- Hardware & Software IT Services

- Home Wi-Fi Router and Extender Market

Home Wi-Fi Router and Extender Market Size, Share, and Growth Forecast, 2026 - 2033

Home Wi-Fi Router and Extender Market by Device Type (Routers, Extenders / Repeaters, Mesh Systems), Technology (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, Wi-Fi 7), Distribution Channel (Retail, Online, ISP/Telco bundle, Direct Sales, Others), and Regional Analysis for 2026 - 2033

Home Wi-Fi Router and Extender Market Size and Trends

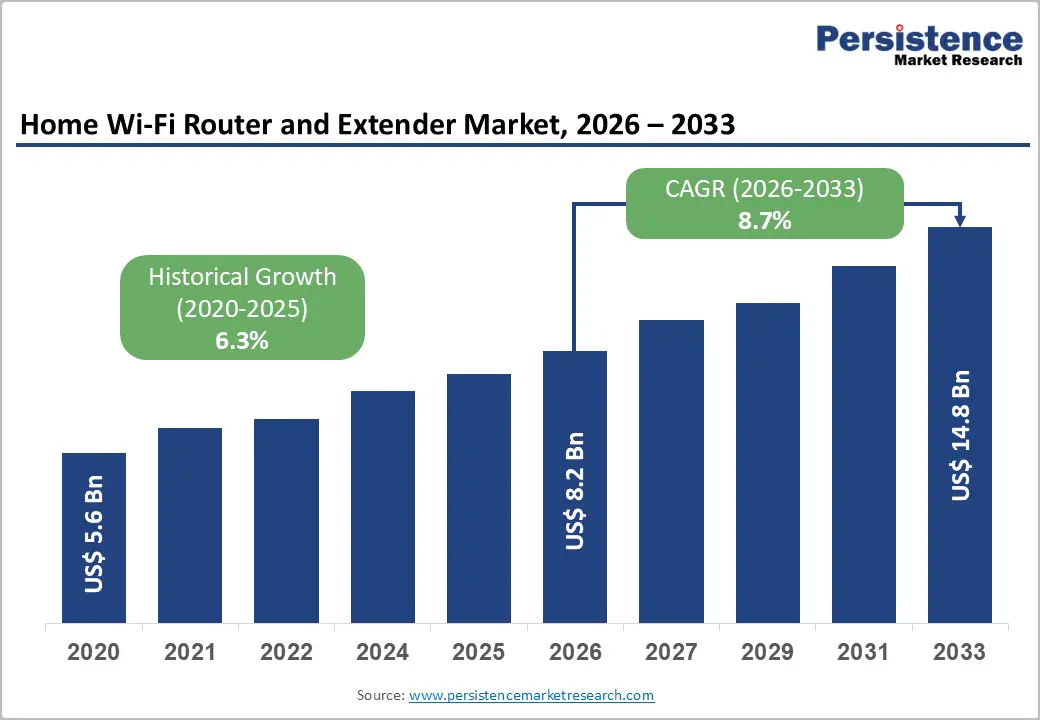

The global home Wi-Fi router and extender market is projected to grow from US$8.2 billion in 2026 to US$14.8 billion by 2033. It is anticipated that the market will grow at a CAGR of 8.7% from 2026 to 2033, driven by the accelerating global rollout of high-speed broadband infrastructure, the rapid proliferation of smart home devices, and the mass adoption of next-generation Wi-Fi standards such as Wi-Fi 6E and emerging Wi-Fi 7.

According to the International Telecommunication Union (ITU), as of 2025, an estimated 6 billion people are active internet users, creating sustained demand for reliable home networking hardware. The parallel surge in connected devices per household further compels consumers and ISPs to upgrade from legacy single-router setups to advanced mesh and multi-node systems.

