- Retail

- Nicotine Pouches Market

Nicotine Pouches Market Size, Share, and Growth Forecast 2026–2033

Nicotine Pouches Market by Product Type (Tobacco-Derived Nicotine Pouches, Synthetic Nicotine Pouches, Hybrid Nicotine Pouches, Nicotine-Free Pouches), by Nicotine Strength (Low Strength, Medium Strength, Strong, Extra Strong), by Flavor Type, by Distribution Channel, by Regional Analysis, 2026–2033

Nicotine Pouches Market Share and Trends Analysis

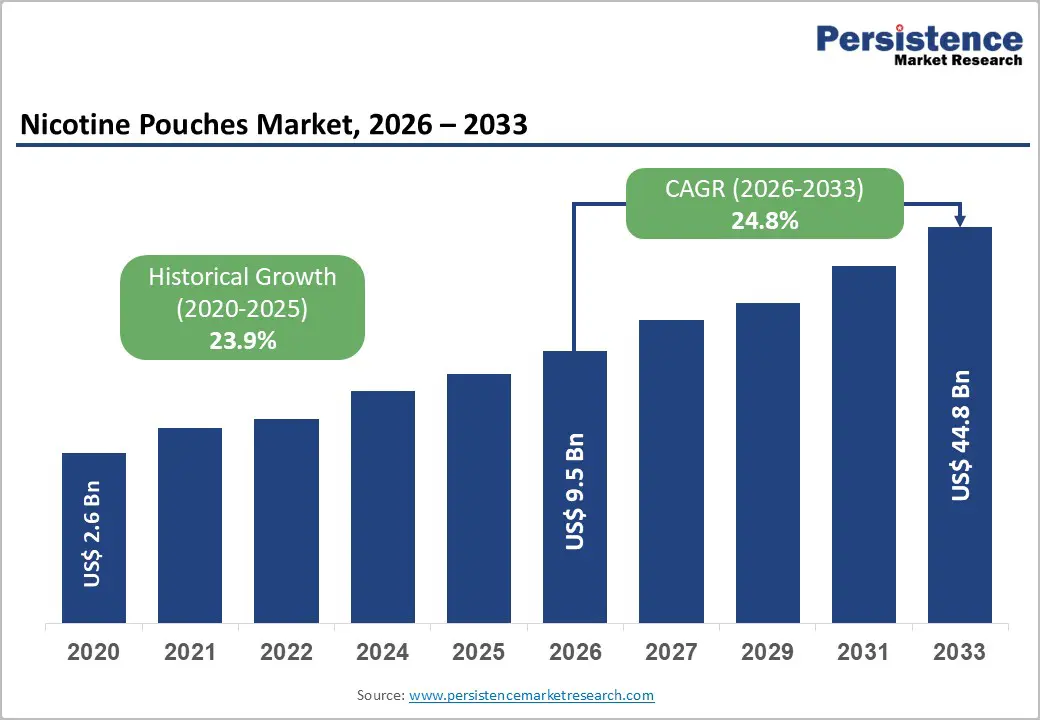

The global nicotine pouches market size is expected to be valued at US$ 9.50 billion in 2026 and is projected to reach US$ 44.79 billion by 2033, growing at a CAGR of 24.8% between 2026 and 2033. This extraordinary growth trajectory reflects a fundamental behavioural shift among adult nicotine consumers, moving decisively away from combustible tobacco products toward tobacco-free, spit-free oral nicotine alternatives.

Key Industry Highlights:

