- Plastics, Polymers & Resins

- Bio Plasticizers Market

Bio Plasticizers Market Size, Share, and Growth Forecast 2026 – 2033

Bio Plasticizers Market by Product Type (Epoxidized Soybean Oil (ESBO), Castor Oil-Based Plasticizers, Citrates, Succinic Acid, Others), Industry (Packaging, Healthcare, Automotive, Construction, Textile & Leather, Electronics, Agriculture, Others), and Regional Analysis, 2026–2033

Bio Plasticizers Market Size and Trend Analysis

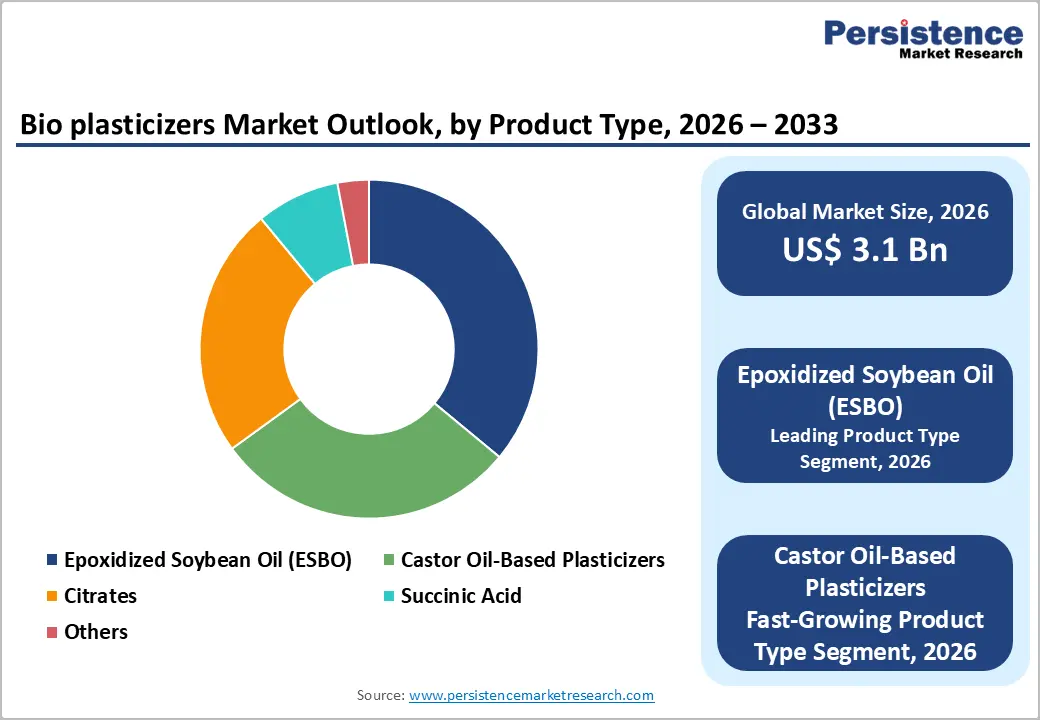

The global bio plasticizers market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 9.5% between 2026 and 2033. This trajectory is driven by the accelerating global regulatory restriction of phthalate plasticizers, brand owner sustainability mandates requiring bio-based content in packaging and consumer goods, and the expanding commercial availability of high-performance bio-based alternatives, including ESBO, castor oil-derived plasticizers, and citrate esters.