Key Industry Highlights:

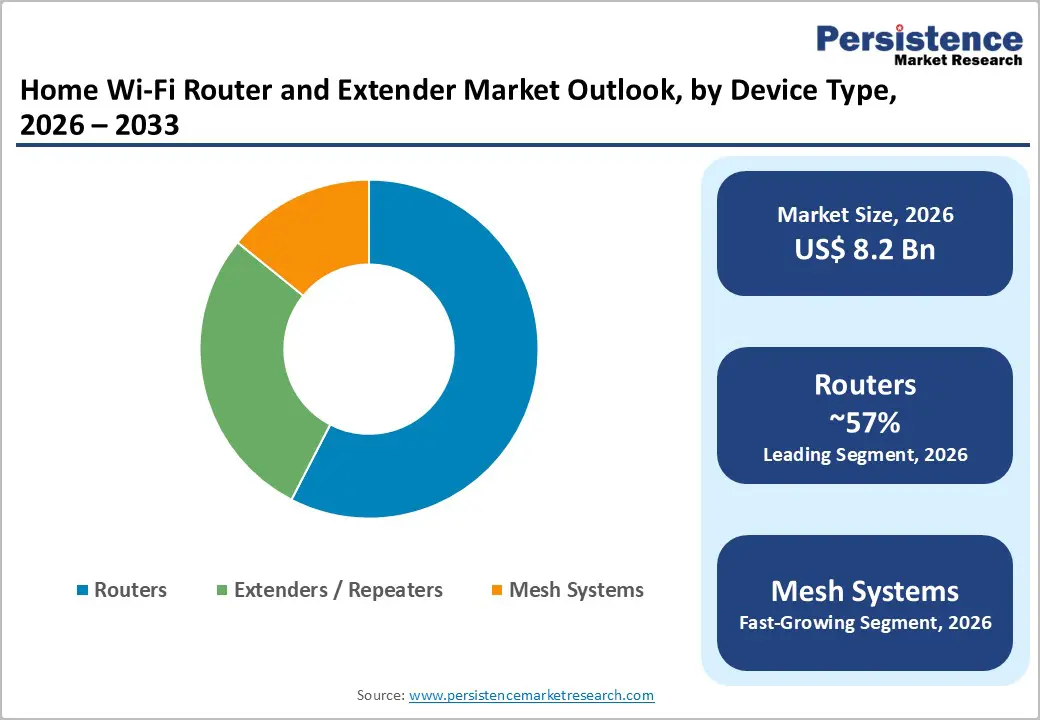

- Leading Device Type: Routers dominate the market with over 57% share in 2026, valued at more than US$ 4.7 Bn, driven by their role as the primary home connectivity hub and rising fiber broadband penetration.

- Leading Technology: Wi-Fi 5 holds over 40% market share in 2026, valued at more than US$ 3.3 Bn, supported by its affordability, compatibility, and widespread installed base for standard internet usage.

- Leading Distribution Channel: Retail leads the market with over 42% share in 2026, valued at more than US$ 3.4 billion, driven by strong consumer preference for product comparison, the availability of multiple brands, and attractive e-commerce promotions.

