- Hardware & Software IT Services

- Data Center Support & Maintenance Services Market

Data Center Support & Maintenance Services Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Support & Maintenance Services Market by Component Type (Servers, Storage Systems, Networking Equipment)., Data Centre Type (Hyperscale Data Centres, Colocation Data Centres, Enterprise Data Centres), Service Type (Preventive Maintenance Services, Corrective / Break-Fix Maintenance, Predictive Maintenance (AI/Monitoring-based), Remote Monitoring & Management Services, On-site Support Services, Managed Maintenance Contracts (AMC / Full Service), Misc.), Industry, and Regional Analysis for 2026 - 2033

Data Center Support & Maintenance Services Market Size and Trends Analysis

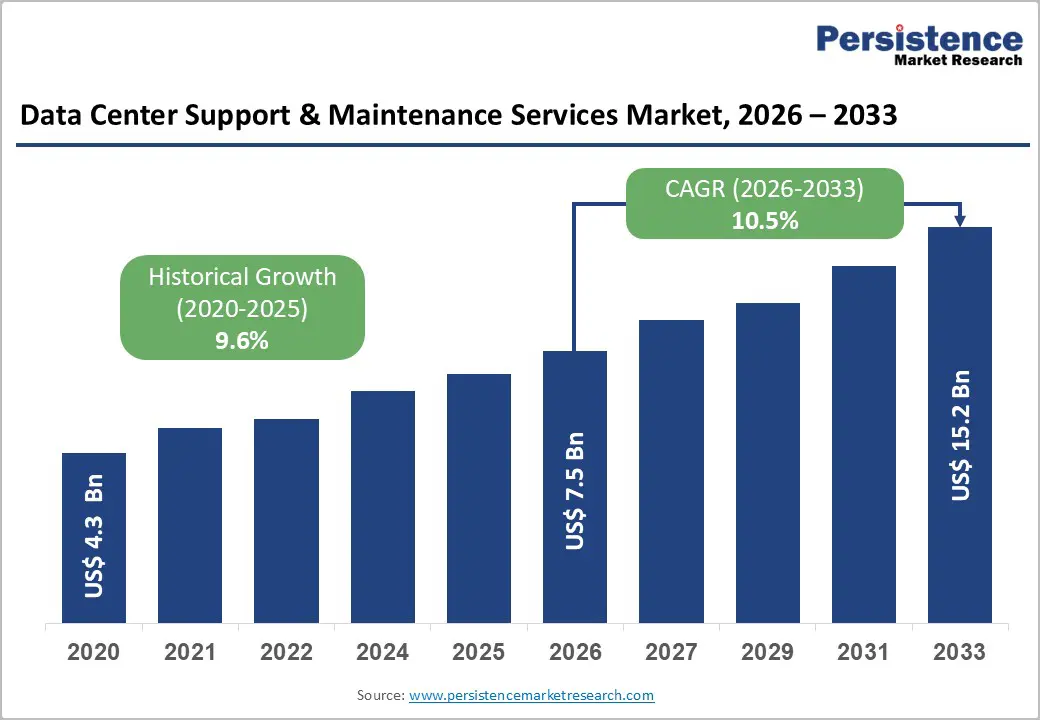

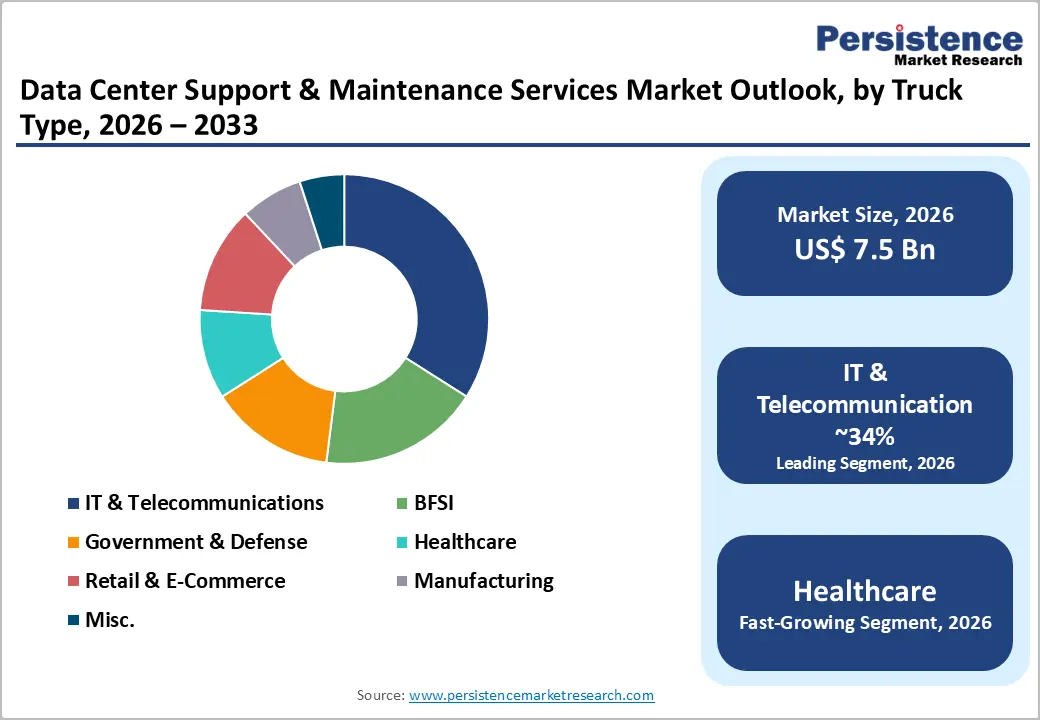

The global data center support & maintenance services market size was valued at US$ 7.5 Bn in 2026 and is projected to reach US$ 15.2 Bn by 2033, growing at a CAGR of 10.5% between 2026 and 2033.

