- Plastics, Polymers & Resins

- Styrene Acrylic Market

Styrene Acrylic Market Size, Share and Growth Forecast, 2026 - 2033

Styrene Acrylic Market by Application (Paints & Coatings, Adhesives & Sealants, Construction Chemicals, Paper & Packaging, Textiles), Product Type (Styrene Acrylic Copolymers, Emulsions, Others), and Regional Analysis for 2026 - 2033

Styrene Acrylic Market Share and Trends Analysis

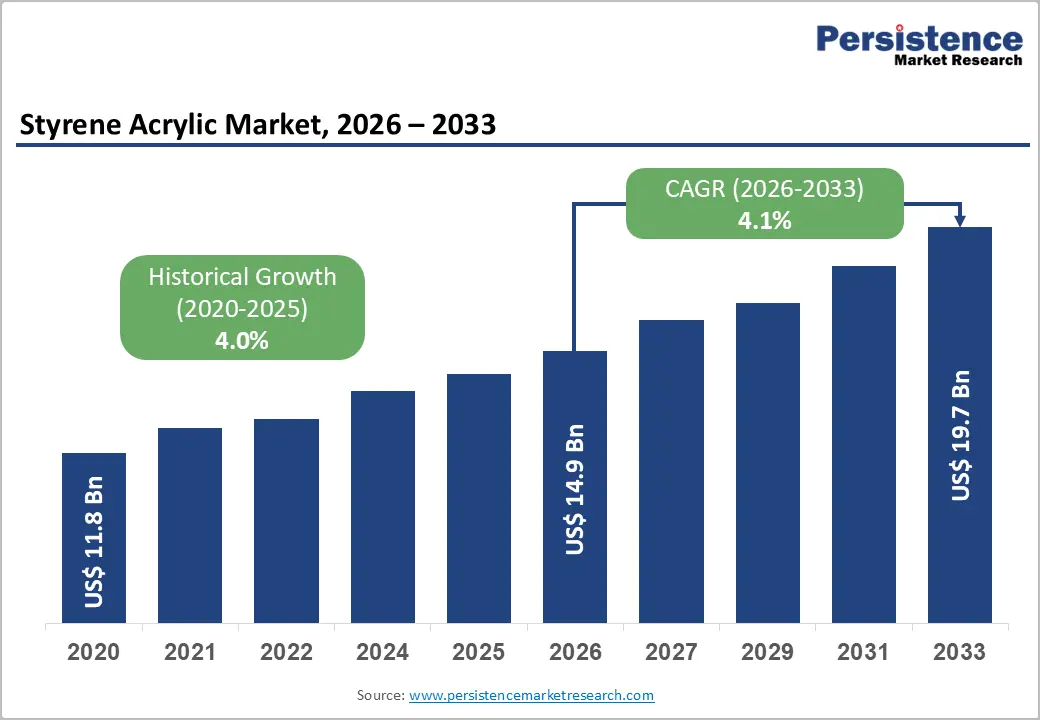

The global styrene acrylic market size is likely to be valued at US$ 14.9 billion in 2026 and is projected to reach US$ 19.7 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026 - 2033, driven by rising demand across paints and coatings, adhesives and sealants, and construction chemicals, supported by rapid urbanization and infrastructure expansion in emerging economies.

Further momentum is driven by the growing shift toward low-VOC, water-based polymer emulsions in response to stringent environmental regulations from organizations such as the U.S. Environmental Protection Agency and REACH. In addition, expanding industrial applications in sectors such as packaging and textiles are contributing to the growing demand for high-performance styrene-acrylic formulations.

Key Industry Highlights:

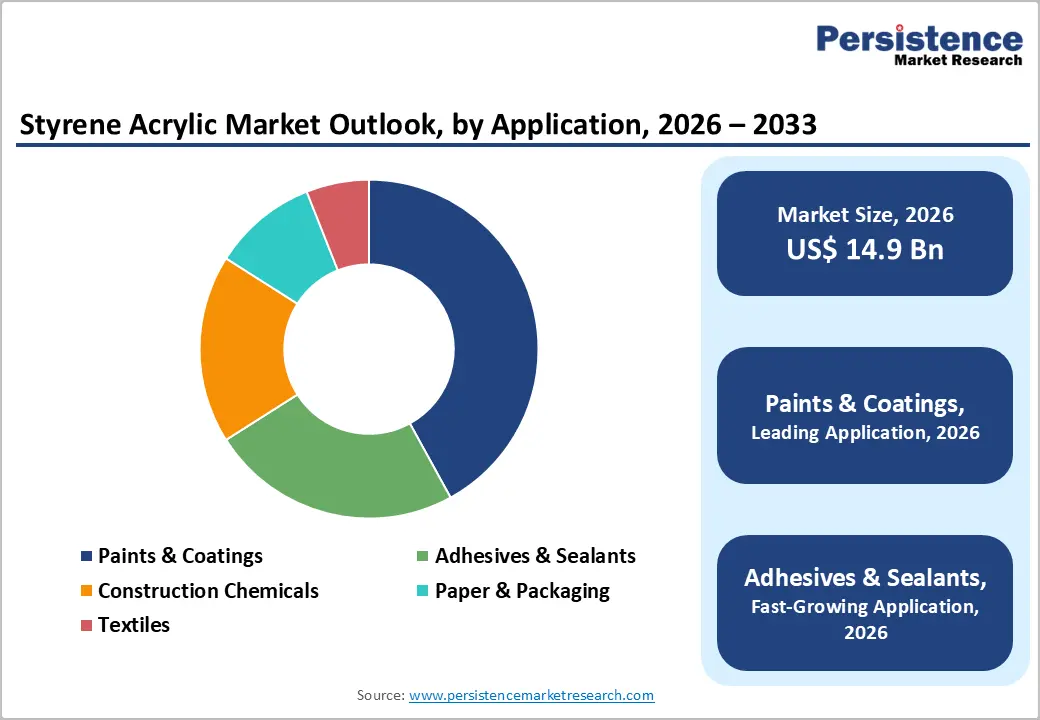

- Application Segment Trend: Paints & coatings are expected to lead with around 42% share in 2026, while adhesives & sealants are projected to grow the fastest, driven by demand for high-performance bonding solutions in packaging, construction, and automotive sectors.

- End-use Industry Trend: The construction segment is set to hold about 38% share in 2026, while automotive is expected to be the fastest-growing end-use through 2033, supported by lightweighting, emission norms, and rising adoption of styrene-acrylic-based coatings and adhesives.

