- Hardware & Software IT Services

- Robotic Process Automation Market

Robotic Process Automation Market Size, Share, and Growth Forecast 2026 - 2033

Robotic Process Automation Market by Component Type (Software and Services), Deployment Model (Cloud-Based, On-Premises, Hybrid), Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs), Industry (BFSI, IT & Telecom, Retail & Consumer Goods, Healthcare & Pharma, Manufacturing & Logistics), and Regional Analysis, 2026 - 2033

Robotic Process Automation Market Size and Trend Analysis

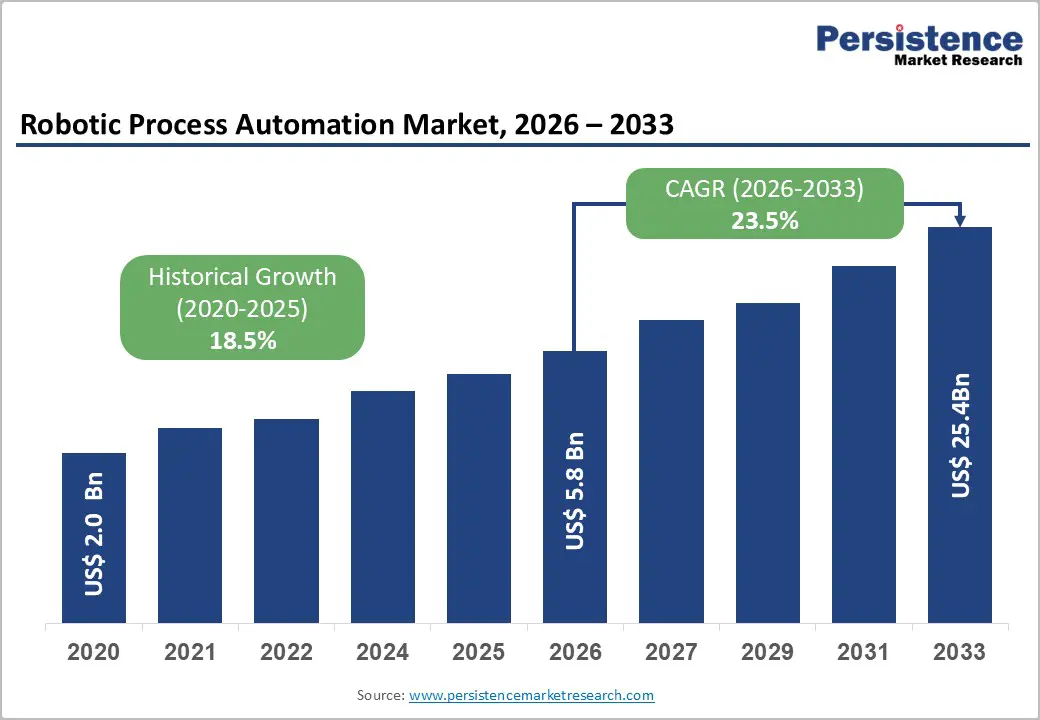

The global robotic process automation market size is likely to be valued at US$ 5.8 billion in 2026 and is projected to reach US$ 25.4 billion by 2033, growing at a CAGR of 23.5% between 2026 and 2033.

The enterprise digital transformation mandates, structural labor cost pressures across BFSI and healthcare verticals, and the convergence of artificial intelligence with core process automation platforms are driving the growth of robotic process automation models. Cloud infrastructure maturity, the democratization of low-code development, and AI-augmented bot intelligence are collectively accelerating enterprise adoption across both developed and emerging economies.

Key Industry Highlights:

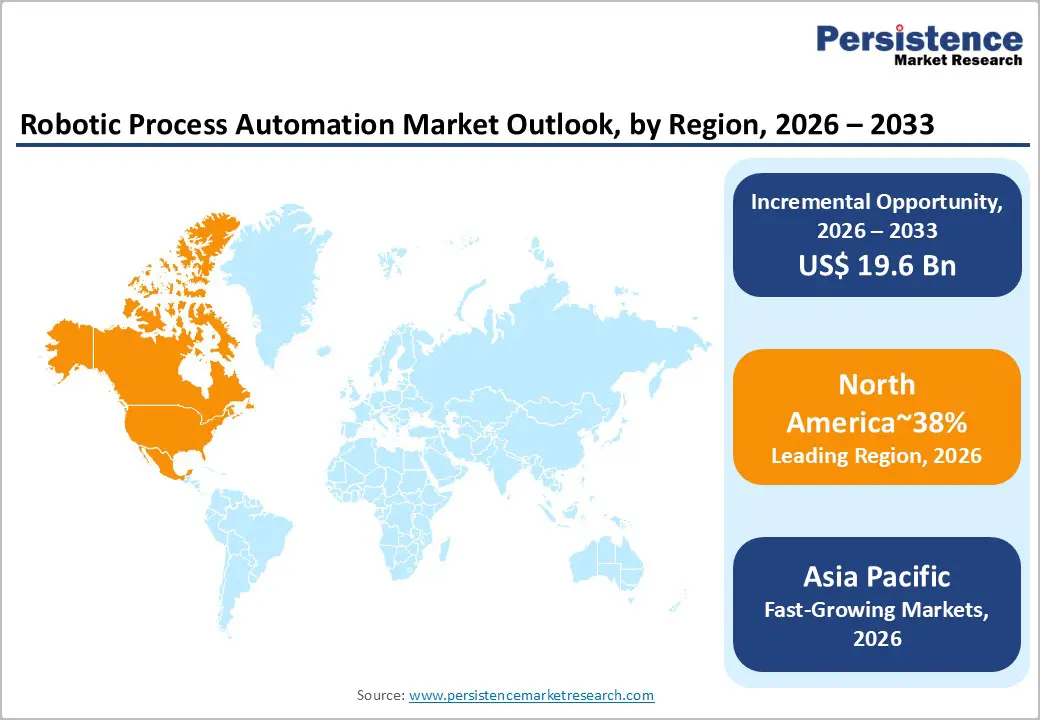

- Leading Region: North America leads the Robotic Process Automation Market with 38% share, driven by a mature enterprise automation ecosystem, strong BFSI and manufacturing adoption, and presence of major RPA vendors like UiPath, Automation Anywhere, and Microsoft-powered deployments.

- Fast-growing Region: Europe holds 27% share, supported by strong regulatory-driven automation demand across BFSI and manufacturing sectors, with Germany emerging as a key country market due to its industrial and financial services automation needs.