Primary growth factors include the rapid proliferation of AI and cloud workloads, the expansion of hyperscale data Centre campuses, and heightened demand for uptime assurance across critical IT infrastructure. Global internet users reached approximately 5.5 billion, representing 68% of the world's population, with year-on-year adoption accelerating to 3.4%, according to the International Telecommunication Union, directly amplifying demand for data Centre operational continuity services.

Key Industry Highlights:

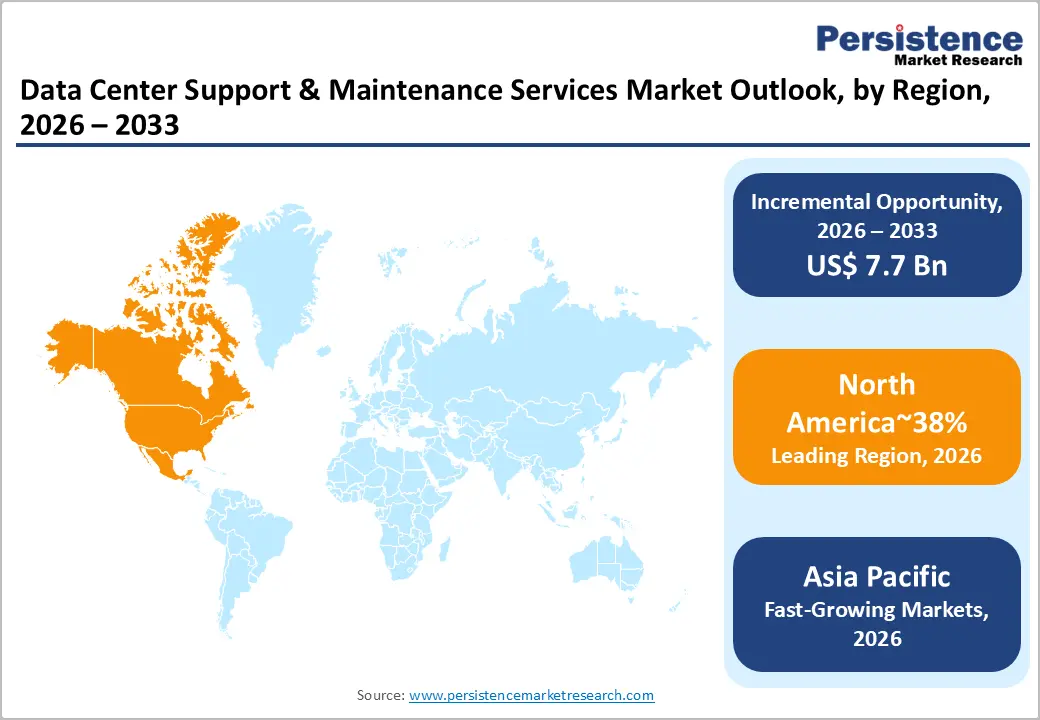

- Leading Regional Market: Asia Pacific dominates the data center Support & Maintenance Services Market with approximately 30% share, driven by rapid digital infrastructure expansion in China and India, a massive internet user base (over 2.0 billion combined users), and large-scale hyperscale data Centre deployments supporting e-commerce, AI, and government digital services.