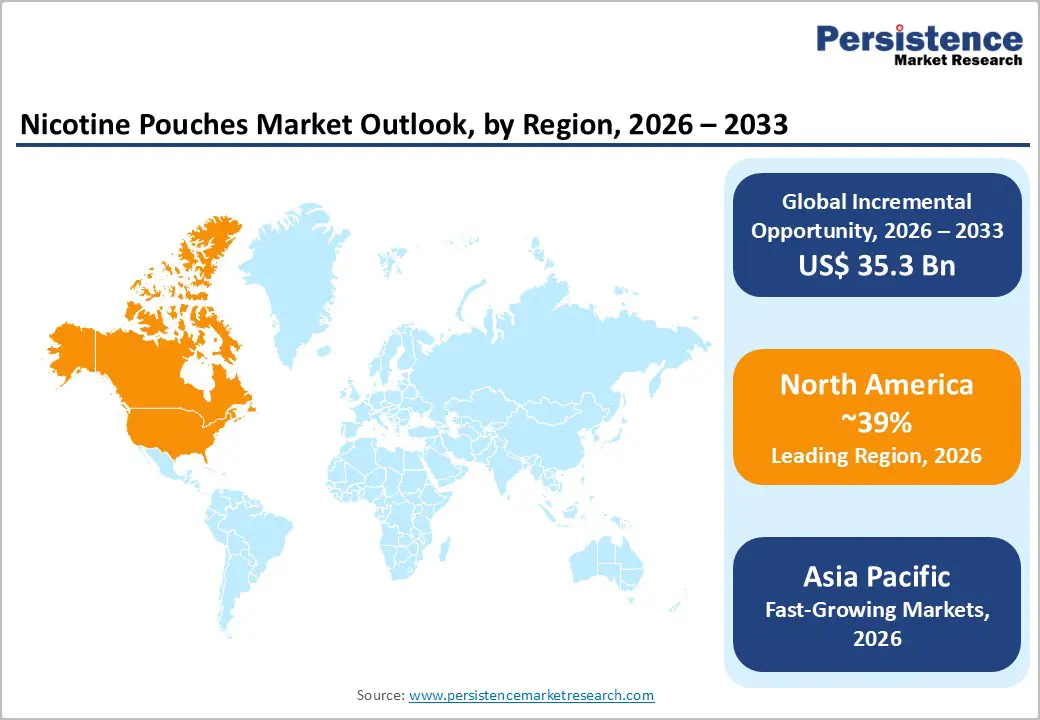

- Leading Region: North America leads the global nicotine pouches market with a 39.0% share (US$ 3.71 Billion in 2026), driven by the FDA's anti-combustible tobacco regulatory actions, a mature convenience retail network, and strong brand investment from multinationals, making it the highest-value commercial priority for manufacturers seeking near-term revenue volume.

- Fastest Growing Region: Asia Pacific is the fastest growing region in the Nicotine Pouches Market, projected to expand at a CAGR of 28.9% by 2033, fuelled by the region's concentration of over half the world's adult smokers, rising disposable incomes, and accelerating urban health consciousness, representing the single largest long-term revenue expansion opportunity in the nicotine pouches space.