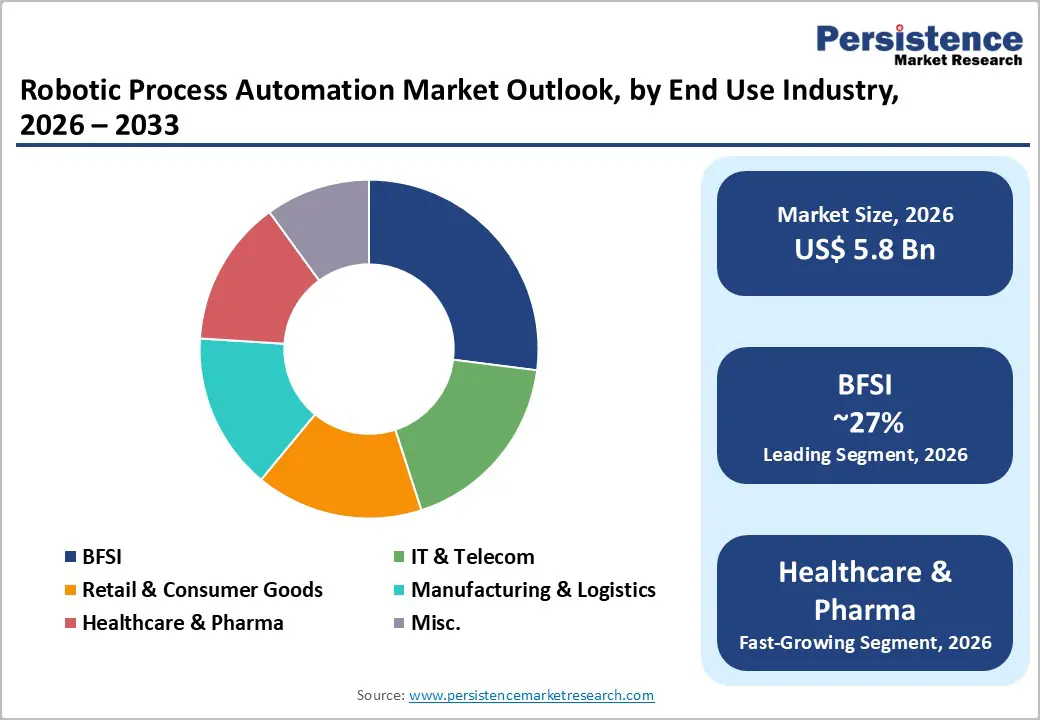

- Leading Industry: BFSI dominates the market 27% share, driven by high-volume compliance, KYC, fraud detection, loan processing, and regulatory reporting workflows across India, Europe, and China’s large-scale banking systems.

- Fast-growing Industry: Healthcare & Pharma is the fastest-growing vertical, fueled by rising regulatory documentation burden, clinical workflow automation, insurance claims processing, and supply chain traceability requirements.

- Leading Component Segment: Software dominates the market 68% share, supported by SaaS-based RPA platforms, AI-enabled automation tools, and strong enterprise adoption of scalable bot orchestration ecosystems.

DRO Analysis

Structural Transformation of BFSI Operations Through Digital Compliance and Workflow Automation

The BFSI sector's rapid structural evolution is generating compulsory demand for rule-based, high-accuracy process automation across compliance, reconciliation, fraud detection, and customer onboarding workflows. This positions BFSI as the primary commercial anchor of the robotic process automation market globally. India's BFSI sector expanded 50 times in market capitalization over two decades, reaching INR 91,00,000 crore (approximately US$ 1 trillion) by 2025 from Rs. 1,80,000 crores in 2005 and now contributes 27% to India's GDP.

Enterprise Digital Transformation and B2B E-Commerce Back-Office Automation Demand

The structural digitization of global procurement, trade, and supply chain operations is generating unprecedented volumes of structured and semi-structured transactional data that organizations must process, validate, and route in real time, creating a systemic driver for robotic process automation market adoption across enterprise operations.

The global B2B eCommerce GMV expanded from US$ 9,837 billion in 2017 to a projected US$ 36,163 billion by 2026, a transaction volume scale that makes manual back-office processing operationally untenable. APAC dominates this digital trade surge, accounting for 80% of global B2B GMV by 2026, with China, India, Japan, and South Korea driving the highest automation demand within digital procurement and logistics workflows.

In India, the logistics sector, contributing 14.4% to GDP and employing over 22 million people, is modernizing through TMS, WMS, and analytics platforms, with India's e-commerce market projected to reach US$ 300 billion by 2030, generating proportional demand for automated invoicing, inventory reconciliation, and shipment tracking processes across the Robotic Process Automation Market. Canada's e-commerce market, reaching US$ 89.4 billion in 2024, further reflects North America's deep enterprise automation pipeline within digital retail and distribution infrastructure.

AI and Intelligent Automation Convergence Redefining Process Bot Capabilities

The integration of artificial intelligence, machine learning, and computer vision into traditional RPA platforms is transforming the Robotic Process Automation Market from rule-based task execution toward adaptive, cognitive automation capable of handling unstructured data, exception management, and end-to-end process orchestration. This technological evolution is substantially expanding the addressable use case base beyond structured data entry toward complex judgment-intensive workflows.

In January 2023, NICE introduced AI-driven enhancements to its RPA portfolio through the NEVA Discover solution, enabling organizations to identify automation opportunities using process analytics and semi-supervised machine learning. In April 2026, Siemens AG successfully deployed an AI-powered humanoid robot in live factory logistics in collaboration with NVIDIA, achieving over 90% task success accuracy in picking, transporting, and placing containers, demonstrating that physical AI and digital process automation are converging into unified intelligent enterprise automation ecosystems.

In February 2023, Vedanta Aluminium introduced RPA in commercial operations, becoming the first company in India's metal and mining sector to implement end-to-end commercial process automation, establishing a precedent for heavy industry adoption and reflecting the Robotic Process Automation Market's penetration into non-traditional industrial verticals.

