- Plastics, Polymers & Resins

- Plasticizers Market

Plasticizers Market Size, Share, and Growth Forecast 2026 - 2033

Plasticizers Market by Plasticizer Type (Phthalate Plasticizers, Non-Phthalate Plasticizers), Application (Flooring & Wall Coverings, Wires & Cables, Coated Fabrics, Consumer Goods, Films & Sheets, Packaging Materials, Automotive Components, Medical Devices, Toys and Childcare Articles), Industry (Construction & Building, Automotive, Electrical & Electronics, Others), and Regional Analysis, 2026 - 2033

Plasticisers Market Size and Trend Analysis

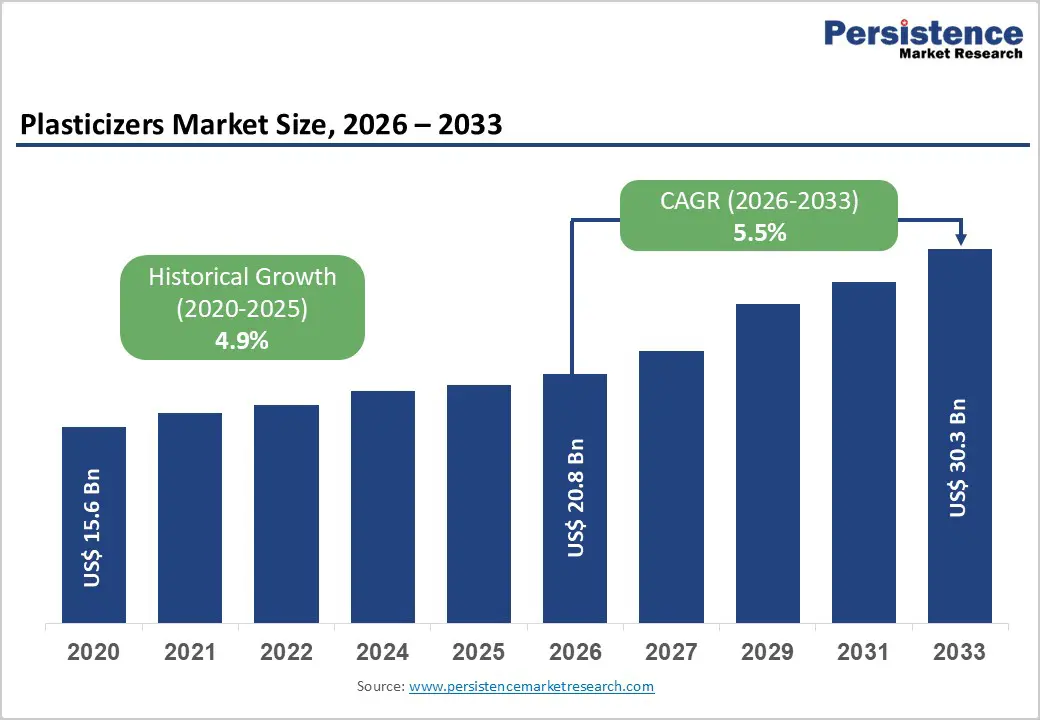

The global plasticizers market size is expected to be valued at US$ 20.8 billion in 2026 and projected to reach US$ 30.3 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.This sustained expansion is driven by accelerating PVC consumption across construction, automotive, and packaging industries, combined with the structural transition from phthalate to non-phthalate formulations driven by tightening global chemical safety regulations.

Rapid infrastructure development in Asia Pacific and the Middle East & Africa, the two fastest-growing demand regions is amplifying consumption of flexible PVC in flooring, wires and cables, and coated fabrics, while the regulatory-driven demand shift toward bio-based and non-phthalate plasticisers is creating premium product categories with above-average growth rates and margin profiles.