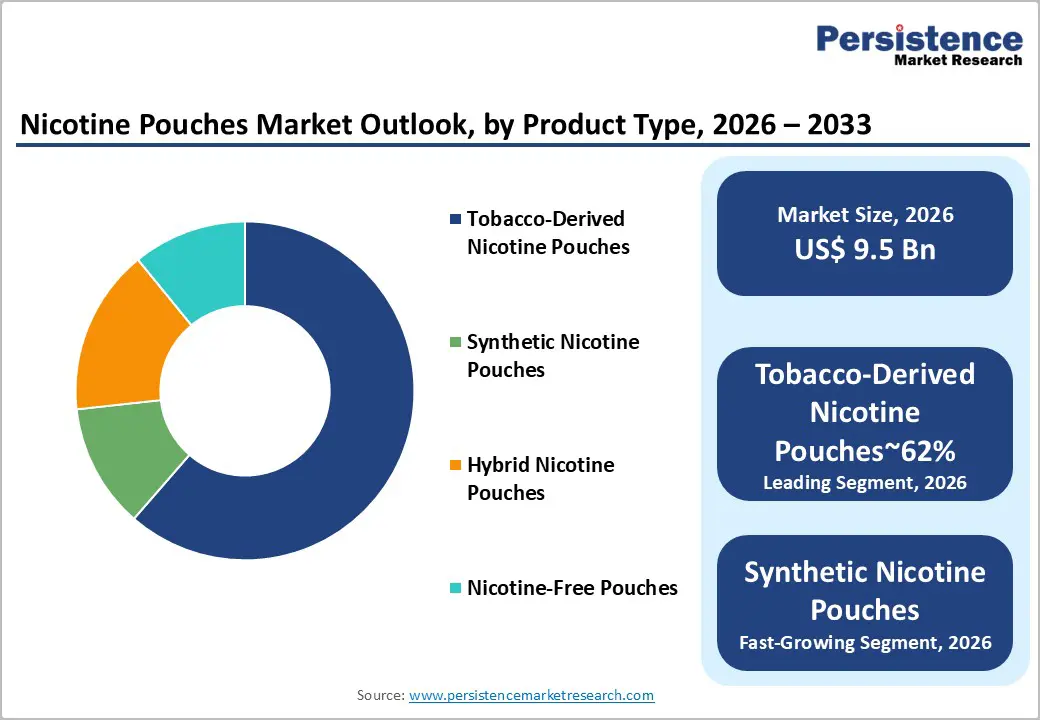

- Leading Segment: Tobacco-derived nicotine pouches dominate product type segmentation with a 62.0% share, underpinned by cost-effective manufacturing, supply chain maturity, and established regulatory precedent in key markets, a structural advantage that will sustain category leadership through the medium term while synthetic formats scale.

- Fastest Growing Segment: Synthetic nicotine pouches are the fastest growing product segment, accelerating due to consumer demand for tobacco-free credentials, declining production costs, and evolving regulatory frameworks that increasingly accommodate synthetic nicotine as a distinct, legitimised category, making it the highest-priority innovation investment for brands targeting younger demographics.

- Key Opportunity: Emerging market expansion represents the most time-sensitive opportunity in the nicotine pouches market, as Southeast Asia, Latin America, and Sub-Saharan Africa collectively host over 60% of global smokers yet remain significantly underpenetrated, early-mover brands that establish local regulatory relationships and affordable SKU strategies now will lock in distribution advantages before multinational competition intensifies.

Market Dynamics

Drivers - Accelerating Regulatory Pressure on Combustible Tobacco Products Redirects Consumer Demand

The global regulatory tightening around combustible cigarettes, which is actively pushing millions of adult smokers toward cleaner alternatives. Governments across North America, the European Union, and the Asia Pacific region have implemented progressively stricter plain packaging laws, flavour bans on cigarettes, and accelerated taxation schedules on combustible tobacco, all of which erode the consumer value proposition of traditional smoking.

Rising Consumer Preference for Discreet, Tobacco-Free Nicotine Delivery

What drives growth in the nicotine pouches market beyond regulation is an independently motivated lifestyle shift, consumers increasingly demand nicotine formats that are invisible in social and professional settings. Nicotine pouches require no combustion, produce no smoke or odour, leave no staining, and generate no second-hand exposure, making them uniquely compatible with indoor workplace environments, air travel, and hospitality settings where smoking bans apply.

Based on authenticated consumer research, a growing share of nicotine-pouch users, estimated at over 40% in surveys across Scandinavian markets, report adopting the format primarily for convenience and social discretion rather than harm-reduction motivations alone. This demand diversification broadens the addressable consumer base well beyond ex-smokers into a younger, urban demographic that had never engaged with combustible tobacco in the first place.

Restraints - Complex and Inconsistent Regulatory Classification Across Jurisdictions Creates Market Entry Barriers

One of the most consequential restraints on the Nicotine Pouches Market is the fragmented and, in many cases, contradictory regulatory treatment of nicotine pouches across national jurisdictions. Unlike combustible cigarettes, which operate under well-established frameworks, nicotine pouches occupy a legal grey zone in numerous markets, classified variously as tobacco products, novel nicotine products, food-grade items, or general consumer goods depending on the country.

This inconsistency forces manufacturers to navigate 40% higher compliance cost structures for multi-market launches compared to single-market strategies, according to industry trade association data. In key growth markets including Australia, India, and several Southeast Asian nations, outright bans or pending regulatory reviews actively suppress market formation and suppress the nicotine pouches market forecast from reaching its theoretical potential.

Flavour Restriction Legislation Threatens the Product's Broadest Consumer Appeal Vectors

Flavoured nicotine pouches represent the dominant demand architecture of the category, yet this very strength is under legislative threat in several high-value markets. Regulators in the United States, through FDA (Food and Drug Administration) enforcement actions, have moved to restrict flavoured oral nicotine products by denying or challenging marketing authorisation applications for non-tobacco flavour variants, directly constraining the product portfolio strategies of major manufacturers.