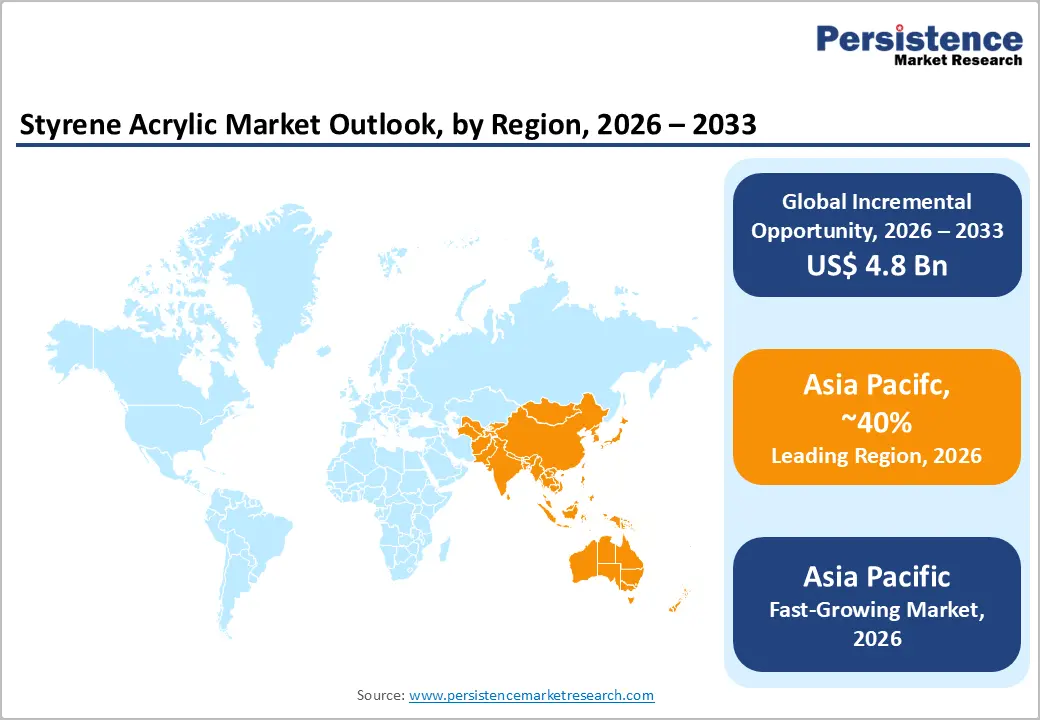

- Regional Leadership: Asia Pacific is likely to dominate with nearly 45% share in 2026 and grow the fastest through 2033, led by strong manufacturing expansion, coating demand, and infrastructure development in China and India.

- Key Growth Drivers: Growth is driven by rising demand for sustainable styrene-acrylic emulsions, the increasing use of high-performance hybrid polymers, and accelerating global infrastructure and industrial recovery.

- Competitive Landscape: The market is moderately consolidated, with top players holding a majority share, competing through capacity expansion, backward integration, and innovation in styrene acrylic resins and emulsion polymers.

DRO Analysis

Driver - Rising Demand for Sustainable Water-Based Polymer Systems

The styrene-acrylic emulsions market is being structurally reshaped by tightening global environmental regulations, which are accelerating the transition from solvent-based systems to sustainable, water-based alternatives. Recent regulatory actions in 2025-2026, including stricter VOC emission limits under the U.S. EPA Clean Air Act framework and updated EU Ecolabel requirements for paints and coatings, are reinforcing compliance pressure across construction, adhesives, and industrial coatings industries. These measures are directly influencing formulation standards and material substitution trends at a global scale.

This regulatory shift is driving a clear industry transition toward low-VOC styrene acrylic emulsions that deliver both performance and environmental compliance. Manufacturers are increasingly reformulating product portfolios to meet evolving sustainability benchmarks while maintaining durability and application efficiency. The business impact is significant, as compliance-driven demand is accelerating adoption rates, strengthening long-term product replacement cycles, and positioning water-based polymer systems as a core growth pillar in global coatings and construction chemical markets.

Restraint - Volatility in Raw Material Prices and Petrochemical Dependency

Volatility in raw material prices continues to define the operating environment of the styrene acrylic market, as production remains tightly linked to benzene- and ethylene-based styrene monomer supply. Crude oil-linked feedstock fluctuations, as highlighted in OECD petrochemical assessments, have consistently driven cost instability, with raw materials accounting for nearly 55-70% of total production expenses. This pressure has intensified as global petrochemical markets experienced sharp pricing swings, driven by uneven demand recovery and energy cost variability reported in major energy and trade updates.

This ongoing instability is reshaping industry economics, with manufacturers facing compressed margins and limited pricing flexibility in downstream segments such as coatings and construction chemicals. Supply disruptions across Asia-Pacific petrochemical hubs have further amplified procurement uncertainty, while episodic feedstock shortages and logistics constraints have disrupted production planning. As a result, the market is witnessing delayed capacity expansions and increased emphasis on cost-hedging strategies, underscoring the structural barrier that petrochemical dependency poses to stable, long-term growth.

Opportunity - Growth in Green Building and High-Performance Construction Materials

The expansion of green building and high-performance construction materials is emerging as a key growth lever for the styrene acrylic market, driven by the global shift toward sustainable and energy-efficient infrastructure. Styrene-acrylic polymers are increasingly preferred in construction chemicals, sealants, and coatings due to their water resistance, flexibility, and strong adhesion. With green construction expected to account for over 40% of global building activity by 2030, demand visibility is strengthening across both developed and emerging markets.

This opportunity has been reinforced by stricter building efficiency regulations and large-scale infrastructure modernization programs across major economies. The European Union’s continued enforcement of energy performance standards and retrofit mandates has accelerated the adoption of low-VOC coating systems in public and commercial infrastructure.

Simultaneously, infrastructure investment cycles across North America and parts of the Asia Pacific are emphasizing sustainable construction materials, as highlighted in recent government infrastructure funding announcements and global policy updates. These developments are expanding the range of applications, accelerating the shift to water-based systems, and strengthening long-term demand for styrene-acrylic solutions in modern construction.