- Fast-growing Market: North America holds around 38% share, led by the United States, supported by advanced cloud infrastructure, strong presence of hyperscale operators, and early adoption of AI-driven predictive maintenance and remote monitoring technologies across large-scale data Centre estates.

- European Market Scenario: Europe accounts for nearly 20% share, supported by high internet penetration (94% of the EU population), strong enterprise digitization, and expanding cloud adoption across Germany, the UK, France, and the Netherlands, driving steady demand for structured maintenance and lifecycle management services.

- Leading Segment Data Center Type: Hyperscale Data Centers dominate with approximately 48% share, driven by exponential growth in cloud computing, AI workloads, and B2B e-commerce traffic, requiring SLA-driven predictive maintenance, automated monitoring, and large-scale infrastructure lifecycle support.

- Fastest-Growing Segment: Enterprise data centers are the fastest-growing segment, fueled by BFSI, healthcare, and manufacturing sectors adopting hybrid IT models, AI integration, and regulatory compliance-driven demand for third-party maintenance and extended hardware lifecycle management.

- Leading Industry: IT & Telecommunications leads the market with around 34% share, supported by massive telecom infrastructure expansion, rising data consumption, and continuous network modernization requiring high-availability server, storage, and networking maintenance services.

| Key Insights | Details |

|---|---|

| Market Data Centre Support & Maintenance Services Size (2026E) | US$ 7.5 Bn |

| Market Value Forecast (2033F) | US$ 15.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

DRO Analysis

Drivers - Structural Expansion of Global Digital Infrastructure and Internet Adoption Reinforces Demand in the Data Center Support & Maintenance Services Market

The accelerating scale of global internet adoption and digital service consumption creates sustained demand for data Centre operational continuity, directly underpinning the Data Center Support & Maintenance Services Market.

According to the International Telecommunication Union, approximately 5.5 billion people were using the internet in 2024, representing 68% of the global population, up from 65% the prior year, with year-on-year adoption growth accelerating from 2.7% to 3.4%. China alone reported 1.108 billion internet users as of December 2024, with mobile internet users accounting for 99.7% of all netizens, according to the China Internet Network Information Centre.

China's data-intensive services, including social networking, e-government platforms, and generative AI, reaching 249 million users, are significantly amplifying traffic volumes and reliability requirements across national data Centre networks. In the European Union, 94% of individuals used the internet in 2025, according to Eurostat, with one in three using generative AI tools. India recorded 954.40 million internet subscribers as of March 2024, with rural subscribers at 398.35 million over a decade. This global-scale digital expansion translates into continuous infrastructure growth, hardware lifecycle complexity, and elevated requirements for support and maintenance services.

India's Digital Connectivity Infrastructure Build-Out and Telecom Investment Drive Regional Data Centre Maintenance Demand

India's large-scale national connectivity infrastructure program is generating a structurally significant demand environment for the data center support & maintenance services market, as expanded telecom and broadband coverage directly amplifies the installed base of servers, networking equipment, and edge computing nodes requiring professional maintenance services. India's gross telecom revenue reached US$ 43.42 billion in FY25, up from US$ 39.22 billion in FY24, according to government data. Cumulative FDI inflows into the telecom sector reached Rs. 3,43,360 crore, approximately US$ 40.07 billion, between April 2000 and March 2025, making it the fourth-largest sector for FDI equity inflows.

The BharatNet program has made 2.13 lakh Gram Panchayats service-ready with optical fibre connectivity, while the Universal Service Obligation Fund has targeted 35,680 uncovered villages and habitations with an investment of approximately INR 11,000 crore. Average internet download speeds improved from 4.18 Mbps to 105.85 Mbps, reflecting substantial telecom infrastructure upgrade activity. These investments in national connectivity infrastructure expand the operational IT asset base, reinforcing sustained demand for data Centre support and maintenance services across India's rapidly evolving digital ecosystem.