The European Union's evolving position on flavour restrictions under the Tobacco Products Directive revision cycle introduces further uncertainty for brands whose growth projections depend heavily on mint, fruit, and beverage flavour portfolios. For the nicotine pouches industry, this creates a bifurcated competitive risk, the most commercially appealing products face the highest regulatory scrutiny, compressing margin expansion opportunities.

Opportunities - Emerging Market Expansion Offers Disproportionate Long-Term Revenue Upside

Expansion of distribution and building strong brand presence in underpenetrated emerging markets across Southeast Asia, Latin America, and Sub-Saharan Africa as these regions have some of the highest adult smoking population, yet remain largely untapped for nicotine pouches.

Companies that move early to establish retail networks, regulatory relationships, and locally tailored product offerings in countries such as Vietnam, Brazil, Nigeria, and Indonesia can secure strong first-mover advantages before competition intensifies. These regions together represent over 60% of the global adult smoking population but currently contribute only a small portion of nicotine pouch revenues, highlighting a major growth gap. Manufacturers should focus on offering affordable, region-specific products and work closely with health authorities to position nicotine pouches within harm-reduction strategies. Acting early is critical, as the opportunity window is narrowing with rising global interest.

Synthetic Nicotine Innovation Unlocks Regulatory Arbitrage and Brand Differentiation

The shift toward synthetic nicotine presents a strong strategic opportunity in the Nicotine Pouches Market by enabling companies to differentiate their products and navigate regulatory environments more effectively. Unlike traditional nicotine derived from tobacco plants, synthetic nicotine is lab-produced and can, in some markets, fall outside strict tobacco regulations. This also appeals to consumers who prefer “tobacco-free” products for health or lifestyle reasons.

Although the United States brought synthetic nicotine under FDA oversight in 2022, this move has also added credibility and clarity to the category. Consumer research shows that more than 35% of users under 35 prefer tobacco-free labeling, indicating strong demand potential. Companies investing in synthetic nicotine research and supply chains today will gain a competitive advantage in the future. Forming partnerships with pharmaceutical-grade nicotine suppliers can help reduce costs and achieve competitive pricing, making synthetic products more accessible to mainstream consumers.

Category-wise Analysis

Product Type Insights

Tobacco-derived nicotine pouches hold the leading share in the global share accounting for 62.0% of the total market value in 2026, equivalent to US$ 5.89 billion. This dominance is driven by their cost efficiency, established manufacturing processes, and stable supply chains, which allow companies to offer competitive pricing across markets. Additionally, regulatory systems in major regions such as the United States and Europe are already well-defined for tobacco-derived products, providing companies with predictable compliance pathways.

Synthetic nicotine pouches are the fast-growing segment, driven by increasing demand for tobacco-free alternatives and expanding access to pharmaceutical-grade nicotine. Regulatory flexibility in certain markets further supports this growth. While tobacco-derived products will remain dominant in the near term, their share is expected to gradually decline as synthetic nicotine becomes more affordable and widely accepted. Companies should maintain a balanced portfolio to manage this long-term transition effectively.

Nicotine Strength Insights

Medium-strength nicotine pouches lead the market by strength category, accounting for 41.0% of total market share in 2026, valued at approximately US$ 3.90 billion. These products, typically containing 6mg to 10mg of nicotine per pouch, offer the ideal balance between effectiveness and comfort, making them suitable for a wide range of adult consumers. They are particularly popular among individuals transitioning from cigarettes, as they provide sufficient nicotine satisfaction without being too intense.

Consumer data from markets such as Scandinavia and North America consistently shows strong repeat purchase rates for medium-strength products. The strong-strength category, typically ranging from 11mg to 16mg, is the fastest-growing segment, driven by experienced users seeking higher nicotine delivery. Although medium strength will continue to dominate, the increasing demand for stronger products suggests a gradual shift in consumption patterns. Companies should also monitor regulatory developments regarding nicotine limits in key markets.