Category-wise Analysis

Application Insights

Paints & coatings are estimated to dominate the styrene acrylic market with a 42% share in 2026, driven by architectural and industrial demand across construction and infrastructure.

Growth is supported by strict emission norms and the shift toward water-based, low-VOC systems. In 2026, Sherwin-Williams expanded its waterborne protective coatings for structural steel and industrial fabrication in North America to comply with EPA requirements. This reinforces paints & coatings as the core demand stabilizer, driven by solvent-to-waterborne substitution.

Construction chemicals are estimated to be the fastest-growing application through 2033, supported by infrastructure modernization. Demand is concentrated in waterproofing, sealants, and repair systems requiring durability and moisture resistance. In 2026, Sika expanded the use of polymer-modified waterproofing in major Middle East transport infrastructure projects, including metro and airport developments. This is shifting the segment toward specification-driven demand, thereby increasing styrene-acrylic value intensity.

Product Type Insights

Styrene-acrylic emulsions are expected to lead the market with a 45% share in 2026, driven by coatings, adhesives, and construction applications. Demand is supported by strong film formation, cost efficiency, and compatibility with water-based systems. AkzoNobel expanded waterborne coatings in Europe using advanced acrylic emulsions for low-VOC architectural applications. This reinforces emulsions as the default platform for compliant coating systems.

Hybrid polymers are estimated to be the fastest-growing product type through 2033, driven by performance needs. Demand is rising for automotive, industrial, and infrastructure applications that require durability and chemical resistance. In 2026, AkzoNobel upgraded Intershield 300+ for corrosion protection of offshore wind and marine infrastructure in Europe. This positions hybrid systems as premium solutions that enable longer asset lifespans and shorter maintenance cycles.

Regional Analysis

North America Styrene Acrylic Market Trends

North America is estimated to account for 22% share of the global styrene acrylic market in 2026, supported by a mature industrial base, strong construction activity, and early adoption of low-VOC water-based technologies. The region’s growth trajectory is increasingly shaped by environmental compliance frameworks and the steady modernization of industrial infrastructure. Demand visibility remains stable, particularly across coatings and construction chemicals, where performance and regulatory alignment are both critical purchasing factors.

U.S. Styrene Acrylic Market Trends

The U.S. is estimated to contribute 55% of the regional market in 2026, underpinned by large-scale industrial coatings consumption and infrastructure-linked demand. In 2025-2026, PPG Industries expanded its waterborne protective coatings offerings for industrial steel fabrication and heavy manufacturing facilities across the U.S., aligning with evolving EPA-driven emissions constraints for industrial coating operations. This reflects a gradual but clear substitution away from solvent-based systems toward styrene acrylic-enabled waterborne formulations in high-volume industrial environments.

Canada Styrene Acrylic Market Trends

Canada is estimated to hold 10% share within North America in 2026, driven by infrastructure renewal and public construction spending. In 2026, government-backed transport and civic infrastructure upgrades increasingly emphasized low-emission material standards in procurement frameworks, indirectly strengthening demand for durable polymer-based coatings and construction chemicals. This is reinforcing steady adoption of styrene acrylic systems in long-life public infrastructure applications, particularly in climate-exposed regions.

Europe Styrene Acrylic Market Trends

Europe is estimated to represent 20% share of the global styrene acrylic market in 2026, characterized by a highly regulated environment and strong emphasis on sustainability-led material substitution. Growth remains moderate but structurally stable, supported by renovation-driven construction activity, industrial refurbishment, and circular economy initiatives. The region continues to prioritize low-emission, water-based polymer systems across both coatings and construction chemical applications.

Germany Styrene Acrylic Market Trends

Germany is estimated to account for 30% of the European market in 2026, anchored by its industrial coatings, automotive, and machinery sectors. In 2026, BASF expanded its water-based acrylic dispersion capacity at Ludwigshafen to support rising demand for low-emission coatings across European manufacturing industries. This reflects an ongoing shift in industrial supply chains toward compliant, waterborne styrene acrylic systems, particularly in high-spec manufacturing applications.