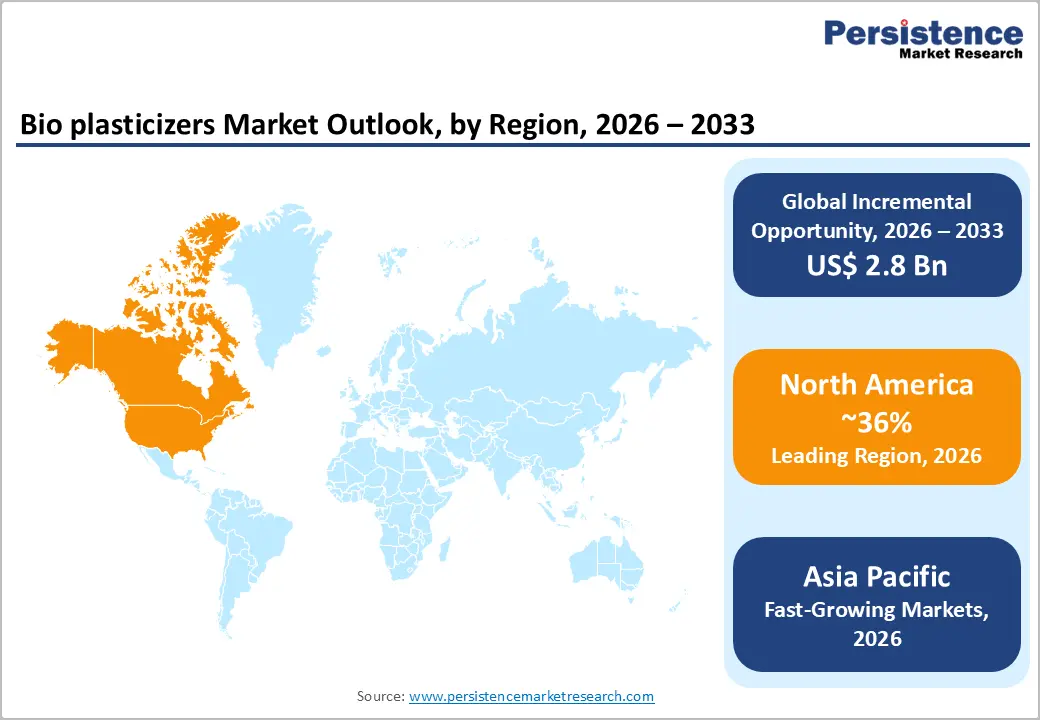

The verified historical CAGR of 9.1% between 2020 and 2025, achieved against a backdrop of phthalate phase-out regulation and bio-economy policy investment, confirms the structural durability of demand. North America leads today with 36% global share, while Asia Pacific is positioned as the fastest growing region through 2033 as bio-economy infrastructure and environmental regulation mature across the region.

Key Industry Highlights

- Leading Region: North America leads the global bio plasticizers market with approximately 36% share in 2026, anchored by U.S. ESBO production scale from domestic soybean oil, stringent CPSIA and FDA phthalate regulations, and a large consumer goods and packaging industry committed to bio-based material sourcing.

- Fastest Growing Region: Asia Pacific is projected to reach 11.2% CAGR by 2033, driven by China's tightening phthalate chemical regulation, India's strategic dominance in global castor oil supply, and rapidly expanding consumer goods and healthcare manufacturing sectors across the region.

- Dominant Product Segment: ESBO holds approximately 41% of the global bio plasticizers market in 2026, sustained by its dual functionality as plasticizer and PVC thermal stabilizer co-agent, broad food-contact regulatory approval, and cost competitiveness from established U.S. and Chinese soybean oil supply chains.

- Fastest Growing Product Segment: Castor oil-based bio plasticizers are expected to reach 11% CAGR through 2033, driven by superior technical performance in automotive, medical, and high-performance cable applications, and India's structurally advantaged position supplying 80–90% of global castor oil.

- Key Opportunity: WHO and FDA guidance recommending DEHP replacement in neonatal, dialysis, and oncology devices creates a high-value, compliance-driven demand stream for citrate and ESBO medical-grade bio plasticizers commanding the highest price premium in the market.

