- Hardware & Software IT Services

- Shared Services Market

Shared Services Market Size, Share, and Growth Forecast, 2026 - 2033

Shared Services Market by Deployment Type (On-premises, Cloud), Application (CRM, F&A (Finance & Accounting), HR, IT, SCM), and Regional Analysis for 2026 - 2033

Shared Services Market Size and Trends Analysis

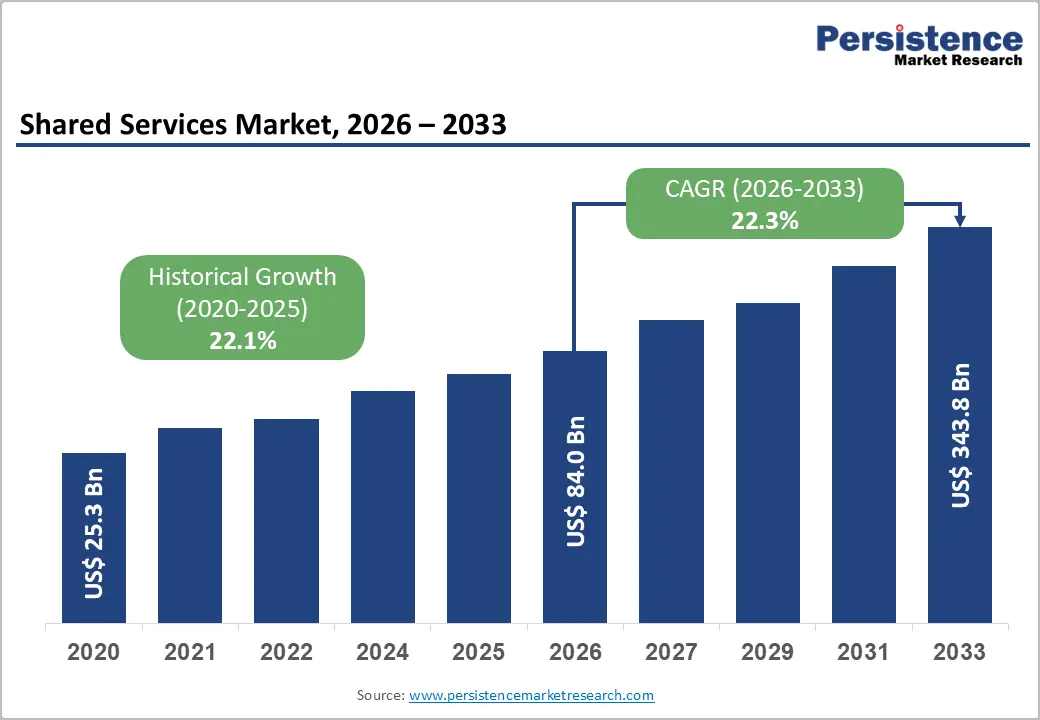

The global shared services market size is likely to be valued at US$84.0 billion in 2026 and is expected to reach US$343.8 billion by 2033, growing at a CAGR of 22.3% during the forecast period from 2026 to 2033, driven by enterprise-wide digital transformation and the shift toward global business services (GBS) models.

The adoption of advanced technologies such as automation, artificial intelligence, and cloud platforms is transforming shared services into agile and scalable operations. Industries including BFSI, manufacturing, and IT are leading adoption, while small and mid-sized enterprises are embracing outsourced and cloud-based models. This shift is positioning shared services as a critical enabler of digital transformation and long-term business value creation.

Key Industry Highlights:

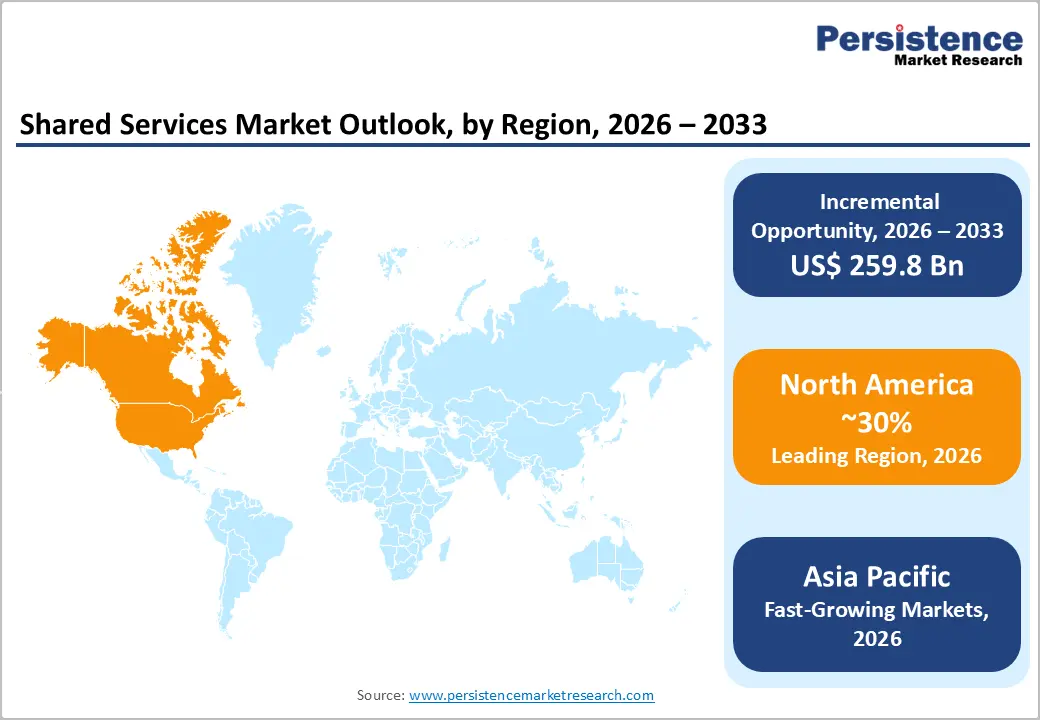

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 30% in 2026, driven by the strong presence of multinational corporations, advanced digital infrastructure, and mature outsourcing ecosystems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by strong GCC expansion, cost advantages, and a large skilled workforce.

- Leading Deployment Type: Cloud is projected to represent the leading deployment type in 2026, accounting for 60% of the revenue share, driven by its scalability, flexibility, and cost efficiency.

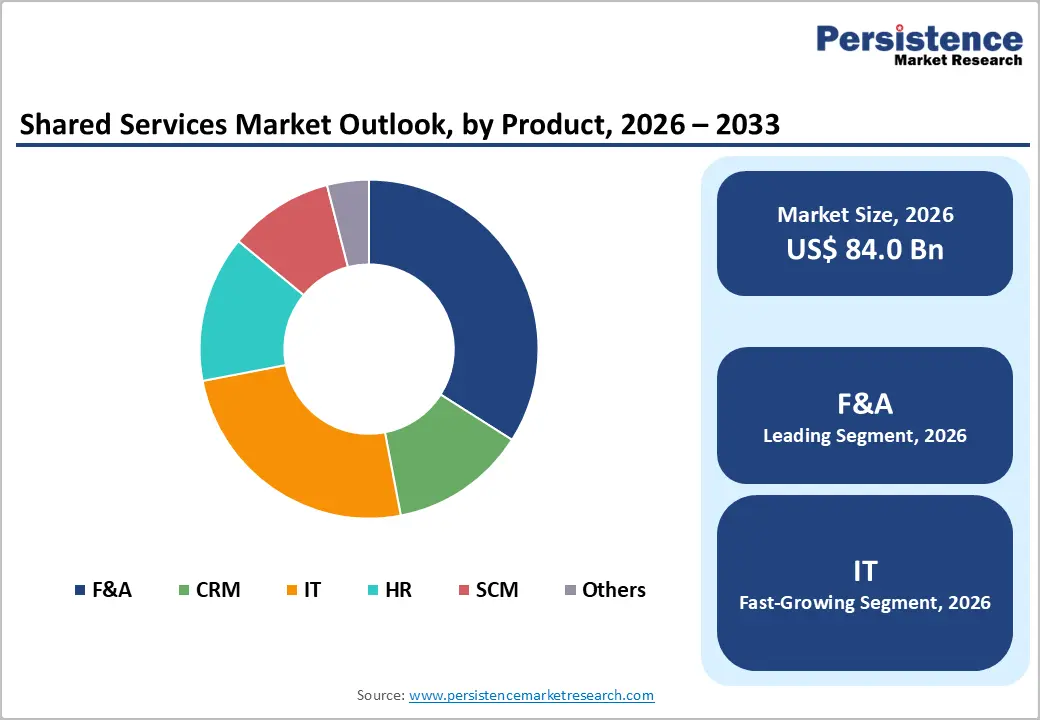

- Leading Application: Finance & accounting (F&A) is anticipated to be the leading application, accounting for over 35% of the revenue share in 2026, supported by its highly standardized and transaction-intensive nature.

