- Plastics, Polymers & Resins

- Flexible Barrier Films for Electronics Market

Flexible Barrier Films for Electronics Market Size, Share, and Growth Forecast, 2026 - 2033

Flexible Barrier Films for Electronics Market by Product Type (Flexible Barrier Films for Electronics)., Application (Display, Solar Cells, Sensors, Lighting), Material Type (Polymer, Metal / Metal Oxide, Composite / Multilayer) and Regional Analysis for 2026 - 2033

Flexible Barrier Films for Electronics Market Size and Trends Analysis

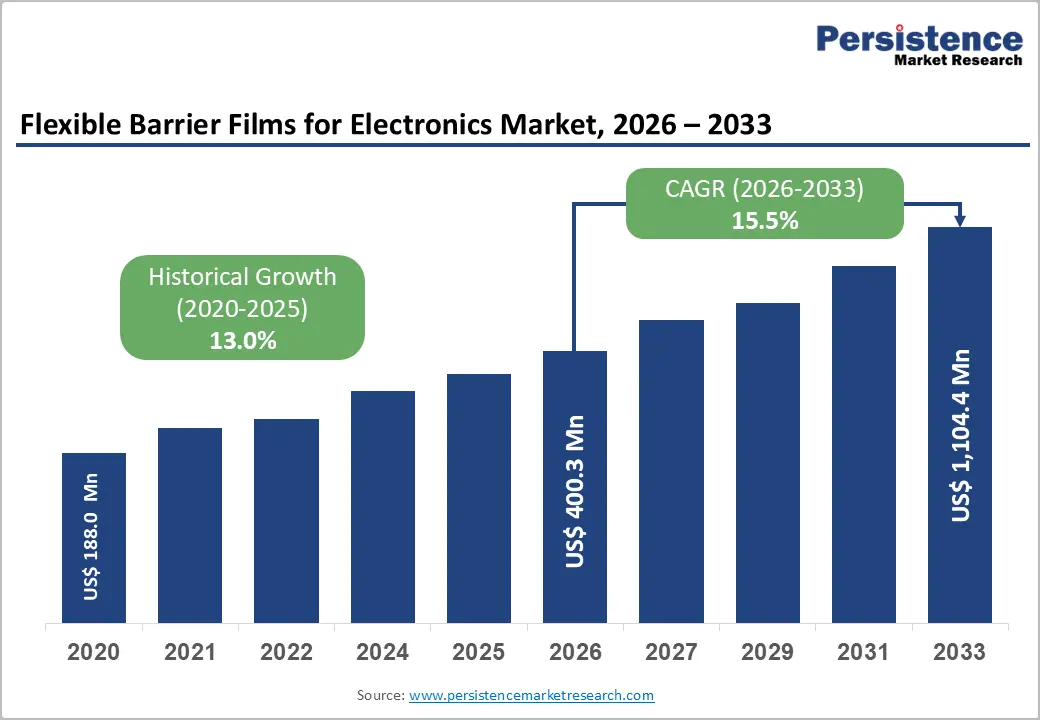

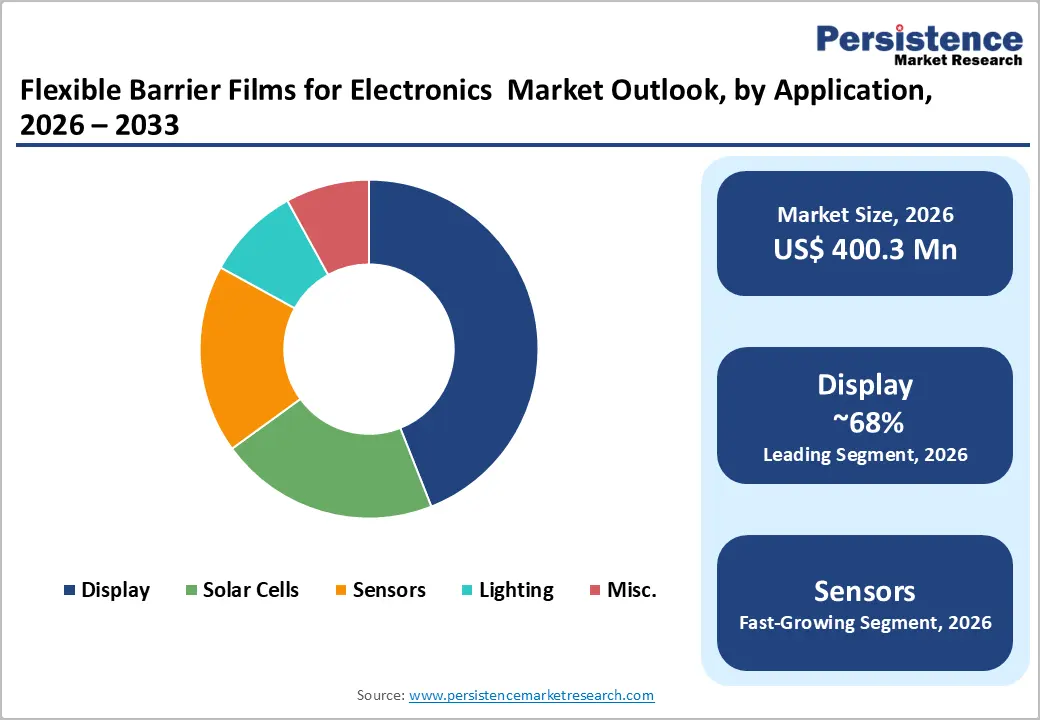

The global flexible barrier films for electronics market size was valued at US$ 400.3 Mn in 2026 and is projected to reach US$ 1,104.4 Mn by 2033, growing at a CAGR of 15.5% between 2026 and 2033.

Primary growth factors include the accelerating deployment of flexible display technologies, the proliferation of organic photovoltaic modules, and the rapid expansion of the global electronics and IT industry, which reached approximately US$ 3.99 trillion in production output in 2025, as reported by the Japan Electronics and Information Technology Industries Association. The global semiconductor market is projected to reach US$ 975 billion by 2026 from US$ 305 billion in 2013, reinforcing structural demand for high-performance encapsulation materials across flexible device architectures.

Key Industry Highlights:

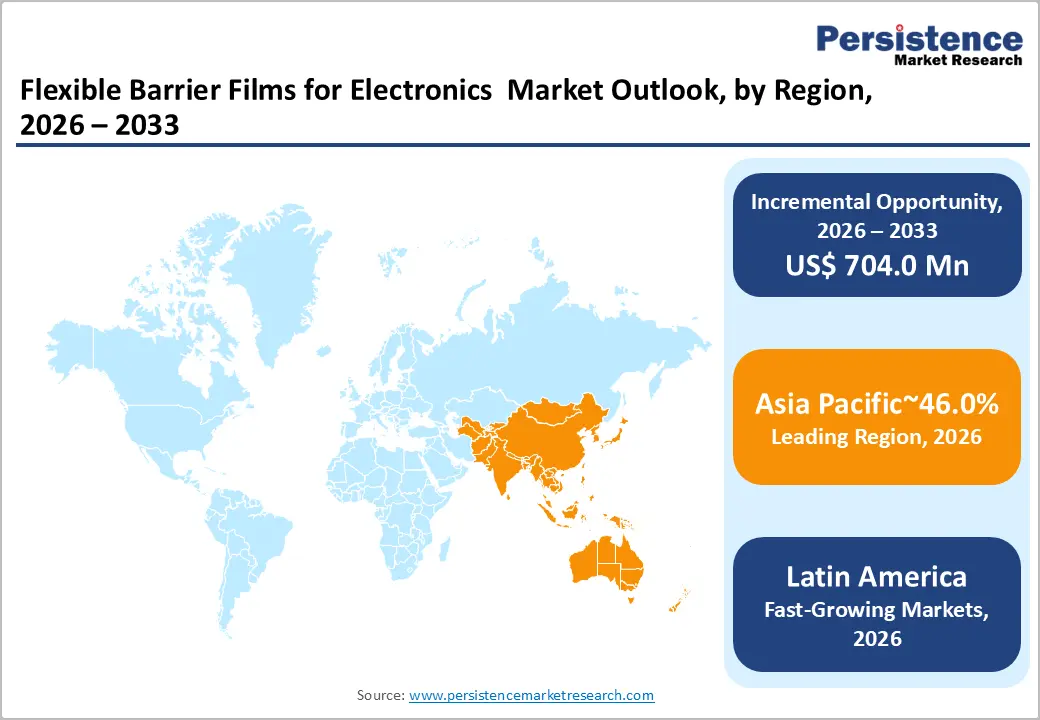

- Leading Regional Market: Asia Pacific dominates the flexible barrier films for electronics market with 46.0% share, driven by concentrated electronics manufacturing, AMOLED production, and semiconductor fabrication across China, South Korea, Japan, and India.

- Fast-growing Market: North America holds 28.5% share, supported by high electronics consumption, a strong semiconductor ecosystem, and sustained import-driven demand for display-integrated devices.

- Emerging Regional Market: Europe accounts for 17.5% of the market, driven by renewable energy investments, flexible electronics R&D, and policy-led demand for photovoltaic and sustainable electronic applications.

- Dominant Product Segment: Flexible Electronics leads with 47% share, driven by rising adoption of foldable displays, wearable devices, and flexible circuit applications requiring ultra-high barrier performance.

- Fastest-Growing Product Segment: Photovoltaic (Flexible Solar) is the fastest-growing segment, fueled by expanding deployment of perovskite solar films, BIPV solutions, and portable energy applications.

- Leading Application Segment: Display applications dominate with a 44% share, driven by strong demand for OLED/AMOLED panels in smartphones, tablets, and next-generation foldable devices.

| Key Insights | Details |

|---|---|

| Market Flexible Barrier Films for Electronics Size (2026E) | US$ 400.3 Mn |

| Market Value Forecast (2033F) | US$ 1,104.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 15.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.0% |

DRO Analysis

Growth Drivers

Sustained Expansion of Global Electronics and Semiconductor Production Underpins Demand in the Flexible Barrier Films for Electronics Market

The structural scale-up of global electronics manufacturing creates foundational procurement demand for flexible barrier films, which serve as critical moisture and oxygen encapsulants across display panels, wearable devices, and semiconductor packaging applications. According to the Japan Electronics and Information Technology Industries Association, global electronic and IT industry production expanded from US$ 2.65 trillion in 2014 to approximately US$ 3.99 trillion in 2025, representing a more than 50% output expansion over a decade.

A major acceleration phase occurred between 2020 and 2022, with production reaching US$ 3.47 trillion in 2022, driven by pandemic-induced demand for remote working infrastructure, data centers, and consumer electronics. Following inventory corrections in 2023, the sector rebounded in 2024 and 2025, supported by structural demand from artificial intelligence, 5G deployment, and electric vehicle electronics.

The global semiconductor market expanded from US$ 305 billion in 2013 to a projected US$ 975 billion in 2026, with growth of 22.5% recorded in 2025 and a projected 26.3% in 2026 alone. This scale and velocity of electronics industry growth directly amplify volume demand for flexible barrier films across the Flexible Barrier Films for Electronics Market.

U.S. Electronics Trade Momentum and Domestic Demand Sustain North American Barrier Film Procurement

The United States represents a high-consumption electronics market that directly sustains demand for flexible barrier films across consumer electronics, display devices, and photovoltaic modules. U.S. electronic product imports reached US$ 672.2 billion in 2024, rebounding from a 2023 dip to mark the highest import value in the 2020 to 2024 period, reflecting strong domestic end-user demand for semiconductor-intensive consumer electronics that incorporate flexible barrier-encapsulated components.