Restraints - Process Complexity and Legacy System Integration Barriers

Integrating RPA platforms with deeply entrenched legacy IT infrastructure remains a critical operational and financial barrier, particularly across large BFSI and government institutions operating decades-old mainframe and ERP architectures. In Europe, the EU banking sector underwent structural contraction with credit institutions declining by 2.9% to 5,304 institutions and bank branches reducing to approximately 129,400 environments where legacy systems with limited API compatibility significantly extend RPA deployment timelines, increase total cost of ownership, and elevate implementation failure risk. Process standardization prerequisites, change management requirements, and bot maintenance overhead after go-live further amplify the hidden cost burden beyond initial licensing investment.

Data Security, Governance, Risk, and Regulatory Compliance Complexity

RPA bots operating across sensitive financial, healthcare, and personal data environments create significant cybersecurity and data governance vulnerabilities that regulatory frameworks are only beginning to address formally. In the context of IoT and AI convergence, the U.S.-China Economic and Security Review Commission has explicitly flagged risks of unauthorized access to enterprise data systems a concern directly applicable to RPA bot credentials and privileged access management. The absence of harmonized global RPA governance standards across GDPR in Europe, HIPAA in the US, and data localization mandates in India and China forces multi-jurisdiction enterprises to implement market-specific compliance controls, substantially increasing deployment complexity and ongoing audit overhead.

Opportunities - Healthcare and Pharma Automation, Regulatory Compliance, and Clinical Workflow Efficiency

The healthcare and pharmaceutical sector represents the highest-velocity growth frontier for the Robotic Process Automation Market, driven by mounting regulatory documentation burdens, clinical trial data management, insurance claims processing, and supply chain traceability requirements that are uniquely suited to rule-based automation. As healthcare systems globally face dual pressures of operational cost containment and regulatory compliance rigor, RPA provides an immediately deployable solution without full electronic health record system replacements.

India's digital healthcare ecosystem, supported by Digital India and BharatNet infrastructure initiatives, is enabling clinic and hospital networks to deploy RPA for patient data entry, billing reconciliation, and supply chain management across tier-II and tier-III cities. In Europe, Eurostat data confirms that IoT health device adoption remains at only 8% among EU consumers, yet large enterprises lead IoT deployment at 56% versus 26% in small firms for condition-based maintenance and process automation, indicating that healthcare institutions with enterprise-scale operations already possess the data and connectivity infrastructure needed to accelerate RPA integration.

SS&C Blue Prism's recognition as a Gartner Magic Quadrant Leader for the sixth consecutive year in 2024 across financial services and healthcare underscores the growing commercial depth of proven RPA platforms in regulated industries within the Robotic Process Automation Market.

Emerging Market First-Time Enterprise Automation Deployments

Emerging economies across South Asia, Southeast Asia, and Latin America present high-potential greenfield opportunities for the Robotic Process Automation Market, where first-time enterprise automation deployments bypass legacy modernization challenges that slow adoption in mature markets. India's rapidly formalizing BFSI sector, where life insurance AUM reached US$ 693 billion and mutual fund AUM reached US$ 844 billion by March 2025, is generating massive back-office processing volumes across policy administration, claims, and KYC compliance that traditional staffing models cannot absorb efficiently.

Latin America's banking sector, where over 50% of adults remain unbanked, and banks face urgent pressure to modernize legacy core systems, presents a compelling commercial opportunity. Core modernization through API-first, incremental approaches as highlighted in Latin American banking sector analysis, creates the technical foundation required for RPA overlay deployment without full system replacement.

India's National Logistics Policy mandates reducing logistics costs from 13 to 14% of GDP to global benchmark levels by 2030, combined with India's e-commerce market projection to US$ 345 billion by 2030, positions Indian retail and logistics enterprises as high-urgency adopters of the Robotic Process Automation Market for order-to-cash, procure-to-pay, and shipment-tracking automation workflows.

Low-Code RPA Democratization Accelerating Mid-Market and SME Penetration

The democratization of RPA through low-code and no-code development environments is unlocking an entirely new segment of the Robotic Process Automation Market, the mid-market and SME enterprise base that previously lacked the technical resources and IT budgets to deploy traditional RPA platforms. This commercial expansion multiplies the total addressable market by enabling non-technical business users to build, deploy, and manage automation workflows without specialist programming expertise.