Key Industry Highlights

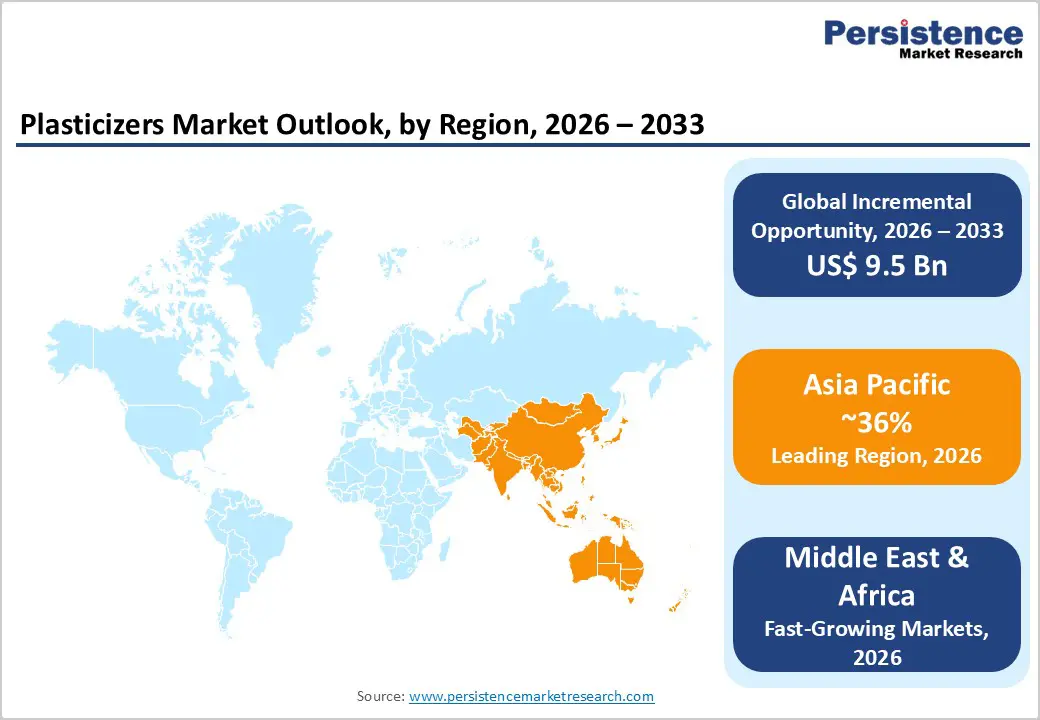

- Leading Region: Asia Pacific leads the global plasticisers market with approximately 36% share in 2025, anchored by China's world-leading PVC production and consumption base, and rapid construction and manufacturing growth across India, Vietnam, and Indonesia.

- Fastest Growing Market: Middle East & Africa is the fastest growing plasticizers region through 2033, driven by large-scale infrastructure investment programs in Saudi Arabia's Vision 2030, UAE urban development, and Sub-Saharan Africa's expanding construction and electrification activity.

