- Semiconductor Materials & Components

- Organic Substrate Packaging Material Market

Organic Substrate Packaging Material Market Size, Share, and Growth Forecast, 2026 - 2033

Organic Substrate Packaging Material Market by Package Type (SO (Small Outline) Packages, GA (Grid Array) Packages, Others), Application (Consumer Electronics, Automotive, Others), Material Type, and Regional Analysis for 2026 - 2033

Organic Substrate Packaging Material Market Size and Trends Analysis

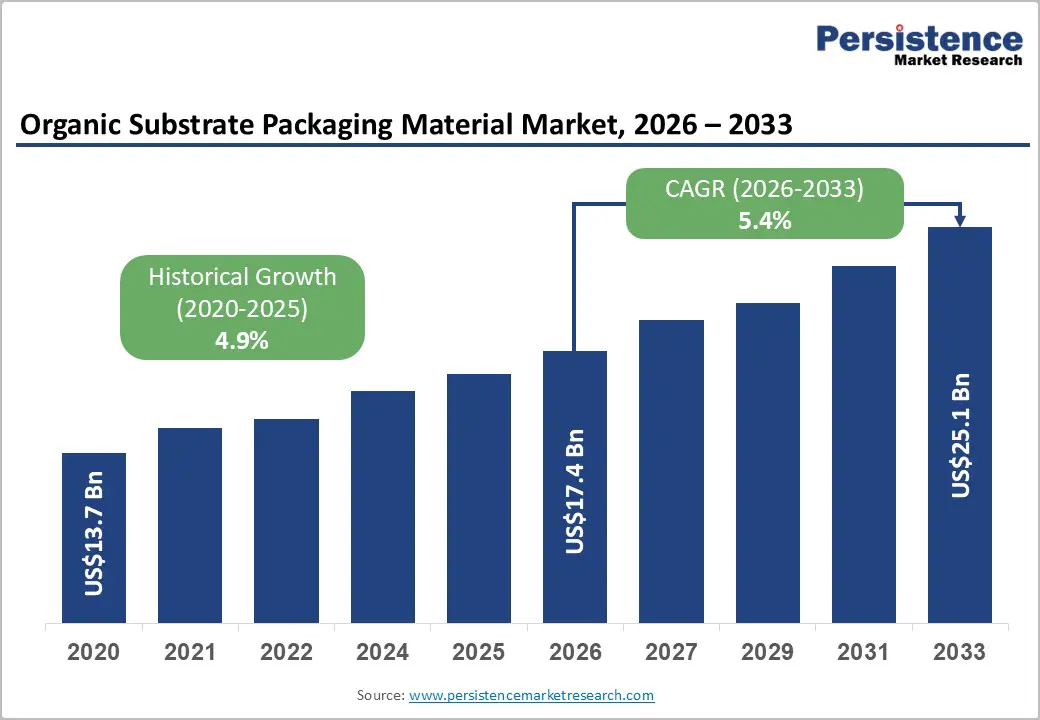

The global organic substrate packaging material market size is likely to be valued at US$17.4 billion in 2026 and is expected to reach US$25.1 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by the rapid adoption of artificial intelligence (AI), high-performance computing (HPC), electric vehicles (EVs), advanced driver-assistance systems (ADAS), and 5G communication infrastructure.

Increasing semiconductor complexity and growing demand for advanced packaging technologies are driving the need for high-performance organic substrate materials capable of supporting improved thermal management, signal integrity, and miniaturization requirements.

Key Industry Highlights:

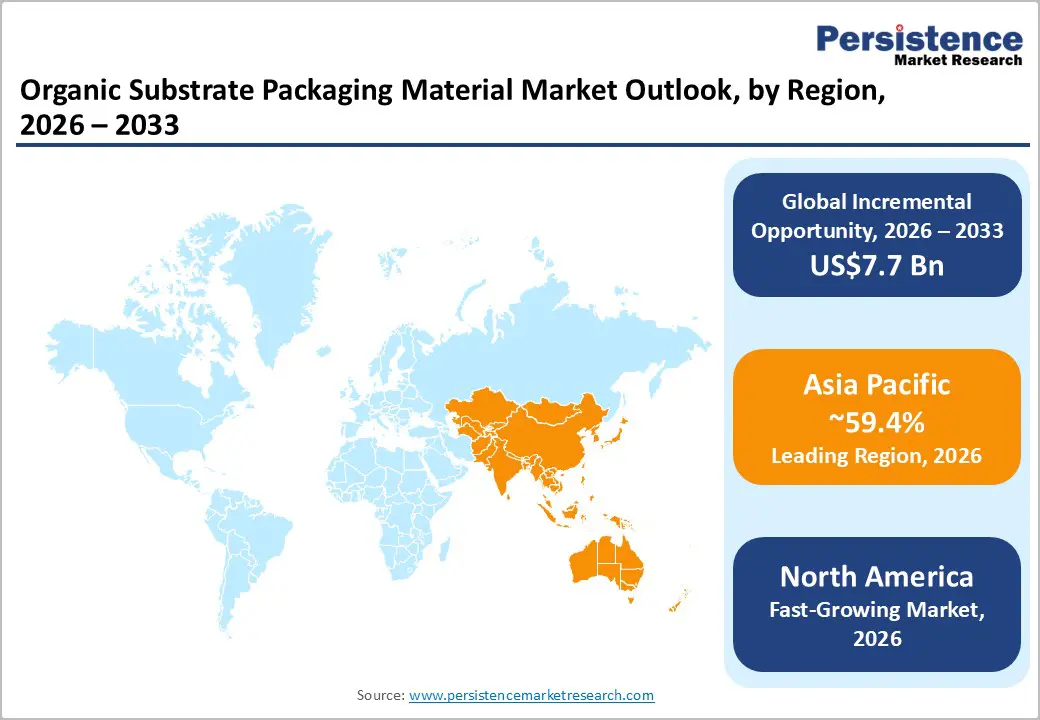

- Leading Region: Asia Pacific is projected to account for approximately 59.4% of the market share in 2026, supported by its dominance in semiconductor manufacturing, advanced packaging capacity, and electronics production.

- Fastest-Growing Region: North America is projected to register the highest growth rate through 2033, driven by semiconductor localization initiatives, AI infrastructure investments, advanced packaging expansion, and growing demand from hyperscale data centers.

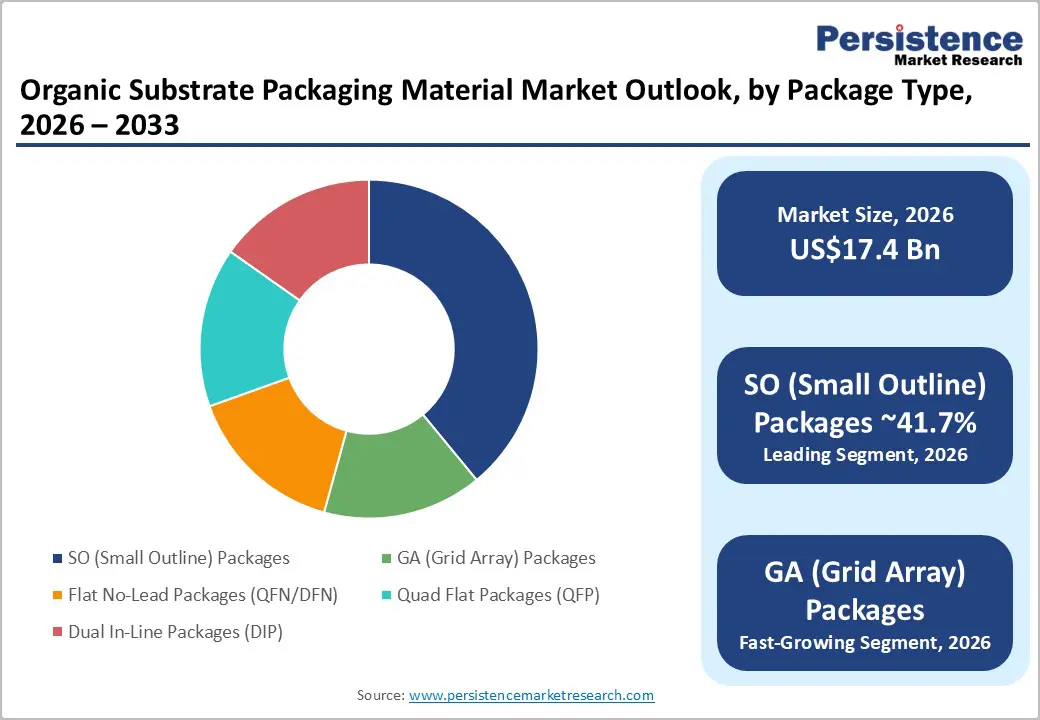

- Dominant Package Type: SO (Small Outline) packages are expected to hold approximately 41.7% market share in 2026, supported by widespread use in consumer electronics, industrial equipment, communication devices, and cost-sensitive semiconductor applications.