DRO Analysis

Drivers - Regulatory Phase-Out of Phthalate Plasticizers Creating Demand for Bio-Based Alternatives

The single most powerful demand driver for bio plasticizers is the expanding global regulatory architecture restricting phthalate compounds, creating a compliance-driven substitution cycle that is independent of commodity price dynamics and consumer preference trends. The EU REACH Regulation has placed DEHP, DBP, BBP, and DIBP on the Substances of Very High Concern (SVHC) authorization list, requiring companies to seek authorization for continued use or transition to safer alternatives, a regulatory mechanism that directly accelerates bio-based adoption in European flexible PVC applications.

The U.S. Consumer Product Safety Improvement Act (CPSIA) restricts phthalate content in children's toys and childcare articles to 0.1% by weight, while South Korea's Act on Registration and Evaluation of Chemical Substances (K-REACH) and China's Measures for Environmental Management of New Chemical Substances are progressively extending similar restrictions. Collectively, these mandates represent a durable, compounding demand generator for compliant bio-based plasticizer grades through 2033.

Consumer Brand Owner Sustainability Commitments and Circular Economy Policy Driving Bio-Based Packaging Demand

Global consumer goods brand owners, directly responsible for a significant share of flexible PVC packaging and film demand, have published supply chain decarbonization and bio-based content commitments that structurally pull bio plasticizer demand upstream through their supply chains. Unilever's Sustainable Living Plan, Nestlé's commitment to 100% reusable or recyclable packaging by 2025, and Procter & Gamble's renewable materials sourcing targets collectively represent a massive downstream pull for bio-based additives, including bio plasticizers in films, coatings, and flexible packaging.

The European Union's Green Deal and Circular Economy Action Plan are reinforcing these corporate commitments through regulatory instruments, including the Packaging and Packaging Waste Regulation (PPWR), which prioritizes recyclable and bio-based material content. For bio plasticizer producers, this convergence of corporate and regulatory demand signals provides a visible, policy-backed demand runway through 2033.

Restraints - Premium Price Differential Versus Conventional Phthalate Plasticizers Constraining Volume Adoption

Bio plasticizers consistently command a 30–80% price premium over equivalent-volume phthalate alternatives, a cost gap that suppresses adoption in price-sensitive, high-volume applications in developing economies where regulatory phthalate restrictions have not yet taken effect. In markets including Southeast Asia, South Asia, and Sub-Saharan Africa, flexible PVC compounders select plasticizer grades primarily on a cost-per-unit-performance basis, and bio-based alternatives cannot yet compete at volume without significant feedstock cost reductions or policy-based mandates. This price barrier structurally limits bio plasticizer penetration to regulated or premium-positioned application segments, reducing the addressable volume market in the near term.

Feedstock Supply Volatility and Land Use Competition for Bio-Based Raw Materials

Bio plasticizer production, particularly for ESBO (from soybean oil) and castor oil-derived grades, is exposed to agricultural commodity price volatility, seasonal supply fluctuations, and the growing competition for vegetable oil feedstocks between food, fuel, and chemical industries.

The Food and Agriculture Organization (FAO) has documented significant interannual volatility in global soybean and castor oil production, driven by weather events, geopolitical trade disruptions, and shifting biofuel policy mandates in Brazil, India, and the United States. For bio plasticizer manufacturers without securing long-term agricultural offtake agreements, this feedstock volatility creates margin unpredictability that complicates long-term capacity investment decisions.

Opportunities - Castor Oil-Based Plasticizers Emerging as Highest-Growth Platform Across Performance-Demanding Applications

Castor oil-derived bio plasticizers, including sebacic acid and azelaic acid derivatives, represent the fastest growing product category within the bio plasticizers market, projected at 11% CAGR through 2033, and present a first-mover premium product opportunity for chemical companies able to scale supply of high-purity castor-based grades into automotive, medical device, and high-performance film applications. Unlike ESBO, whose adoption is maturing in commodity food packaging applications, castor oil-derived plasticizers offer superior low-temperature flexibility and thermal stability, making them technically preferred in automotive underbody coatings, cable sheathing, and medical-grade flexible PVC.