Microsoft's Power Automate Desktop, publicly previewed for low-code attended and unattended RPA automation, is a watershed product that embeds RPA capability within the existing Microsoft 365 enterprise ecosystem used by hundreds of millions of business users globally. This distribution leverage means RPA adoption can scale within existing software licensing agreements, dramatically reducing procurement friction and deployment cycles. In November 2024, Tungsten Automation launched TotalAgility 8.1, integrating RPA, AI agents, and low-code capabilities to enable faster autonomous workflow development, reflecting the industry-wide convergence toward platforms that empower business analysts rather than solely IT developers within the Robotic Process Automation Market.

Category-wise Analysis

Component Type Insights

The software segment commands approximately 68% of the robotic process automation market, reflecting its foundational role as the core value delivery mechanism encompassing bot development environments, orchestration platforms, process discovery tools, and analytics dashboards. Software dominance is reinforced by the SaaS transition, where leading vendors, including UiPath, Automation Anywhere, and SS&C Blue Prism, distribute platforms on subscription models that generate recurring, scalable revenue tied directly to enterprise automation scope.

SS&C Blue Prism's six consecutive Gartner Magic Quadrant Leader recognitions through 2024 reflect the competitive depth and enterprise validation of RPA software platforms. Pegasystems' recognition as a Forrester Wave Leader in Q1 2023, with the highest scores in automation design and development, further confirms that software capability differentiation is the primary competitive battleground within this segment.

The services segment, encompassing RPA implementation, consulting, managed services, training, and ongoing bot maintenance, is the fastest-growing component of the Robotic Process Automation Market, driven by enterprises' need for specialized deployment expertise as automation programs scale from pilots to enterprise-wide deployments. As organizations move from deploying tens of bots to managing hundreds or thousands across multi-geography operations, demand for governance, center-of-excellence establishment, change management, and performance-optimization services compounds significantly.

Deployment Model Insights

Cloud-based deployment commands approximately 52% of the robotic process automation industry, driven by its inherent advantages in scalability, rapid provisioning, automatic software updates, and lower upfront capital requirements relative to on-premises alternatives. Cloud RPA's alignment with the broader enterprise SaaS transition, where organizations increasingly standardize on cloud platforms for ERP, CRM, and collaboration tools, creates natural integration pathways that reduce deployment complexity. The global B2B eCommerce ecosystem's cloud-native architecture, processing US$ 36,163 billion in annual GMV, relies on cloud-based automation platforms for invoice processing, procurement validation, and logistics data management.

Microsoft's Power Automate, embedded within the Azure and Microsoft 365 cloud ecosystem, exemplifies how cloud RPA benefits from hyperscaler distribution and cross-platform workflow integration at enterprise scale.

On-premises deployment is the fastest-growing model within the Robotic Process Automation Market, driven by data sovereignty requirements, regulatory mandates, and security governance priorities within highly regulated verticals, particularly BFSI, defense-adjacent manufacturing, and government institutions. In Europe, where GDPR imposes strict data residency and processing transparency requirements, and in China, where national data security laws mandate localized data handling, organizations operating sensitive workflows cannot route bot-processed data through public cloud infrastructure.

Industry Insights

BFSI holds the dominant position within the robotic process automation market at approximately 27%, reflecting the sector's high density of structured, rule-intensive, high-volume processes, including KYC verification, loan origination, claims processing, regulatory reporting, and trade settlement that represent ideal RPA automation targets. India's BFSI sector's market capitalization journey from US$ 20.28 billion in 2005 to US$ 1 trillion by 2025 represents a 50-fold expansion that has proportionally scaled back-office processing volumes across banks, NBFCs, AMCs, and insurers.

European BFSI generated €0.9 trillion in value added in 2022 across approximately 867,000 enterprises, maintaining a gross operating rate of 24%. In this environment, marginal improvements in operational efficiency through automation translate directly into significant absolute profitability gains. In 2023, European banking total assets reached €43.6 trillion, with over 2 million banking employees, representing automation substitution potential across repetitive transaction-processing workflows.