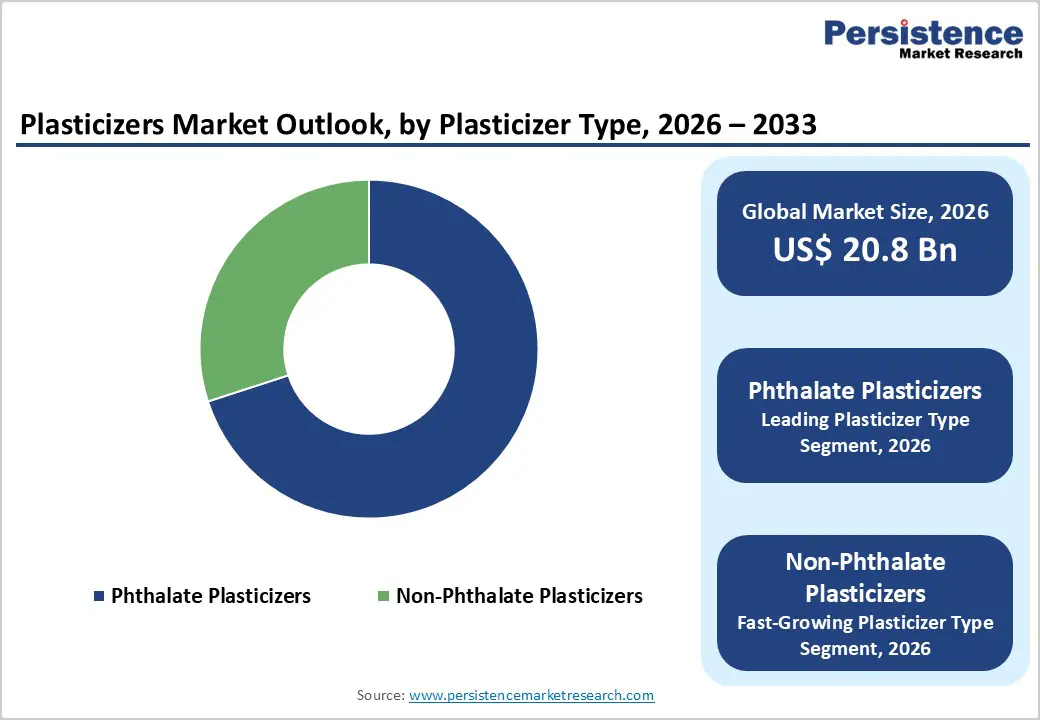

- Dominant Plasticizer Segment: Phthalate plasticizers hold approximately 63% of the global market share in 2025, sustained by cost competitiveness and established processing compatibility in high-volume flooring, cable, and general-purpose flexible PVC applications across developing economies.

- Fastest Growing Plasticizer Segment: Non-phthalate plasticizers are projected to grow at 6.0% CAGR through 2033, driven by EU REACH SVHC mandates, U.S. CPSIA toy and medical device restrictions, and brand owner sustainability commitments, accelerating formulation transition across regulated applications.

- Key Opportunity: Bio-based and medical-grade non-phthalate plasticisers offer the highest-margin expansion opportunity, commanding premium pricing from ESG-aligned packaging brands and medical device OEMs mandating DEHP-free PVC formulations for patient safety compliance.

DRO Analysis

Drivers - Accelerating PVC Demand from Construction, Infrastructure, and Electrical Sectors

Plasticizers with flexible PVC, their dominant end-use platform, are structural beneficiaries of global construction and infrastructure investment cycles, and market participants supplying these sectors can expect sustained volume growth anchored in government-backed spending programs.

The Global Construction Perspectives project forecasts global construction output to grow by 42% to reach US$ 15.2 trillion by 2030, with emerging economies in Asia, Africa, and Latin America driving the majority of incremental demand. Flexible PVC is the single largest application of plasticizers, used in flooring, wall coverings, roofing membranes, and wire insulation, all categories growing in parallel with construction activity.

The International Electrotechnical Commission (IEC) estimates continued growth in global electrical infrastructure buildout, directly stimulating wires and cables PVC compound demand. For plasticizer producers supplying construction-adjacent value chains, this macroeconomic alignment represents a durable, policy-backed volume growth engine through 2033.

Regulatory-Driven Substitution from Phthalate to Non-Phthalate and Bio-Based Plasticizers

The accelerating regulatory restriction of phthalate plasticizers, particularly DEHP, DBP, and BBP, across the European Union, United States, Japan, and increasingly South Korea and China, is generating a structurally defined demand pull for non-phthalate alternatives that reward chemical companies with established DINCH, DOTP, citrate ester, and bio-based product portfolios. The EU REACH Regulation has placed DEHP, DBP, BBP, and DIBP on the Substances of Very High Concern (SVHC) authorization list, effectively mandating transition across food contact, medical device, toy, and childcare applications in Europe.

The U.S. Consumer Product Safety Improvement Act (CPSIA) similarly restricts phthalate content in children's toys and childcare articles to 0.1% by weight. These regulatory mandates create a durable, compliance-driven substitution cycle that, independent of macroeconomic conditions, will sustain non-phthalate demand growth at above-market CAGR through 2033.