E-Commerce and B2B Digital Platform Expansion Multiplies Data Centre Operational Complexity and Support Requirements

The structural shift toward digital commerce and cloud-enabled procurement is a key macro-level driver for the Data Center Support & Maintenance Services Market, as escalating transaction volumes and platform uptime requirements increase the criticality and complexity of data Centre infrastructure operations. The global B2B e-commerce market recorded a CAGR of 14.5 per cent from 2017 to 2026, with gross merchandise value climbing from US$ 9,837 billion to US$ 36,163 billion over this period.

Asia Pacific dominated with 80% of global GMV in 2026, driven by China, India, Japan, and South Korea. Canada's e-commerce market reached an estimated US$ 89.4 billion in 2024, with online retail accounting for 6.1% of total retail sales. India's industrial and warehousing leasing demand surged 63% year-on-year to a record 27.1 million square feet in H1 2025, with 3PL players at 32% and e-commerce firms at 25% of leasing demand, according to CBRE. The proliferation of digital commerce platforms and cloud-based logistics systems intensifies real-time data processing requirements, directly elevating the demand for proactive maintenance, hardware lifecycle management, and network reliability services across hyperscale and enterprise data Centres.

Market Restraining Factors

High Cost of Specialised Maintenance Expertise and Third-Party Service Dependency

The data center support & maintenance services market faces structural cost constraints as specialised maintenance of AI-accelerated servers, high-density GPU platforms, and advanced networking equipment demands certified expertise that is both scarce and expensive. Organisations operating heterogeneous multi-vendor infrastructure face compounding service contract costs, particularly for hardware beyond original equipment manufacturer warranty periods.

For smaller enterprise operators and emerging market deployments, total maintenance expenditure can represent a disproportionate share of IT operational budgets, leading to underinvestment in proactive maintenance programs and increased exposure to unplanned downtime risk, which the Uptime Institute estimates costs enterprises an average of over US$ 9,000 per minute of outage.

Supply Chain Constraints for Spare Parts and Extended Hardware Lifecycle Management

Maintaining ageing and heterogeneous data Centre hardware increasingly depends on the availability of legacy spare parts, which are subject to global semiconductor supply chain volatility and extended procurement lead times. The global semiconductor market experienced a contraction of 8.2% in 2023 due to inventory corrections, which cascaded into delays for replacement components across server and networking equipment categories.

As data centre operators extend hardware lifespans beyond OEM support windows to optimise capital expenditure, the complexity of sourcing compatible components across third-party maintenance networks intensifies, creating delivery risk, cost escalation, and service quality variability that constrain uniform service delivery across the global data center support & maintenance services market.

Key Market Opportunities

Healthcare Digitalisation and Clinical IT Infrastructure Expansion Create High-Value Maintenance Procurement Pipelines

Healthcare institutions represent one of the most strategically valuable and structurally underserved customer segments for the data center support & maintenance services market, as hospitals, diagnostic chains, and public health agencies accelerate the deployment of clinical data management systems, electronic health record platforms, and AI-assisted diagnostic infrastructure that demand continuous operational reliability.

Healthcare data environments are governed by stringent regulatory frameworks, including HIPAA in the United States and equivalent data protection standards globally, creating mandatory requirements for documented maintenance protocols, audit trails, and uptime assurance programs.

China's internet-connected healthcare services recorded strong adoption growth by December 2024, while India's digital health initiatives under the National Health Mission are expanding clinical IT deployments across tier-2 and tier-3 cities. The European Union's Eurostat data confirms that 52% of EU individuals used electronic identification to access digital public services in 2025, including healthcare portals, amplifying the criticality of supporting institutional IT infrastructure.

Healthcare's transition toward integrated care delivery platforms, telemedicine, and real-time patient data analytics significantly elevates the availability and performance requirements for supporting server and networking infrastructure within the data center support & maintenance services market, creating long-term, contract-based maintenance revenue streams for providers.