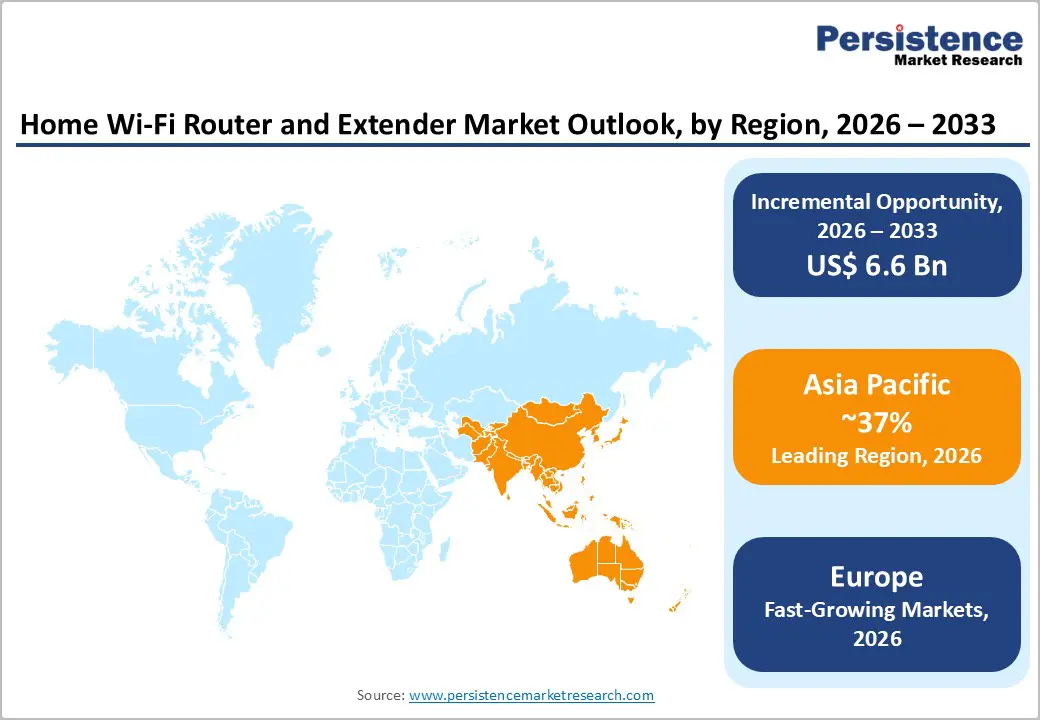

- Leading Region: Asia Pacific leads with over 37% share in 2026, valued at around US$ 3.0 Bn, supported by rapid broadband expansion, strong manufacturing ecosystem, and low-cost data availability. North America holds over 32% share in 2026, valued at approximately US$ 2.6 Bn, supported by near-universal broadband availability, high household device penetration, and strong demand for premium Wi-Fi 6E and Wi-Fi 7 mesh systems.

| Key Insights | Details |

|---|---|

|

Home Wi-Fi Router and Extender Market Size (2026E) |

US$8.2 Bn |

|

Market Value Forecast (2033F) |

US$14.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.3% |

Market Dynamics

Driver - Rising Household Data Consumption and Connected Devices

Global internet traffic continues to surge, with average household data consumption exceeding 300 GB per month in developed markets, driven by 4K streaming, gaming, and cloud applications. The number of connected devices per household has crossed 5-10 devices in many urban regions, according to a study. This exponential growth necessitates robust and high-capacity routers and extenders to maintain seamless connectivity. The parallel growth in the Smart Home Devices Market and IoT adoption further accelerates demand for reliable Wi-Fi infrastructure, making routers and extenders essential household utilities rather than discretionary purchases.

Expansion of Fiber Broadband and Government Digital Initiatives

Governments worldwide are investing heavily in broadband infrastructure, with programs such as India’s BharatNet, the U.S. Broadband Equity, Access, and Deployment (BEAD) Program, and the European Gigabit Society targets aiming to deliver high-speed internet access. According to Ericsson, the global fixed broadband connection growth projection is that 1.6 billion connections will increase to 2 billion by 2030, with 550 million additional connections in fiber, FWA, and satellite, underscoring the need for advanced routers capable of handling gigabit speeds. As ISPs bundle routers and extenders with broadband subscriptions, the demand for home networking equipment is expanding in parallel, particularly in emerging economies transitioning from DSL to fiber networks.

Restraint - High Replacement and Upgrade Costs Limiting Consumer Spending

Affordability constraints remain a tangible barrier to market penetration, particularly in price-sensitive markets across South Asia, Sub-Saharan Africa, and Latin America. Premium Wi-Fi 6E and Wi-Fi 7 mesh systems from some vendors are priced at US$ 400–700 or more, placing them well beyond the budgetary reach of a large segment of global consumers. This cost barrier prolongs the device replacement cycle, suppressing overall unit shipment volumes and moderating revenue growth in the near term.

Cybersecurity Vulnerabilities and Consumer Awareness Gaps

The U.S. Cybersecurity and Infrastructure Security Agency (CISA) and ENISA (European Union Agency for Cybersecurity) have repeatedly flagged home routers as among the most frequently exploited attack surfaces in consumer electronics.

According to a study, the majority of residential Wi-Fi routers operate on outdated firmware, leaving networks vulnerable to exploitation. Consumer awareness gaps around firmware updates, password hygiene, and encryption standards create friction in the adoption of newer, more secure hardware and slow market growth as regulatory bodies in the EU and U.S. contemplate mandatory security certification requirements for home networking equipment.

Opportunity - Gaming, Streaming, and Remote Work Vertical-Specific Product Segmentation

The sustained normalization of remote and hybrid work models, first catalyzed by the pandemic and now structurally embedded across industries globally, has made home office-grade Wi-Fi performance a non-negotiable requirement for a growing professional demographic. Cloud gaming platforms, including Microsoft Xbox Cloud Gaming, NVIDIA GeForce NOW, and Sony PlayStation Now, require low latency and stable high-bandwidth connections, compelling performance-oriented consumers to invest in gaming-optimized networking hardware with dedicated quality of service controls and low-latency modes.