- Leading Application: Consumer electronics is anticipated to account for approximately 45.6% of market revenue in 2026, driven by sustained demand for smartphones, PCs, tablets, wearables, gaming systems, and smart home devices.

DRO Analysis

Driver - Rising Demand for AI, HPC, and Advanced Semiconductor Packaging

The accelerating deployment of AI servers, data centers, cloud computing infrastructure, and high-performance computing systems is significantly increasing demand for advanced semiconductor packaging solutions. Modern AI processors and graphics processing units require substrates with higher layer counts, finer circuit patterns, improved thermal characteristics, and greater electrical performance.

As semiconductor manufacturers transition toward chiplet architectures and advanced packaging formats such as FC-BGA, substrate materials have become increasingly critical for ensuring signal integrity and power efficiency. Leading packaging manufacturers are investing heavily in next-generation substrate technologies to support increasingly complex processor designs. This trend is elevating substrate materials from a supporting component to a strategic technology enabler, driving revenue growth across the organic substrate packaging ecosystem.

Expansion of EV Electronics, ADAS Systems, and 5G Infrastructure

The growing penetration of electric vehicles and advanced automotive electronics is creating substantial demand for organic substrate packaging materials. Modern EVs contain significantly more semiconductor content than traditional internal combustion vehicles, including power management systems, battery management units, radar modules, sensors, infotainment systems, and autonomous driving platforms.

Simultaneously, global 5G network deployments continue to accelerate investments in base stations, networking equipment, edge computing devices, and telecommunications infrastructure. These applications require highly reliable substrate materials capable of supporting advanced integrated circuits under demanding operating conditions. The diversification of demand across automotive, industrial, and telecommunications sectors is reducing dependence on consumer electronics and creating a more resilient long-term growth environment for substrate manufacturers.

Restraint - High Capital Requirements and Advanced Manufacturing Barriers

The organic substrate packaging material market remains highly capital intensive, particularly within advanced substrate manufacturing segments. Production facilities require substantial investments in precision equipment, cleanroom infrastructure, quality control systems, and process development capabilities.

New market entrants face extended qualification periods, strict customer approval requirements, and significant yield management challenges. Advanced packaging applications demand extremely low defect rates and consistent performance characteristics, creating high operational barriers. Furthermore, supply chain concentration among a limited number of qualified suppliers increases competitive pressure while limiting opportunities for smaller manufacturers. These factors collectively restrain market entry and can slow capacity expansion during periods of strong demand growth.

Opportunity - Next-Generation Materials for AI and Chiplet Architectures

The transition toward larger semiconductor packages, advanced chiplet integration, and high-bandwidth computing systems is creating opportunities for next-generation substrate materials. Innovations involving low-coefficient-of-thermal-expansion (low-CTE) materials, advanced build-up films, hybrid substrate structures, and glass-core technologies are attracting significant industry attention.

As semiconductor manufacturers seek higher package densities and improved thermal performance, demand for advanced substrate materials capable of supporting increasingly sophisticated architectures is expected to rise. Suppliers that successfully develop solutions addressing warpage reduction, thermal management, and signal transmission challenges are likely to secure long-term partnerships with leading semiconductor manufacturers.

Regional Supply Chain Localization and Manufacturing Expansion

Governments across North America, Europe, and Asia are actively supporting semiconductor manufacturing localization initiatives. Investments in semiconductor fabrication, assembly, testing, and advanced packaging facilities are creating new opportunities for substrate material suppliers.

The emphasis on supply chain resilience and regional manufacturing capabilities is encouraging semiconductor companies to diversify sourcing strategies and establish local supplier networks. As advanced packaging capacity expands globally, substrate manufacturers capable of supporting regional production ecosystems will benefit from new customer relationships, long-term supply agreements, and increased investment opportunities.

Category-wise Analysis

Package Type Insights

SO packages are anticipated to account for 41.7% of the market share in 2026, maintaining their leadership due to widespread adoption across consumer electronics, industrial control systems, and communication devices. Their standardized design, cost efficiency, and established manufacturing ecosystem make them a preferred choice for high-volume semiconductor packaging applications. For example, SO packages are extensively used in memory chips, power management ICs, and microcontrollers found in smartphones, home appliances, and consumer electronics.