Restraints - Volatile Crude Oil and Petrochemical Feedstock Prices Destabilizing Plasticizer Margins

Plasticizer production, particularly for phthalate and adipate types, is directly exposed to the price volatility of petrochemical feedstocks, including 2-ethylhexanol (2-EH), orthoxylene, and phthalic anhydride, all of which are derivatives of crude oil and naphtha.

The International Energy Agency (IEA) data confirms that crude oil prices exhibited extreme volatility between 2020 and 2024, ranging from negative territory to over US$ 120/barrel. These feedstock price swings compress producer margins when downstream PVC compounders and end-users resist equivalent price pass-through, particularly in commodity-segment applications where contract structures lag spot market moves. For mid-tier producers without integrated feedstock positions, this creates structural profitability risk that can deter capacity investment.

Intensifying Health and Environmental Scrutiny, Creating Product Liability and Reformulation Costs

Beyond formal regulatory restrictions, growing scientific and public health scrutiny of plasticizer migration from PVC products into food, drinking water, and human tissue is creating reputational risk and compounding reformulation investment requirements for producers whose product portfolios remain phthalate-heavy.

The European Chemicals Agency (ECHA) continues to evaluate additional phthalate compounds for SVHC listing, creating regulatory uncertainty that depresses long-term investment in phthalate capacity. For producers serving healthcare and food packaging applications segments where material safety documentation requirements are most rigorous, the cost of maintaining comprehensive toxicological data packages for legacy phthalate grades while simultaneously funding non-phthalate R&D creates a dual cost burden that constrains innovation investment.

Opportunities - Bio-Based and Sustainable Plasticizer Development Capturing Premium ESG-Aligned Demand

Bio-based plasticizers derived from vegetable oils, citric acid, and succinic acid represent the highest-growth, highest-margin product development opportunity in the plasticizers market, positioned at the convergence of regulatory pressure, brand owner sustainability commitments, and consumer preference for products with verifiable environmental credentials.

The European Bioplastics Association reports that bio-based chemical production capacity in Europe is expanding at an accelerating pace, with flexible PVC applications identified as a priority target market for bio-derived additive substitution. Major consumer goods brands, including Unilever, Nestlé, and Procter & Gamble, have published supply chain decarbonization commitments that explicitly require bio-based or recycled content in packaging materials. Companies, including Cargill, Eastman Chemical, and Evonik, are already commercialising bio-based plasticizer platforms and are best positioned to capture this demand as it scales from niche to mainstream.

Expanding Healthcare and Medical Device Applications Driving High-Value Non-Phthalate Demand

The healthcare sector represents the most structurally attractive high-value application growth vector for non-phthalate plasticizer producers, as ageing populations in North America, Europe, and East Asia drive sustained expansion in medical device manufacturing, IV bags, blood storage containers, surgical tubing, and respiratory equipment, where the transition away from DEHP is both regulatory-mandated and patient-safety-driven.

The World Health Organisation (WHO) and the U.S. Food and Drug Administration (FDA) have both issued guidance documents recommending the replacement of DEHP-plasticised PVC in medical devices used in neonatal intensive care, dialysis, and chemotherapy applications, effectively creating a compliance-driven specification requirement for DINCH, TOTM, and other non-phthalate alternatives.

The Global Medical Devices Association data confirms annual growth in medical device manufacturing output of approximately 5-7% per year in key producing markets, including Germany, the United States, Ireland, and Malaysia all demanding non-phthalate compliant PVC formulations. This application commands a meaningful price premium over commodity-grade plasticiser products.

Category-wise Analysis

Plasticizer Type Insights

Phthalate Plasticizers command the leading share of approximately 63% of the global plasticizers market by type in 2025, reflecting their entrenched position across high-volume PVC applications, including flooring, wire insulation, automotive underbody coatings, and non-food-contact packaging, where cost competitiveness, established processing compatibility, and extensive application knowledge bases sustain their commercial dominance. DEHP, DINP, and DIDP together represent the largest-volume phthalate grades, with DINP having largely displaced DEHP in general-purpose flexible PVC applications following the EU REACH authorisation requirements.