France Styrene Acrylic Market Trends

France is estimated to hold 18% share within Europe in 2026, supported by renovation-led construction activity and public infrastructure upgrades. In 2025-2026, public-sector building modernization programs increasingly embedded low-carbon and low-VOC coating requirements in refurbishment tenders for schools, housing, and civic infrastructure. This is steadily reinforcing demand for water-based acrylic systems, with procurement policy acting as a key demand driver rather than discretionary consumption.

Asia Pacific Styrene Acrylic Market Trends

Asia Pacific is estimated to dominate with 40% share of the global styrene acrylic market in 2026, driven by large-scale urbanization, industrial expansion, and sustained infrastructure investment cycles. The region benefits from cost-efficient manufacturing ecosystems and strong downstream demand from coatings, adhesives, and construction chemicals. Over time, regulatory alignment toward environmental standards is gradually accelerating the shift toward water-based polymer systems.

China Styrene Acrylic Market Trends

China is estimated to account for 45% of the Asia Pacific market in 2026, making it the single largest national contributor globally. In 2026, major chemical producers expanded waterborne acrylic dispersion capacity in coastal industrial clusters to meet rising demand from coatings and adhesive applications under tightening environmental controls in industrial zones. This reflects a structural transition in the country’s chemical manufacturing base toward higher-compliance, water-based production systems.

India Styrene Acrylic Market Trends

India is estimated to represent 18% of the regional market in 2026, supported by infrastructure expansion and rapid urban development. In 2025-2026, transport corridors, housing programs, and urban infrastructure projects increasingly specified polymer-modified construction materials in procurement guidelines focused on durability and lifecycle performance. This is reinforcing steady penetration of styrene acrylic systems in construction chemicals, with demand increasingly tied to specification-led infrastructure development rather than general material substitution.

Competitive Landscape

The global styrene acrylic market is moderately consolidated, with BASF, Dow, Arkema, Synthomer, and Celanese collectively holding an estimated 45% share in 2026.

These players benefit from integrated value chains, strong global reach, and established customer relationships across coatings, construction chemicals, and adhesives. In 2025-2026, competition has intensified around low-VOC, water-based styrene acrylic emulsions, driven by stricter environmental regulations. This is reinforcing a technology-led structure where innovation and compliance determine market positioning.

Regional players in the Asia Pacific and Europe are expanding through cost-efficient production and application-specific offerings, especially in construction and industrial coatings. Competition is increasingly shifting toward customized formulations rather than standardized products. In 2025-2026, selective acquisitions and capacity expansions by larger firms have strengthened geographic and specialty polymer portfolios. This is gradually increasing consolidation while raising entry barriers linked to scale, integration, and regulatory compliance.

Key Industry Developments:

- In March 2026, BASF expanded its North American acrylic polymers capacity to support rising demand for water-based formulations across paints, coatings, and construction applications. The move also aligns with its broader global strategy to strengthen dispersion and waterborne polymer production capabilities.

- In February 2025, Dow and Sumitomo Chemical entered a strategic partnership to co-develop and supply styrene acrylic emulsions for industrial coatings, targeting improved performance and sustainability. The collaboration reflects the industry-wide shift toward high-performance, waterborne binder systems in coatings and adhesives applications.

Companies Covered in Styrene Acrylic Market

- BASF SE

- Dow Inc.

- Arkema S.A.

- Synthomer plc

- Wacker Chemie AG

- LG Chem Ltd.

- Mitsubishi Chemical Group

- Celanese Corporation

- Ashland Global Holdings

- Nippon Shokubai Co. Ltd.

- BASF-YPC

- Trinseo S.A.

- Hexion Inc.

- Sasol Limited

- Jiangsu Huarun Chemical

Frequently Asked Questions

The global styrene acrylic market is projected to reach US$ 14.9 billion in 2026.

The styrene acrylic market grows due to rising demand for water-based coatings, infrastructure development, and stricter VOC emission regulations.

The styrene acrylic market is expected to grow at a CAGR of 4.1% from 2026 to 2033.

Growth is driven by expansion in green construction, sustainable coatings, and high-performance construction chemicals.

Key players include BASF SE, Dow Inc., Arkema, Synthomer, and Celanese Corporation.