Government and Defence Digital Modernisation Programs Drive Public Sector Maintenance Procurement

Government-led digital infrastructure modernisation programs across major economies represent a large-scale and policy-secured demand channel for the data center support & maintenance services market, as public agencies upgrade legacy IT estate, deploy sovereign cloud infrastructure, and invest in defence-grade data Centre resilience programs. In the United States, federal and state-level digital modernisation initiatives include defence cloud transformation and smart infrastructure programs that require advanced asset lifecycle analytics and supply chain-integrated spare parts logistics for large government data Centre campuses.

India's government launched innovation programs under Digital India with a combined funding outlay of approximately INR 800 crore, alongside the BharatNet program serving 2.13 lakh Gram Panchayats, collectively expanding the public sector IT asset base requiring professional maintenance coverage. The EU's public sector digital services adoption, with 52% of individuals using eID in 2025, reflects the broad deployment of government IT infrastructure that requires long-term operational support. India's Press Information Bureau confirmed that 95.15% of villages had access to 3G or 4G connectivity as of March 2024, with network infrastructure build-out ongoing, creating addressable support and maintenance opportunities for public sector IT operators within the Data Center Support & Maintenance Services Market.

Category-wise Analysis

Component Type Insights

The Servers segment holds the dominant position likely to account for approximately 52% of total revenue in 2026. Server maintenance services encompass firmware updates, thermal management, hardware diagnostics, predictive failure analytics, and component replacement across general-purpose, blade, rack-mounted, and GPU-accelerated server platforms.

The exponential growth of compute-intensive workloads, including AI and machine learning training, high-performance computing, and real-time analytics, has amplified hardware complexity, thermal loads, and component failure risk, significantly elevating the demand for proactive server maintenance and lifecycle management services.

Dell Technologies launched its Rack 7000 integrated rack-scalable server and storage system in 2024, reflecting the accelerating complexity of next-generation server architectures that require specialised maintenance expertise. China's data-intensive platform ecosystem, serving over one billion users across social networking, e-government, and generative AI applications, relies on massive server infrastructure requiring continuous operational support.

With virtualisation density and GPU-accelerated workloads per server rack continuing to intensify, the server maintenance segment is expected to retain its leadership position throughout the forecast period.

Networking Equipment represents the fastest-growing component segment within the global data center support & maintenance services market, driven by the exponential scale-up of data Centre interconnect bandwidth, the transition to 400G and 800G Ethernet switching fabrics, and the proliferation of software-defined networking architectures that require specialised configuration management and hardware support. The data Centre networking equipment market was valued at US$ 24.3 billion in 2024 and is projected to reach US$ 74.0 billion by 2032, reflecting the sustained capital investment in networking infrastructure that subsequently generates maintenance and support revenue.

Data Centre Type Insights

Hyperscale Data Centres command the largest share of the global data center support & maintenance services market, accounting for approximately 48% of total revenue in 2026. Hyperscale operators managing hundreds of thousands of server nodes, petabyte-scale storage systems, and high-density networking fabrics require highly structured, SLA-governed maintenance programs that encompass predictive diagnostics, automated hardware decommissioning, and supply chain-integrated spare parts logistics.

The global B2B e-commerce GMV trajectory toward US$ 36,163 billion by 2026, combined with cloud platform expansion across APAC, North America, and Europe, directly sustains capital investment and operational maintenance demand at hyperscale facilities.

China's internet ecosystem, with over one billion active users across multiple platform categories and strong government support for 5G and gigabit fibre, generates continuous hyperscale data processing demand requiring enterprise-grade maintenance contracts. APAC's B2B e-commerce dominance at 80% of global GMV reinforces the region's hyperscale data Centre operational intensity.

Advanced asset lifecycle analytics, automated decommissioning workflows, and IoT-enabled predictive maintenance are increasingly standard requirements within hyperscale maintenance service agreements, defining the high-specification procurement environment that sustains this segment's market leadership.

Enterprise data centres represent the fastest-growing data center type segment within the data center support & maintenance services market, as organisations across BFSI, healthcare, logistics, and manufacturing accelerate on-premises and hybrid infrastructure deployments to support digital transformation initiatives while maintaining data sovereignty and regulatory compliance. Enterprise operators upgrading ageing server and networking assets to support AI workloads, IoT data ingestion, and real-time analytics require comprehensive third-party maintenance programs that extend hardware lifecycles beyond OEM warranty periods.