The European Council for Plasticisers and Intermediates (ECPI) confirms that phthalates meeting current regulatory requirements, specifically DINP and DIDP, for general-use applications, remain the lowest-cost performance option for flexible PVC compounders globally. This leadership is stable in volume terms, though share is structurally eroding in regulated application categories as non-phthalate substitution accelerates.

The fastest growing type is Non-Phthalate Plasticizers, projected at a 6.0% CAGR through 2033, driven by regulatory mandates, consumer brand sustainability commitments, and the expansion of high-value medical device and food-contact applications that require demonstrably safer additive formulations.

Application Insights

Flooring & Wall Coverings represents the leading application segment with approximately 26% of global plasticizer demand in 2025, underpinned by the massive and structurally growing global market for resilient vinyl flooring, one of the most plasticizer-intensive PVC applications, consuming 30-40 parts plasticizer per 100 parts PVC in standard formulations.

The World Floor Covering Association (WFCA) and industry data from the European Resilient Flooring Manufacturers Association (ERFMI) confirm that luxury vinyl tile (LVT) and vinyl sheet flooring have been the fastest-growing floor covering category globally for over a decade, driven by superior cost-performance ratio versus natural materials and expanding construction activity. Urbanisation trends in China, India, and Southeast Asia continue to create high-volume demand for affordable, durable vinyl flooring in residential and commercial construction, sustaining this segment's dominant application position.

The fastest growing application is Medical Devices, where regulatory-mandated transition to non-phthalate formulations and expanding healthcare infrastructure investment in emerging economies are simultaneously driving above-market demand growth for high-purity, DEHP-free plasticizer grades.

Industry Insights

Construction & building is the dominant industry with approximately 34% of global plasticizer consumption in 2025, driven by the irreplaceable role of flexible PVC, the single largest plasticizer end-use platform in flooring, wall coverings, roofing membranes, window profiles, pipes, and sealing systems that are foundational to modern construction. The United Nations Environment Programme (UNEP) estimates that the construction sector accounts for approximately 40% of global materials consumption, with PVC representing one of the most widely specified polymer materials due to its durability, fire resistance, and processability.

Government-led infrastructure investment programs in China, India, Indonesia, and across the Middle East are providing sustained structural demand tailwinds for construction-grade plasticizer volumes through the forecast period. This segment's dominance is structurally stable given the capital-intensive, multi-decade lifecycle of construction infrastructure investment cycles.

The fastest growing end-use industry is Healthcare, driven by ageing demographics, rising medical device production in both developed and emerging economies, and the regulatory acceleration of DEHP-to-non-phthalate substitution in IV bags, blood storage containers, surgical tubing, and respiratory care equipment.

Regional Insights

North America Plasticizers Market Trends and Insights

North America holds approximately 19% of the global plasticizers market in 2025, shaped by mature PVC construction demand, stringent CPSIA and EPA phthalate regulations accelerating non-phthalate adoption, and a growing bio-based plasticizer innovation ecosystem anchored in the United States. The region is a global leader in non-phthalate and speciality plasticizer R&D, with above-average growth in medical device and food packaging applications.

U.S. Plasticizers Market Size

The United States accounts for approximately 78% of North America's plasticizer market in 2025, driven by its large PVC construction, automotive, and healthcare manufacturing base. The CPSIA phthalate restrictions and FDA medical device guidance are the primary demand drivers for non-phthalate grades, with Eastman Chemical and Lanxess among the leading domestic suppliers. Steady growth is forecast through 2033.

Europe Plasticizers Market Trends and Insights

Europe accounts for approximately 21% of the global plasticizers market in 2025, representing the most advanced regulatory environment for phthalate substitution globally. The EU REACH SVHC authorisation framework has structurally elevated non-phthalate demand across all end-use applications, while Germany's strong PVC wire, cable, and automotive compound manufacturing base sustains overall regional volume. Bio-based plasticizer adoption is advancing at the fastest pace globally in European markets.