Targeted marketing toward these high-disposable-income, performance-conscious demographics enables manufacturers to command significant price premiums over generic consumer router products, meaningfully improving revenue per unit metric.

Cybersecurity-Integrated Routers and Subscription-Based Network Security Services

As home networks become the primary gateway for sensitive professional and personal data, the demand for routers with built-in, enterprise-grade cybersecurity capabilities is emerging as a distinct and high-revenue-potential product category. The convergence of networking and security is structurally reshaping the home Wi-Fi market, with the subscription-based security services segment encompassing deep packet inspection, network intrusion prevention, parental controls, and real-time threat detection growing rapidly in high-density smart home environments.

Governments and industry bodies across the United States, the European Union, and the United Kingdom are increasingly mandating improved baseline cybersecurity standards for connected devices, including routers, prompting both consumer-driven upgrades and regulatory-compliance-driven hardware replacement. This environment creates a compelling dual-revenue opportunity for manufacturers' premium hardware with embedded security chipsets at higher ASPs, combined with recurring monthly or annual subscription fees for managed threat intelligence services.

Category-wise Analysis

Device Type Insights

Routers dominate the market, capturing more than 57% share in 2026 with a value exceeding US$ 4.7 Bn, due to their essential role as the primary connectivity hub in every household. Consumers prioritize high-speed performance, wider coverage, and multi-device handling, making routers a necessity rather than an option. Increasing fiber broadband penetration and higher bandwidth plans further reinforce router upgrades. Advancements in dual-band and tri-band routers cater to latency-sensitive applications, strengthening their dominance.

Mesh systems are expected to grow rapidly due to increasing demand for whole-home coverage and elimination of dead zones in larger and multi-story homes. Users are shifting from traditional extenders to mesh systems for their seamless roaming and unified network experience. The rise in connected devices per household is creating a need for consistent performance across all rooms. Ease of installation and app-based network management are also appealing to non-technical consumers. Growing adoption of smart homes and IoT ecosystems further accelerates demand. Premiumization trends are pushing consumers toward higher-value mesh solutions.

Technology Insights

Wi-Fi 5 holds over 40% share in 2026, with a value exceeding US$ 3.3 Bn, due to its widespread installed base and affordability. Many households continue to rely on Wi-Fi 5 as it sufficiently supports standard internet usage such as HD streaming and browsing. Cost-sensitive consumers, especially in emerging markets, prefer it due to lower upfront investment. Compatibility with existing devices and infrastructure also sustains its relevance. Retail availability and bundled offerings further support its continued adoption.

Wi-Fi 7 is expected to experience rapid growth due to the increasing demand for ultra-high-speed, low-latency connectivity, driven by applications such as 8K streaming, AR/VR, and cloud gaming. The need for higher bandwidth and reduced network congestion in device-dense environments is accelerating adoption. Early adopters and tech-savvy consumers are driving initial demand, especially in developed regions. The expansion of gigabit and multi-gigabit broadband services complements Wi-Fi 7 capabilities.

Distribution Channel Analysis

Retail commands a large share at over 42% in 2026, with a value exceeding US$ 3.4 Bn, due to strong consumer preference for direct product comparison and immediate purchase. Both offline and online retail channels offer a wide range of brands, specifications, and price points, enabling informed decision-making. E-commerce platforms are playing a crucial role in expanding access, especially in urban and semi-urban areas. Promotional discounts, bundled deals, and customer reviews further influence purchasing behavior. Consumers upgrading their home networks often prefer retail channels for flexibility and choice. Brand visibility and marketing campaigns also heavily drive retail dominance.

The ISP/Telco bundle is expected to grow at a CAGR of 11.6% as demand for hassle-free connectivity solutions bundled with broadband subscriptions increases. Consumers prefer plug-and-play devices provided by service providers, reducing setup complexity and compatibility concerns. ISPs are leveraging bundled routers and extenders to improve customer retention and service quality. The rise in fiber-to-the-home (FTTH) deployments is accelerating the adoption of bundled equipment. Subscription-based models and device financing options are also making advanced equipment more accessible.

