotic drink market with approximately 45% revenue share in 2025.

Expansion of plant-based probiotic drinks targeting lactose-intolerant, vegan consumers across emerging markets globally.

Yakult Honsha Co., Ltd., Danone, Bio-K+, PepsiCo, Lifeway Foods, Inc., GoodBelly.