- Key Opportunity: The key market opportunity is the transformation of traditional shared services into intelligent, integrated digital platforms using AI, cloud, and automation to deliver end-to-end business value and operational agility.

DRO Analysis

Driver Digitalization and Automation of Back-Office Functions

Functions, such as finance, HR, procurement, and IT, are increasingly being centralized and digitized using cloud platforms, robotic process automation, and artificial intelligence. These technologies reduce manual intervention, minimize errors, and accelerate processing times. As businesses expand, the need for standardized and scalable processes becomes critical, making shared services an ideal model to support seamless operations across multiple geographies and business units.

Automation is enhancing the value proposition of shared services by enabling real-time data processing, predictive analytics, and improved decision-making capabilities. Organizations are leveraging intelligent automation tools to handle repetitive, rule-based tasks, freeing up human resources for more strategic activities. The integration of digital tools allows shared services centers to evolve into strategic hubs that deliver insights and innovation.

Restraint - Organizational Resistance and Change-Management Challenges

Despite its advantages, the adoption of shared services often faces resistance from employees and management due to concerns about job displacement, loss of control, and changes in organizational structure. Transitioning from decentralized operations to a centralized shared services model requires significant cultural and operational adjustments. Employees may be hesitant to adopt new technologies or workflows, leading to delays and inefficiencies during implementation.

Change-management challenges also arise from the complexity of integrating diverse business units, legacy systems, and regional practices into a unified framework. Organizations must align processes, standardize workflows, and ensure compliance across multiple geographies, which can be both time-consuming and resource-intensive. Poorly managed transitions can disrupt business continuity and impact service quality.

Opportunity - AI- and Analytics-Driven Shared-Services Platforms

AI-powered platforms can analyze large volumes of data to generate actionable insights, improve forecasting accuracy, and enhance decision-making processes. Shared services centers are increasingly adopting machine learning algorithms, natural language processing, and intelligent automation to optimize workflows and deliver more personalized and efficient services across functions such as finance, HR, and customer support.

These advanced technologies are transforming shared services into strategic business partners that contribute to innovation and competitive advantage. Analytics-driven platforms enable real-time monitoring of performance metrics, identification of process inefficiencies, and proactive issue resolution. AI-enabled chatbots and virtual assistants are improving service delivery by providing faster and more accurate responses to user queries. As organizations continue to invest in digital transformation, the adoption of AI and analytics within shared services is accelerating, creating new growth opportunities and redefining the role of shared services in modern enterprises.

Category-wise Analysis

Deployment Type Insights

Cloud is expected to lead the shared services market, accounting for approximately 60% of revenue in 2026, as organizations prioritize flexibility, scalability, and cost efficiency in managing centralized operations. Cloud-based platforms enable enterprises to standardize processes across geographies while ensuring real-time accessibility and seamless integration with enterprise systems. Large enterprises and SMEs alike are increasingly shifting from legacy systems to cloud-enabled shared services to enhance operational agility. For instance, SAP SE provides cloud-based ERP and shared-services solutions that help organizations streamline finance, HR, and procurement functions.

Cloud is also likely to represent the fastest-growing segment, supported by increasing demand for digital transformation and real-time analytics capabilities. Organizations are adopting cloud platforms to support cross-border operations, improve collaboration, and enable data-driven decision-making. As businesses seek to modernize their operations, cloud deployment offers a future-ready solution that adapts to evolving organizational needs. A notable example includes Oracle Corp, which offers cloud-based shared services applications that enhance process efficiency and support business scalability.

Application Insights

The Finance & Accounting (F&A) segment is projected to lead the market, capturing around 35% of the revenue share in 2026, supported by its highly standardized, transaction-intensive, and compliance-driven processes. Organizations centralize functions such as accounts payable, payroll, and financial reporting within shared services centers to improve accuracy, reduce costs, and ensure regulatory compliance. For example, Genpact Ltd. delivers finance and accounting shared services that help enterprises optimize financial operations and enhance reporting efficiency.

The IT segment is likely to be the fastest-growing application, driven by increasing digital service demands and the need for continuous system support and innovation. IT shared services cover areas such as infrastructure management, helpdesk support, and application maintenance, all of which benefit from automation and cloud integration. A notable example includes ServiceNow Inc., which enables enterprises to manage IT services through integrated platforms that enhance efficiency, automation, and overall service performance.