Regional Insights

North America Home Wi-Fi Router and Extender Market Trends

North America holds over 32% share in 2026, reaching US$ 2.6 Bn value, driven by near-universal broadband availability and high consumer spending on connected devices. According to the Federal Communications Commission, 95% of U.S. households & small businesses have access to fixed broadband, supporting a mature, replacement-driven market. Premium devices such as Wi-Fi 6E and Wi-Fi 7 mesh systems witness strong adoption, further accelerated by ISP-bundled routers in subscription plans. Initiatives like the BEAD Program are expanding rural connectivity, creating incremental hardware demand. The region also serves as an early adoption hub for next-generation standards led by the Wi-Fi Alliance.

Asia Pacific Home Wi-Fi Router and Extender Market Trends

Asia Pacific holds over 37% share in 2026, reaching US$ 3.0 Bn value, supported by rapid internet subscriber expansion and a strong manufacturing ecosystem led by China. Government initiatives under China’s Five-Year Plan and affordable devices from domestic brands are driving large-scale adoption. In India, the Telecom Regulatory Authority of India reported over 970 million broadband connections, fueled by low-cost data and emerging 5G-FWA services. Developed markets like Japan demand high-performance routers for ultra-fast fiber, while ASEAN countries see strong first-time adoption. Price-sensitive consumers and increasing mesh/extender usage in dense urban housing further accelerate volume growth.

Europe Home Wi-Fi Router and Extender Market Trends

Europe is expected to hold more than 24% share by 2026, led by Germany, the UK, France, and Spain, contributing over 50% of regional revenue. The European Commission’s Digital Decade 2030 initiative is driving gigabit connectivity and 5G expansion, accelerating demand for high-performance routers. With FTTH penetration exceeding 55% in EU27, households increasingly require advanced routers and mesh systems to optimize speeds. ISP-provided routers and upgrades driven by regulators like Ofcom are key growth enablers. Rising cybersecurity awareness and compliance with ETSI and RED standards are boosting the adoption of WPA3-enabled secure networking devices.

Competitive Landscape

The global home Wi-Fi router and extender market exhibits a moderately consolidated competitive structure, dominated by a handful of established players that together account for a substantial share of global unit shipments. Market leaders differentiate through aggressive product tiering, proprietary mesh networking ecosystems, and AI-driven network management software.

Emerging business models include subscription-based network security services, ISP co-branding partnerships, and cloud-managed consumer networking platforms. R&D expenditure is intensifying as vendors race to commercialize Wi-Fi 7 portfolio lines and explore integration with smart home and Matter protocol ecosystems.

Key Industry Developments:

- In January 2026, ASUS unveiled its ROG NeoCore WiFi 8 concept router, showcasing next-generation wireless technology focused on ultra-high reliability, lower latency, and smarter multi-device connectivity. The router demonstrates real-world WiFi 8 performance gains over WiFi 7, including up to 2× higher throughput, wider IoT coverage, and significantly reduced latency, with commercial rollout expected later in 2026.

- In January 2025, TP-Link announced its expanded Wi-Fi 7 portfolio, including new Deco mesh systems, Archer routers, and travel routers designed to deliver faster speeds, lower latency, and broader coverage for home, outdoor, and on-the-go connectivity. The lineup focuses on Wi-Fi 7 for Everyone, offering high-performance networking solutions, such as multi-gig mesh systems and gaming-optimized routers, to improve streaming, gaming, and smart home connectivity.

Companies Covered in Home Wi-Fi Router and Extender Market

- TP-Link Technologies Co., Ltd.

- NETGEAR Inc.

- ASUSTeK Computer Inc.

- Huawei Technologies Co., Ltd.

- D-Link Corporation

- Xiaomi Corporation

- Linksys Holdings, Inc.

- Amazon

- Tenda Technology

- Zyxel Communications

- Ubiquiti Inc.

- Nokia

- Others

Frequently Asked Questions

The global home Wi-Fi Router and Extender market is projected to be valued at US$8.2 Bn in 2026.

Increasing remote work, online education, and streaming services fuel the need for wider and more reliable network coverage, are key drivers of the market.

The home Wi-Fi Router and Extender market is expected to witness a CAGR of 8.7% from 2026 to 2033.

Expansion of smart homes and IoT ecosystems creates strong opportunities for advanced Wi-Fi 6/6E and mesh networking solutions.

TP-Link Technologies Co., Ltd., NETGEAR Inc., ASUSTeK Computer Inc., Huawei Technologies Co., Ltd., D-Link Corporation, Xiaomi Corporation, Linksys Holdings, Inc., and Amazon are among the leading key players.