Flavor Type Insights

Mint and menthol flavors dominate the global nicotine pouches market, holding 44.0% of total market share in 2026, equivalent to US$ 4.18 billion. Their popularity is driven by a clean, refreshing taste that aligns well with consumer expectations of oral products. These flavors are strongly associated with freshness and hygiene, similar to products like toothpaste, chewing gum, and breath mints, making them a natural choice for first-time users. This familiarity helps drive both initial trials and repeat purchases across multiple markets.

However, fruit flavors are emerging as the fastest-growing segment, particularly among younger adult consumers who seek more variety and enjoyable taste experiences. Additionally, regulatory restrictions on menthol in certain regions are encouraging companies to expand their fruit-flavored offerings. While mint and menthol will continue to lead, the overall flavor landscape is becoming more diverse. Companies should balance traditional and innovative flavors to capture wider consumer segments.

Distribution Channel Insights

Offline retail continues to dominate the nicotine pouches market, accounting for 68.0% of total market share in 2026, equivalent to US$ 6.46 billion. This is largely because nicotine pouches are often purchased as quick, routine items from physical stores such as convenience outlets, petrol stations, supermarkets, and tobacconists. These locations support impulse buying and offer easy accessibility, especially in well-established markets like the United States, Sweden, Germany, and Japan.

The existing retail infrastructure for nicotine products provides a strong advantage for offline channels. However, online retail is the fastest-growing distribution channel, supported by increasing adoption of e-commerce, subscription-based models, and improved age-verification systems. Online platforms also offer competitive pricing and wider product availability, attracting a growing number of consumers. Although offline retail will remain dominant in the near term, the gap between offline and online channels is expected to narrow significantly by 2030.

Regional Insights

North America Nicotine Pouches Market Trends and Insights

North America holds 39.0% of the global nicotine pouches market in 2026, valued at US$ 3.71 billion, making it the leading region. Growth is driven by high smoking prevalence, strong retail infrastructure, strict anti-smoking regulations, and brand-conscious consumers. FDA policies and nicotine reduction initiatives will further expand adoption through the forecast period.

- United States Nicotine Pouches Market Size

The United States accounts for 88% of North America’s nicotine pouches market, reaching US$ 3.27 billion in 2026. Growth is supported by adult smokers shifting to alternatives, widespread convenience retail networks, and strong brand performance. Continued FDA pressure on combustible and menthol cigarettes will sustain conversion rates and market expansion through 2033.

Europe Nicotine Pouches Market Trends and Insights

Europe represents 26.0% of the global market in 2026, valued at US$ 2.47 billion, making it the second largest region. Strong adoption stems from familiarity with oral nicotine products, especially in Scandinavia. However, regulatory risks such as nicotine caps and flavour restrictions may constrain growth across European markets during the forecast period.

- Germany Nicotine Pouches Market Size

Germany holds 18% of the European market, reaching approximately US$ 445 million in 2026. Demand is driven by high cigarette consumption and relatively flexible product classification allowing broad retail availability. Increasing health awareness and anti-smoking campaigns are expected to accelerate the shift toward nicotine pouches as an alternative product category.

- United Kingdom Nicotine Pouches Market Size

The United Kingdom accounts for 20% of Europe’s market, valued at US$ 494 million in 2026. A supportive regulatory approach focused on harm reduction and the Smokefree 2030 initiative drives adoption. Additionally, strong e-commerce infrastructure and consumer preference for online purchasing significantly boost nicotine pouch sales across the country.

- France Nicotine Pouches Market Size

France represents 12% of the European market, equating to US$ 296 million in 2026. Growth is supported by high smoking prevalence and rising demand for smoke-free alternatives among urban consumers. Expanding pharmacist distribution channels and EU-aligned regulatory frameworks are expected to gradually increase nicotine pouch penetration in the coming years.

Asia Pacific Nicotine Pouches Market Trends and Insights

Asia Pacific accounts for 29.0% of the global market, valued at US$ 2.75 billion in 2026, and is the fastest growing region. Growth is fueled by large smoker populations, rising incomes, and health awareness. The region is expected to surpass Europe by 2030, driven by strong demand and improving distribution networks.