Germany Plasticizers Market Size

Germany represents approximately 25% of Europe's plasticizer market in 2025, underpinned by its leading position in automotive PVC compounds, wire and cable insulation, and industrial flooring applications. BASF and Evonik Oxeno operate significant plasticizer production facilities in Germany, supplying both domestic compounders and pan-European customers. Growth through 2033 will be led by non-phthalate and bio-based grades compliant with EU REACH.

U.K. Plasticizers Market Size

The U.K. holds approximately 14% of Europe's plasticizer market in 2025, supported by demand from construction, medical device manufacturing, and consumer goods sectors. Post-Brexit, the U.K. has maintained regulatory alignment with EU phthalate restrictions under the UK REACH framework, sustaining the transition to non-phthalate grades. Medical device plasticizer demand anchored by Ireland's medtech manufacturing cluster is a secondary growth driver. Steady growth is expected through 2033.

France Plasticizers Market Size

France accounts for approximately 12% of Europe's plasticizer market in 2025, with demand concentrated in construction flooring, packaging films, and automotive applications. France's ANSES (National Agency for Food, Environmental and Occupational Health Safety) has historically taken a precautionary stance on phthalate exposures, reinforcing early non-phthalate adoption. Specialty and bio-based plasticizer demand is growing in food packaging and medical segments. Growth is expected to be steady through 2033.

Asia Pacific Plasticizers Market Trends and Insights

Asia Pacific leads all regions with approximately 36% of the global plasticizers market in 2025, anchored by China's massive PVC production and consumption base, the world's largest, alongside rapid construction and manufacturing growth in India, Vietnam, Indonesia, and South Korea. China alone accounts for approximately 55% of the Asia Pacific's plasticizer consumption, with DOP and DINP the dominant grades across domestic flooring, cable, and packaging applications. The region is forecast to sustain above-global-average growth through 2033 as urbanisation and infrastructure investment continue.

India Plasticizers Market Size

India holds approximately 12% of the Asia Pacific's plasticizer market in 2025, driven by rapid construction activity, PVC pipe and cable demand, and growing consumer goods manufacturing. The India Brand Equity Foundation (IBEF) confirms sustained infrastructure investment growth, directly translating into PVC and plasticizer demand. KLJ Group is the dominant domestic plasticizer producer, with significant capacity serving both Indian and export markets. Growth is forecast to accelerate through 2033.

Japan Plasticizers Market Size

Japan accounts for approximately 9% of Asia Pacific's plasticizer market in 2025, characterised by a mature PVC market and stringent phthalate regulations under the Japan Chemical Substances Control Law. Non-phthalate grades, including DINCH and DOTP, have high penetration in Japanese medical device and food packaging applications. Kao Corporation and DIC Corporation are significant domestic suppliers. Japan's market is growing steadily, driven by premium non-phthalate and bio-based plasticizer applications.

Southeast Asia Plasticizers Market Size

Southeast Asia contributes approximately 11% of the Asia Pacific's plasticizer market in 2025, with growth concentrated in Vietnam, Indonesia, Malaysia, and Thailand, all geographies benefiting from manufacturing FDI inflows and rapid construction expansion. NAN YA PLASTICS CORPORATION and regional compounders are key market participants. The sub-region is forecast to grow at above-regional-average rates through 2033, supported by urbanisation, consumer goods manufacturing growth, and expanding electrical infrastructure investment.

Competitive Landscape

The global plasticizers market is moderately consolidated, with a tier of large integrated chemical producers, such as BASF, Eastman Chemical, Lanxess, Evonik Oxeno, and LG Chem, competing alongside regional volume producers, including KLJ Group, NAN YA PLASTICS, and UPC Technology.

Key differentiators among market leaders include non-phthalate and bio-based product portfolio breadth, backward integration into feedstocks, application-specific technical service, and regulatory affairs capability to navigate multi-jurisdiction compliance requirements. Dominant strategic themes include capacity expansion in the Asia Pacific, accelerated R&D investment in bio-based and speciality plasticiser platforms, and sustainability-linked product positioning targeting ESG-committed consumer goods and packaging brand owners.