Industry Insights

IT & Telecommunications holds the largest Industry share in the Global Data Center Support & Maintenance Services Market, accounting for approximately 34% of revenue in 2026. Telecommunications operators, cloud service providers, and managed IT service companies operate some of the most extensive and complex data Centre estates globally, requiring continuous maintenance coverage across server farms, networking fabrics, and storage systems that support real-time communication services and digital platform delivery. India's telecom sector generated gross revenue of US$ 43.42 billion in FY25, with wireless services accounting for over 96% of total subscriptions, reinforcing the scale of IT infrastructure supporting national telecom operations.

The EU's information and communication services sector employed nearly 7.2 million people and generated approximately €667 billion in value added in 2022, representing 6.6% of total EU business economy value added, according to Eurostat. The global semiconductor market's projected expansion to US$ 975 billion in 2026, driven by AI and 5G investment cycles, is directly expanding the compute and networking infrastructure installed base within IT and telecom data Centres, amplifying professional maintenance requirements across the segment.

Healthcare represents the fastest-growing Industry segment in the Global Data Center Support & Maintenance Services Market, driven by the accelerating deployment of electronic health record systems, AI-assisted diagnostics, telemedicine infrastructure, and clinical data analytics platforms across hospital networks, diagnostic laboratories, and public health agencies globally. Healthcare IT environments demand the highest levels of data availability and system uptime, given the patient safety implications of infrastructure failure, creating strong demand for comprehensive, SLA-backed maintenance contracts.

Regional Insights and Trends

Asia Pacific Data Center Support & Maintenance Market Trends

Asia Pacific holds approximately 30% of global revenue in the data center support & maintenance services market and represents the region with the highest forward growth momentum, anchored by China, India, Japan, South Korea, and Australia. China's internet ecosystem reached 1.108 billion users as of December 2024, with mobile internet users at 99.7% of all netizens and data-intensive services including generative AI reaching 249 million users, according to CNNIC. Online payment users surpassed 1.029 billion, and e-government users exceeded 1.004 billion, reflecting the scale of digital platform infrastructure requiring continuous data Centre operational support.

India's internet subscriber base reached 954.40 million as of March 2024, expanding from 251.59 million in March 2014 at a CAGR of 14.26%, according to the Press Information Bureau. BharatNet has connected 2.13 lakh Gram Panchayats, while 5G networks already contribute nearly a quarter of total wireless data usage, per the Telecom Regulatory Authority of India. India's industrial and warehousing leasing hit a record 39.5 million square feet in 2024, with 3PL and e-commerce operators deploying IoT and automation systems creating distributed enterprise IT infrastructure. APAC's B2B e-commerce GMV is projected to represent 80% of the global total by 2026, sustaining hyperscale and enterprise data Centre expansion that directly generates professional maintenance procurement across the region.

North America Data Center Support & Maintenance Services Market Trend

North America holds the largest regional share in the data center support & maintenance services market, accounting for approximately 38% of global revenue, with the United States as the dominant national market. Federal and state-level digital modernization programs, including defense cloud transformation and smart infrastructure initiatives, create large-scale government procurement pipelines for data Centre maintenance and lifecycle management services.

North America's share of global B2B e-commerce GMV stood at approximately 13.7% of a projected US$ 36,163 billion total by 2026, reflecting an absolute market value exceeding US$ 4.9 trillion, underpinned by advanced digital procurement infrastructure and cloud-native enterprise IT environments. Canada's e-commerce market reached US$ 89.4 billion in 2024 and is projected to reach US$ 104 billion by 2029, with continued expansion in cloud-integrated retail and logistics platforms driving enterprise data centre maintenance requirements. The U.S. remains the global innovation leader in predictive maintenance technologies, AI-assisted hardware diagnostics, and remote monitoring platforms, reinforcing North America's competitive leadership in high-value, technology-differentiated maintenance service delivery within the Data Center Support & Maintenance Services Market.

Europe Data Center Support & Maintenance Services Market Market Trend

Europe holds approximately 20% of global revenue with Germany, the United Kingdom, France, and the Netherlands serving as primary demand centers. According to Eurostat, the EU information and communication services sector comprised 1.4 million enterprises, employed 7.2 million people, and generated €667 billion in value added in 2022, with Germany accounting for 22.8% of EU sectoral value added and 22.6% of employment. This scale of digital economy activity sustains large enterprises and colocation data Centre estates across the region requiring structured maintenance programs.