Over the same period, U.S. electronic product exports grew steadily from US$ 255.7 billion in 2020 to US$ 337.9 billion in 2024, underpinned by global demand for high-value American electronic hardware and advanced semiconductors. The U.S. flexible packaging industry generated US$ 41.5 billion in sales, capturing 21% of the national US$ 180.3 billion packaging market, employing over 85,000 workers, with the electronics and medical segments representing high-specification sub-markets where barrier performance standards converge with flexible electronics requirements.

Government-Led Semiconductor and Flexible Electronics Manufacturing Policies Catalyze Investment and Supply Chain Expansion

National industrial policy frameworks supporting domestic semiconductor and flexible electronics fabrication are functioning as macro-level structural catalysts for the Flexible Barrier Films for Electronics Market, expanding both manufacturing capacity and end-use application volumes. India's central government launched the Semicon India Program, backed by Rs 76,000 crore, approximately US$ 10 billion, providing a 50% capital match for companies establishing semiconductor foundries, OLED display fabrication plants, and MEMS sensor manufacturing facilities.

Complementing this, the Tamil Nadu Semiconductor and Advanced Electronics Policy 2024 introduced targeted R&D expenditure incentives and capital support for advanced electronics manufacturers. In China, large-scale government-backed investment in AMOLED production has created a concentrated demand center for display-grade barrier films, with China accounting for 12.5% of the global flexible barrier films for electronics market share. The global semiconductor market's projected expansion to US$ 975 billion in 2026, driven by geopolitical localization efforts and next-generation chip demand, is accelerating the build-out of electronics value chains requiring barrier film encapsulation across wafer packaging, flexible display integration, and sensor device production.

Restraint - High Production Cost and Technical Complexity of Ultra-Barrier Film Manufacturing

Manufacturing ultra-high-barrier films to achieve water vapor transmission rates required for OLED and organic photovoltaic applications demands sophisticated multilayer deposition processes, including atomic layer deposition, plasma-enhanced chemical vapor deposition, and roll-to-roll sputtering. These processes require precision clean-room equipment, advanced precursor materials, and long process validation cycles, resulting in cost structures significantly higher than conventional rigid glass encapsulation.

This premium cost profile limits adoption in cost-sensitive mid-market electronics segments, constraining rapid penetration beyond premium display and photovoltaic tiers and creating a structural bifurcation in the Flexible Barrier Films for Electronics Market between volume commodity products and high-performance specialty films.

Supply Chain Concentration Risk in Specialty Material Inputs and Deposition Equipment

The flexible barrier films for the electronics market depend on a narrow base of globally concentrated suppliers for critical inputs, including high-purity alumina and silica precursors, specialty polymer substrates, and indium tin oxide targets.

This concentration risk was evidenced during the global electronics inventory correction of 2023, when the semiconductor market contracted by 8.2%, triggering cascading delays in material procurement and production scheduling for barrier film manufacturers. Specialized deposition equipment carries long lead times, limiting capacity scale-up responsiveness. Geopolitical tensions affecting Asia-concentrated supply chains further expose manufacturers to trade disruption, raw material cost inflation, and delivery uncertainty across key input categories.

Opportunities - Flexible Photovoltaic Encapsulation for Building-Integrated and Portable Solar Applications

Flexible photovoltaic modules for building-integrated photovoltaics and portable off-grid energy systems represent a high-volume, policy-supported demand channel for participants in the Flexible Barrier Films for Electronics Market. These applications require conformal, lightweight encapsulants that deliver ultra-low moisture permeability, along with optical clarity and UV stability, for extended outdoor lifetimes.