India supplies approximately 80–90% of the world's castor oil, creating a structurally advantaged supply chain for Indian chemical companies, including Emery Oleochemicals and Goldstab Organics to develop integrated castor oil-to-plasticizer value chains. As automotive lightweighting programs and medical device manufacturing expansion drive demand for high-performance bio plasticizers, the castor oil segment is uniquely positioned to deliver premium margins at growing volumes through 2033.

Healthcare and Medical Device Sector Transition to DEHP-Free Bio Plasticizers Opening High-Value B2B Demand Stream

The healthcare sector's accelerating transition away from DEHP-plasticized PVC in medical devices, IV bags, blood storage containers, enteral feeding tubes, and respiratory care equipment represents a high-value, compliance-driven demand stream for bio-based and non-phthalate plasticizers that commands the most significant price premium in the entire plasticizers value chain. The World Health Organization (WHO) and U.S. Food and Drug Administration (FDA) have both issued guidance documents recommending DEHP replacement in medical devices used in neonatal care, dialysis, and oncology, creating specification-level pull for alternative grades.

The global medical devices market, valued at over US$ 600 billion according to Medical Device Manufacturers Association (MDMA), is growing at approximately 5–6% annually, with PVC-based devices representing a disproportionately large share of consumable medical materials. Bio plasticizer producers including BASF, Evonik, and Cargill that can supply DEHP-free, pharmacopoeia-compliant citrate and ESBO grades are best positioned to capture this premium demand stream, which is growing faster than the overall bio plasticizers market.

Category-wise Analysis

Product Type Insights

Epoxidized Soybean Oil (ESBO) commands the leading share of approximately 41% of the global bio plasticizers market by product type in 2026, reflecting its entrenched position as the lowest-cost, most widely commercialized bio-based plasticizer and heat stabilizer co-plasticizer across flexible PVC food packaging, flooring, and wire insulation applications. ESBO's dominance is underpinned by its dual functionality as both plasticizer and PVC thermal stabilizer, reducing total additive system cost, and its broad compliance approval under EU Regulation (EC) No 10/2011 for food contact materials and FDA 21 CFR in the United States.

Cargill, Dow, and ACS Technical Products are established ESBO producers, with U.S. and Chinese soybean oil supply chains providing scale and cost advantage. ESBO's leadership is stable in volume terms, though share erosion is expected in premium applications such as castor oil-based and citrate ester grades capture higher-value market positions. The fastest growing product type is Castor Oil-Based Plasticizers, projected at 11% CAGR through 2033, driven by superior technical performance in automotive, medical, and high-performance cable applications, and advantaged by India's dominant global castor oil supply position.

Industry Insights

Packaging is the leading segment with approximately 29% of global bio plasticizer demand in 2026, driven by the massive and structurally growing global flexible packaging market, in which flexible PVC films, pouches, and wraps represent a major application platform, and the accelerating regulatory and brand owner pressure to transition away from phthalate-plasticized formulations in food-contact materials. The EU Packaging and Packaging Waste Regulation (PPWR), finalized in 2024, prioritizes recyclability and bio-based content in packaging materials, directly mandating the evaluation of bio-based plasticizer alternatives by packaging film producers supplying European markets.

The Flexible Packaging Association (FPA) confirms sustained growth in flexible packaging consumption globally, with food and beverage segments representing the highest-volume demand contributors. Brand owner sustainability mandates from Nestlé, Unilever, and PepsiCo further reinforce bio plasticizer adoption in food-contact packaging supply chains. The fastest growing Industry is Healthcare, driven by the accelerating regulatory-mandated transition away from DEHP-plasticized PVC in medical devices, expanding global healthcare infrastructure investment, and the growing demand for bio-based and non-phthalate-compliant flexible PVC formulations in IV bags, blood containers, and enteral feeding devices.