Regional Insights

North America Shared Services Market Trends

North America is anticipated to be the leading region, accounting for a market share of 30% in 2026, driven by strong enterprise digitalization and outsourcing ecosystems. The U.S. leads in contributing nearly 70% of the regional adoption, due to its high concentration of multinational corporations, advanced cloud infrastructure, and increasing adoption of AI-enabled shared services. Canada is witnessing growth through the expansion of nearshore shared service hubs, accounting for approximately 20% of the share. While Mexico is emerging as a cost-efficient destination supported by nearshoring trends under USMCA. For instance, Infosys Ltd. has expanded delivery centers across the U.S. and Canada to strengthen digital shared services capabilities.

The region is also evolving rapidly with increasing integration of automation, analytics, and hybrid delivery models, positioning it as an innovation hub for shared services transformation. Mexico is gaining traction as a strategic hub for supply chain and customer support services due to lower operational costs and proximity to the U.S. market. A notable example includes Cognizant Technology Solutions Corp., which has expanded its North American operations to enhance digital, IT, and customer experience shared services across all three countries.

Europe Shared Services Market Trends

Europe is expected to remain a key market for shared services, expanding at a CAGR of approximately 16.9%, driven by the widespread adoption of centralized operating models and compliance-driven business frameworks. The U.K. dominates the region, accounting for nearly 35% of the market, supported by its robust financial ecosystem, a high concentration of multinational headquarters, and sustained foreign investment in digital and professional services, all of which are accelerating the adoption of shared services.

Germany accounts for approximately 30% of the regional market, supported by its strong manufacturing base and rising investment levels. France is progressing steadily, driven by government-backed digital transformation initiatives and robust demand from large enterprises. For instance, Capgemini plays a significant role in delivering shared services and digital transformation solutions across the U.K., Germany, and France.

Asia Pacific Shared Services Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rapid digital transformation and a large skilled workforce across key economies. China contributes nearly 40% of the regional market, driven by strong government-backed digitalization and service-sector expansion initiatives. Recent policy developments in China emphasize scaling the services economy and strengthening business services such as IT, logistics, and analytics, which directly support shared services growth.

India contributes around 30% of the regional market, fueled by the rapid expansion of Global Capability Centers (GCCs), strong IT outsourcing capabilities, and increasing enterprise demand for centralized operations. For example, Infosys Ltd. continues to expand shared services and digital delivery centers across India and Asia Pacific, supporting enterprises. Japan is accelerating adoption due to the need to modernize legacy IT systems and improve operational efficiency.

Competitive Landscape

The global shared services market exhibits a moderately fragmented structure, driven by the presence of multiple consulting firms, IT service providers, and specialized outsourcing companies competing across regions and industry verticals. The market is characterized by a mix of large multinational players and niche regional providers, creating a dynamic and competitive environment.

With key leaders including Accenture, IBM, Capgemini, Genpact, and Cognizant, the market demonstrates strong competition based on innovation and service integration. These players compete through advanced digital capabilities, including AI, robotic process automation, and cloud-based shared services platforms, along with strategic mergers, acquisitions, and partnerships to strengthen delivery networks.

Key Industry Developments:

- In March 2026, Cognizant Technology Solutions Corp. announced the launch of its AI Factory, a multi-tenant cloud-based platform designed to enable scalable and secure deployment of AI solutions across enterprise operations, enhancing automation and efficiency in business services.

- In October 2025, Infosys Ltd. collaborated with Telenor Shared Services to modernize HR operations by implementing a cloud-based Human Capital Management platform, aiming to standardize processes, improve employee experience, and enhance operational efficiency.

- In August 2025, Maersk launched a new shared service center in Warsaw, Poland, to support its European operations by delivering multilingual services and enhancing centralized business functions across the region.

Companies Covered in Shared Services Market

- Accenture PLC

- Atos SE

- Capgemini Services SAS

- CGI Inc.

- Cognizant Technology Solutions Corp.

- Deloitte Touche Tohmatsu Ltd.

- ExlService Holdings Inc.

- Gartner Inc.

- Genpact Ltd.

- HCL Technologies Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- KPMG International Ltd.

- Oracle Corp

- PricewaterhouseCoopers LLP

- SAP SE

- ServiceNow Inc.

Frequently Asked Questions

The global shared services market is projected to reach US$84.0 billion in 2026.

Cost reduction and digital transformation through cloud, automation, and AI are the key drivers of the shared services market.

The shared services market is expected to grow at a CAGR of 22.3% from 2026 to 2033.

Expansion of AI, cloud, and Global Capability Centers (GCCs), creating scalable and value-driven shared service models, is the key market opportunity.

Accenture PLC, Atos SE, Capgemini Services SAS, CGI Inc., Cognizant Technology Solutions Corp., and Deloitte Touche Tohmatsu Ltd. are the leading players.