In the global flexible photovoltaic films market, Perovskite photovoltaic films are emerging as the fastest-evolving technology segment, driven by improving efficiency and low manufacturing costs. Amcor Plc and Power Roll Limited signed a Memorandum of Understanding to jointly develop a lightweight, low-cost, flexible photovoltaic film using roll-to-roll barrier manufacturing, leveraging proven barrier technologies without reliance on rare-earth minerals.

This commercial partnership validates the cost competitiveness and scale potential of flexible PV barrier encapsulation, presenting actionable licensing, co-development, and supply chain integration opportunities for barrier film manufacturers seeking a position in the photovoltaic segment of the flexible barrier films for electronics market.

Wearable and Flexible Sensor Adoption Across Healthcare, Industrial IoT, and Smart Infrastructure

The rapid commercialization of flexible sensors and wearable electronics creates a structurally new, high-specification demand channel for conformal barrier film encapsulants within the Flexible Barrier Films for Electronics Market. These devices require ultra-thin, mechanically robust barrier layers that maintain protective integrity under repetitive bending, stretching, and thermal cycling across healthcare monitors, industrial IoT nodes, environmental sensors, and smart textile applications.

The global Personal Computing Device market recorded Q3 2025 shipments of 113.5 million units, with the PC segment expanding 8.9% year-on-year to 75.5 million units, reflecting a broader consumer and commercial appetite for next-generation electronic form factors. India's Semicon India Programme explicitly supports MEMS and compound semiconductor sensor manufacturing, creating downstream procurement demand for flexible encapsulation materials. Manufacturers capable of supplying roll-to-roll processed, validated flexible barrier films with documented flex-endurance specifications across thousands of bending cycles are positioned to capture this high-growth, differentiated application channel as flexible sensor devices transition from niche to mainstream commercial production.

Foldable Displays and AMOLED Device Expansion Create Premium Barrier Film Procurement Pipelines

The commercialisation of foldable smartphones, rollable displays, and next-generation AMOLED panels creates a premium, high-margin procurement opportunity for advanced display-grade barrier films within the Flexible Barrier Films for Electronics Market. OLED architectures require sub-ambient moisture-barrier performance to prevent cathode oxidation, making barrier-film specification a direct determinant of display longevity and field reliability.

Android and HarmonyOS devices recorded 7.9% growth in 2024, commanding significant global smartphone shipment volumes, while International Data Corporation forecasts iOS shipments will grow 5.4% by 2027, collectively reinforcing sustained high-volume premium display demand.

TOPPAN Holdings launched production of its GL-SP BOPP-based transparent barrier film from its GL BARRIER series at its Indian subsidiary, TOPPAN Specialty Films Private Limited, targeting supply to the Americas, Europe, India, and ASEAN. This geographic diversification of display-grade barrier film supply reflects the structural decentralization of AMOLED manufacturing ecosystems and opens procurement partnership opportunities for barrier film suppliers capable of serving emerging Asian display fabrication hubs within the Flexible Barrier Films for Electronics Market.

Category-wise Analysis

Product Type Insights

Flexible electronics commands the leading position, accounting for approximately 47% of total revenue in 2026. This segment encompasses barrier films deployed in foldable displays, wearable health monitors, electronic skin patches, flexible printed circuit boards, and soft robotics components, all of which demand encapsulants combining ultra-low moisture vapour transmission rates with mechanical conformability. The dominance of this segment is directly tied to the rapid proliferation of OLED-on-foil and flexible AMOLED display architectures in premium consumer electronics, where barrier film performance is a non-negotiable product reliability parameter.

The global electronic and IT industry's production trajectory, reaching approximately US$ 3.99 trillion in 2025, reflects the macro-scale demand environment sustaining flexible electronics component procurement. Beneq's ALD platform, capable of depositing sub-50-nanometer barrier layers on flexible polymer substrates, exemplifies the precision encapsulation technology serving this segment. The manufacturing and resources sector held 24.5% of market share in 2024, reinforcing the industrial breadth of flexible electronics applications. As foldable device architectures scale from premium to mid-market price tiers, the Flexible Electronics segment is positioned for sustained volume leadership across the forecast period.