Healthcare and Pharma are the fastest-growing Industries within the Robotic Process Automation Market, propelled by the sector's accelerating digital transformation, mounting prior authorization burdens, clinical documentation requirements, and pharmaceutical supply chain compliance mandates. The global pharmaceutical logistics and hospital administration landscape is increasingly deploying RPA for patient scheduling, insurance eligibility verification, drug inventory reconciliation, and regulatory submission management.

Regional Insights

Asia Pacific Robotic Process Automation Market Trends and Insights

Asia Pacific holds approximately 24% of the global robotic process automation market, representing the highest absolute growth potential globally given the region's scale of enterprise digitization, BFSI formalization, and e-commerce infrastructure investment. China's Robotic Process Automation market, reflecting the country's role as Asia Pacific's RPA leader driven by its US$ 467.3 trillion banking asset base, state-directed enterprise technology modernization mandates, and the world's largest B2B eCommerce transaction volumes. China's insurance sector grew 9.2% year-on-year to RMB 39.2 trillion in assets as of Q2 2025, with primary premium income of RMB 3.7 trillion generating massive underwriting, claims, and regulatory reporting automation requirements within the Robotic Process Automation Market.

India represents the fastest-growing RPA market in Asia Pacific, valued at US$ 187.5 Mn in 2025, driven by the formalization of the BFSI sector, which expanded its GDP contribution from 6% to 27%, and the country's accelerating digital economy targeting US$ 1 trillion by 2030. Vedanta Aluminium's February 2023 deployment of end-to-end commercial process automation through RPA, the first in India's metal and mining sector, signals that RPA adoption is expanding well beyond BFSI into capital-intensive industrial sectors. India's e-commerce market, projected to reach US$ 345 billion by 2030, combined with record warehousing leasing of 39.5 million sq. ft. in 2024, is creating parallel demand for automated supply chain documentation, order processing, and 3PL management workflows. India's approximately 94 domestic IoT solution companies profiled by industry reports reflect the depth of India's technology ecosystem that is enabling RPA integration with connected enterprise infrastructure across manufacturing, logistics, and retail verticals.

North America Robotic Process Automation Market Trends and Insights

North America commands approximately 38% of the Global Robotic Process Automation Market, the largest regional share anchored by the United States as the world's most mature enterprise automation ecosystem. The United States Robotic Process Automation market was valued at US$ 1,799.1 Mn in 2025, supported by the highest enterprise RPA licensing density globally, a deep systems integration services ecosystem, and the broadest concentration of RPA platform headquarters, including UiPath, Automation Anywhere, WorkFusion, Pegasystems, Vecna, OnviSource, and OTTO Motors.

The U.S. food and beverage manufacturing sector, employing approximately 1.7 million workers and accounting for 16.8% of total U.S. manufacturing sales in 2021, represents a primary non-BFSI automation demand vertical, where FDA compliance, USDA traceability mandates, and perishable inventory management workflows create high-priority RPA deployment targets.

North America's B2B e-commerce sector, representing approximately 13.7% of global B2B GMV by 2026 in an absolute market of US$ 36,163 billion, is generating sustained back-office automation demand across procurement, accounts payable, and vendor onboarding workflows. Canada's e-commerce market, valued at US$ 89.4 billion in 2024 and projected at approximately US$ 104 billion by 2029, is driving incremental RPA adoption across retail fulfillment, customs documentation, and bilingual compliance workflows.

Pegasystems' Forrester Wave leadership recognition in Q1 2023, with the highest scores in automation design and development, reflects the competitive technical depth of North American-headquartered platforms, while Microsoft's Power Automate Desktop distributed through the world's largest enterprise software ecosystem is uniquely positioned to drive SME-level RPA penetration across the North American mid-market at scale not achievable through standalone RPA vendor channels.

Europe Robotic Process Automation Market Trends and Insights

Europe holds approximately 27% of the Global Robotic Process Automation Market, characterized by a regulatory-driven environment, world-class BFSI and manufacturing sectors, and the strongest enterprise data governance requirements globally. Germany leads European RPA adoption with a market value of US$ 281.2 Mn in 2025, anchored by the country's automotive OEM ecosystem, precision manufacturing industrial base, and advanced BFSI sector all of which operate high-volume, compliance-intensive workflows ideally suited for RPA.