Key Developments:

- In January 2026 - The Company launched Vertiv™ Next Predict, an AI-powered predictive maintenance managed service designed for data centres, leveraging machine learning-based anomaly detection, continuous condition monitoring, and root-cause analysis to anticipate equipment failures across power, cooling, and IT systems. The solution enables a shift from schedule-based to data-driven maintenance, improving uptime and operational resilience in high-density, AI-driven infrastructure environments.

- In June 2025, Siemens AG deployed its Senseye Predictive Maintenance solution at Sachsenmilch Leppersdorf GmbH, enabling AI-driven analysis of vibration, temperature, and operational data to detect early-stage equipment failures, including pump end-of-life prediction. The successful pilot improved uptime in a high-throughput 24/7 production environment and is being further scaled through integration with SAP Plant Maintenance, demonstrating the growing role of AI-powered predictive maintenance in continuous-process industries.

Plasticizers Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 15.6 billion |

| Current Market Value (2026) | US$ 20.8 billion |

| Projected Market Value (2033) | US$ 30.3 billion |

| CAGR (2026 - 2033) | 5.5% |

| Leading Region | Asia Pacific, 36% market share (2026) |

| Dominant Plasticizer Type | Phthalate Plasticizers, 63% share (2026) |

| Top-Ranking Application | Flooring & Wall Coverings, 26% share (2026) |

| Incremental Opportunity | US$ 9.5 billion (Absolute Dollar Opportunity) |

Companies Covered in Plasticizers Market

- Eastman Chemical Company

- KLJ Group

- BASF SE

- Polynt S.p.A.

- NAN YA PLASTICS CORPORATION

- Kao Corporation

- LG Chem

- Cargill, Incorporated

- LANXESS AG

- Aekyung Chemical Co., Ltd.

- Solvchem Custom Pack

- Evonik Oxeno GmbH & Co. KG

- UPC Technology Corporation

- Avient Corporation

- DIC CORPORATION

- Perstorp Group

- Valtris Specialty Chemicals

- OQ Chemicals GmbH

- Shandong Qilu Plasticizers Co., Ltd.

Frequently Asked Questions

The global Plasticizers market is valued at US$ 20.8 billion in 2026. This growth is driven by accelerating PVC consumption in construction, electrical infrastructure, and packaging sectors globally, combined with the regulatory-mandated transition from phthalate to non-phthalate plasticizer formulations in developed economies.

The primary demand drivers include global construction output growth projected to reach US$ 15.2 trillion by 2030, which is significantly boosting PVC and plasticiser demand across flooring, cables, roofing, and wall applications. The second key driver is regulatory substitution of restricted phthalates under EU REACH and U.S. CPSIA, driving strong adoption of safer alternatives like DINCH, DOTP, citrate esters, and bio-based plasticizers.

Asia Pacific leads the global Plasticizers market with approximately 36% of market share in 2025. Its leadership is anchored by China's position as the world's largest PVC producer and consumer, combined with rapid construction, electrical infrastructure, and consumer goods manufacturing expansion in India, Vietnam, Indonesia, and South Korea. KLJ Group, NAN YA PLASTICS, and Kao Corporation are among the prominent regional suppliers serving this demand base.

The key growth opportunity lies in bio-based and medical-grade non-phthalate plasticizers, driven by sustainability mandates from consumer brands like Unilever, Nestlé, and P&G, along with regulatory pressure from the WHO and the FDA to replace DEHP in medical devices. These combined sustainability and healthcare requirements make this segment the highest-margin growth area through 2033.

The Leading Companies in the Global Plasticizers Market Include Eastman Chemical Company, BASF SE, LANXESS AG, Evonik Oxeno Gmbh & Co. KG, LG Chem, Nan Ya Plastics Corporation, Kao Corporation, Cargill Incorporated, Polynt S.P.A., DIC CORPORATION, Avient Corporation, UPC Technology Corporation, Perstorp Group, And Valtris Speciality Chemicals.