Photovoltaic, or flexible solar, represents the fastest-growing product type, propelled by accelerating deployment of organic photovoltaics, perovskite thin-film modules, and building-integrated solar applications that require flexible, transparent barrier encapsulants engineered for multi-year outdoor durability. Unlike rigid glass-encapsulated solar panels, flexible photovoltaic modules impose unique encapsulation requirements centred on optical transmission, UV stability, and water vapour permeability control at film thicknesses compatible with roll-to-roll manufacturing.

Application Insights

The display application segment holds the largest share in the global flexible barrier films for electronics market, accounting for approximately 44% of total market revenue in 2026. Flexible and foldable displays, including OLED and AMOLED configurations deployed in smartphones, tablets, smart wearables, and automotive infotainment panels, are the highest-volume single-application category for advanced barrier films due to the extreme sensitivity of organic light-emitting materials to even trace levels of moisture and oxygen. The global Personal Computing Device market reached 113.5 million units in Q3 2025 shipments, with notebook volumes reaching 53.2 million units, reinforcing the scale of display-integrated device demand.

China's government-backed investment in AMOLED manufacturing has created a highly concentrated demand centre for display-grade barrier films within the Asia Pacific, with China accounting for 12.5% of the global market. U.S. electronic product imports reached US$ 672.2 billion in 2024, a substantial portion of which comprised display-integrated consumer electronics requiring high-performance encapsulants. TOPPAN's GL BARRIER series, incorporating silica and alumina vapour deposition layers to achieve display-grade moisture permeability specifications, represents the technical benchmark for this segment, highlighting that display-grade procurement continues to drive the highest specification and price-per-square-meter profiles within the Flexible Barrier Films for Electronics Market.

Regional Insights and Trends

Asia Pacific Flexible Barrier Films For Electronics Market Trends

Asia Pacific dominates the global flexible barrier films for electronics market, holding approximately 46.0% of global revenue, anchored by the region's concentration of consumer electronics manufacturing, semiconductor fabrication, and AMOLED display panel production across China, South Korea, Japan, and India. China alone accounted for 12.5% of global market share, supported by large-scale government-backed AMOLED capacity expansion that has triggered structural demand for display-grade barrier films across Chinese electronics value chains. Government subsidy programs in China also played a direct role in stimulating consumer and commercial electronics demand, as evidenced by the global PCD market recovery to 113.5 million units in Q3 2025 shipments.

India represents the region's most strategically dynamic emerging market node. The Semicon India Programme, backed by approximately US$ 10 billion, provides a 50% capital match for semiconductor foundries, display fab investments, and MEMS sensor manufacturing. The Tamil Nadu Semiconductor and Advanced Electronics Policy 2024 further added targeted R&D and capital incentives for advanced electronics manufacturers. TOPPAN Holdings launched production of its BOPP-based GL-SP transparent barrier film at its Indian subsidiary, targeting supply to the Americas, Europe, India, and ASEAN, signalling the geographic diversification of Asia Pacific's barrier film supply chain into South and Southeast Asia.

Japan's barrier film technology leadership, exemplified by TOPPAN's GL BARRIER platform and established transparent vapour deposition capabilities, reinforces Asia Pacific's dual role as both the dominant production hub and the most consequential demand centre for the global Flexible Barrier Films for Electronics Market. South Korea's advanced OLED panel manufacturing ecosystem continues to drive premium barrier film procurement, while the region's renewable energy mandates amplify photovoltaic-grade barrier film demand.

North America Flexible Barrier Films For Electronics Market Insights

North America holds approximately 28.5% of global revenue in the Flexible Barrier Films for Electronics Market, with the United States serving as the region's dominant national market, underpinned by strong technology R&D capabilities, significant electronics import dependency, and an active semiconductor investment policy.