GA packages are expected to register the fastest growth. Demand is being driven by increasing deployment of AI processors, high-performance computing systems, networking equipment, and advanced automotive electronics. Their superior thermal performance and higher input/output density make them suitable for applications such as AI accelerators, server processors, graphics processing units (GPUs), and advanced driver-assistance systems (ADAS), supporting continued market expansion.

Application Insights

Consumer electronics are anticipated to account for 45.6% of market revenue in 2026, making them the largest application segment. Strong demand for smartphones, laptops, tablets, wearable devices, gaming consoles, and smart home products continues to drive substrate consumption. Rising semiconductor content per device and growing adoption of advanced packaging technologies are increasing substrate requirements. Products such as premium smartphones, AI-enabled PCs, and high-performance gaming devices remain key demand contributors.

The automotive segment is projected to grow, driven by the rapid expansion of electric vehicles, autonomous driving technologies, and connected vehicle platforms. Modern vehicles increasingly rely on semiconductor-intensive systems, including battery management systems, radar modules, infotainment units, and ADAS controllers. The growing production of EVs and software-defined vehicles is expected to significantly increase demand for advanced organic substrate packaging materials.

Regional Insights

North America Organic Substrate Packaging Material Market Trends

North America is anticipated to be the fastest-growing regional market during the forecast period, supported by increasing investments in semiconductor manufacturing, advanced packaging technologies, AI infrastructure, and cloud computing. The region benefits from strong government support for domestic semiconductor production and growing demand from hyperscale data centers, defense electronics, and next-generation telecommunications networks.

U.S. Organic Substrate Packaging Material Market Trends

The U.S. is set to dominate the North America market due to its leadership in semiconductor design, AI computing, cloud infrastructure, and advanced packaging innovation. Major investments in domestic semiconductor fabrication and packaging facilities are strengthening the regional supply chain. Growing deployment of AI accelerators, high-performance computing systems, and data center processors continues to drive demand for advanced organic substrate materials.

Canada Organic Substrate Packaging Material Market Trends

Canada is emerging as a supportive market through investments in semiconductor research, advanced manufacturing, and telecommunications infrastructure. Increasing adoption of AI technologies and growing participation in North American semiconductor supply chains are expected to create additional opportunities for substrate material suppliers.

Europe Organic Substrate Packaging Material Market Trends

Europe remains an important market for organic substrate packaging materials, supported by strong automotive manufacturing, industrial automation, aerospace, and telecommunications industries. Regional initiatives aimed at strengthening semiconductor production capabilities and reducing supply chain dependence are encouraging investments in advanced packaging technologies.

Germany Organic Substrate Packaging Material Market Trends

Germany leads the Europe market due to its advanced manufacturing ecosystem and position as the region's largest automotive producer. Rising adoption of electric vehicles, autonomous driving technologies, and industrial automation solutions continues to increase demand for semiconductor packaging materials.

U.K. Organic Substrate Packaging Material Market Trends

The U.K. is expanding its semiconductor research and innovation capabilities while increasing investments in digital infrastructure and advanced electronics. Growth in telecommunications networks, data centers, and next-generation computing applications supports market expansion.

France Organic Substrate Packaging Material Market Trends

France is strengthening its position through semiconductor development programs, EV adoption initiatives, and investments in high-tech manufacturing. Growing demand from automotive electronics and industrial applications is supporting substrate material consumption.

Spain Organic Substrate Packaging Material Market Trends

Spain is benefiting from increasing investments in digital transformation, renewable energy technologies, and telecommunications infrastructure. The country's expanding electronics manufacturing sector is expected to contribute to steady market growth.

Asia Pacific Organic Substrate Packaging Material Market Trends

Asia Pacific is anticipated to account for approximately 59.4% of market revenue in 2026, making it the dominant regional market. The region serves as the global hub for semiconductor manufacturing, electronic component production, and advanced packaging technologies. Strong supply chain integration, extensive manufacturing capabilities, and continuous technology investments support regional leadership.

China Organic Substrate Packaging Material Market Trends

China is expected to represent approximately 44.6% of Asia Pacific demand in 2026, making it the largest national market in the region. The country's extensive electronics manufacturing base, significant semiconductor investments, and strong domestic consumption continue to drive substrate demand. Rapid expansion of AI infrastructure, electric vehicle production, and 5G deployment further strengthens growth prospects.