Eurostat's 2025 digital economy data confirmed that 94% of EU individuals used the internet, with 74% ordering or buying online, and one in three using generative AI tools, reflecting deep enterprise and consumer digital engagement that amplifies data Centre operational demand. The Netherlands and Luxembourg reported 99% household internet access in 2025, among the highest globally, reflecting mature digital infrastructure requiring sustained maintenance investment.

Competitive Landscape

The global data center support & maintenance services market exhibits a moderately consolidated structure, positioned between consolidated and fragmented, with a defined tier of multinational OEM-aligned and independent service providers commanding significant revenue share. Leading players include IBM, Hewlett Packard Enterprise, Dell Technologies, Cisco Systems, Vertiv Holdings, and Schneider Electric, each competing across server, storage, networking, and critical power maintenance service categories.

Competitive differentiation is anchored by proprietary remote monitoring platforms, certified engineer networks, OEM parts supply agreements, and SLA performance guarantees. The absence of a single dominant provider across all hardware categories and geographies confirms the market's moderately consolidated nature.

The dominant strategic themes in the Global Data Center Support & Maintenance Services Market are predictive intelligence, ecosystem partnership models, and geographic service network expansion. Market leaders differentiate through AI-powered remote monitoring, digital twin-enabled asset management, and OEM-certified parts supply ecosystems. Emerging business models include outcome-based SLA contracts, multi-vendor independent maintenance aggregation platforms, and subscription-based hardware lifecycle management services targeting hyperscale and enterprise operators.

Key Developments :

- In January 2026, Vertiv announced the launch of Vertiv™ Next Predict, an AI-powered predictive maintenance service for data centres that leverages machine learning to proactively identify and mitigate infrastructure risks across power, cooling, and IT systems, enhancing uptime and operational efficiency.

- In June,2025, Cisco announced a suite of AI-ready data Centre innovations, including Unified Nexus Dashboard for centralized infrastructure management, intelligent network automation, and enhanced AI POD architectures, enabling improved monitoring, operational efficiency, and scalable infrastructure support across hyperscale and enterprise data Centres.

- March 2025, Cisco Systems, Inc. & NVIDIA: Cisco announced a collaboration with NVIDIA to develop the Cisco Secure AI Factory, a next-generation data Centre architecture integrating AI infrastructure, networking, and embedded security layers to simplify deployment, management, and protection of AI workloads across enterprise-scale environments.

Companies Covered in Data Center Support & Maintenance Services Market

- Husqvarna AB

- ANDREAS STIHL AG & Co. KG

- Honda Motor Co., Ltd.

- Deere & Company

- Robert Bosch GmbH

- Positec Technology Co., Ltd.

- STIGA S.p.A. (3i Group plc)

- Globe Tools Group Co., Ltd.

- Segway Inc. (Ninebot Ltd.)

- Shenzhen Mammotion Technologies Co., Ltd.

- EcoFlow Technology Inc.

- FJDynamics International Ltd.

- Yamabiko Corporation

Frequently Asked Questions

The global data center support & maintenance services market is projected to be valued at US$ 7.5 Bn in 2026.

The Hyperscale Data Centres segment is expected to account for approximately 48% of the Global Data Center Support & Maintenance Services Market by Data Centre Type in 2026.

The market is expected to witness a CAGR of 10.5% from 2026 to 2033.

The Data Center Support & Maintenance Services Market is primarily driven by rapid global internet adoption, large-scale digital infrastructure expansion, accelerating telecom and broadband investments, and the exponential growth of data-intensive applications such as e-commerce, cloud computing, and AI, all of which significantly increase data centre operational complexity, hardware density, and demand for continuous uptime and lifecycle maintenance services.

Key market opportunities in the Data Center Support & Maintenance Services Market include rising healthcare digitalization driven by electronic health records, telemedicine, and AI-enabled diagnostics requiring highly reliable, compliance-driven IT infrastructure and expanding government and defense digital modernization programs across regions like the US, India, and the EU, which are increasing sovereign cloud adoption, upgrading legacy IT systems, and creating long-term, contract-based demand for secure, continuously maintained data center infrastructure.

Key players in the Data Center Support & Maintenance Services Market include IBM, Hewlett Packard Enterprise, Dell Technologies, Cisco Systems, Vertiv Holdings, and Schneider Electric.