- China Nicotine Pouches Market Size

China holds 35% of the Asia Pacific market, reaching US$ 963 million in 2026. Demand is driven by its vast smoker base and increasing health awareness among urban populations. Regulatory clarity will be crucial for future growth, with early market entrants likely to gain significant advantages through strong compliance and distribution strategies.

- India Nicotine Pouches Market Size

India represents 20% of the Asia Pacific market, valued at US$ 550 million in 2026. Growth is supported by a large tobacco-using population and rising demand for cleaner alternatives. Regulatory clarity under existing tobacco laws will be a key factor determining whether the market accelerates or experiences slower adoption in the near term.

- Japan Nicotine Pouches Market Size

Japan accounts for 22% of the Asia Pacific market, reaching US$ 605 million in 2026. Demand is driven by strict smoking regulations, social norms discouraging smoking, and strong adoption of alternative nicotine products. A technologically advanced consumer base supports premium and innovative nicotine pouch products, driving continued market growth.

Competitive Landscape

The global nicotine pouches market operates within a moderately consolidated competitive structure at the premium end, where three to five multinational tobacco and next-generation product (NGP) companies command the majority of branded market share, led by Philip Morris International, British American Tobacco, and Altria Group. Below this tier, the competitive field fragments sharply into a diverse ecosystem of regional specialists, direct-to-consumer digital-native brands, and private-label manufacturers.

The primary basis of competition varies meaningfully by tier: multinationals compete on brand equity, distribution scale, and regulatory navigation capability, while challenger brands compete on product innovation, flavour differentiation, and agile e-commerce execution. The most consequential strategic theme shaping the nicotine pouches competitive landscape in 2024–2025 is the race to secure FDA marketing authorisation in the United States, which functions as a de facto market access barrier and quality signal that reshapes consumer and retail buyer preference. Strategic M&A activity is accelerating as large players acquire innovative mid-tier brands to expand their nicotine strength and flavour portfolios rapidly.

Key Developments:

- January, 2025: Philip Morris International completed the full acquisition of Swedish Match and accelerated the international rollout of the ZYN nicotine pouch brand into 15 new markets across Asia Pacific and Latin America, signalling the company's commitment to nicotine pouches as a core pillar of its smoke-free product strategy.

- March, 2024: British American Tobacco announced the commercial expansion of its Velo nicotine pouch range into 8 additional markets in Southeast Asia and Eastern Europe, alongside a new manufacturing investment in Sweden to scale production capacity in response to double-digit demand growth across its international portfolio.

- September, 2024: Altria Group filed expanded premarket tobacco product applications with the FDA for additional flavour variants of its ON! nicotine pouch brand, reflecting a strategic effort to broaden its approved product portfolio and defend share against growing competition from synthetically derived pouch formats entering the US market.

Companies Covered in Nicotine Pouches Market

- British American Tobacco

- Altria Group

- Philip Morris International

- Swedish Match

- Japan Tobacco International

- GN Tobacco Sweden

- Skruf Snus

- Nicopods ehf

- Swisher

- Tobacco Concept Factory

- Imperial Brands

- Turning Point Brands

- Nevcore Innovations

- Nicotobacco Factory

- NGP Empire

- Haypp Group

- Rogue Holdings

- Nicovibes

- Zone X

- Zyn

Frequently Asked Questions

The Nicotine Pouches Market size is valued at US$ 9.50 Billion in 2026 and is projected to reach US$ 44.79 Billion by 2033, growing at a CAGR of 24.8%.

Growth is driven by strict regulations on smoking products and rising consumer preference for discreet, smoke-free, and odorless nicotine alternatives suitable for indoor and socially acceptable usage environments globally.

Tobacco-derived nicotine pouches lead with 62.0% share due to lower costs, established supply chains, and regulatory clarity, though synthetic nicotine is gaining traction as a fast-growing alternative segment.

North America leads with 39.0% share, supported by strong regulations on tobacco products and widespread retail availability, making nicotine pouches easily accessible to a large consumer base.

Key opportunities lie in expanding distribution and brand presence in emerging markets like Southeast Asia, Latin America, and Africa, where high smoking populations remain largely untapped for nicotine pouch adoption.

Leading companies include Philip Morris International, British American Tobacco, and Altria Group. The market is moderately consolidated globally but remains fragmented at regional and smaller player levels.