Japan Organic Substrate Packaging Material Market Trends

Japan is estimated to account for approximately 16.4% of market demand in 2026, remaining a key supplier of advanced substrate materials and packaging technologies. The country benefits from strong expertise in semiconductor materials, precision manufacturing, and advanced packaging innovation. Demand is supported by automotive electronics, industrial automation, and high-performance computing applications.

South Korea Organic Substrate Packaging Material Market Trends

South Korea plays a critical role in the regional semiconductor ecosystem through its leadership in memory semiconductors, advanced packaging, and consumer electronics manufacturing. Investments in AI chips, data centers, and next-generation semiconductor technologies continue to support substrate material demand.

Taiwan Organic Substrate Packaging Material Market Trends

Taiwan is one of the world's most important semiconductor manufacturing centers and hosts several leading substrate and packaging suppliers. Strong foundry activity, advanced packaging capabilities, and growing demand for AI processors contribute significantly to regional market growth.

India Organic Substrate Packaging Material Market Trends

India is emerging as an attractive semiconductor manufacturing destination due to government incentives, growing electronics production, and increasing investments in semiconductor assembly and packaging facilities. Expanding domestic electronics consumption is expected to create long-term opportunities for substrate suppliers.

Competitive Landscape

The global organic substrate packaging material market exhibits a moderately concentrated structure at the high-performance segment level while remaining fragmented across broader substrate categories. Leading suppliers collectively control a substantial share of advanced substrate production capacity. Competitive advantages are primarily driven by manufacturing expertise, advanced process capabilities, material innovation, customer relationships, and long-term supply agreements with semiconductor manufacturers.

Leading companies in the industry are increasingly focusing on advanced material innovation to enhance product performance and meet evolving technological requirements. To capitalize on the growing demand driven by artificial intelligence and high-performance computing applications, many firms are expanding their production capacities. Geographic diversification and the strengthening of supply chain resilience have also become key priorities, helping companies reduce risks associated with regional disruptions. Strategic partnerships with semiconductor manufacturers are enabling closer collaboration and faster technology development.

Key Industry Developments:

- In September 2025, Samsung Electro-Mechanics showcased its next-generation package substrate portfolio, including glass core substrates, ultra-high-layer substrates, and AI server packaging solutions at KPCA Show 2025, reinforcing its strategy to expand in AI, server, and autonomous driving semiconductor applications.

- In April 2026, Kyocera Corporation announced the commercialization of a breakthrough multilayer ceramic core substrate designed for advanced AI semiconductors, enabling higher-density wiring, reduced package warpage, and improved performance for next-generation data center processors and ASICs.

Companies Covered in Organic Substrate Packaging Material Market

- Unimicron Technology Corp.

- Ibiden Co., Ltd.

- Nan Ya PCB Corporation

- Shinko Electric Industries Co., Ltd.

- AT&S AG

- Samsung Electro-Mechanics Co., Ltd.

- Kinsus Interconnect Technology Corp.

- Ajinomoto Co., Inc.

- Resonac Corporation

- Kyocera Corporation

- TTM Technologies, Inc.

- SIMMTECH Co., Ltd.

- Zhen Ding Technology Holding Limited

- ASE Material Inc.

- Daeduck Electronics Co., Ltd.

- LG Innotek Co., Ltd.

Frequently Asked Questions

The global organic substrate packaging material market is estimated to be valued at US$17.4 billion in 2026.

The organic substrate packaging material market is projected to reach approximately US$25.1 billion by 2033.

Key trends include increasing adoption of AI and high-performance computing (HPC) chips, growing demand for ABF substrates, expansion of advanced packaging technologies, rising semiconductor content in electric vehicles (EVs), and continued deployment of 5G infrastructure worldwide.

SO (Small Outline) Packages are the leading package type segment, anticipated to account for approximately 41.7% of the global market in 2026 due to their widespread use in consumer electronics and industrial applications.

The organic substrate packaging material market is expected to grow at a CAGR of 5.4% between 2026 and 2033.

Major companies include Unimicron Technology Corp., Ibiden Co., Ltd., Nan Ya PCB Corporation, Shinko Electric Industries Co., Ltd., and Samsung Electro-Mechanics.