The EU financial and insurance sector generated €0.9 trillion in value added in 2022 across approximately 867,000 enterprises, with Germany, France, Italy, Spain, and Poland collectively accounting for over 65% of sectoral value added and 66% of employment a concentrated regional demand base where RPA adoption directly translates to competitive operational efficiency advantages.

Spain accounts for approximately 7.5% of the European Robotic Process Automation Market, making it the most significant emerging growth market in the EU. Spain's financial services consolidation where BFSI institutions are accelerating digitization to compete with neo-banks and fintech disruptors is driving first-generation enterprise RPA deployments across claims processing, retail banking, and insurance policy administration.

Competitive Landscape

The global robotic process automation market exhibits a semi-consolidated competitive structure, where three dominant pure-play RPA vendors, UiPath, Automation Anywhere, and SS&C Blue Prism hold disproportionate market influence through platform maturity, enterprise customer depth, and analyst recognition. Beneath this top tier, technology conglomerates including Microsoft, SAP, and NICE are aggressively integrating RPA capabilities into broader enterprise platforms, creating a convergence dynamic that blurs traditional product boundaries.

The market is not oligopolistic a large number of specialist and regional players participate but the top six vendors command the majority of enterprise contract value, making it closer to consolidated than fragmented across Fortune 1000 customer segments.

The dominant strategic themes in the Robotic Process Automation Market are AI-augmentation of core bot platforms, platform ecosystem integration within ERP and CRM environments, and consumption-based pricing models that lower adoption barriers. Market leaders differentiate through analyst recognition, process discovery intelligence, and center of excellence enablement frameworks. The most significant emerging business model trend is the shift toward agentic automation, where AI-driven bots make real-time decisions without human intervention, transitioning RPA from task execution to autonomous process ownership.

Key Developments:

- July 1, 2025, UiPath Recognized as a Leader in the 2025 Gartner® Magic Quadrant™ for Robotic Process Automation for the seventh consecutive year and positioned highest for “Ability to Execute,” reinforcing its leadership in advancing agentic automation platforms that integrate AI-driven software robots, orchestration, and enterprise workflows.

- June 2025, Automation Anywhere, recognized as a Leader in the Gartner® Magic Quadrant™ for Robotic Process Automation for the seventh consecutive year, highlighting its strong market position driven by a cloud-native RPA platform and advancements in Agentic Process Automation (APA), including AI-powered agents and Process Reasoning Engine enabling intelligent, scalable enterprise automation.

- June 30, 2025, SS&C Blue Prism: Recognized as a Leader in the 2025 Gartner® Magic Quadrant™ for Robotic Process Automation for the seventh consecutive year, underscoring its strong market position through integration of AI-powered digital workers and orchestration capabilities that enable large-scale, secure, and intelligent automation across complex enterprise processes.

Global Robotic Process Automation Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.0 Bn |

|

Current Market Value (2026) |

US$ 5.8 Bn |

|

Projected Market Value (2033) |

US$ 25.4 Bn |

|

CAGR (2026-2033) |

23.5% |

|

Leading Region |

North America, 38% share |

|

Dominant End Use Industry |

BFSI, 27% share |

|

Top-ranking Component |

Software, 68% |

|

Incremental Opportunity |

US$ 8.1 Bn |

Companies Covered in Robotic Process Automation Market

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Limited

- Microsoft Corporation

- NICE Ltd.

- Pegasystems Inc.

- SAP SE

- WorkFusion, Inc.

- EdgeVerve Systems Limited (Infosys)

- Tungsten Automation Corporation

- OnviSource, Inc.

- NTT Advanced Technology Corporation

- FPT Software

- BlackLine Inc.

- Uniphore

Frequently Asked Questions

The global Robotic Process Automation Market is projected to be valued at US$ 5.8 Bn in 2026.

Software leads the market with approximately 68% share, driven by SaaS-based RPA platforms and AI-integrated automation solutions.

The BFSI sector dominates with approximately 27% share, supported by large-scale digital transformation in banking and insurance industries.

The market is expected to witness a CAGR of 23.5% from 2026 to 2033.

The Robotic Process Automation Market is driven by the structural transformation of BFSI and enterprise operations, rapid expansion of B2B e-commerce and high-volume digital transactions, and the convergence of AI with automation technologies that enable intelligent, scalable, and end-to-end process automation across industries.