U.S. electronic product imports reached US$ 672.2 billion in 2024, recovering sharply after a 2023 dip, while exports grew steadily to US$ 337.9 billion in 2024, highlighting the structural trade deficit that reflects U.S. reliance on Asian electronics manufacturing while maintaining a competitive export position in advanced semiconductor and electronic components. This import-driven consumption sustains North American downstream demand for flexible barrier films embedded in consumer electronics, displays, and flexible energy devices.

Europe Flexible Barrier Films For Electronics Market Trends

Europe accounts for approximately 17.5% of global revenue as Germany, France, the Netherlands, and the United Kingdom account as the primary demand hubs across renewable energy, automotive electronics, and applied research applications. The European Union's Horizon Europe research framework and the European Green Deal have jointly mobilised investment in organic photovoltaic technologies and flexible electronics as part of the EU's energy sovereignty and decarbonization agenda, directly stimulating demand for advanced photovoltaic-grade barrier encapsulants across BIPV and off-grid solar applications. The EU's near-zero energy building directives create a structured long-term pipeline for building-integrated photovoltaic modules, representing a high-volume deployment channel for flexible barrier films.

Competitive Landscape

The global flexible barrier films for electronics market exhibits a moderately fragmented structure, positioned between fragmented and consolidated, with a defined top tier of large, diversified multinationals competing alongside specialised niche technology companies. Leading players include 3M Company, Amcor Plc, Toppan Printing Co. Ltd., Honeywell International Inc., Eastman Chemical Company, and Tera-Barrier Films Pte Ltd, each competing across distinct application tiers. Competitive differentiation is driven by barrier performance specifications, substrate compatibility, roll-to-roll scalability, and application-specific customisation.

Market leaders differentiate through proprietary deposition architectures such as ALD and PECVD multilayer stacks, substrate-agnostic film designs, and documented performance validation for specific end-use environments. Emerging business models include technology licensing for barrier film IP and joint development agreements with photovoltaic and display OEM manufacturers.

Key Industry Developments

- In April 2022, Toray Industries developed a super high-barrier film designed for flexible electronics such as wearable sensors, flexible displays, and solar cells. Innovation significantly reduces costs by up to 80% compared to conventional deposition-based barrier films, enabling broader commercialisation.

- In March, 2022, Toray Industries introduced REACTIS™-based stretchable film for circuit mounting applications in flexible electronics. The film offers high elasticity, heat resistance, and electrical stability, making it suitable for wearables, industrial sensors, and soft robotics.

Companies Covered in Flexible Barrier Films for Electronics Market

- 3M Company

- Amcor Plc

- Beneq

- Eastman Chemical Company

- Fraunhofer Polo Alliance

- Honeywell International Inc.

- Materion Corporation

- Sigma Technologies Int'l, LLC.

- Alcan Packaging

- Tera-Barrier Films Pte Ltd

- Toppan Printing Co., Ltd.

- General Electric

Frequently Asked Questions

The global Flexible Barrier Films for Electronics Market is projected to be valued at US$ 400.3 Mn in 2026.

The Photovoltaic (Flexible Solar) segment is expected to account for approximately 47% of the Global Flexible Barrier Films for Electronics Market by Product Type in 2026.

The market is expected to witness a CAGR of 15.5% from 2026 to 2033.

Growth in the Flexible Barrier Films for Electronics Market is driven by rapid expansion in global electronics and semiconductor production, strong U.S. electronics demand and trade, and government-backed investments in semiconductor and flexible electronics manufacturing.

Key opportunities in the Flexible Barrier Films for Electronics Market include rising demand from flexible photovoltaics, rapid adoption of wearable and flexible sensors, and expanding procurement for foldable and AMOLED display technologies.

Key players in the Flexible Barrier Films for Electronics Market include 3M Company, Amcor Plc, Toppan Printing Co. Ltd., Honeywell International Inc., Eastman Chemical Company