Regional Analysis

North America Bio Plasticizers Market Trends and Insights

North America leads the global bio plasticizers market with approximately 36% share in 2026, underpinned by stringent CPSIA, EPA, and FDA phthalate restrictions, a mature ESBO production base anchored in U.S. soybean processing, and a large consumer goods and packaging industry committed to bio-based materials sourcing. The region leads globally in bio plasticizer R&D investment and commercialization of novel citrate and succinic acid-based grades.

U.S. Bio Plasticizers Market Size

The United States accounts for approximately 82% of North America's bio plasticizers market in 2026, driven by its world-leading ESBO production from domestic soybean oil, CPSIA phthalate restrictions in consumer products, and the concentration of major bio-based chemical innovators including Cargill, Dow, and Avient Corporation. Growth through 2033 will be led by healthcare-grade and food packaging bio plasticizer adoption.

Europe Bio Plasticizers Market Trends and Insights

Europe holds approximately 27% of the global bio plasticizers market in 2026, representing the most advanced regulatory environment for phthalate substitution globally. The EU REACH SVHC authorization framework, PPWR, and Green Deal policy architecture collectively accelerate bio plasticizer adoption across packaging, medical, and construction applications. Germany, France, and the U.K. represent the region's core demand markets, with a strong bio-economy manufacturing base supporting domestic supply.

Germany Bio Plasticizers Market Size

Germany represents approximately 26% of Europe's bio plasticizers market in 2026, driven by its leading position in flexible PVC compounding, automotive components, and packaging manufacturing. BASF SE and Evonik Industries are the dominant domestic bio plasticizer producers, with significant R&D investment in citrate ester and succinic acid-based grades. Germany's bio plasticizer market is forecast to grow steadily through 2033, supported by EU REACH compliance mandates.

U.K. Bio Plasticizers Market Size

The U.K. contributes approximately 17% of Europe's bio plasticizers market in 2026, with demand concentrated in food packaging, medical device manufacturing, and consumer goods. Post-Brexit UK REACH alignment with EU phthalate restrictions sustains the substitution dynamic. The U.K.'s strong pharmaceutical and medtech cluster, particularly in Ireland and Scotland, drives growing healthcare-grade bio plasticizer demand. Growth is forecast to be steady through 2033.

France Bio Plasticizers Market Size

France holds approximately 15% of Europe's bio plasticizers market in 2026, supported by Roquette Frères' leading global position in citrate ester and succinic acid bio plasticizer production at its Lestrem facility. France's strong food processing and pharmaceutical industries generate above-average demand for food-contact-compliant and medical-grade bio plasticizers. Growth is forecast to continue at above-European-average rates through 2033 as citrate ester adoption expands.

Asia Pacific Bio Plasticizers Market Trends and Insights

Asia Pacific is the fastest growing bio plasticizers region, forecast to expand at approximately 11.2% CAGR through 2033, driven by rapidly maturing environmental chemical regulation in China, South Korea, and Japan, combined with India's strategic advantage as the world's dominant castor oil producer. China is advancing domestic bio plasticizer production capacity as its Measures for Environmental Management of New Chemical Substances regulation tightens phthalate use across consumer goods and packaging applications. The region represents the largest volume opportunity for bio plasticizer market participants over the forecast horizon.

India Bio Plasticizers Market Size

India accounts for approximately 14% of Asia Pacific's bio plasticizers market in 2026, with a structurally unique advantage: India supplies 80–90% of global castor oil, enabling domestic producers including Emery Oleochemicals and Goldstab Organics to develop integrated castor-to-plasticizer value chains. Growing healthcare infrastructure and tightening phthalate restrictions in consumer goods are accelerating domestic bio plasticizer adoption. India's market trajectory through 2033 is strongly positive.

Japan Bio Plasticizers Market Size

Japan holds approximately 12% of Asia Pacific's bio plasticizers market in 2026, characterized by rigorous phthalate regulation under the Japan Chemical Substances Control Law and strong demand from food packaging and medical device sectors for citrate ester and ESBO grades. DIC Corporation is a key domestic bio plasticizer producer. Japan's bio plasticizers market is growing steadily, with premium healthcare and food-contact applications leading demand through 2033.

Southeast Asia Bio Plasticizers Market Size

Southeast Asia contributes approximately 10% of Asia Pacific's bio plasticizers market in 2026, with growth concentrated in Malaysia, Vietnam, and Indonesia, geographies benefiting from expanding consumer goods manufacturing and food processing sectors. Palm oil-derived bio plasticizer feedstock availability in Malaysia and Indonesia offers a regional supply chain advantage. The sub-region is forecast to grow at above-regional-average rates through 2033 as environmental regulation tightens.

Competitive Landscape

The global bio plasticizers market is moderately fragmented, with a tier of large integrated specialty chemical companies, BASF SE, Cargill, Evonik Industries, Dow, and Lanxess, competing alongside specialized bio-based chemical producers including Roquette Frères, Emery Oleochemicals, and Matrìca S.p.A.

Key competitive differentiators include feedstock integration (soybean, castor, palm oil), application-specific technical performance data packages, regulatory compliance documentation across multiple jurisdictions, and sustainability certifications including ISCC PLUS and RSPO. Dominant strategic themes include bio-attributed product lines, agricultural offtake partnership formation, and expansion of healthcare and food-grade product portfolios to capture premium pricing.

Key Developments

- In March 2025, Roquette Frères expanded commercial production of its Citrofol citrate ester bio plasticizer range at its Lestrem, France facility, targeting growing demand from medical device and food-contact flexible PVC applications requiring SVHC-compliant and pharmacopoeia-certified formulations across European markets.

- In November 2024, Cargill, Incorporated announced an expansion of its Vikoflex ESBO bio plasticizer production capacity in the United States, citing growing demand from food packaging film producers transitioning away from phthalate plasticizers under FDA and EU REACH compliance requirements.

- In June 2024, BASF SE launched a bio-attributed version of its Hexamoll DINCH non-phthalate plasticizer under its biomass balance program certified to ISCC PLUS standards, enabling customers in medical device and toy manufacturing to source a drop-in sustainable plasticizer with verified renewable carbon content.

Global Bio Plasticizers Market – Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 1.8 billion |

|

Current Market Value (2026) |

US$ 3.1 billion |

|

Projected Market Value (2033) |

US$ 5.9 billion |

|

CAGR (2026–2033) |

9.5% |

|

Leading Region |

North America, ~36% market share (2026) |

|

Dominant Product Type |

Epoxidized Soybean Oil (ESBO), ~41% share (2026) |

|

Top-Ranking Industry |

Packaging, ~29% share (2026) |

|

Incremental Opportunity |

US$ 2.8 billion (Absolute Dollar Opportunity) |

Companies Covered in Bio Plasticizers Market

- Avient Corporation

- BASF SE

- Cargill, Incorporated

- DIC Corporation

- Dow, Inc.

- Evonik Industries AG

- LANXESS

- Solvay

- ACS Technical Products

- Emery Oleochemicals

- Matrìca S.p.A.

- Roquette Frères

- Zhejiangjiaao Enprotech Stock Co., Ltd.

- GRUPO PRINCZ IPASA

- Goldstab Organics Pvt. Ltd.

Frequently Asked Questions

The market is estimated to be valued at US$ 2.8 Bn in 2025.

Rising demand for bio-based and non-toxic plasticizers in the medical sector is the key demand driver.

In 2025, North America dominates the global market with a 30.1% share

Among types, the preference for Epoxidized Soybean Oil (ESBO) segment is expected to grow rapidly at 9.7% CAGR from 2025-2032.

BASF SE, Evonik Industries AG, Dow Inc., Lanxess AG, Eastman Chemical Company, and PolyOne Corporation are the leading players in the market.